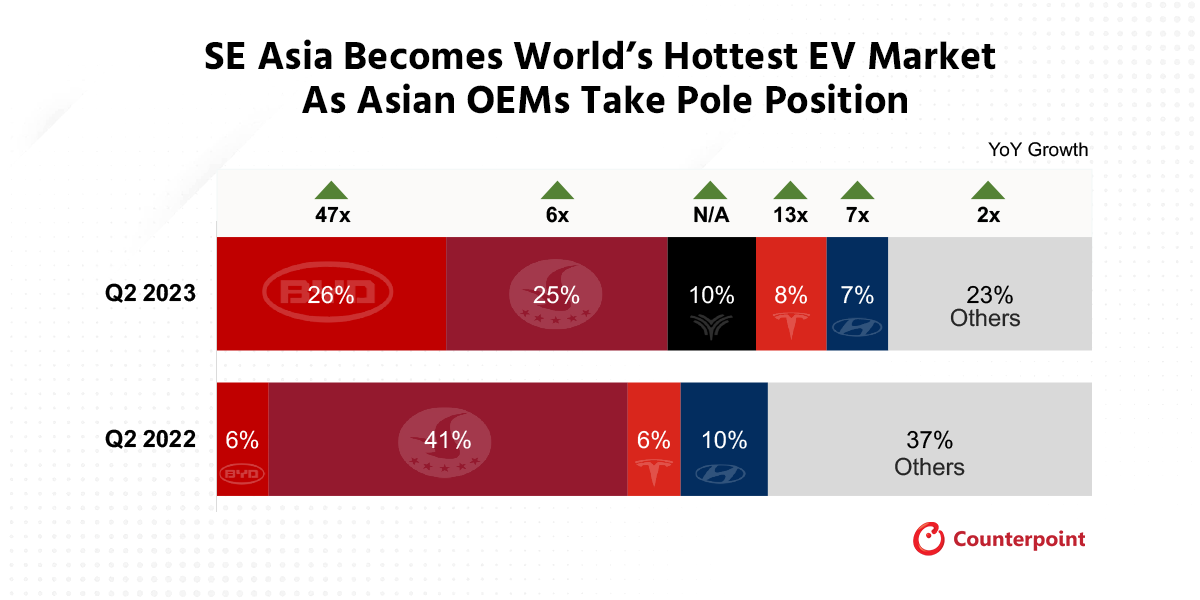

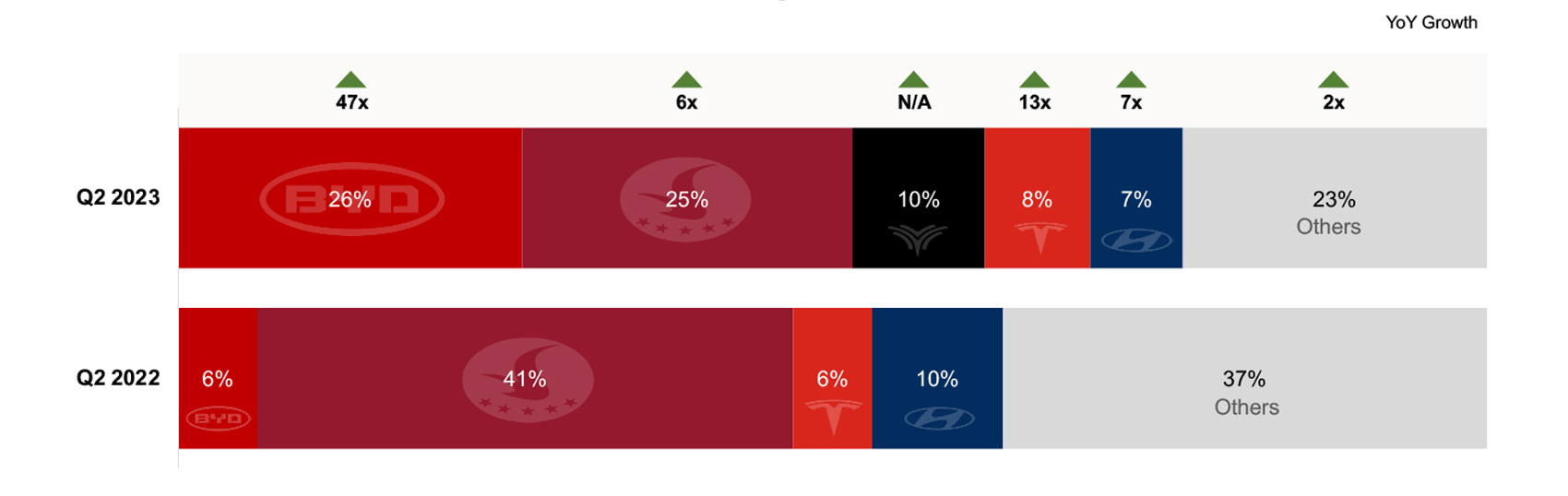

SE Asia was the hottest major EV market globally in Q2, growing nearly 10X YoY driven by key countries in Indochina

BYD took top position in unit sales share followed closely by domestic market favorite Vingroup

Chinese OEMs advanced the most, underscoring strong demand for lower-tier price segments

Hong Kong, Jakarta, New Delhi, London, Boston, Seoul – September 21, 2023

According to Counterpoint Research’s latestSE Asia Passenger Electric Vehicle Tracker, Q2 2023battery electric vehicle (BEV) unit sales in the region grew by 894%, driven by strong demand across Thailand, Vietnam, Indonesia, and Malaysia.

Base effects are in play as markets are very early stage, but significant progress is being made with EV share of overall passenger vehicle sales rising to over 6% during the quarter, with key Asian OEMs capitalizing on strong initial demand.

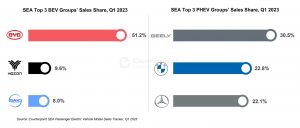

Passenger EV* Unit Sales Share and YoY Growth by Auto Group

Source: Counterpoint Research SE Asia Passenger EV Tracker. *Battery electric vehicles (BEV) only.

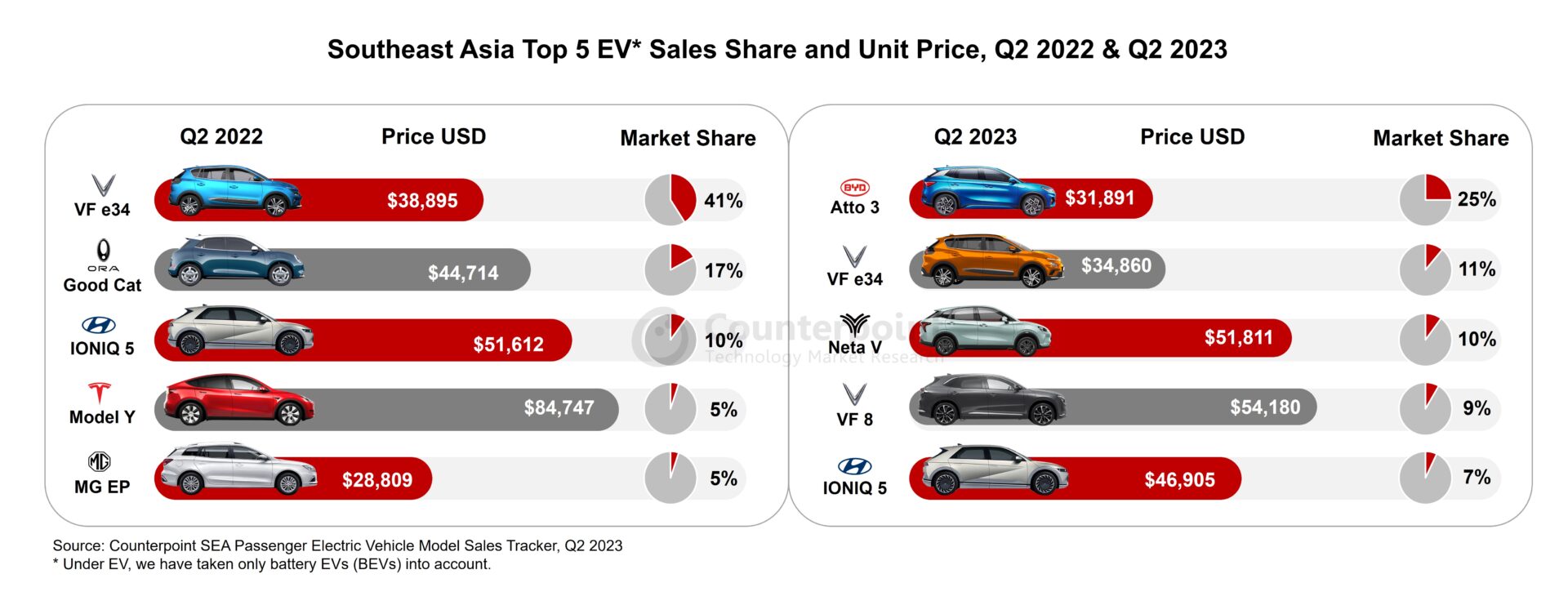

“What we’re seeing is just the beginning with SE Asia’s biggest markets starting to scale. It’s happening as government efforts to promote electrification dovetail with a flurry of products coming online that might not be budget, but are a lot more accessible to more buyers in the region,” saysSoumen Mandal, Senior Analystfor Automotive. “Vietnam and Thailand are great examples, with automakers introducing lower-priced models targeting the broadest range of consumers.”

“The result has been a big decline in prices over the past year as OEMs like Vinfast and BYD introduced cars with better sticker appeal. Comparing the top 5 best sellers YoY, prices have come down over 20%.”

Chinese OEMs are set to become the biggest beneficiary of SE Asia’s appetite for EVs over the short term, and Thailand will be a hot spot as this new breed of automakers sets up shop in the Kingdom – the region’s auto manufacturing hub;traditional players like Toyota are leaving the door open as they falter in the transition to EVs.

“There’s a big window of opportunity especially for someone like BYD, which has enjoyed a massive home market head start,” notesIvan Lam, Senior Analyst对制造业。“规模和端到端基本ring prowess gives it a competitive advantage few EV players can match – affordable cars, robust supply, more frequent product launches. This might not sound exciting in terms of traditional combustion engine vehicles, but in EVs, it’s revolutionary.”

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

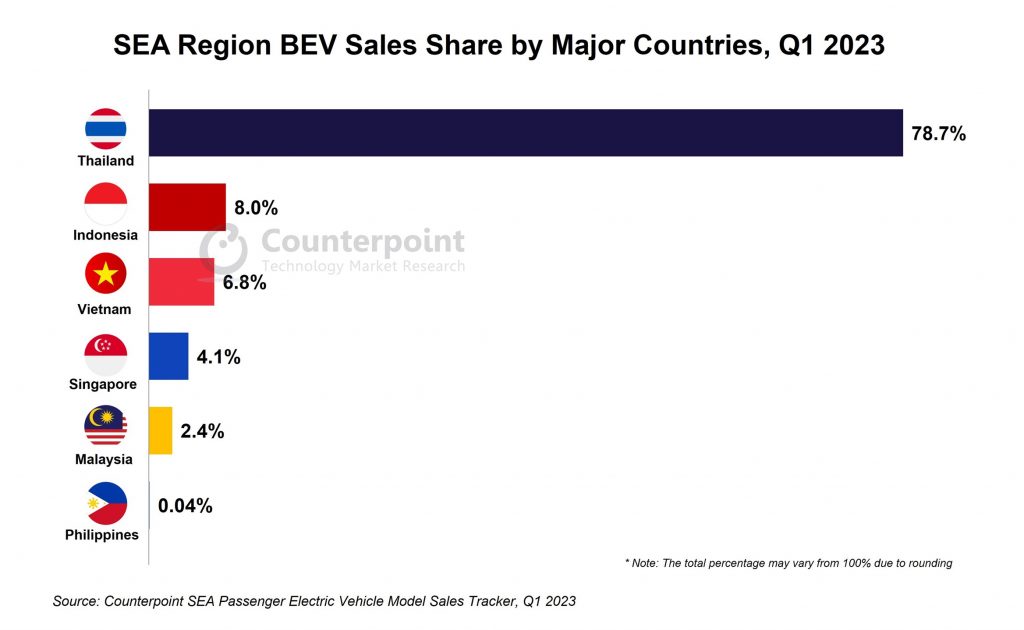

Thailand accounted for over 75% of BEV sales in the SEA region during Q1 2023.

Three out of every four BEVs sold were from a Chinese automaker.

The top three groups accounted for 68% of BEV sales.

BYD’s Atto 3 was the best-selling BEV.

New Delhi,London,San Diego, Buenos Aires, Hong Kong, Beijing, Seoul –July 20, 2023

Southeast Asia’s#(SEA’s) passenger battery electric vehicle (BEV) sales* grew by almost 10 times YoY in Q1 2023, according to the latest research from Counterpoint’sSEA Passenger Electric Vehicle Model Sales Tracker. The share of BEVs in total passenger vehicle sales experienced significant growth in Q1 2023, reaching 3.8% compared to a mere 0.3% one year ago.Thailandemerged as the leading country, capturing over 75% of the BEV sales, followed byIndonesiaandVietnam.Thailandalso boasted the highest proportion of BEVs in total passenger vehicle sales, followed by Singapore and Vietnam. However, plug-in hybrid electric vehicle (PHEV) sales saw a modest YoY growth of 5.8%.

Commenting on the market dynamics,Research Analyst Abhilash Guptasaid, “Thailand’s government-led efforts to promote EV sales have yielded positive outcomes, while Indonesia and Vietnam are also performing well in the region. However, Malaysia, Philippines and Myanmar require additional regulatory support and encouragement to foster EV growth. Despite overall passenger vehicle sales remaining relatively stagnant, the sales of BEVs have experienced a significant andrapid expansion. Besides, the market for hybrid electric vehicles (HEVs) has experienced remarkable growth in SEA, playing a pivotal role in the transition from traditional internal combustion engine (ICE) vehicles to EVs.”

Gupta added, “Chineseauto groups are experiencing rapid growth and outpacing their competitors in the SEA region, with their market share increasing from 38% a year ago to nearly 75%. In Q1 2023,BYD Groupemerged as the BEV leader in the SEA region, capturing the majority of sales, followed byHozon New Energy, andSAIC Group. These top three groups collectively accounted for over 68% of the BEV market. In the PHEV market,Geely Holding Groupclaimed the top position, followed byBMW Group, andMercedes-Benz Group.”

BYD’s Atto 3 was the best-selling BEV across SEA, followed by the Neta V and Tesla Model Y. In PHEVs, Volvo’s XC60 sold the most, followed by the BMW 3 series and Mercedes-Benz E-Class.

Commenting on the market outlook,Senior Analyst Soumen Mandalsaid, “In addition to offering subsidies and tax incentives, Thailand’s government has set ambitious goals to position itself as a global hub for EV production. The country’s EV sector has witnessed a significant rise in foreign direct investment (FDI) in the past year. Notably, several Chinese automakers, including Great Wall Motors, BYD, Hozon New Energy and Changan Automobile, have shown interest in establishing or have already commenced the construction of production facilities inThailand. Similarly,Indonesiaannounced a subsidy package in March 2023 to promote the purchase and manufacturing of EVs, with a special focus on increasing local production. This move is expected to further accelerate the production and sales of EVs in the region.”

Mandal added, “The Chinese presence in the SEA EV market is poised to strengthen as they establish regional manufacturing bases, thereby driving further growth in the EV sector. The overall sales of EVs are experiencing an upward trajectory in the SEA region. The outlook appears promising, and there is an expectation that the share of BEVs in total vehicle sales will reach6%by the end of this year.”

*Sales refer to wholesale figures, i.e. deliveries from factories by the respective brands/companies.

#SEA here includes Indonesia, Malaysia, Myanmar, Philippines, Singapore, Thailand and Vietnam.

Feel free to reach us at press@www.arena-ruc.com for questions regarding our latest research and insights.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

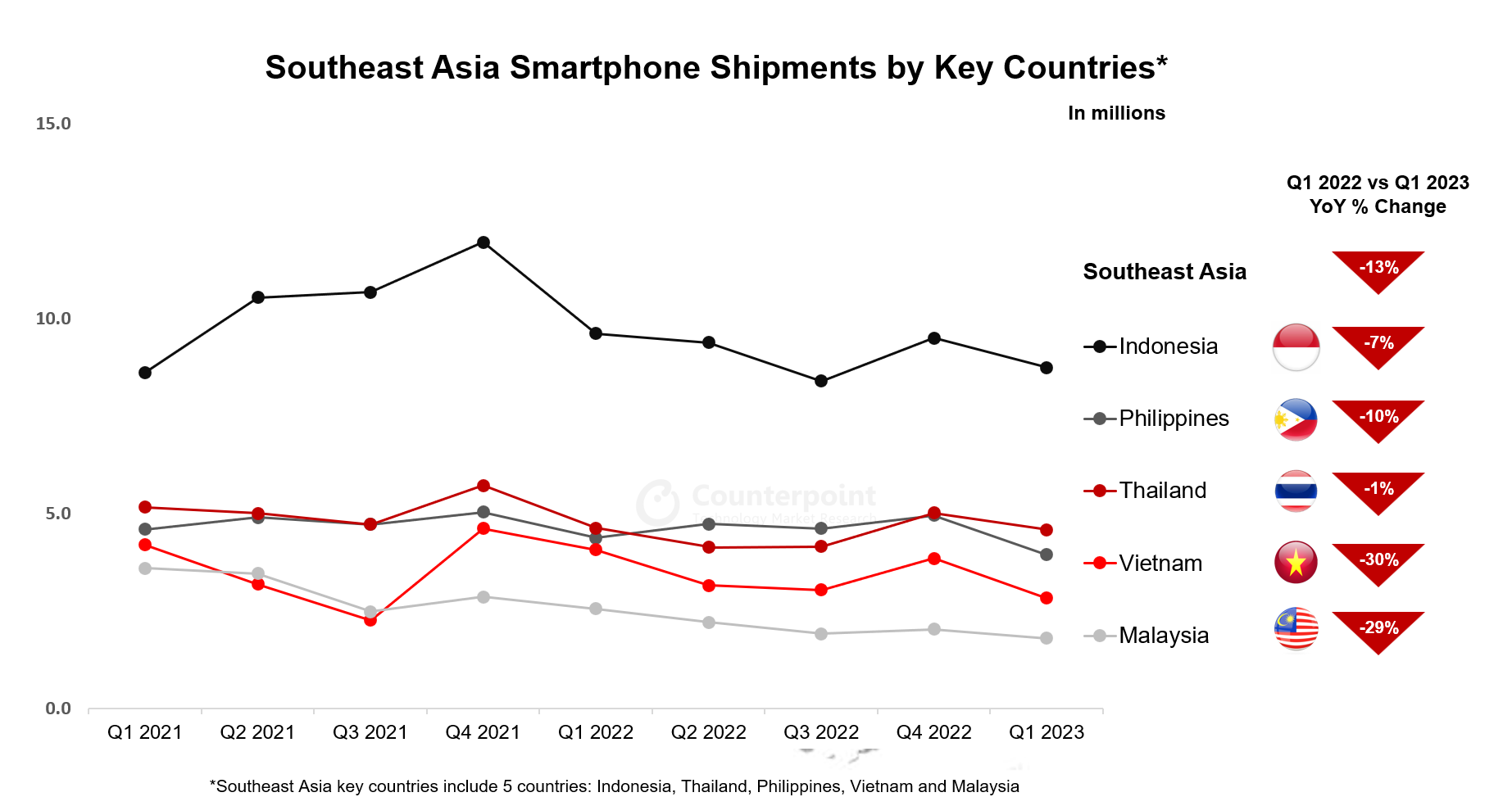

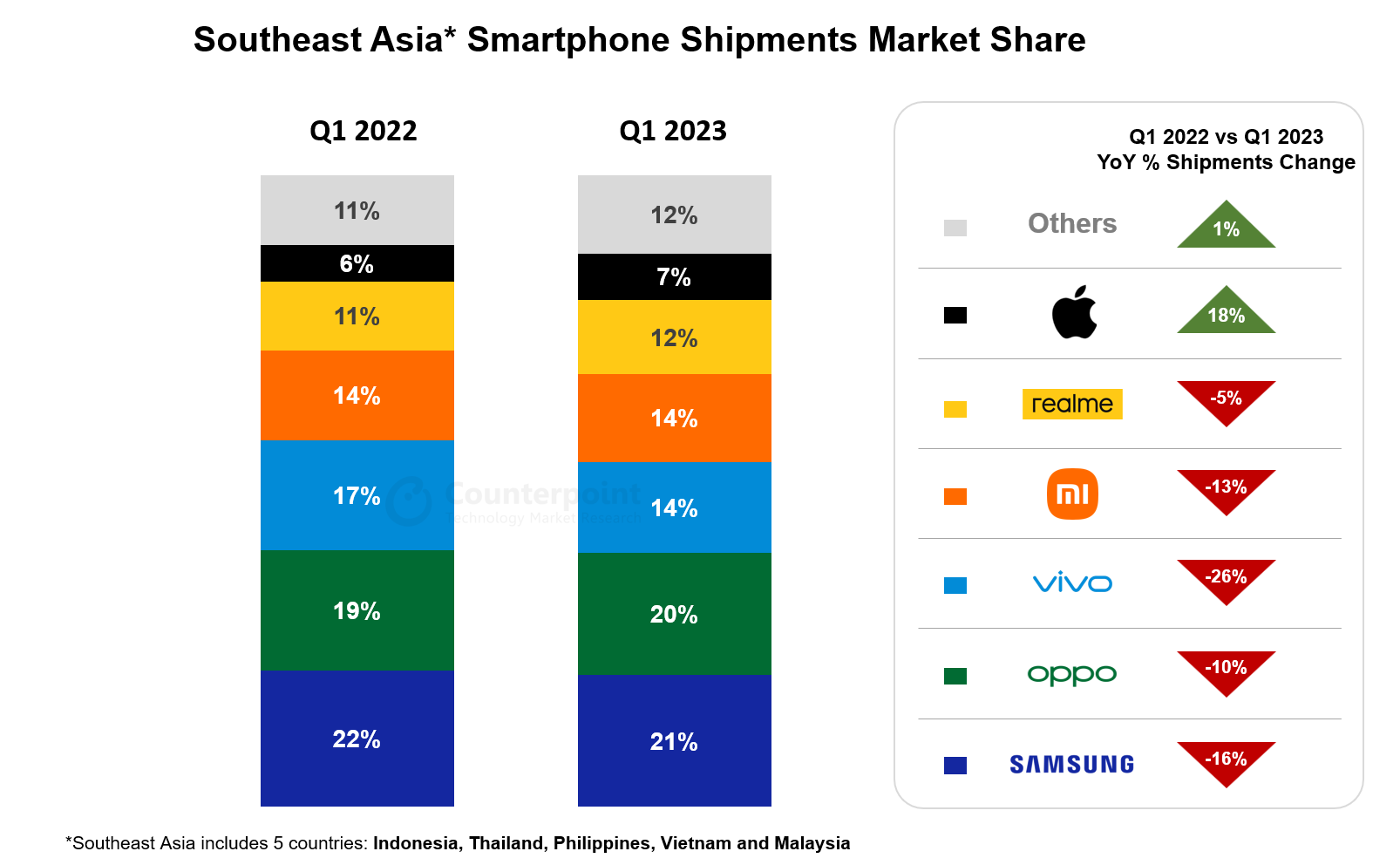

Smartphone shipments in Southeast Asia’s five key markets* declined 13% YoY in Q1 2023.

Apple’sshipments increased by 18% YoY during the same period.

Infinixwitnessed a 41% increase as the brand grew across SEA markets.

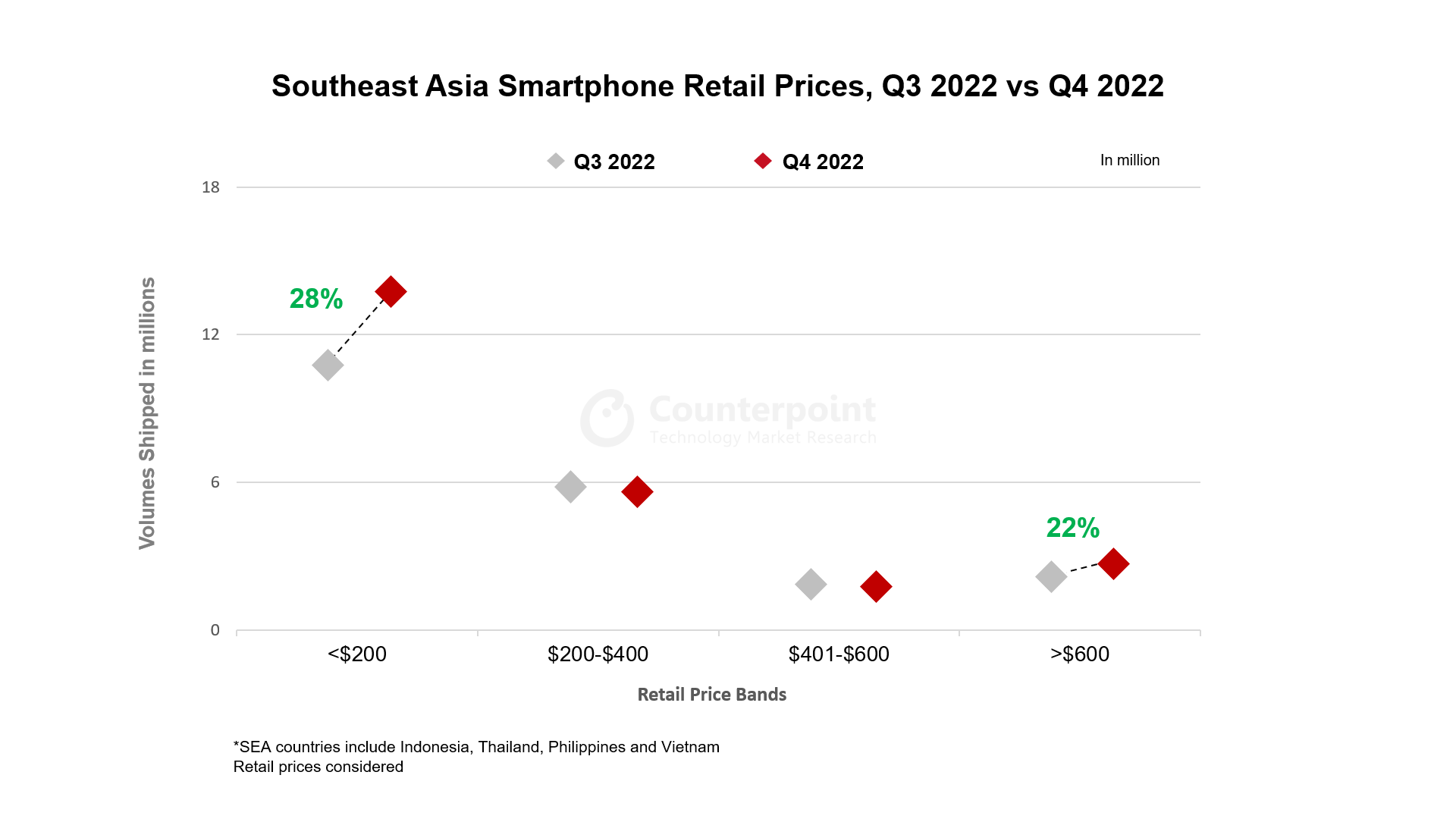

While mid-to-high-end ($201-$600) ranges suffered the most, the>$600 rangeshipments increased by 4%.

Jakarta, Hong Kong, London, Boston, Toronto, New Delhi, Beijing, Taipei, Seoul – May 15, 2023

Smartphone shipments inSoutheast Asia’sfive key countries (Indonesia, Thailand, Philippines, Vietnam and Malaysia) fell 13% YoY due to low demand and a seasonal drop, according to Counterpoint Research’sSoutheast Asia Monthly Smartphone Channel Share Tracker.

All key SEA countries saw a decline in Q1 2023 but some more than others. Countries like Vietnam received relatively more shipments in Q4 2022 and so OEMs felt the need to reduce volumes in Q1 2023. Consumer sentiment has not completely revived in Vietnam. Factors like a 10% fall inSamsung’sproduction, seasonally low smartphone demand after Q4 2022, and reduced revenues for OEMs and operators were also among the driving factors.Indonesiaand Thailand did comparatively well than the other countries as demand started improving in March 2023.

来源:对比研究东南亚ly Smartphone Tracker

All key SEA countries are coming out of the geopolitical effects from last year while still reeling under some inflation effects. For instance, thePhilippinessuffered high inflation at the start of this year. However, operators continue to remain aggressive on 5G development and partnerships with tech companies. The industry has resumed its earlier levels of advancement as foreign investments are again entering big economies likeIndonesiaand Malaysia. There are collaborations happening on the financial services front as well. For example, OPPO inIndonesiais partnering with banks to provide banking services while AIS, the leading operator inThailand曼谷银行合作提供菲南cial services on digital platforms. Consumers are not exactly feeling the improvements on the ground though. Most smartphone purchases are being delayed.

来源:对比研究东南亚ly Smartphone Tracker

Vietnam is a growingAppleiPhone market. The demand for theiPhone 13 and 14series was good in Q1 2023. Indonesia has seen growth iniPhoneshipments as well. Overall, iPhone shipments grew 18% YoY in Q1 2023.

Infinixis the official smartphone partner for Mobile Legends professional league in the Philippines. Infinix has improved on promoting itself as agaming brandin the region. Overall, though Infinix’s volumes are not on a par with the top brands, it continues to grow in the region. The brand grew 41% in Q1 2023.

While certain brands have been in focus at the start of this year, the price range share favored two consumer groups in Q1 2023. <$200 smartphones witnessed a 4% YoY growth despite an overall decline in volumes. Since entry-level phone shipments had been consistently low, pent-up demand motivated higher shipments in Q1 2023. However, not all countries saw a spike in low-end smartphone demand. OEMs in Vietnam were still looking to push these volumes. ThePhilippines’ low-income families are reeling under high tax and inflationary issues, restricting low-end smartphone purchases. Premium-end (>$600) smartphone shipments continued to rise and saw 4% YoY growth. Mid-to-high-end ($201-$600) smartphone shipments suffered the most across the region.

Commenting on the SEA economies in 2023,Senior Analyst Glen Cardozasaid, “Southeast Asia is at a stage where different consumer types are behaving in a different manner. Low-end smartphone buyers are recovering but they are not just there yet. Mid-to-high-end smartphone buyers are holding on to their wallets and extending the ownership of their phones, whilehigh-to-premium smartphonebuyers are unaffected by the economics of the situation. These consumers are going out and choosing to buy the S series, foldables andiPhones. While5Gis becoming a norm, operators are coming out with creative packages and providing options for all types of smartphones. The coming months are likely to see a bit more improvement in consumer sentiment while governments make sure that their countries remain largely unaffected by global macro issues.”

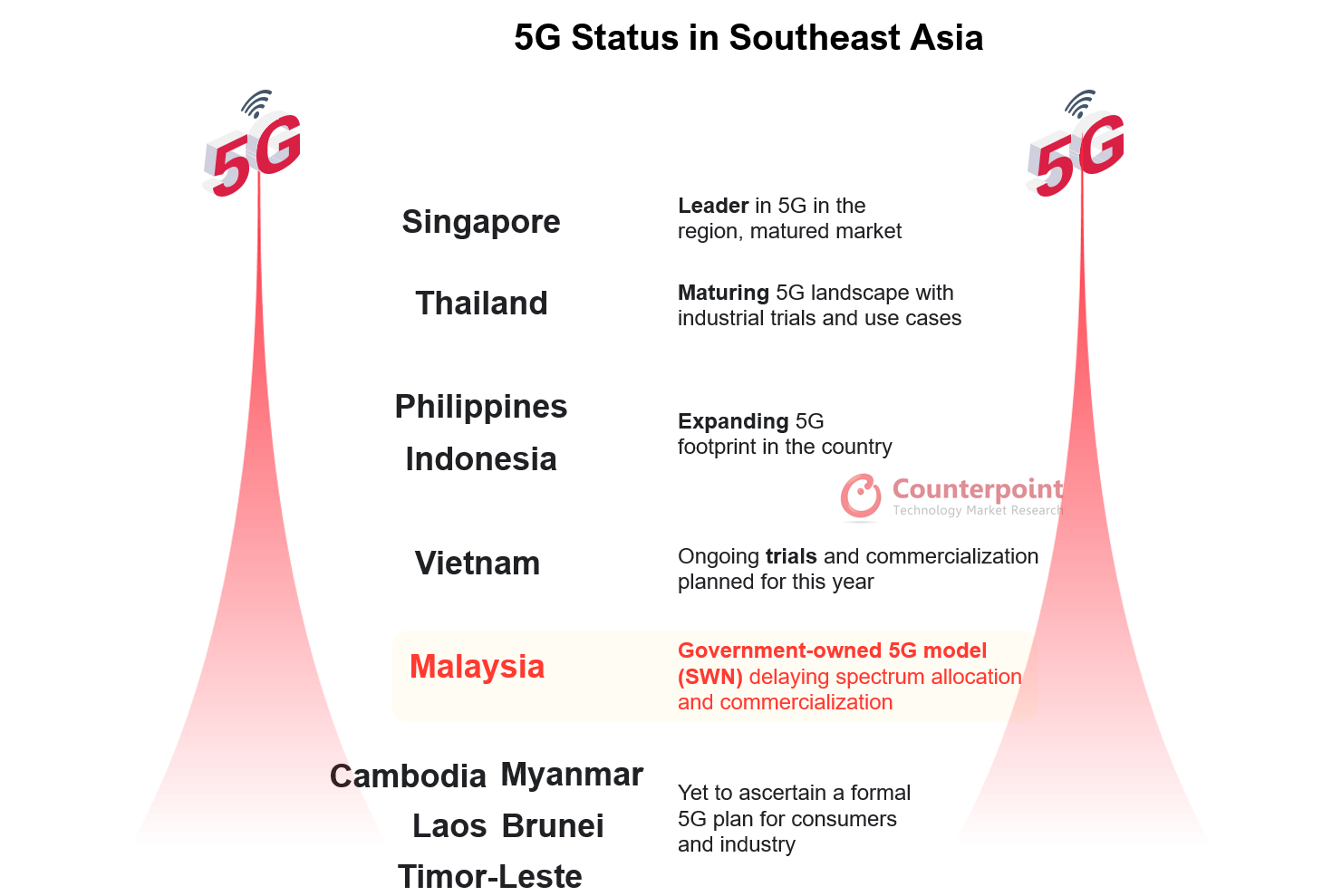

The Vietnamese government is looking to commercialize 5G in the country this year. This will facilitate a new level of manufacturing and consumer usage if done earlier than later. While theMalaysiangovernment and industry work on 5G commercialization and the terms for it, consumers are already equipped with5G smartphones.

With an increase in tourism in SEA countries earlier in the year, there is a chance that tourism business and revenue will increase this year. Countries likeThailandare also concentrating on eco-tourism initiatives that focus on sustainability, all through smartphones. All these developments are likely to spell normalcy for the public, leading to a likely improvement in consumer sentiment in the coming quarters.

*Key Southeast Asia countries/marketsinclude Indonesia, Thailand, Philippines, Vietnam and Malaysia.

Feel free to contact us atpress@www.arena-ruc.comfor questions regarding our latest research and insights.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Hong Kong, Jakarta, London, Boston, Toronto, New Delhi, Beijing, Taipei, Seoul – February 23, 2023

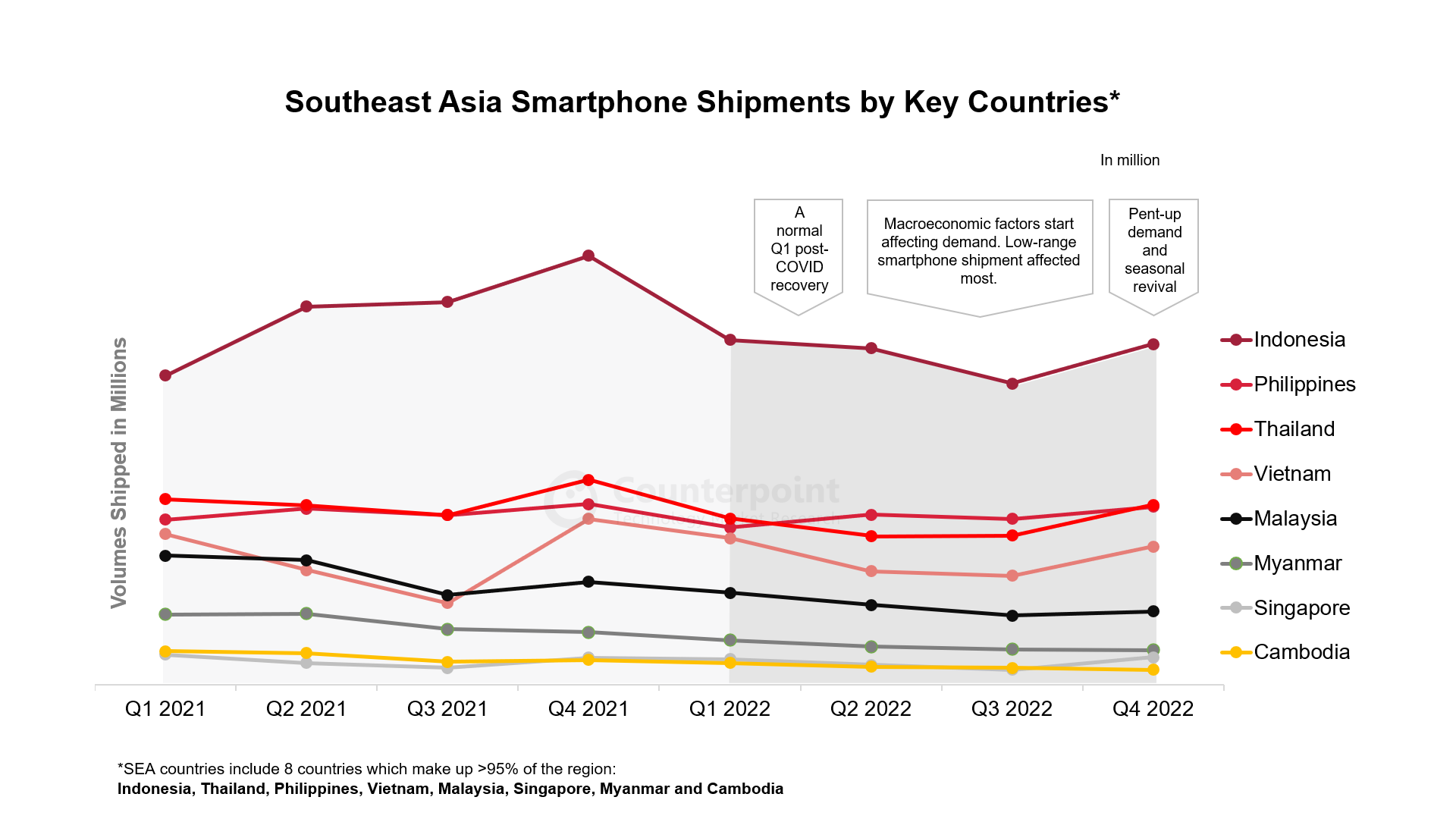

KeySoutheast Asia(SEA) smartphone markets* saw a somewhat consistent YoY drop in shipments throughout 2022. Inventory was still high in countries likeIndonesia, Philippines and Thailand, which led to a 17% YoY drop in shipments in Q4 2022, according to theMarket Monitor Smartphone Quarterly Report.

More notably, the end of the year signaled a much-awaited increase in demand forentry-level smartphones, resulting in a 28% QoQ increase in such shipments. New launches and pent-up demand played major roles in this. In thepremium segment, consumers kept the demand alive due to which there was a 22% QoQ increase in premium shipments.

Source: Counterpoint Research Southeast Asia Smartphone Tracker, February 2023

While the region’s smartphone shipments declined, countries like Vietnam andPhilippinesshowed more resilience to economic factors than others. Consumer demand seemed to have been less affected by macro effects. Smaller markets like Cambodia, Myanmar and even Malaysia declined relatively more. While they represent a small part of the region, their populations include a higher share of economically disadvantaged consumers. The decline in entry-level smartphone shipments affected these countries more than the rest.

Mature markets like Thailand and Singapore concentrated more on 5G penetration and further stages of industrial5Gapplications. Singapore’s operator partnership with Ericsson and 5G utilization in healthcare planning are just a few examples. InThailand, smart factory technology is being developed, private networks are increasingly used, and operators like AIS are helping out on automation through 5G.

Apart from an uptick in premium smartphone sales in these countries, there was also an increased focus on sustainability in the form of trade-ins,refurbishedsmartphone demand and corporate ESG initiatives.

Source: Counterpoint Market Monitor Smartphone Report, February 2023

The IT and e-commerce sectors saw job cuts inSEA没有项目2022年健康H2。即使是online smartphone channels contributed relatively less in seasonal campaigns like 11.11 and December sales. At the same time, OEMs, operators and retailers have been increasing offline networks across geographies. As the economies are struggling to come back to normal, a surge in tourism in this region contributed to the rebound.

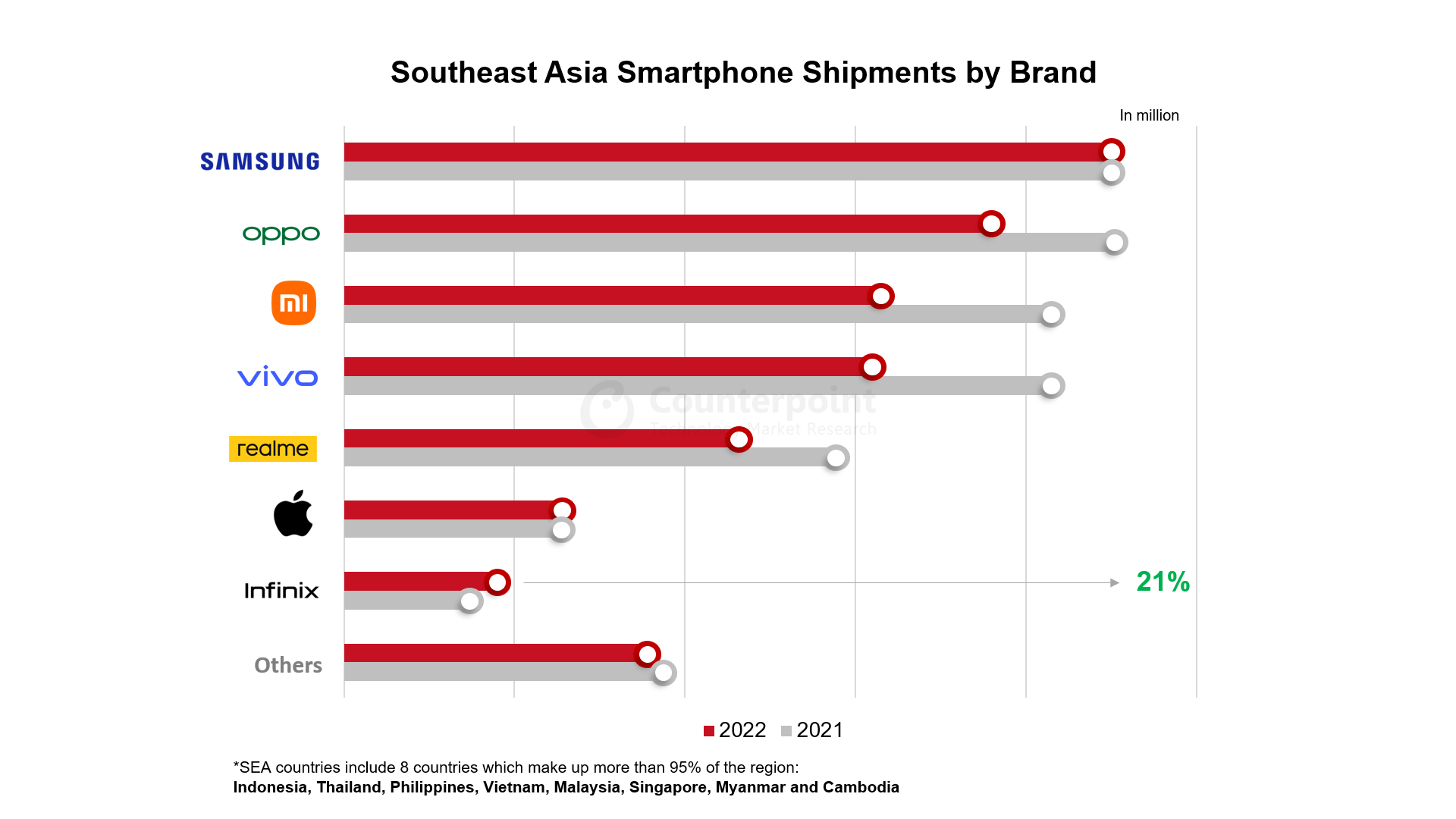

Chinese brands likevivo,realmeand Xiaomi consistently struggled with inventory levels and low shipments during Q3 and Q4 2022.OPPOimproved with demand due to its Reno series.

As premium demand surged,Samsung’sS seriesandApple’siPhone 13 and 14 series contributed to these brands’ volumes. Vietnam showed some surprising success with Apple shipments. Apart from newer models, even older ones like the iPhone 11 series were being sold well in the country.

The biggest gainer of 2022 is clearlyInfinix. TheTranssionbrand steadily grew in this region in 2022. Infinix’s focus on basic specs, practical pricing, channel offers and gaming all helped it gain momentum. The brand is especially doing well in the Philippines, Indonesia and Thailand.

Source: Counterpoint Market Monitor Smartphone Report, February 2023

Commenting on theSEAeconomies in 2023,Senior Analyst Glen Cardoza说:“东南亚在多个领域in 2022. Countries continue to increase interest rates, inflation is still a factor and trade volumes are dependent on the partner country’s demands. Any macro-level improvements in tourism, government relief and financial management will take time to positively impact the common consumer. In the absence of further adverse macro effects, the region is on a path to recovery. OEMs are however pessimistic about the recovery at this point and it is visible in their shipment levels. Improving entry-level smartphone shipments is a much-needed boon at this point. H1 2023 is likely to suffer the effects of low shipments, but we are likely to see a steady increase in shipments starting Q2 2023.”

Industrial and consumer 5G use cases will be visible in countries like Singapore and Thailand, while Indonesia and Philippines will concentrate on 5G penetration more than others.

What isChina’sloss is working out to be Southeast Asia’s gain in part.Manufacturingcenters like Vietnam stand to benefit from increased investments from companies looking to diversify from China.

The silver lining lies in the role of smartphones in digital transformation across this region. It also lies in the increase of foreign direct investment. All macro factors remaining constant, H2 2023 has the potential to make up for H1’s losses.

*Key Southeast Asia countries/marketsinclude Indonesia, Thailand, Philippines, Vietnam, Malaysia, Singapore, Myanmar and Cambodia.

Feel free to contact us atpress@www.arena-ruc.comfor questions regarding our latest research and insights.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

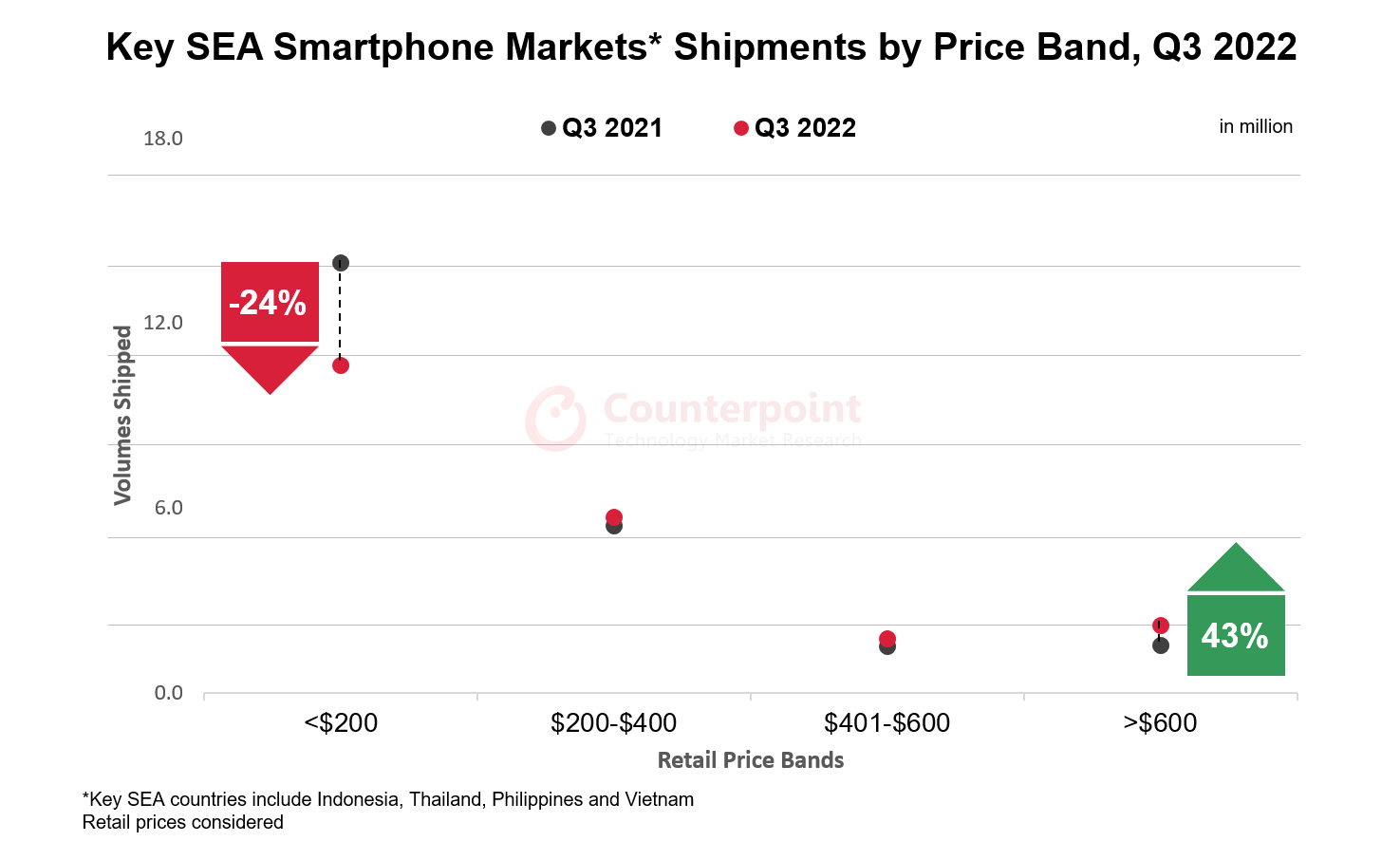

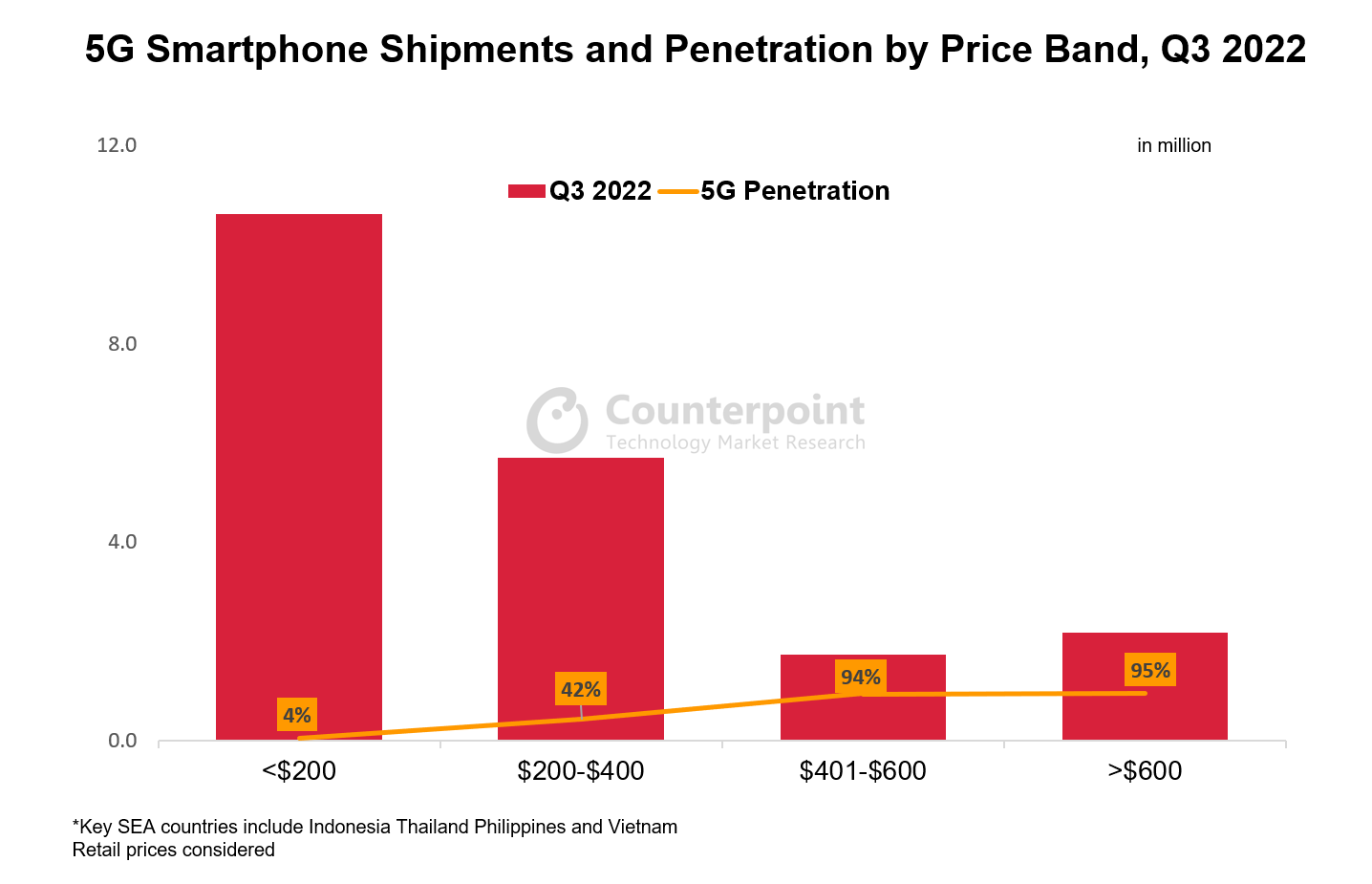

Premium smartphone (>$400) shipments grew 29% YoY while the <$200 price band shipments fell 24%.

Overall Southeast Asia smartphone shipments dropped 10% YoY.

Apple’s iPhone shipments grew 63% YoY in Q3 2022.

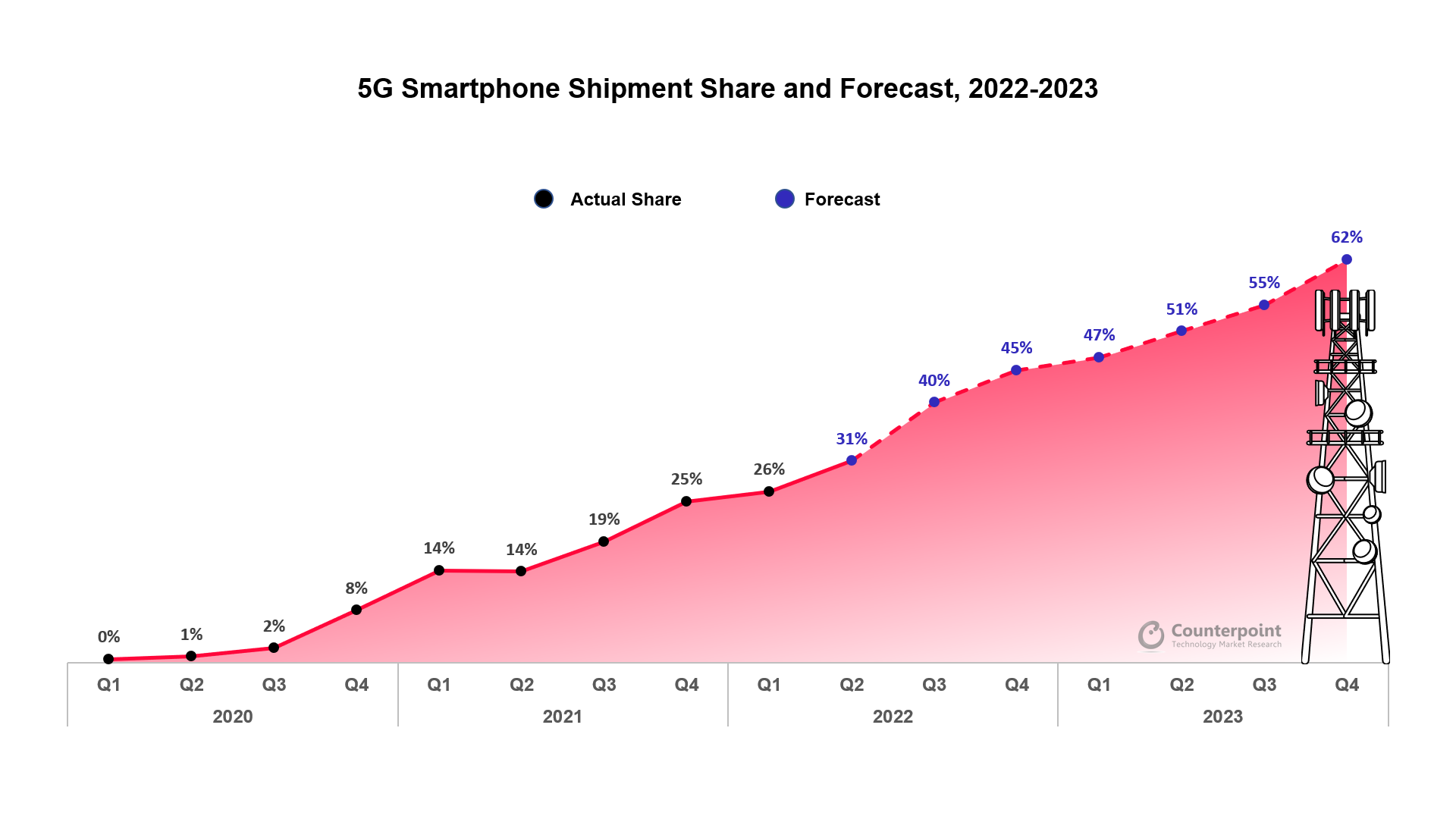

5Gmade up 32% of total shipments in the key countries, 5G smartphone shipments grew 56% YoY in Q3 2022.

The $200-$400 5G smartphone band saw a 73% YoY growth.

Hong Kong, Jakarta, London, Boston, Toronto, New Delhi, Beijing, Taipei, Seoul – November 17, 2022

Premiumsmartphone (priced more than $400) shipments in the key Southeast Asian markets* increased 29% YoY in Q3 2022, according toCounterpoint Research’s Southeast Asia Monthly Smartphone Channel Share Tracker. On the other hand, total smartphone shipments declined 10% YoY during the quarter. Southeast Asia is still facingmacroeconomic headwinds. This has resulted in weak business and consumer sentiments. Investments have slowed down too, including FDI volumes for some countries. All this has led to key smartphone OEMs collecting more than the required inventory before Q4 2022. The massive YoY increase inpremiumsmartphone shipments reflects the resilience of this segment’s customers during difficult times.

来源:对比研究东南亚ly Smartphone Channel Share Tracker, November 2022

September was supposed to see an increase in shipments across the region. But in 2022, this seasonal behaviour has been limited due to consistently low consumer sentiment. The lower economic strata are reeling under economic uncertainty, which shows in lower shipments and higher inventories overall. The Q4 festive season is expected to bring some relief.

There were some brand-level hits and misses too in Q3 2022. While Samsung shipments fell 13% YoY,Apple’sshipments were up 63% YoY across all the key countries.Vietnamseemed to be grabbing iPhones at a faster rate than its neighbours.

5Gsmartphone demand has seen slow progress in some countries likeIndonesiaandVietnamwhile it is much faster inThailandand Philippines, where the network is better and a large number of consumers are quite tech-savvy.Operatorsare still giving good package value to consumers even as it affects margins.

Specifications like processor, RAM, internal storage, battery capacity and charging speed remain a priority. Even if consumers in Indonesia and Vietnam do not actively consider5Gas a purchase factor, they tend to count it as a feature needed for the future.

Operators like Globe in thePhilippinesare keen on expanding their 5G infrastructure beyond the metro areas, whereas in Indonesia, 5G use cases have started showing for industries like mining. The $200-$400 5G smartphone price band saw a 73% YoY growth, which means that 5G is being made a staple feature by most OEMs.

来源:对比研究东南亚ly Smartphone Channel Share Tracker, November 2022

Commenting on the economy,Senior Analyst Glen Cardozasaid, “Most Southeast Asian countries like Indonesia, Thailand and Philippines raised interest rates in Q3 2022 to ease the blow of rising prices on the common consumer.Inflationduring the quarter was an average 5% in most SEA countries, which is not alarming but did take its toll on consumers. Prices for fuel, overall logistics and staple items went up, causing consumers to hold on to their wallets and defer big expenses like smartphones. The majority of such consumers are blue-collar workers or from economically weaker sections. While a country likeThailandis struggling to regain pre-COVIDvolumes due to depleted tourism levels, Vietnam has shown a 13% GDP growth in Q3. The effect of the same is reflected in the smartphone shipments in the last few months.”

OEMs still have more than the required inventory of older models which they might try to sell using all possible marketing tools acrossofflineandonlinechannels. New models launched since August will continue to fill the market with mostly5Gdevices. Offline retail players are likely to propagate experiential outlets, increased payment convenience, trade-in offers and better after-sales support. Models likeSamsung’sGalaxy A04s andvivo’sY02s might lead the charge in increasing low-range smartphone shipments again. This is necessary for the market to portray normalcy.

* Key Southeast Asia countries include Indonesia Thailand Philippines and Vietnam

Feel free to contact us atpress@www.arena-ruc.comfor questions regarding our latest research and insights.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Rising inflation and reduced consumer spending are resulting in a lengthening smartphone replacement cycle. So, how are OEMs navigating this trend with different financial schemes, easy upgrades, cashbacks and more? 5G smartphone shipments in Southeast Asia markets are also growing, so how are operators geared up for rolling out 5G services and demonstrating their use cases?

In the latest episode of ‘The Counterpoint Podcast’, host Tarun Pathak is joined by Senior AnalystsFebriman AbdillahandGlen Cardozato discuss the key trends in the SEA smartphone market. From falling shipments to H2 2022 outlook, 5G and online vs offline, we discuss all this and more in the podcast.

Gamingas an industry has been growing in leaps and bounds globally. While consoles and PCs are widely used platforms, the smartphone gaming demographic is growing the fastest and this is particularly seen inSoutheast Asia. The region also looks to be more promising as there are many factors propelling the current growth, chief among them being a whole new demographic adopting smartphones, getting digitally savvy and getting to know the gaming world. There are other important factors like increased internet connectivity and favorable changes accelerated by the COVID-19 pandemic in the last two years.

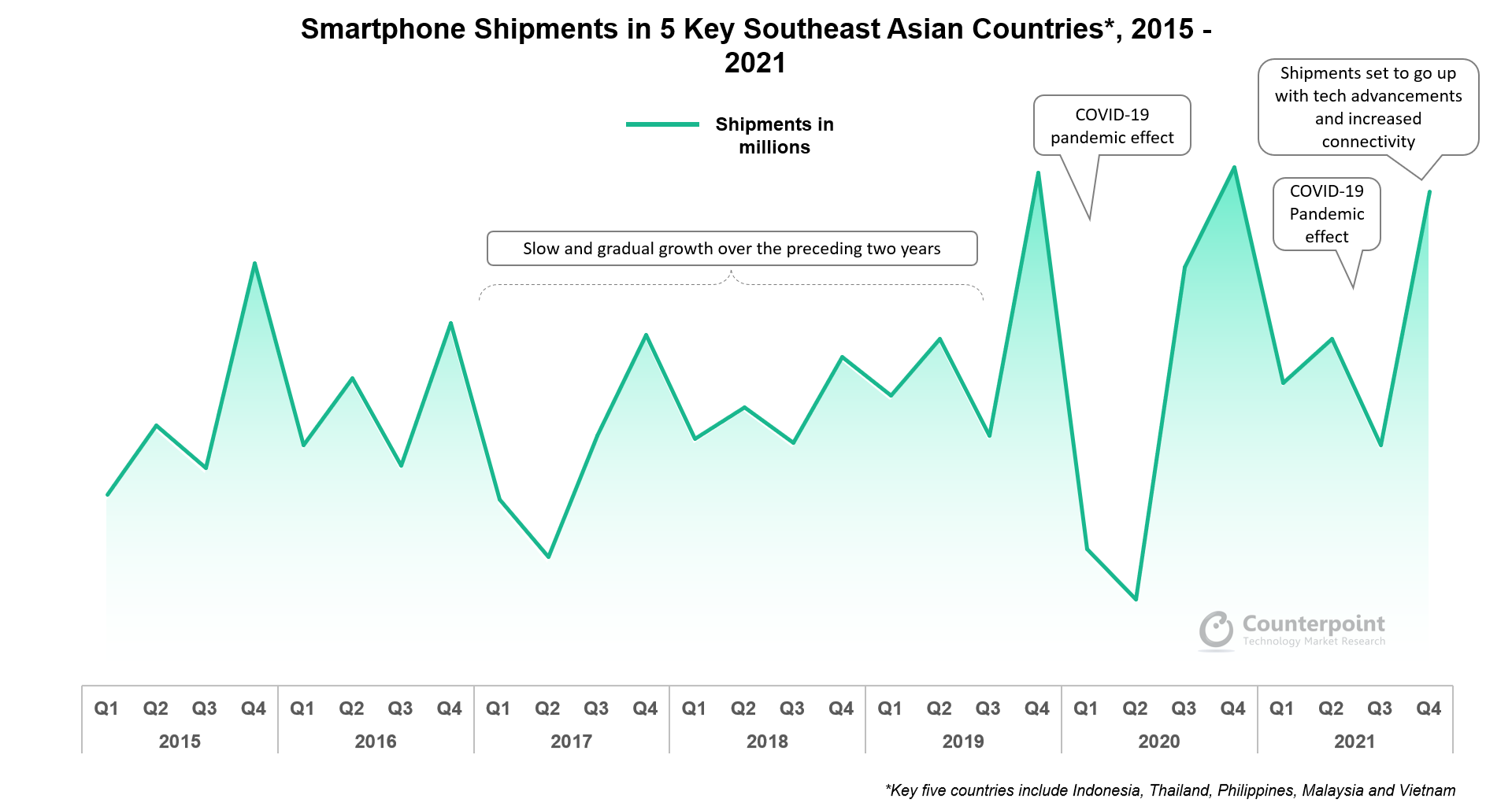

There are many other reasons at the country level as well, but there is one undeniable factor that would not have made this growth possible – smartphones. According toCounterpoint Research’s Southeast Asia Smartphone Tracker,key Southeast Asian countries’ (Indonesia,Thailand, Philippines, Malaysia and Vietnam) smartphone shipments in 2021 were back to 2019 levels.

Source: Counterpoint Research Southeast Asia Smartphone Tracker

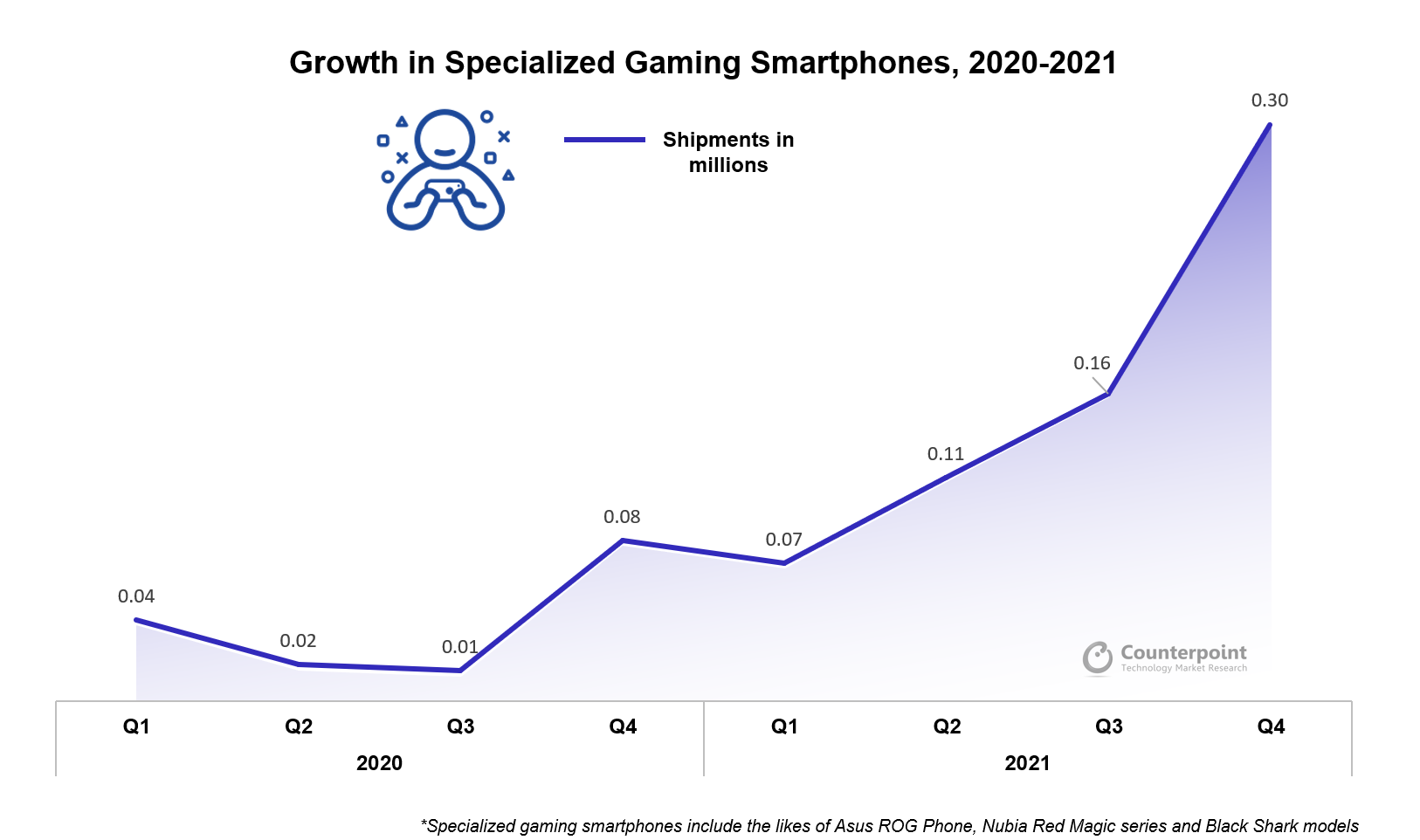

Gamingsmartphonescontinue to see an increase in demand. During the festive season in Q4 2021, gaming smartphones saw a 270% YoY increase. The affluent gamer demographic is growing exponentially, and this trend is likely to increase with all the focus that gaming is getting in these markets. Along with consumer interest, there is an increased focus one-gamingfromgovernmentsand industry players across the ecosystem. Currently there are more than 102 million active smartphone gamers in the 5 key Southeast Asian countries and this number is bound to increase in the coming years.

Source: Counterpoint Research Southeast Asia Smartphone Tracker

Indonesia,Malaysia, Thailand,Vietnam, Singapore, and the Philippines are the six most significant countries for mobile gaming in Southeast Asia. Whether they are small quick games to pass some time or more engaging strategy and shooter-type games, the gamer consumer base has gone up in the region just as fast as smartphone adoption over the last two years.

Factors pushing gaming growth over the last two years:

An effective way to pass the time when stranded at home during pandemiclockdownsand restrictions. For many people, less work or no work is a motivation to play on smartphones.

An escape from ongoing volatility in macroeconomic factors likeinflation, sustained COVID-19 repercussions, war situation in Europe and other more country-level factors.

Widening choice with multiple gaming genres (like strategy, shooting and e-sports) across multiple platforms (mobile, PC, console and even television).

Types of games all the way from casual to elaborate heavy-duty games that make a player a full-time earning pro-gamer. Some countries in this region also promote international gaming tournaments.

Connectivity and Ecosystem Initiatives:

Connectivityhas played a vital role in increasing online gaming in the region.Fixed broadbandconnections have seen tremendous growth in the last two years along with a jump in new subscribers. Tier 2 and Tier 3 cities in the key SEA countries have seen some major growth as well. Broadband, whether fiber or fixed wireless, makes up more than 38% of the base in these key SEA countries. 5G connectivity is being improved starting with metro and Tier 1 cities. 4G connectivity is being increased throughout these countries as well. All this has played a major role in pushing the gaming culture irrespective of geography, age, gender, or economic background of the user.

OEMs have understood that a good gaming experience is supposed to be a necessity even for the casual gamer and not just the heavy-duty gamer.

Esports is big in thePhilippines.realme, one of the top smartphone brands in the country, has partnered with the national team SIBOL for esport tournaments. realme itself has its pro-gaming tournament ‘Realme Mobile Legends Cup’ in the country.

Infinixis an upcoming brand in most Southeast Asian countries. Its focus on gaming models has led to the brand being considered for low-range to mid-range smartphones for gaming. Gaming smartphone biggies likeAsushave said that the gaming smartphone business is not yet profitable for them, but they are still sticking to their image and launching more gaming phones.

Operators likeDtacinThailandare offering gamers a specialized package with maximum speed and special internet lanes to make sure excess usage does not result in lags.

Top semiconductor companiesQualcommandMediaTekhave been focusing on thegamingconsumer for a while now with gaming-related chipset versions of their standard offerings. Even chipset makers likeARMhave been considering gaming as a motivation behind future tech. ARM recently came out with a gaming-specific chip.

The Changing Ecosystem:

There is a mix of low-end to high-end smartphone users in each of the SEA countries, but every country shows different characteristics and preferences in gaming genres. Southeast Asia’s consumer base is maturing. Indonesia and Thailand are the region’s largest revenue earners, followed by the Philippines andMalaysia. TheIndonesianmarket is not only the region’s largest but also the fastest growing. In Southeast Asia, the younger population, which used to play smaller games on cheaper phones, is upgrading to mid-tier phones and preferring more heavy-duty games.

It is already established that SEA is a huge gaming market with more potential but there are many factors changing this volatile tech trend currently.

Trends changing the gaming ecosystem:

Female gamers lead male gamers in many areas of the region. Most avid gamers can be found between the ages of 25 and 60. The bulk of this demographic in the region usually does not have a very high-priced smartphone. This means that even low-range to mid-range smartphones are being used for gaming and not necessarily just for casual games.

Increase invideo contentrelated to gaming, with the rising viewership on online platforms such as Twitch and YouTube, is resulting in marketing initiatives across platforms, apps and games.

Cloud-based gamingand interconnectivity of gaming platforms are likely to affect device purchases in the coming year. There is an opportunity for consumers to opt for phones with lower specifications. As cloud gaming increases its footprint, gamers will only need a steady, fast internet connection.

To counter the frequent churn due to higher boredom levels in casual games, more variety is now being introduced in these games. Game makers are investing in research, marketing campaigns and, more importantly, associating with the right players in the ecosystem.

Consumers are actively demanding the capability to play heavy-duty console and PC games on mobile platforms. This is a big opportunity for smartphone OEMs especially with growth in 5G connectivity.

Gamers and their Smartphones:

Source: Counterpoint Research

Gamerswho are invested in heavy multiplayer graphics online games like PUB G make up a smaller portion of the pie in this region. Instead, games like Subway surfer, Mobile legends, Arena of Valor, Roblox and Free Fire are played the most.

Gaming companies are making sure that smartphone versions of their games are available and that the hardware requirements need not be too high to enjoy these games on the mobile phone. Multiplayer gaming platforms on mobiles are nascent in this region as of now but as the telecom sector advances, this gaming preference is set to grow.

5G and Gaming:

5Gpenetration into gaming will be a slow process for another 2-3 years, especially for major markets like Indonesia. While Singapore is leading the curve in 5G,Thailandand thePhilippinesare more capable of advancing with5Gin gaming. The future of cloud gaming and multiplayer mobile setups, however, is bound to remain bleak in this region as compared to the West.

The 5G share in monthly smartphone shipments is likely to reach well above 45% by the end of this year. Most gamers, whether casual or professional, will look to include5Gin their gaming experience, especially since there is growth in the smartphone version of games usually played on consoles and personal computers.

Source: Counterpoint Research Southeast Asia Smartphone Tracker

The Future of Gaming

Though Southeast Asia has the highest number of gamers in Asia, it contributes the least revenue. The entry point of free games is a crowd puller, but gaming companies and developers are trying to have a stronger revenue model. Ecosystem players have focused on all segments of consumers and made sure that multiple platforms can cater to different demographics based on their convenience and motives. Mobile gaming in Southeast Asia is capable of not just increasing gamer volumes and revenue but also spreading across multiple sectors like retail,e-commerceand sports.

While gamers in Southeast Asia are spread across early teens to senior citizens, the 18-35 age bracket is the one contributing most to the maturing gamer ecosystem.

在接下来的几个月,我们可能会看到更多的标志eting initiatives on platforms, and gaming business models centered around profit generation, which could be through increased micro-transactions within free game offerings. OEMs, operators, and retail distributors will combine the gaming aspect much more with their offerings.

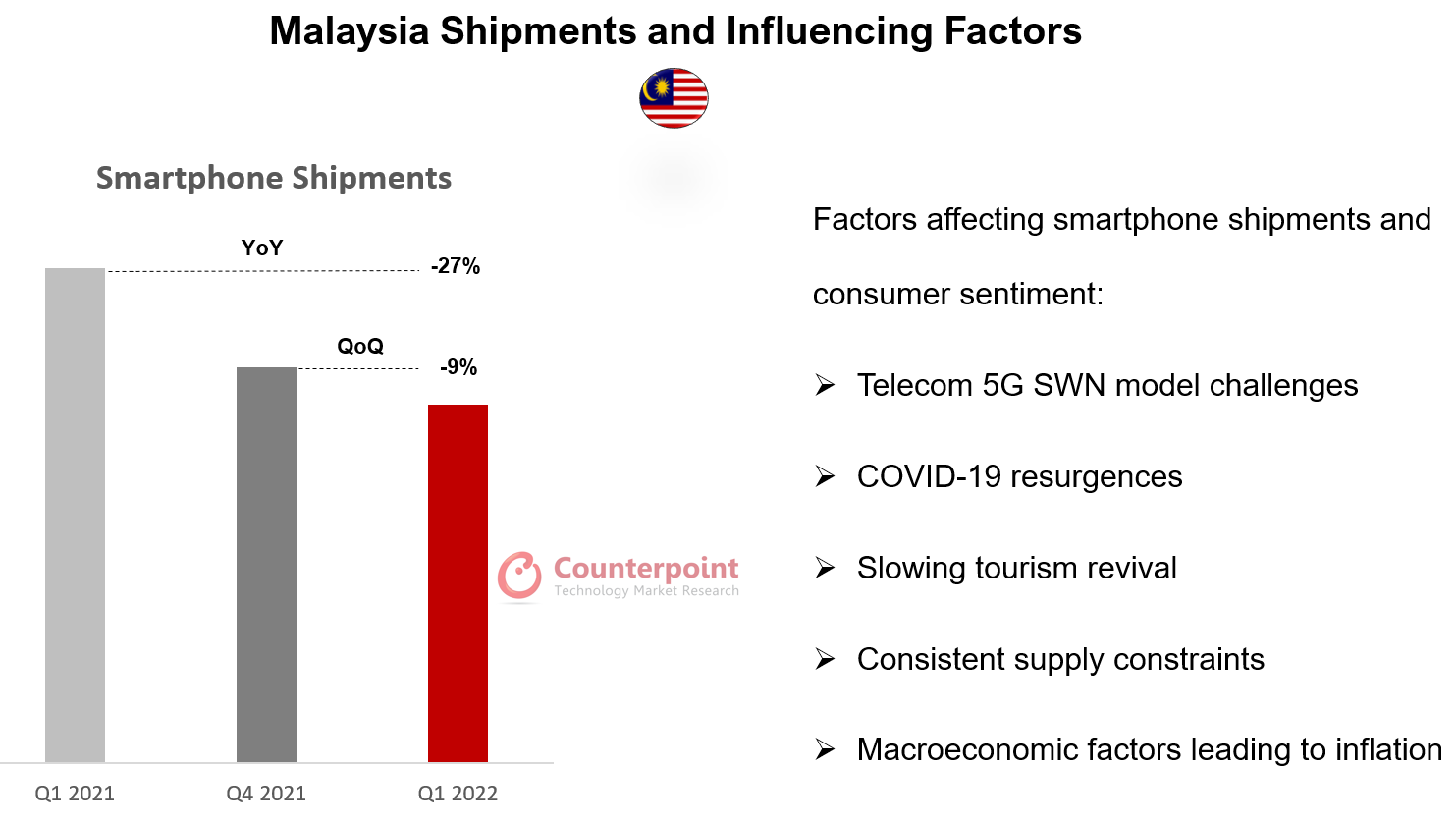

Malaysia’s smartphone market went through its seasonal dip in volumes in Q1 2022, but there were other factors at play as well. According toCounterpoint Research’s Southeast Asia Monthly Smartphone Tracker, not only did Malaysia’s smartphone shipments fall 9% QoQ in Q1 2022 but also dropped 27% YoY, which is notable. Apart from factors likesupply constraints,COVID-19resurgence and drop in tourism revenues, the decline can also be attributed to issues related to5Gspectrum allocation.

5G Conundrum

Malaysia is going through an extended negotiation phase in thetelecomsector. The two sides here are thegovernmentand the four mainoperatorsin the Malaysian telecom landscape – Maxis BHD, Celcom Axiata BHD, Digi Telecommunications and U Mobile. These four operators have recently requested a review of the government’s 5G access offer as they want at least a 51% stake in the government-owned5Gagency DNB. They are also looking for a review of the access offer with regard to the pricing plan and network access plan offered by the government. Cost and transparency seem to be a concern here, while control and profit are at stake.

While the government andoperatorscontinue to re-pitch propositions and cement their stance on the government-run 5G model, other segments of the industry and consumers are making sure their interests are not affected. OEMs continue to launch5Gsmartphones in a country where digital transformation is in full swing, with 28% of smartphone shipments in Q1 2022 coming from 5G-compatible models.

Economy

With a 5% YoY GDP growth in Q1 2022, the country is riding high and promising to show further growth on account of high domesticdemand, consistency in external demand and an improved labour market. While the retail industry and offline channels have opened, themanufacturingsector has grown in the first quarter as well. There would have been an added layer of excitement leading to higher achievements had the5Gsituation not escalated over the past 18 months. Industrial propulsion is thus limited due to the absence of 5G use cases.

Covid Effect

The country was reeling under its worst COVID-19 resurgence in the second half of Q1 2022, which handicapped a big portion of the offline channel dynamics, leading to much lower shipments. However, April onwards, the country is seeing relaxation in curbs on not only domestic movement but also international travel policies. Ifsupply constraintsreduce, we may see much better Q2 and Q3 on account of pent-up demand.

Consumer Front

A big portion of the Malaysian smartphone-using population is tech-savvy. Many consumers have already transitioned to using e-commerce, e-banking, e-finance,digitaland social marketing, and other platforms. There are several actively growing consumer sub-genres in the form of gamers, power users, consumers switching from feature phones, and more. At this point, there is a growing frustration as the people have access to 5G devices, they have the know-how and are motivated, but still can’t access 5G. The lack of 5G infrastructure and commercialization is limiting Malaysia’s growth potential in a very important sector — technology.

The Malaysian smartphone market is promising for the region and its consumer base is one of the most versatile with regard to technology. The 5G situation, however, needs to catch up with government and industry momentum. The coming months may see higher volumes for the smartphone market, but it will see an overall development only when 5G is commercialized.

Online channel share was 26% in Q4 2021, the highest compared to the neighboring SEA countries likeIndonesia,PhilippinesandVietnam.

5Gcompatible devices made up 40% of Thailand’s total smartphone volumes in 2021.

香港、伦敦、波士顿、多伦多、新德里、贝jing, Taipei, Seoul – February 17, 2022

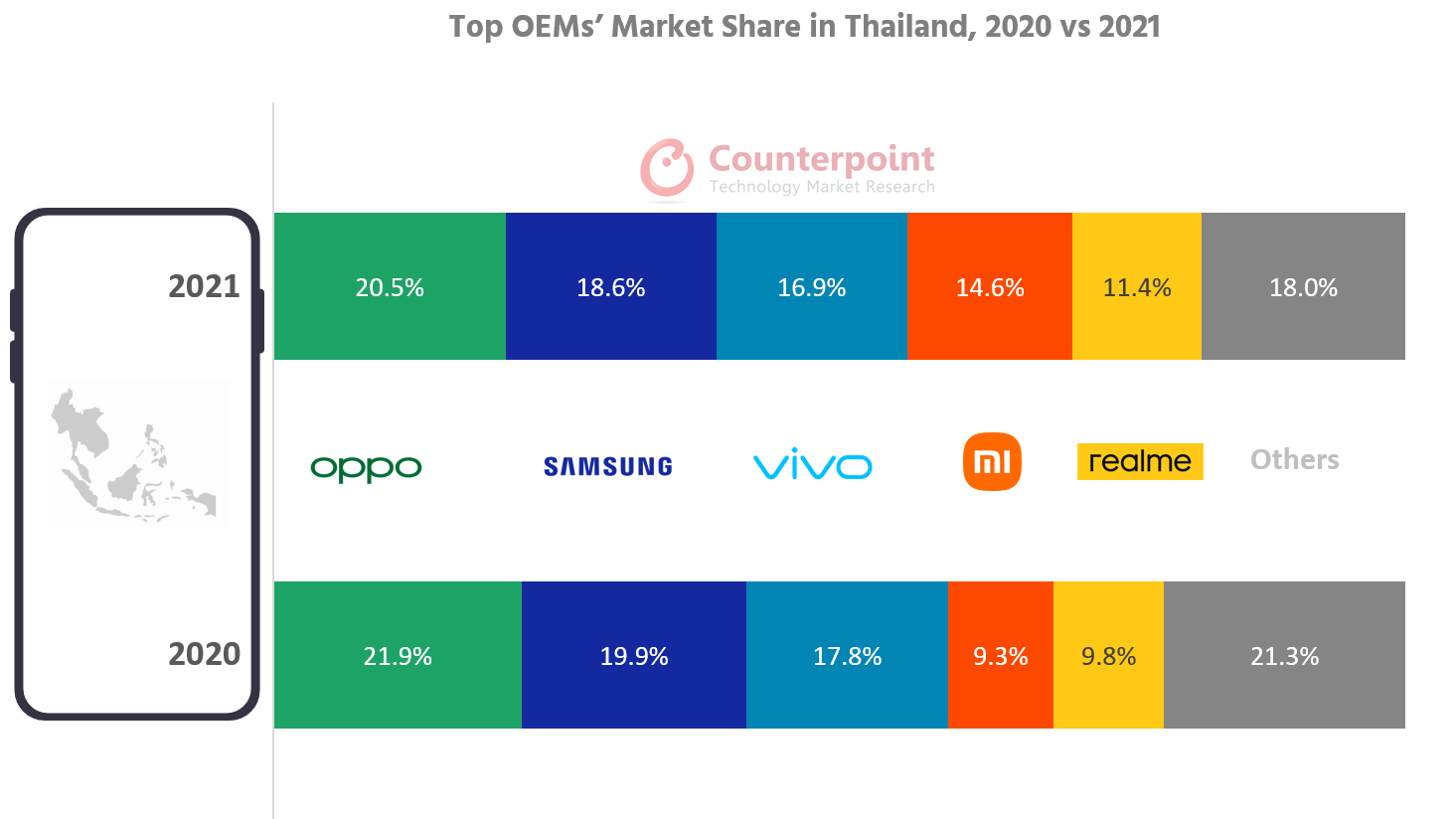

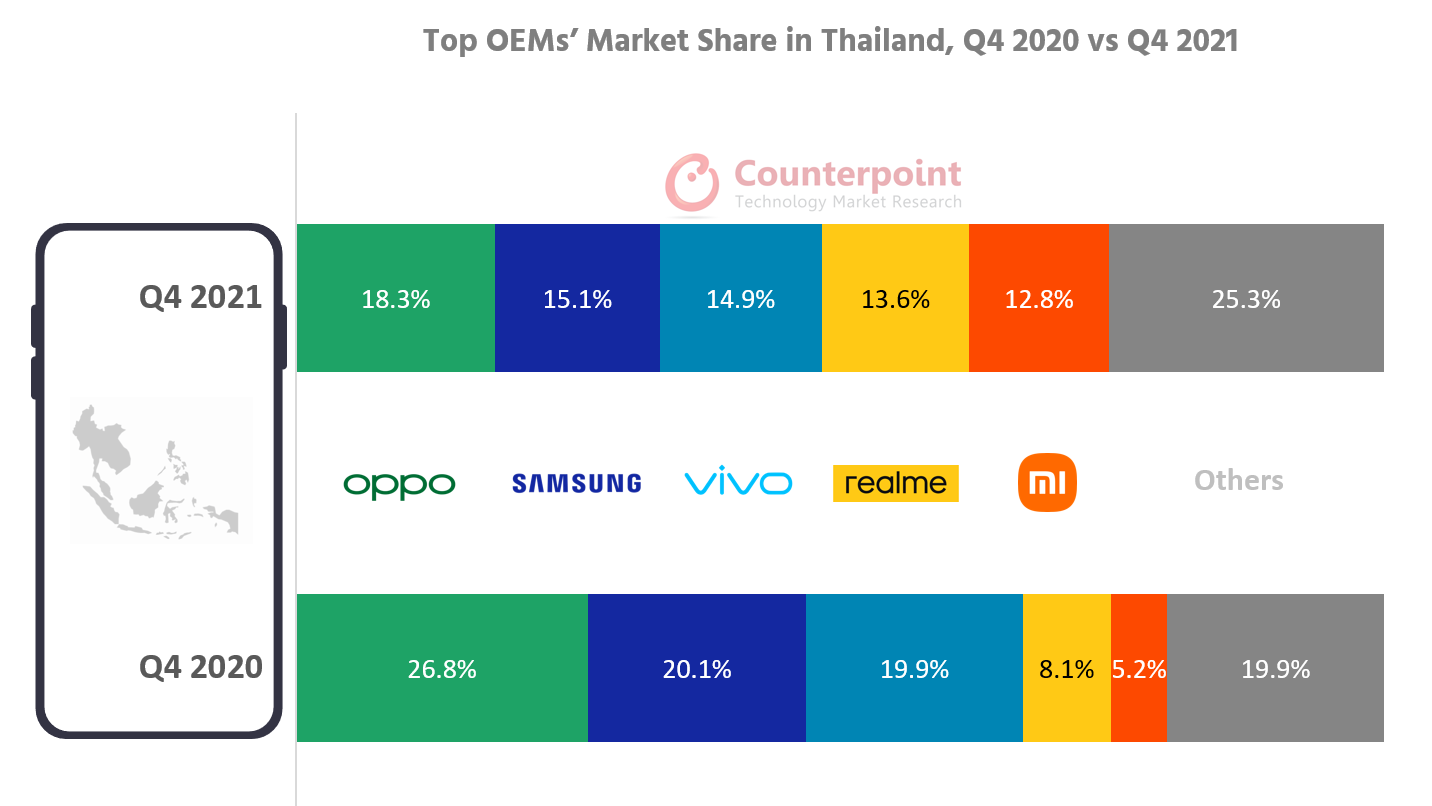

Thailandwent through a challenging time in 2021 withCOVID-19 and subsequent economic effects taking a toll on consumer spending habits and overall market sentiments. According toCounterpoint Research’s Southeast Asia Monthly Smartphone Channel Share Tracker, Thailand smartphone shipments grew 3% YoY in 2021 driven by increased 5G transition, more digital transformation in Tier II and Tier III towns and an all-time-high increase in e-commerce purchases.

Talking about the smartphone brands and their performance in 2021,Senior Analyst Glen Cardozasaid, “Xiaomiinvested comparatively less in marketing initiatives but was one of the brands that achieved the highest shipments ever due to its launches, partnerships in channels and association with ecosystem players like operators.Applemanaged much higher volumes in Q4 2021 after the iPhone 13 series’ launch, crossing even the 2020 levels.realmedid well with online festive sales and had good YoY growth in Q4 2021.Infinixperformed much better on online sale days. Being an online-centric brand, Infinix has aggressively made its presence known on most e-commerce sites.”

来源:对比研究东南亚ly Smartphone Channel Share Tracker, December 2021

Thesmartphoneindustry had a good first half in 2021 but Q3 pulled down the shipment levels for most brands due to high COVID-19 infection rates.Supply constraintsincreased in H2 2021, but brands made sure that Q4 had enough inventory with most channel partners. On the country’s economy,Cardozasaid, “Thailand’stourism industry has always been a major revenue generator, but it has consistently taken a hit over the last two years. Consumer buying behavior has been volatile over 2021. As the year went by, there were worries of declining consumer purchasing power. In contrast, due to Q3 restrictions, Q4 was able to utilize the benefits of pent-up demand. At the same time, the government’s digital economy initiatives did not stop. It made sure that broadband networks continued to expand in all regions and tech expertise reached major industries like healthcare and manufacturing, with the integration of 5G use cases in the pipeline. Even tourism started seeing an increase in domestic visitors. Q4 2021 was a bounce-back for most OEMs with regards tosmartphoneshipments but brands like Xiaomi slipped in rankings due to acute supply issues.”

来源:对比研究东南亚ly Smartphone Channel Share Tracker, December 2021

The transition to5Ghas been a consistently strong trend in this country. Q4 2021 alone saw 49% of shipments coming from 5G smartphones. All main OEMs, led by Apple,vivoand OPPO, actively launched5Gsmartphones through 2021. Just like the 5G trend, online shipment share grew much more towards the last quarter as compared to any year. Online shipments increased 27% in 2021 and most of this increase came in H2 2021.

In 2021, more cohesiveness was seen betweenoperators, retail offline channels and e-commerce players, giving a big push to OEM volumes. Moreover, foreign investments continued to pour into Thailand, showing faith in the country’s growth strategy. In 2022, we should see tougher competition between the top five brands. There is also a possibility of increased shipments in the low- and mid-tier price bands as long ascomponent constraintsdo not hamper production.

市场总结:

Samsung在2021年与朋友紧张的比赛。麸皮d coordinated with all its operator and retail partners to make sure that not only mid- and premium-end devices were promoted well but also their low-tier partners, including the A series, which worked so well for Samsung through the year. In marketing, Samsung’s partnership with South Korean band BTS was notable.

OPPOsaw an 11% dip in overall shipments in 2021 but still managed to lead the market by a very slim margin with Samsung. OPPO’s Reno series did well in H2 2021

Online share of shipments hit 26%in Q4 2021, which is the highest for any quarter in Thailand. This means many more consumers opted to purchase their smartphones online due to factors like cost, offers and convenience.

In Q4 2021,5G smartphones made up 49%of the country’s smartphone shipments, with theiPhone 13series launch pushing the numbers.

Note: Xiaomi includes Redmi, POCO and Mi sub-brands. OPPO includes OnePlus.

Feel free to contact us atpress@www.arena-ruc.comfor questions regarding our latest research and insights.

Background:

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Analyst Contacts:

Glen Cardoza

Follow Counterpoint Research press(at)www.arena-ruc.com

Philippines’ smartphone shipments increased 5% YoY in 2021 but decreased 10% YoY in Q4 2021.

Samsung led the market in 2021 with a 22.4% share, followed by realme at 20.9%, OPPO at 18.5% and vivo at 16.2%.

Online channels grew 34% YoY due to pandemic-induced trends.

Beijing, Seoul, Taipei, London, Boston, Toronto, New Delhi, Hong Kong – February 17, 2022

菲律宾智能手机出货量fell 10% YoY in Q4 2021 but increased 5% YoY in 2021, according toCounterpoint Research’s Philippines Monthly Smartphone Channel Share Tracker. The third-biggestsmartphone marketinSoutheast Asiaexperienced a COVID-19 lockdown in the first half of 2021. But with an increasing vaccination rate (45.3% fully vaccinated at the end of 2021) and e-commerce gaining popularity, the second half of 2021 witnessed a 42% increase over the first half. The market is expected to regain normalcy in 2022, although elections during the year may cause some uncertainty.

Top OEMs’ Market Share in Philippines, 2020 vs 2021

Source: Counterpoint Research’s Monthly Philippines Channel Share Tracker Notes: Xiaomi includes POCO and Redmi; OPPO includes OnePlus.

In terms ofmarketshare in 2021, the top fourOEMswere the same as in 2020. But Samsung took the first spot from vivo with a 44% YoY increase in 2021.realmemade a switch with OPPO for the No. 2 position.Senior Research Analyst Ivan Lamsaid, “Samsung’s good show was driven by its strongersupply chain. After resolving the supply and production issues in Vietnam, Samsung seized the opportunity and came up with a strategy to turn around in the Southeast Asian markets. It launched channel campaigns targeting both wider and specific customer groups. The brand maintained its uptrend in the market from Q2 2021 to the last quarter of the year. realme scored big by bringing in affordable models to target users upgrading from entry-level devices. Its C series continued to be popular among the Philippines consumers. realme’s growth was also driven by itsonlinepresence.”

E-commerce is growing very fast in Southeast Asia. In the Philippines market, online channels accounted for 16% of the total shipments in 2021 with nearly 34% YoY growth.

Senior Research Analyst Glen Cardozasaid, “With the rise ofDito, Smart and Globe Telecom have been actively expanding the 5G reach to face the competition. 5G device penetration also increased in 2021. In terms of overall price band trends, some gains were seen in the mid-tier segment. While the sub-$150 segment’s contribution declined from 60% in 2020 to 40% in 2021, the $250-$499 segment saw a significant increase due to users upgrading to higher segments or 5G phones, and OEMs pushing mid-tier devices due to the ongoing component shortages.”

Top OEMs’ Market Share in Philippines, Q4 2020 vs Q4 2021

Source: Counterpoint Research’s Monthly Philippines Channel Share Tracker Notes: Xiaomi includes POCO and Redmi; OPPO includes OnePlus.

Philippines’ smartphone shipments decreased 10% YoY in Q4 2021.Lamsaid, “The COVID-19 restrictions, including on offline retail, were relaxed only at the end of the quarter. Consumer spending also remained impacted due to stagnant household incomes.”

Samsung took the first position in Q4 2021 with its shipments rising 22% YoY. The second position was taken by realme with an 8% YoY increase.Lamadded, “OPPO andvivoboth experienced a 4G SoC shortage and were forced to prioritize supplies for their home market China.”

Commenting on 2022 expectations,Lamsaid, “The Philippines economy expanded by 5.6% in 2021 after logging 7.7% growth in the fourth quarter. Relaxations in pandemic-related restrictions buoyed business activity. Therefore, 2022 should have a bright start. However, we need to factor in any uncertainty related to the elections that are to be held on May 9.”

Please reach out to press(at)www.arena-ruc.com for press comments and enquiries.

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

In order to access Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not. 当你注册个人信息我们问you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time. In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company. – Passwords are for user’s individual use – Passwords may not be shared with others – Users may not store documents in shared folders. – Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified. Accuracy of Information: While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links: This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience. This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.