(Use the buttons below to download the complete chart)

Global electric vehicle market highlights:

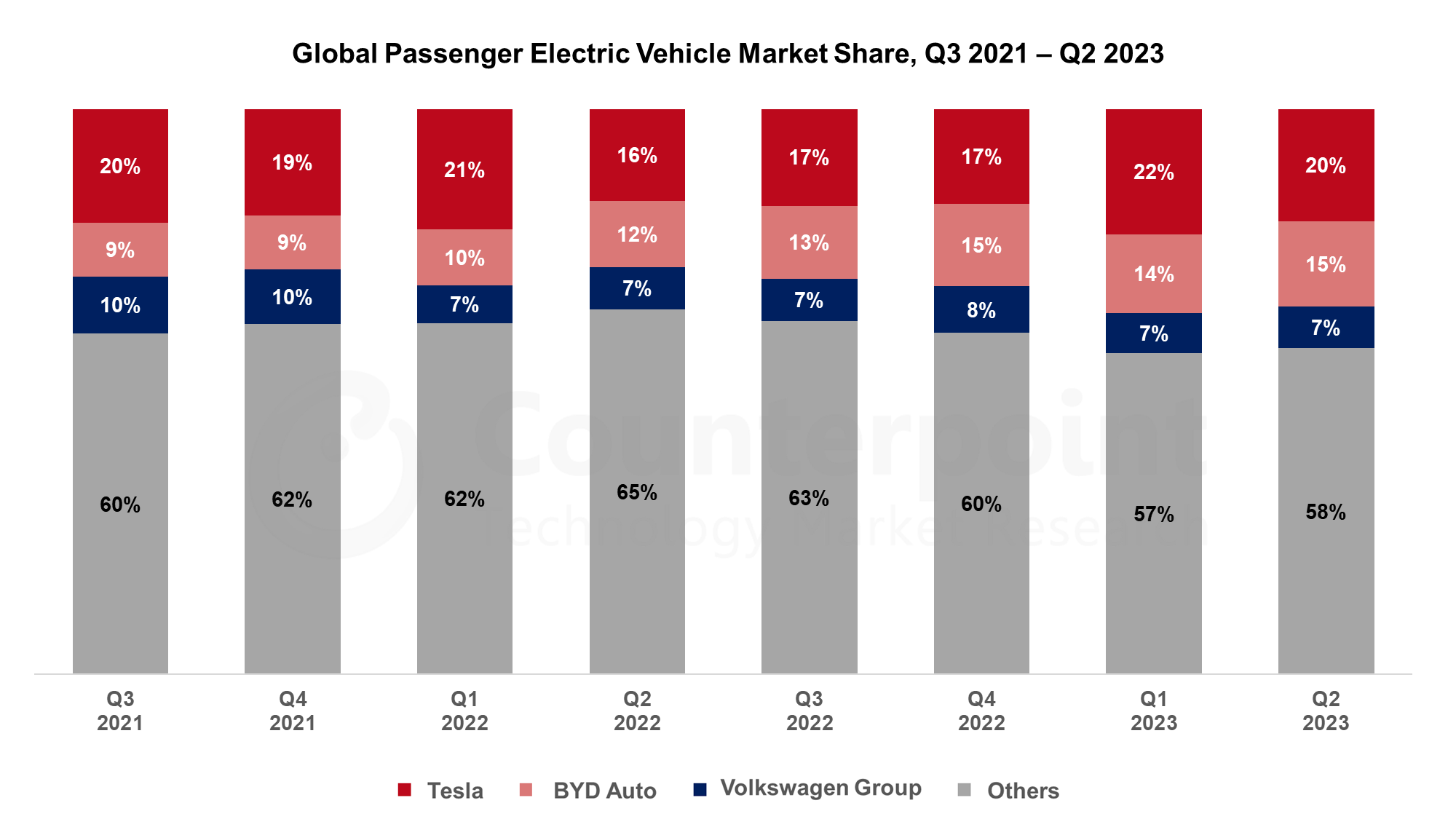

BEV sales during Q2 2023 grew over 50% YoY.

One in every 10 cars sold during Q2 2023 was a pure battery electric vehicle (BEV).

China remained the leader in global BEV sales followed by USA and Germany.

贝福在美国的销售额同比增长了近57%,highest among the top 3 EV markets.

Tesla Model Y retained its title as the ‘best-selling’ passenger car globally.

With the present growth trajectory, total BEV sales are expected to reach over 10 million units by the end of 2023.

Top Electric Vehicle Brands highlights:

Tesla: Tesla sales soared by 83% YoY during Q2 2023. Tesla Model Y accounted for 64% of Tesla’s global sales. Model Y retained its title as the ‘best-selling’ passenger car model globally.

BYD Auto:在2023年第二季度,比亚迪汽车的贝福销售增长了96%YoY, faster than Tesla. BYD Yuan Plus (or Atto 3) was the best-selling BYD model followed by BYD Dolphin and BYD Seagull. BYD Seagull was introduced in April 2023 during the Shanghai auto expo. BYD Seagull also ranked #9 among the top 10 best-selling BEV models globally. BYD exported over 35,000 EVs during Q2 2023. Almost two-thirds of its exported BEVs were sold in Thailand, Israel and Australia.

Volkswagen Group: BEV sales of VW group grew by 48% YoY during Q2 2023. VW ID.4, Audi Q4-etron and VW ID.3 are the top 3 best-selling models of the group, accounting for nearly 50% of the group’s total BEV sales.

* Our present analysis takes Pure Battery EVs (BEVs) into account. We have removed Plug-in Hybrid EVs (PHEVs) from our analysis to avoid confusion.

For our detailed research on the global EV sales market in Q2 2023, clickhere.

For a more detailed electric vehicle model sales tracker, click below:

Global Passenger Electric Vehicle Model Sales Tracker: Q1 2018 – Q2 2023

This report tracks the global passenger vehicle sales* by brand and by model across 23 regions (China, USA, Germany, UK, France, Spain, Japan, India, Italy, South Korea, Thailand, Indonesia, Vietnam, Brazil, Argentina, Russia, Malaysia, Philippines, Singapore, ROE, LATAM, MEA and Oceania) quarterly. The report will help to understand regional trends, brand dynamics and type of EV penetration. The period covered in this report is from Q1 2018 to Q2 2023.

*Sales here refers to wholesale figures, i.e., deliveries out of factories by respective brands/companies.

*Under electric vehicles, the report only considers battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs). Hybrid electric vehicles and fuel cell vehicles (FCVs) are not included.

Table of Contents:

• Definition • Pivot Table • Flatfile

Note: Numbers based on passenger vehicles only. For EVs, we consider only BEVs and PHEVs. Hybrid EVs and fuel cell vehicles (FCVs) are not included in this study.

As more and more carmakers are now introducingelectric vehicles(EVs), the battery and its charging and safety have gained the utmost importance. Counterpoint Research’s data showsEVsales crossed 10 million units in 2022. And as more users and fleet owners consider EVs, be it passenger cars, taxis, or even electric trucks, the range anxiety and charging infrastructure are where many are held back. So, what are companies doing to address these issues?

In a discussion with Qnovo, a company that specializes in developing intelligent lithium-ion battery management software, we gained some interesting insights on how it improves the battery performance in EVs. The desired user experience, be it charging or performance that replicates internal combustion engines, is essential for EV adoption. But how are carmakers and battery companies working together to deliver the best experience?

In the latest episode of ‘The Counterpoint Podcast’, hostJeff Fieldhackis joined byQnovoCEONadim Malufto talk about the intelligent battery management platform and more. They discuss topics including EVs, battery charging and performance, safety, and much more. The discussion also focuses on Qnovo’s technology implementation beyond EVs.

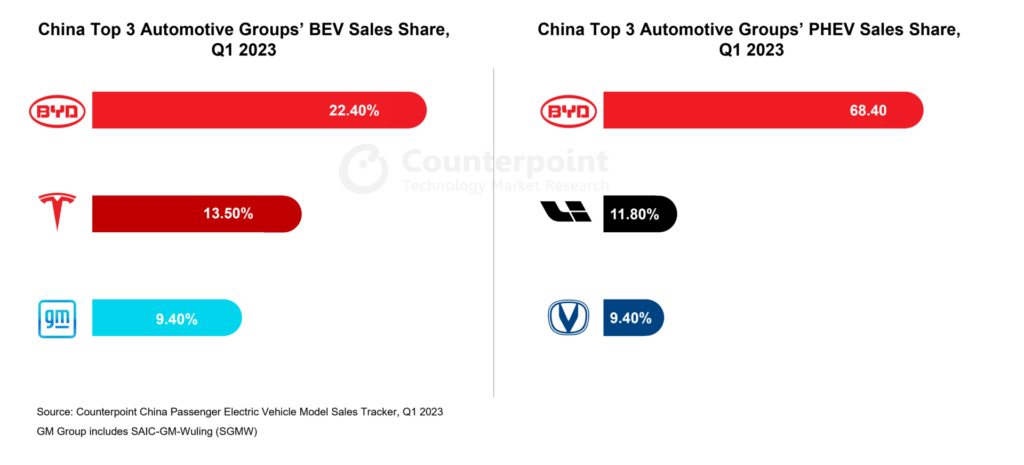

BYD continued to lead China’s increasingly competitive EV market.

The market share of foreign brands declined by 4% points.

EV sales are expected to exceed 8 million units in 2023.

Beijing, New Delhi,London,San Diego, Buenos Aires, Hong Kong, Seoul – June 27, 2023

China’s passenger electric vehicle* (EV) sales grew 29% YoY in Q1 2023, according to the latest research from Counterpoint’sChina Passenger Electric Vehicle Model Sales Tracker.Battery EVs(BEVs) made up nearly70%of the sales. There was a remarkable88% YoYsurge inplug-in hybridEV (PHEV) sales as well. Recently, PHEVs have been experiencing increased popularity in China. BYD secured its leading position with 79% sales growth and 9.8% points increase in market share YoY. Thetop 10 automotive groups, encompassing28 brands, collectively accounted for over80%of the totalpassenger EV sales.

Commenting on the market dynamics,Senior Research Analyst Soumen Mandalsaid, “The discontinuation of the 13-year-old New Energy Vehicle (NEV) purchase subsidy, paired with theTesla-triggered price war, had an adverse impact on domestic EV start-ups. Especially, smart EV brands such asNIO,XpengandNetareported disappointing sales figures compared to the previous quarter. Foreign brands, likeVolkswagen,BMW,Mercedes-Benz,Tesla,HyundaiandNissan, experienced a combined 4% points decrease in market share compared to a year ago. However, Tesla stands out as an exception. Other foreign brands havestruggled to offer strong competitionto domestic brands. Furthermore, Chinese brands such asBYD Auto,Dongfeng Motors,FAW,Great Wall MotorsandGeely Auto冒险超越国内边界建立吗their presence across Europe, Latin America and Asia-Pacific.”

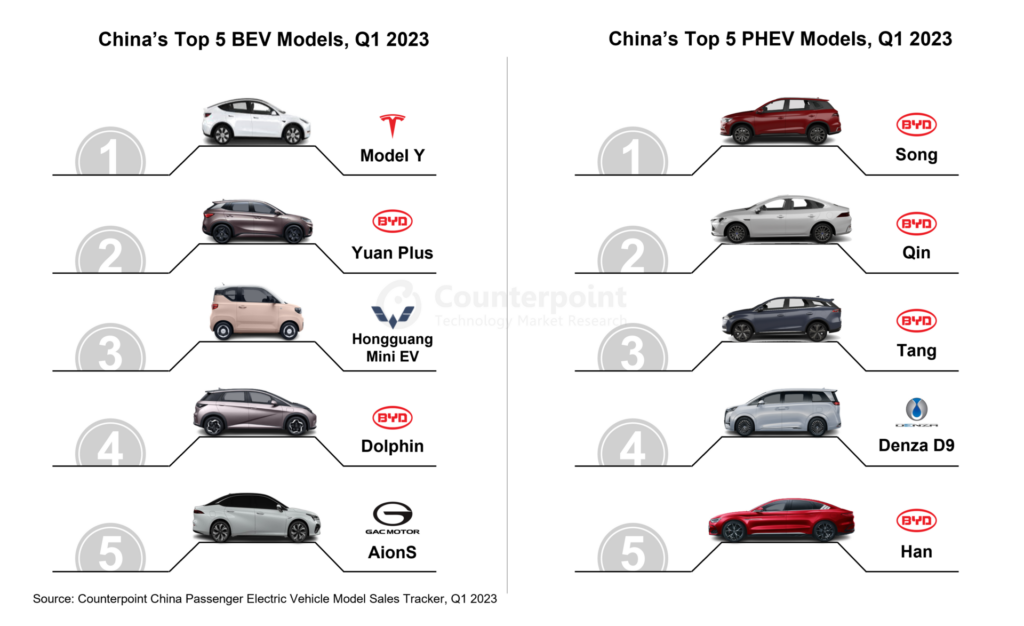

Eight of the top 10best-selling EV models were ofChinese originin Q1 2023. Except Tesla,no foreign modelswere able to secure a position in the top 10. Thetop 10 best-sellingmodelscollectivelyaccounted for46%of China’s passenger EV sales. Moreover, all the top 5 best-selling PHEV models in Q1 2023 were manufactured byBYD Auto.

Discussing the market outlook,Associate Director Brady Wangsaid, “Thegrowth trajectoryof China’s passenger EV market is expected to continuethroughout 2023. Othersupportive policieshave beenimplementedto boost the market’sgrowthafter the elimination of NEV purchase subsidies. In May, China’s Development and Reform Commission released a strategic document aimed at promoting EV adoption in rural areas. This will encourage auto manufacturers to introduce more affordable models, enhance sales systems, and facilitate trade-in services for rural consumers. We expect China’s EV sales toexceed8 millionunits by the end of 2023.”

*Sales refer to wholesale figures, i.e. deliveries from factories by the respective brand/company.

*For EVs, we consider only BEVs and PHEVs. Hybrid EVs and fuel cell vehicles (FCVs) are not included in this study.

Feel free to reach us at press@www.arena-ruc.com for questions regarding our latest research and insights.

Background

市场研究是一个世界人口对位技术l research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

One in every seven cars sold during Q1 2023 was an EV.

Tesla Model Y becomes the best-selling passenger car model globally for the first time ever.

EV sales are expected to reach over 14.5 million units by the end of 2023.

New Delhi,London,San Diego, Buenos Aires, Hong Kong, Beijing, Seoul – June 7, 2023

Global passenger electric vehicle* (EV) sales in Q1 2023 rose 32% YoY, according to the latest research from Counterpoint’sGlobal Passenger Electric Vehicle Model Sales Tracker. One in every seven cars sold during Q1 2023 was an EV. Battery EVs (BEVs) accounted for 73% of all EV sales during the quarter, while plug-in hybrid EVs (PHEVs) made up the rest.

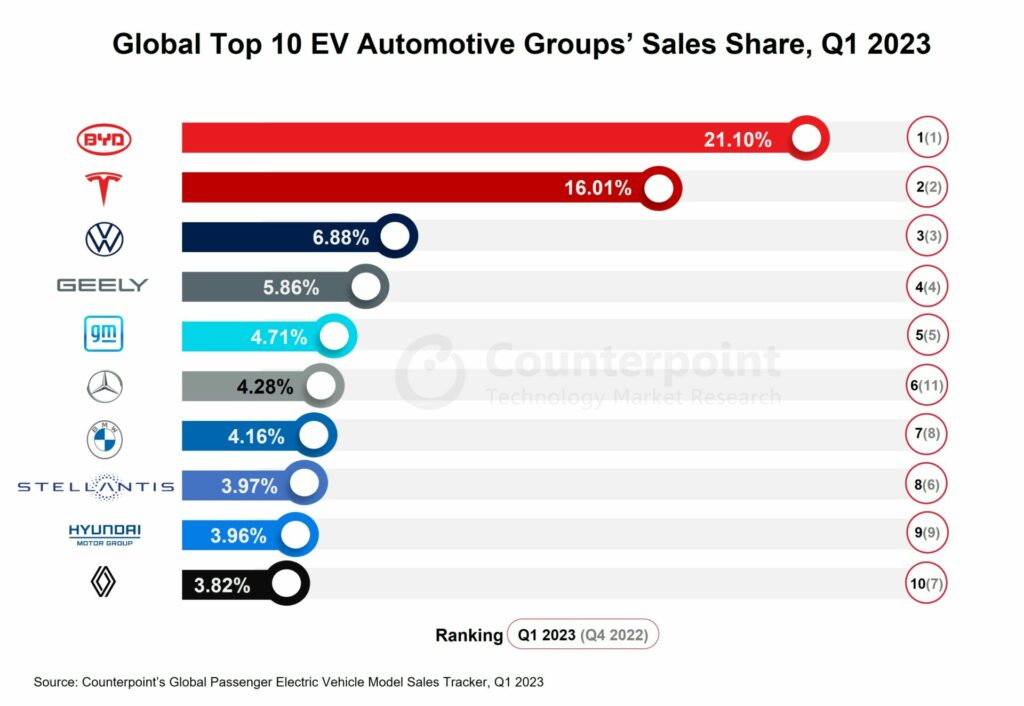

TheUSsurpassedGermanyto become the world’s second-largest EV market in Q1 2023 whileChinaremained theleader. In China, EV sales experienced a remarkable 29% YoY growth, despite a 12% decline in overall sales of passenger vehicles in the country. In the US, EV sales soared over 79% YoY during the quarter. The top 10 automotive groups, encompassing 48 automotive brands, dominated the global EV market in Q1 2023, capturing three-fourths of the total global EV sales.

Commenting on the market dynamics,Research Analyst Abhik Mukherjeesaid, “Global EV sales were largely driven by China with 56% of total EV sales in Q1 2023 coming from this market. The elimination of the NEV purchase subsidy in China resulted in lower-than-expected EV sales in January 2023.Tesla slashed pricesfor its models globally in January, following which other automotive brands announced similar cuts for their car models starting in February, which led to an improvement in EV sales. During February and March, almost 40 automakers, includingBYD,NIO,Xpeng,Volkswagen,BMW,Mercedes–Benz,Nissan,HondaandToyota, reduced their vehicle prices by a couple of hundred dollars to tens of thousands of dollars, which eventually stoked a competitiveprice warin China. Initially, it was thought that the price war would end soon and that auto OEMs would benefit from increased sales. However, as the price war continues to stretch, several automakers in China have reported reduced earnings and even losses.”

Thetop 10 EVmodels accounted for37%of the total passenger EV sales in Q1 2023. Tesla’s Model Y remained the best-selling model globally followed by Tesla’s Model 3 and BYD’s Song. In Q1 2023, Tesla’s Model Y achieved the notable distinction of becoming thebest-sellingpassenger car modelworldwide, surpassing even conventional fuel vehicles.

Commenting on the market outlook,Senior Analyst Soumen Mandalsaid, “Although sales of the traditional internal combustion engine (ICE) vehicles remained stable in Q1 2023 compared with that in the year-ago period, the significant growth in EV sales indicates arapid transitionfrom traditional vehicles to EVs.”

“By the end of 2023, global EV sales are expected to surpass14.5 million units,根据我们的预测。与implementation of the EV tax credit subsidy in the US, EV sales in the country are projected to significantly increase this year. To meet the eligibility criteria for the tax credit, automotive OEMs are moving to partner with battery suppliers and establish battery manufacturing plants across North America. Consequently, the US is poised tosurpassthe EU in the race tobuild EV batteries.”

*Sales refer to wholesale figures, i.e. deliveries from factories by the respective brand/company.

*For EVs, we consider only BEVs and PHEVs. Hybrid EVs and fuel cell vehicles (FCVs) are not included in this study.

Feel free to reach us at press@www.arena-ruc.com for questions regarding our latest research and insights.

Background

市场研究是一个世界人口对位技术l research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

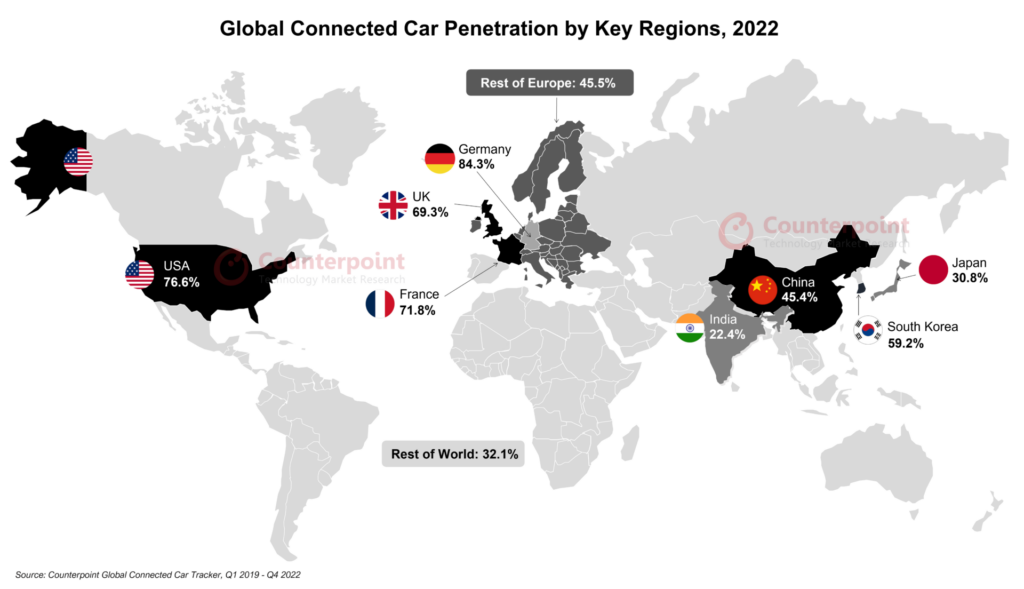

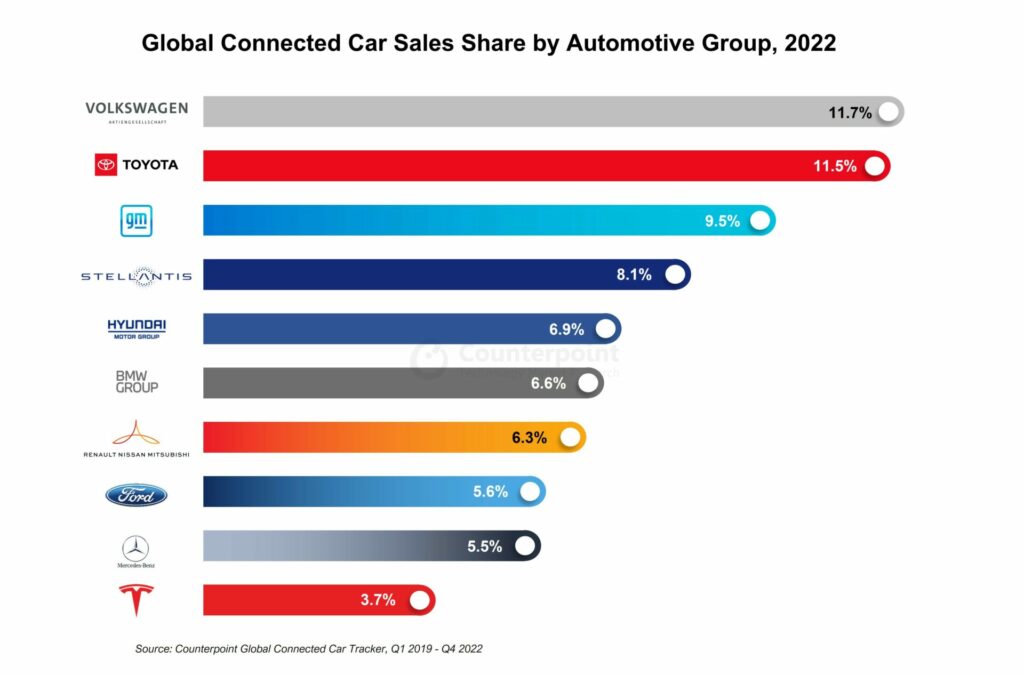

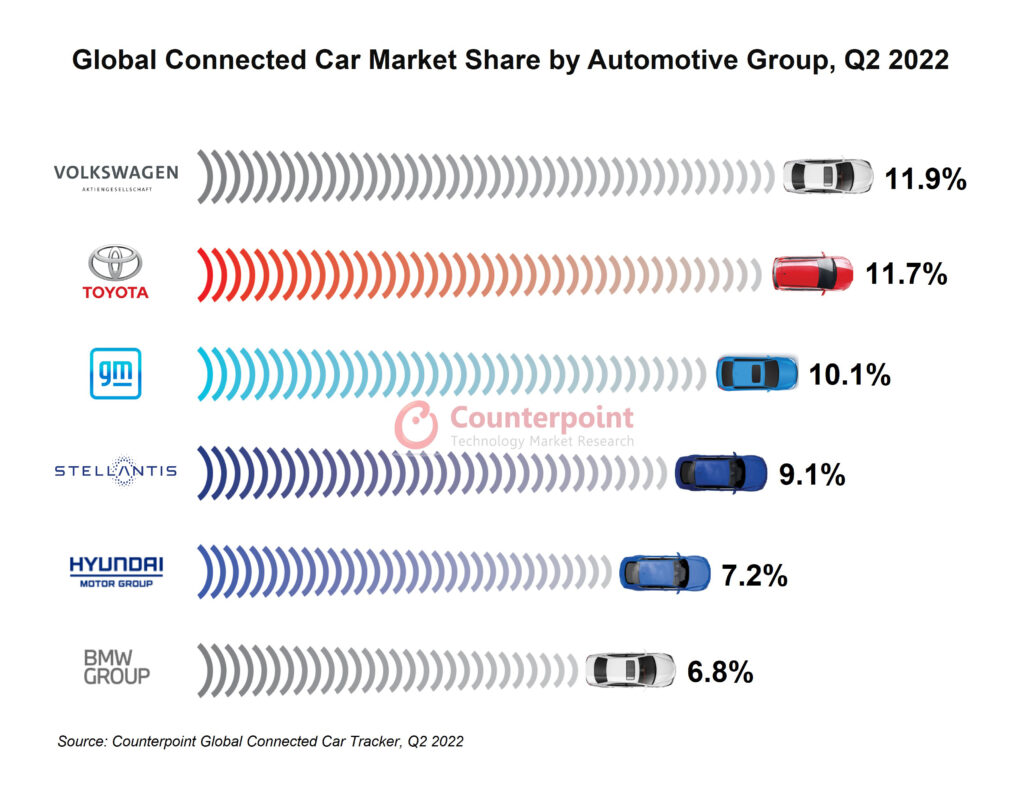

Volkswagen Group led in connected car sales, closely followed by Toyota Group.

4G cars captured more than 95% of connected car sales in 2022.

Tesla broke into the top-10 connected car sales rankings for the first time.

New Delhi,London,San Diego, Buenos Aires, Hong Kong, Beijing, Seoul – April 24, 2023

Global connected car sales* grew 12% YoY in 2022 with the share of connected cars in the overall car sales exceeding 50%, according to the latest research from Counterpoint’sSmart Automotive Service. TheUSremained the strongest market for connected cars followed by China andEurope. These three markets accounted for nearly 80% of the total connected car sales globally in 2022. Despite having a relatively small share of connected car sales, Japan experienced the highest growth in connected car penetration.

Commenting on the market dynamics,Research AnalystAbhilash Guptasaid, “The penetration of connectivity in cars improved during 2022 after struggling in 2020 and 2021. In 2022, new facelift versions of older models like the Honda Civic, Toyota Corolla, Ford Escape and Chevrolet Equinox were introduced with upgraded 4G connectivity and new features. Some prominent features include remote lock/unlock, remote engine start/stop, climate control, vehicle status, location tracking, geofencing, emergency assistance, in-cabin music, video streaming, and over-the-air updates. Next-generation vehicles are being introduced with various connected and autonomous features that require high-speed internet access available through 5G. However, as of now, 5G remains a niche, available only in premium cars like the Ford F-150 Lightning, Cadillac LYRIQ, Mercedes-Benz EQS, Audi e-tron GT, BMW iX and GWM Haval HG.”

Gupta added, “With consumers’ focus shifting to connectivity in the car, non-connected car shipments are steadily declining. The top five automotive groups accounted for nearly half of the connected cars sold in 2022. Volkswagen Group led the charts in terms of connected car sales volume, closely followed by Toyota Group. Tesla broke into the top 10 for the first time.”

Commenting on the market outlook,Senior AnalystSoumen Mandalsaid, “The shift towards digitization in cars is increasing at a rapid pace and is visible in the consistent rise of connected car penetration globally. Currently, 4G dominates the connected car market with almost95%share. But as the automotive market is transitioning towards electrification, software-defined vehicles and autonomy, the need for seamless and faster in-vehicle connectivity will be fulfilled through 5G. By2030, more than 90% of connected cars sold will have embedded 5G connectivity. Connected car sales are expected to grow at a CAGR of 13% between 2022 and 2030.”

*Sales here refer to wholesale figures, i.e. deliveries out of factories by respective brands, and consider only passenger cars with embedded connectivity.

The comprehensive and in-depth ‘Global Connected Car Tracker,Q1 2019-Q4 2022’ and ‘Global Connected Car Forecast, 2019-2030F’ are now available for purchase atreport.www.arena-ruc.com.

Feel free to reach us at press@www.arena-ruc.com for questions regarding our latest research and insights.

Background

市场研究是一个世界人口对位技术l research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

We will be attending CAEV EXPO 2023from 13th-14th April 2023

Our Research Vice PresidentNeil Shahwill be moderating a panel discussion at the CAEV EXPO 2023 on April 14. Our Senior AnalystSoumen Mandaland Research AnalystsAbhik MukherjeeandAbhilash Guptawill be attending the event. You can schedule a meeting with them to discuss the latest trends in the technology, media and telecommunications sector and understand how ourleading researchandservicescan help your business.

Title:Where is India in the CASE Mobility Space? Date:Friday, April 14, 2023 Time:4:15 – 5:00 pm Location:KTPO, Bengaluru

Panelists include:

Moderator:

Neil Shah, Partner & Vice President, Research, Counterpoint Research

Illustrious and exploratory journey for new frontiers in road mobility by Telematics Wire dates back to 2011. Recognising the potential of emerging technologies in mobility space, GPS industry handbook and ‘Vehicle Tracking and Navigation’ conference & exhibition were then pioneer media initiatives taken by Telematics Wire in building up a connected ecosystem within the automotive industry.

Foreseeing emergence of connected vehicle technology in the horizon of Indian automotive industry, 2015 saw the landmark shift in the form of a focussed conference and exhibition ‘Connected Vehicle 2015”. Rest is history. Connected Vehicle (CV) concept soon got aligned to connected and autonomous vehicle with consistent and continuous development of the annual forum of Telematics Wire with yearly International Conferences and Exhibitions.

To get live CAEV EXPO 2023 updates you can watch this space or follow us on TwitterFollow @CounterPointTR

Click here(or send us an email at contact@www.arena-ruc.com) to schedule a meeting with Neil Shah.

EV sales during 2022 were over 10.2 million units, a 65% YoY growth.

7 out of the top 10 EV models were from Chinese brands in Q4 2022.

EV sales are expected to reach nearly 17 million units by the end of 2023.

New Delhi,London,San Diego, Buenos Aires, Hong Kong, Beijing, Seoul – March 6, 2023

Global passenger electric vehicle* (EV) sales in Q4 2022 rose by 53% YoY to bring the 2022 total to over 10.2 million units, according to the latest research from Counterpoint’sGlobal Passenger Electric Vehicle Model Sales Tracker. During Q4 2022, battery EVs (BEV) accounted for almost 72% of all EV sales, while plug-in hybrid EVs (PHEVs) accounted for the rest. The top three EV markets were China, Germany and the US. The top 10 EV automotive groups, which hold more than 39 passenger car brands, contributed to almost 72% of all EV sales in Q4 2022.

Commenting on market dynamics,Research Analyst Abhik Mukherjeesaid, “EV sales were at an all-time high during Q4 2022. The annual total for 2022 would have reached close to 11 million units had fresh COVID-19 infections not surfaced in China.COVID-19 infections in Chinaduring November and December affected automotive production and sales and disrupted the component supply chain. Despite these headwinds, Chinese brands managed to record strong growth. In fact, in 2022, many Chinese brands started to expand in markets like Europe, Southeast Asia and Latin America. Chinese brands are likely to dominate inSoutheast Asiaand Latin America as there are very few brands operating in these regions. But a fight for market presence is expected in Europe.”

Thetop 10 EVmodels accounted for one-third of the total passenger EV sales in Q4 2022. Tesla’s Model Y remained the best-selling model globally followed by BYD’s Song. The Model Y also became the top-selling model in Europe for two consecutive months in Q4 2022. 7 out of the top 10 best-selling EV models in Q4 2022 were from BYD and Wuling. These two brands predominantly operate in China, highlighting the positive evolution of the country’s EV market.Discussing the market outlook,Senior Analyst Soumen Mandalsaid, “EVs are becoming mainstream faster than expected. By the end of 2023, EV sales are expected to reach nearly 17 million units. This year, the US’ EV sales will see aboostas models become slightly more affordable due to the $7,500 tax credit. The end of the purchase subsidy in China might push EV manufacturers to increase their prices. BYD has already implemented one price hike in January. But these price hikes are unlikely to affect EV sales in one of the most matured EV markets. Lithium prices are also expected to come down during the second half of 2023, which will benefit EV sales.”

*Sales refer to wholesale figures, i.e. deliveries from factories by the respective brands/companies.

*For EVs, we consider only BEVs and PHEVs. Hybrid EVs and fuel cell vehicles (FCVs) are not included in this study.

Feel free to reach us at press@www.arena-ruc.com for questions regarding our latest research and insights.

Background

市场研究是一个世界人口对位技术l research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

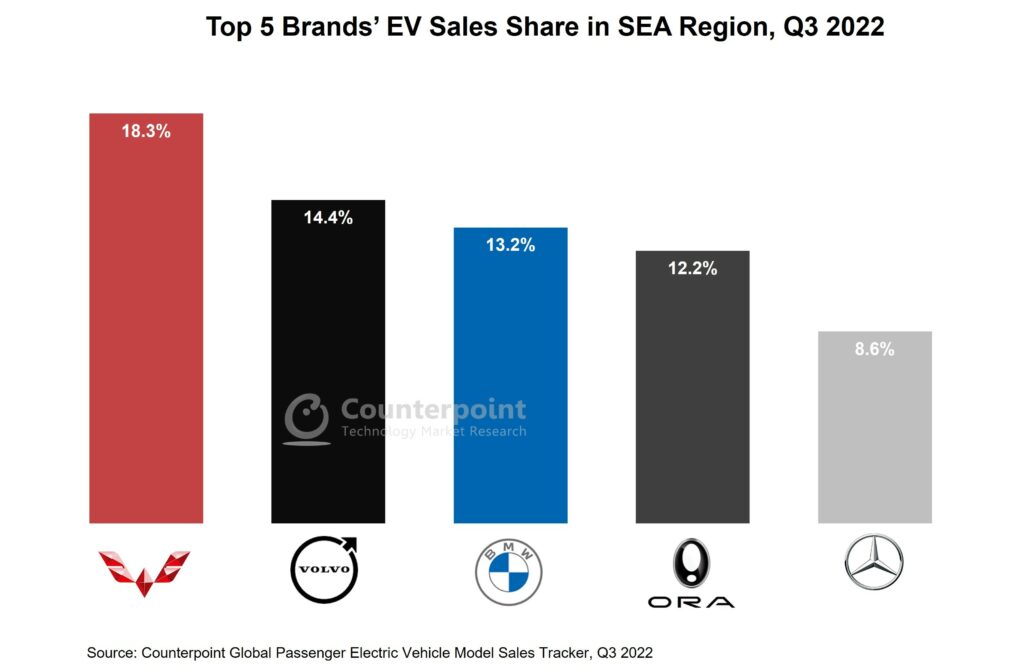

Southeast Asia’s electric vehicle sales grew 35% YoY in Q3 2022.

The top five brands accounted for almost 67% of the region’s passenger EV sales.

The sales are expected to cross 3.5 million units by 2030 at a CAGR of 124%.

New Delhi,London,San Diego, Buenos Aires, Hong Kong, Beijing, Seoul –December 21, 2022

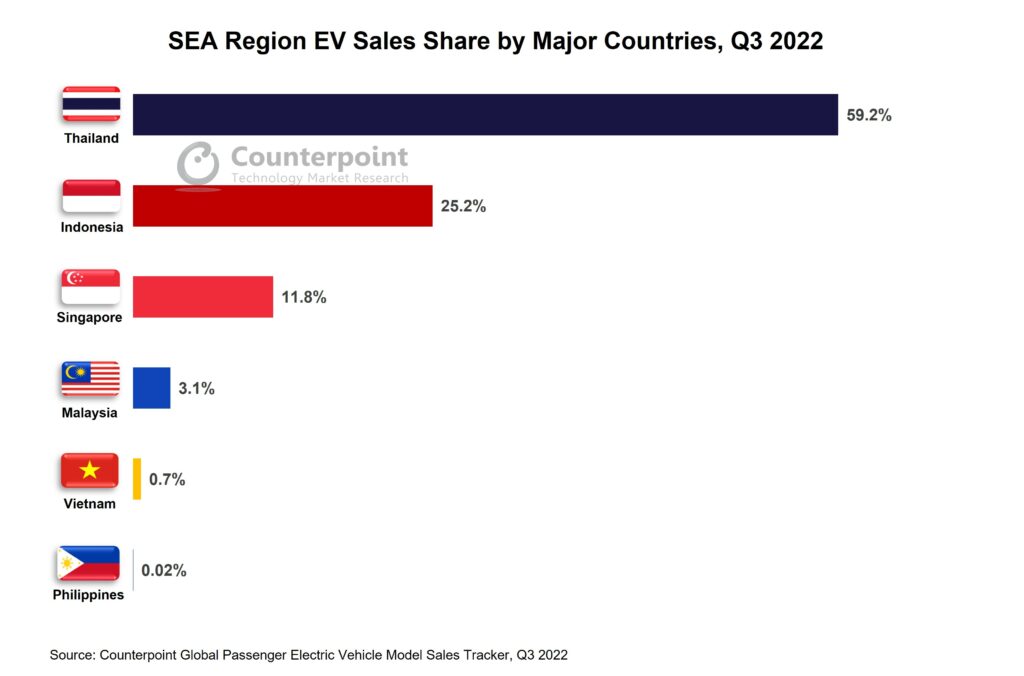

Passenger electric vehicle (EV*) sales** in Southeast Asia (SEA)#grew 35% YoY in Q3 2022, according to the latest research from Counterpoint’sGlobal Passenger Electric Vehicle Model Sales Tracker. Thailand registered the highest EV sales volume in the region, capturing almost 60% share, followed by Indonesia and Singapore. Battery EVs (BEVs) constituted 61% of the sales and plug-in hybrid EVs (PHEVs) the rest. The top five brands accounted for almost 67% of the EV sales in SEA.Wulingemerged as the best-selling EV brand followed by Volvo and BMW.

Commenting on the market dynamics,Research Analyst AbhilashGuptasaid, “Although thepassenger EV salesin SEA are small compared to other regions, the demand is gradually increasing. Currently, EV sales are just a tad over 2% of total passenger vehicle sales in the region. Many OEMs are setting up or are planning to set up manufacturing plants across the region due to favorable policies, subsidies and incentives by major SEA countries like Thailand, Indonesia, Singapore and Malaysia.”

Market summary

Thailand’s EV market has grown tremendously this year, making it SEA’s undisputed EV leader. The country grabbed almost 60% of EV sales in SEA in Q3 2022. It aims to achieve 100% domestic sales from BEVs by 2035. Subsidies, excise duty waivers and import tax reductions have put Thailand on the right path in its EV journey.

Indonesiatook 25% share in the SEA passenger EV market sales for Q3 2022. Also, during Q3, the country registered its highest EV sales volume till now. The Wuling Air EV model launched during this quarter became an instant hit here and was the best-selling EV model. Recently, many companies have announced plans for setting up EV battery production units in Indonesia, which is in line with the country’s target to build 140 GWh of battery capacity by 2030. Indonesia is a major player in vehicle production in SEA.

Singapore,another growing EV market, captured almost 12% share of the SEA EV sales. It has a target to achieve 100% zero-emission vehicle sales by 2030 and has introduced various incentives, policies and schemes to increase EV adoption. Alongside, it is also trying to develop a well-connected network of 60,000 charging points by the end of this decade.

Malaysiaonly had a 3% share in the SEA EV market in Q3 2022. Nonetheless, the Malaysian government is supporting the adoption of EVs and has exempted EVs from road, import, excise and sales taxes. Further push to develop charging infrastructure will boost EV sales.

Vietnamannounced zero registration fee for EVs in March 2022. Vinfast, the major EV brand, recently discontinued its ICE models to focus on EVs. The future looks promising for the EV market to flourish in Vietnam.

Commenting on the market outlook,Senior Analyst Soumen Mandalsaid, “The SEA region’s automotive sector is mainly occupied by Japanese OEMs. However, with the shift in focus to EVs, they are facing stiff competition from theChinese, South Korean and few local players. Affordability remains a major bottleneck for the region’s EV growth. But the scenario is changing with the availability of some cheaper EV options by Wuling, BYD, GWM and SAIC. Unlike developed EV markets such as the US andEurope, low-priced EV options are gaining popularity in emerging markets like Thailand and Indonesia. According to Counterpoint’sGlobal Passenger Vehicle Forecast, the SEA EV market is expected to grow at a fast pace and by the end of this decade EV sales are expected to cross the 3.5-million mark at a CAGR of 124%.”

*For EVs, we consider only BEVs and PHEVs. This study does not include hybrid EVs and fuel cell vehicles (FCVs).

**Sales refer to wholesale figures, i.e. deliveries from factories by the respective brands/companies.

#SEA here includes Indonesia, Malaysia, Myanmar, Philippines, Singapore, Thailand and Vietnam.

Feel free to reach us at press@www.arena-ruc.com for questions regarding our latest research and insights.

Background

市场研究是一个世界人口对位技术l research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

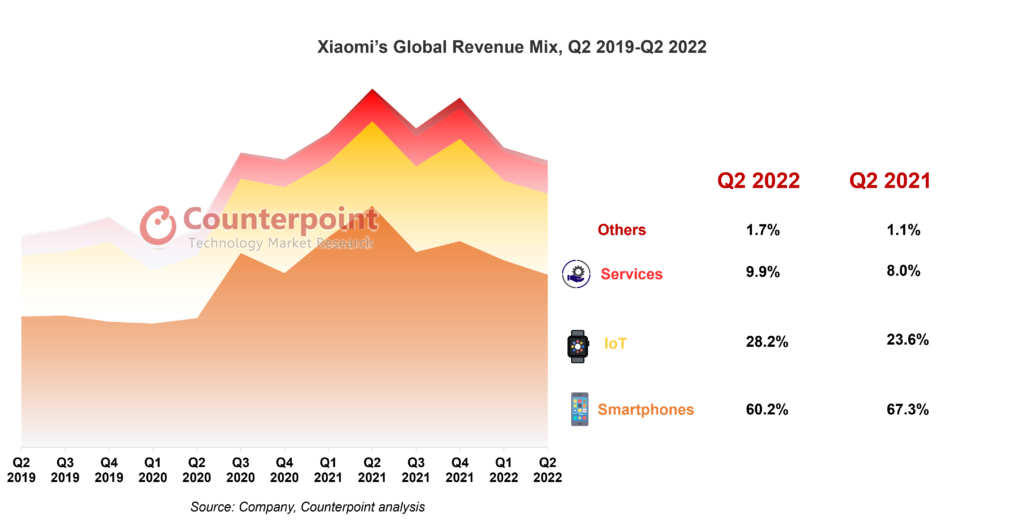

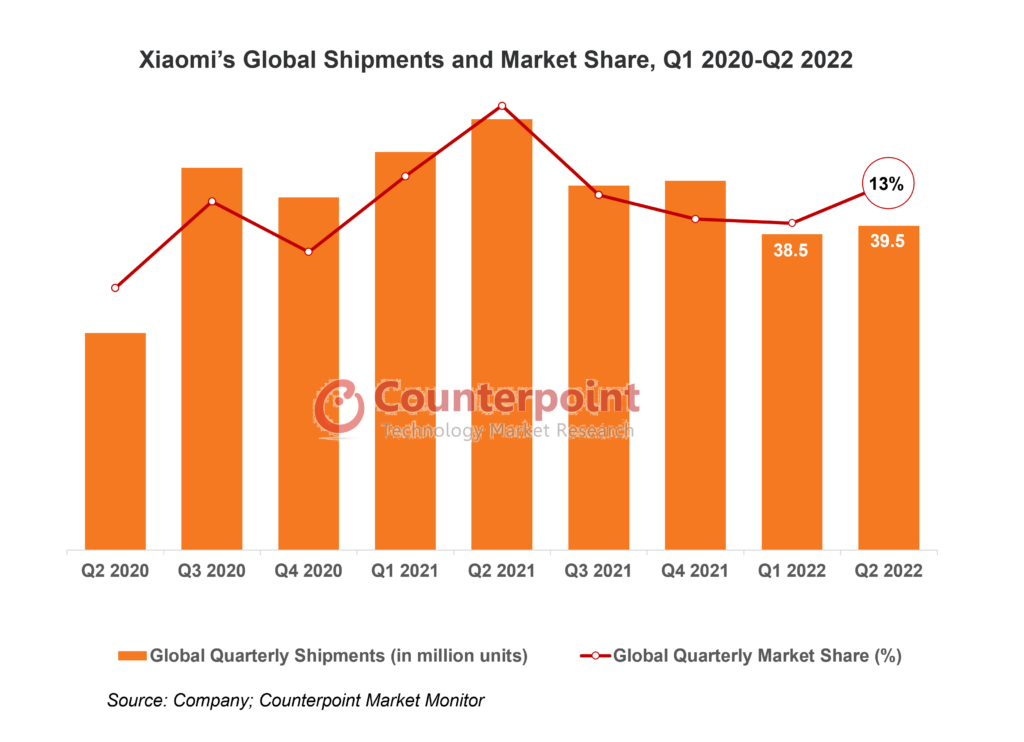

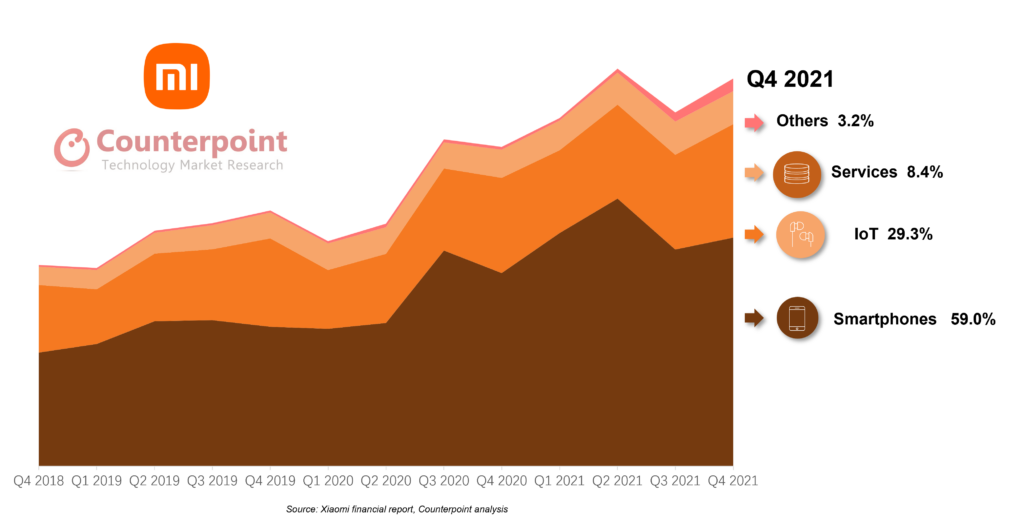

Xiaomi has reported a decline of 9.7% YoY in its Q3 2022 revenue at RMB 70.5 billion (or $9.8 billion). But it stayed largely flat in QoQ terms. The revenue decline was attributed to a slowdown in the company’s three major segments – smartphones, AIoT and internet services.

The smartphone segment suffered the most severe decline among the three, with revenue down 11.1% YoY. Based on Counterpoint’sMarket Monitor Service, Xiaomi’s shipments were down 8.8% YoY in Q3 2022 with a global market share of 13.4%. The decline in shipments was also accompanied by a decrease in the average selling price (ASP). Xiaomi’s smartphone ASP declined 2.2% QoQ from RMB 1,081.7 (or $ 151) per unit in Q2 to RMB 1,058.2 per unit (or $148) in Q3 due to promotional activities in overseas markets to clear out inventory, offsetting the increase in ASP in China’s market.

The smartphone market continues to face headwinds both in China and globally. In Xiaomi’s home market, ongoing COVID-19 restrictions on mobility and weak economic environment have led to sluggish smartphone sales throughout 2022, which is expected to register a double-digit YoY decline, according to Counterpoint’s estimates. The frequent lockdowns across the country are impacting Xiaomi’s strategy to grow its offline channels, which is seen as a key weakness of the company when compared to OPPO and vivo. Coupled with fierce competition from local players OPPO, vivo and HONOR, as well as Apple’s latest series, Xiaomi’s market position dropped one rank to reach fifth inQ3 2022.

Commenting on Xiaomi’s overseas smartphone business in Q3 2022,Research Analyst Mengmeng Zhangsaid, “Overseas shipments accounted for more than 75% of Xiaomi’s total shipments. The sluggish macro environment, inflation and foreign exchange fluctuations have also taken a toll on Xiaomi’s sales in the overseas market. On the bright side, we see that Xiaomi is continuously growing its market share in Europe, Latin America and Middle East.”

Xiaomi’s inventory level in China has normalized after the mid-year ‘618’ shopping festival in Q2. However, to clear its inventory for the global market, the company will have to wait till at least Q4, when festive season promotions are launched.

Xiaomi continues to invest heavily in R&D, with the company’s R&D personnel accounting for 48% of its total employees. Xiaomi’s R&D expenditure also grew 25.7% YoY to RMB 4.1 billion (or $0.57 billion) in Q3. More than RMB 829 million (or $116 million) went to new businesses including EV. Xiaomi’s EV business is still in the early stages of development. It is unclear at the moment whether the company will emerge as a leading player in China’s competitive auto market.

Xiaomi’sIoTand lifestyle products segment saw a 9% YoY decline and 4% QoQ decline in Q3. The slowdown in this segment is largely due to weak consumer sentiment. Commenting on the performance of this segment,Senior Analyst Ivan Lamsaid, “The IoT and lifestyle products remain an important segment for Xiaomi, accounting for 27% of its revenue during the quarter. Despite the segment’s slowing growth, Xiaomi made strong progress in the smart large appliances, such as air conditioners, refrigerators and washing machines, with revenue growing 70% YoY. Smart large appliances are necessities that can better withstand economic downturns. We expect the innovative features of Xiaomi’s smart large appliances to continue to drive demand, especially among younger customers, and become a larger contributor to the IoT and lifestyle products segment.”

Internet servicesrevenue was also muted, declining 3.7% YoY while growing 1.4% QoQ. The segment was particularly hurt by slower China advertisement demand despite growth in overseas markets.Research Analyst Archie Zhangsaid, “Although the monthly active users of MIUI have reached record highs both globally and in China, monetizing the traffic is challenging during the difficult macro environment and will likely carry through to 2023.”

Xiaomi Q2 2022 Update

Global Smartphone Market Downturn Impacts Xiaomi Numbers

August 23, 2022

Xiaomi’s latest financial numbers fully demonstrate the impact of the global smartphone market downturn in Q2 2022. The company’s revenue dropped 20.1% YoY to RMB 70.2 billion (or $10.3 billion) during the quarter. Most of this decline came from the company’s smartphone unit, which dropped 28.5% to RMB 42.3 billion ($6.2 billion). According to Counterpoint’sMarket Monitor Service, Xiaomi’s shipments were down 25% in Q2 2022 with a market share of 13.4%, the third highest after Apple and Samsung.

Xiaomi’s revenue distribution appeared more diversified in Q2 2022 than it was in the same period last year as the non-smartphone units recorded fewer declines in Q2 2022.

Commenting on Xiaomi’s smartphone business in Q2 2022,Senior Analyst Ivan Lam说,“在Q2,小米的智能手机业务是汉堡eezed by Samsung overseas and HONOR in home market China. After the mid-year ‘618’ shopping festival, Xiaomi’s inventory situation in China eased and returned to a normal level. However, inventory issues still haunt Xiaomi in other regional markets as global inflation and the looming macroeconomic recession keep customers from purchasing or replacing smartphones. In China, HONOR’s strong momentum also pressured Xiaomi’s smartphone sales in Q2. Xiaomi’s shipment share ranked fourth in China while HONOR took the top spot. Looking forward, we believe the Chinese smartphone market is bottoming out but not before realizing a double-digit decline in 2022. The global market will contract too. Xiaomi is slowing down expansion offline, which will weaken its ability to take on the competition in China. The headwinds faced by Xiaomi’s main business are far from over.”

智能手机oem厂商面临的库存问题,including Xiaomi, have been under the spotlight this year. There have been reports of OEMs slashing production orders, canceling component purchases and adjusting shipment targets for 2022. According to Counterpoint’s analysis of Xiaomi’s financial report, the company’s inventory turnover days edged higher in Q2 2022. But as the inventory level in China has been lowered, we think Xiaomi may embark on relatively aggressive sales promotion campaigns in other regional markets.

Xiaomi continues to invest in the long term. The company’s R&D expenditure grew 22.8% YoY to RMB 3.8 billion ($0.56 billion) in Q2. More than RMB 611 million went to new businesses including EV.

Founder and CEO Lei Jun said Xiaomi’s EV would go into mass production in the first half of 2024. This means the company still needs one-and-a-half years to see its new growth engine start running. Commenting on Xiaomi’s EV ambition,Research Analyst Archie Zhangsaid, “EV is a brand-new business for Xiaomi. Therefore, its smartphone business needs to generate enough profits to sustain the growing ADAS and digital cockpit R&D expenditure. Xiaomi has a great advantage over car OEMs, especially since it knows what tech-savvy customers are looking for. But our research shows EV customers still prioritize safety over other factors such as in-car entertainment. That is why established car OEMs like BYD and Volkswagen still dominate EV sales in China, according to our data. Xiaomi may need a couple of more years to prove that its EVs are stable and secure to win over a considerable market share.”

Xiaomi Q1 2022 Update

Xiaomi’s 4.6% YoY Revenue Decrease in Q1 2022Signals Turbulence in Smartphone Segment

May 23, 2022

Xiaomi registered a 4.6% YoY and 14.3% QoQ decline in its Q1 2022 revenue, something which was being expected. The result can be mainly attributed to the decline in its smartphone sales globally. The company’s smartphone business, which is its biggest, recorded an 11.1% YoY decline. Xiaomi’s global smartphone shipment share has been declining through the past three quarters, from the highest point of 16% in Q2 2021 to 12% in Q1 2022, according to the latestCounterpoint Market Monitordata. Shipments have hit their lowest point since Q3 2020.

With the ongoing shortages of key components such as 4G SoC, COVID-19 resurgence in some regions, and global macroeconomic headwinds, Xiaomi’s smartphone shipments declined 20.6% YoY in Q1 2022 against the global decline of 8.1% and China market decline of 18.1%, according to Counterpoint’s Market Monitor data.

Commenting on Xiaomi’ssmartphone sales, Senior Analyst Ivan Lam said, “Q1 is usually a seasonal low point for all OEMs. But Xiaomi’s smartphone sales declined more than the market. Historically, Xiaomi built its base with entry-level and budget mid-end smartphones such as the Redmi 9A/9C and the Redmi Note series. Therefore, the LTE chipset shortage weighed on Xiaomi’s performance in the lower-end segments. However, we can also see theASP(average selling price) for Xiaomi’s phones increasing to CNY 1,189 (around $176), which may be the only thing to cheer about in its Q1 2022 numbers.”

Xiaomi’s cost of smartphone sales decreased by 8.1%, primarily due to the reduction in sales, partially offset by an increase in average cost of sales due to a higher proportion of mid-range and premium smartphone shipments. Commenting on the sales activities,Lamsaid, “Xiaomi had a bumpy ride in its offline channel expansion in China. After spending big amounts along with offline partners, Xiaomi saw no change in its share of offline sales. To make matters worse, Xiaomi now has a high inventory, especially of mid-to-high-end and high-end smartphones. This has pushed Xiaomi to spend more on promotion activities. We observed that its number of inventory turnover days at the end of Q1 2022 was much higher than in Q1 2021. A high inventory is a danger sign for Q2 2022 as COVID-19 lockdowns are on in some major Chinese cities, reducing people’s ability to purchase new smartphones.”

Xiaomi’sIoTand lifestyle products segment saw a 6.8% YoY increase and 22.3% QoQ decrease in Q1 2022. The company’s TV product sales in China lead the show for this segment, retaining the No. 1 spot in the home market for 13 quarters now. Commenting on the performance of this segment,Senior Analyst YangWangsaid, “With 26.6% of the total group revenue, IoT and lifestyle products are a major revenue contributor. However, the segment is not making much money compared to the smartphone segment. And the increase in the profit is mainly attributable to the decreased price of key components such as display panels. In wearable products too, Xiaomi has seen disappointing results. Though it is the leading smartphone brand in India, Xiaomi’s TWS and smartwatch models have not been able to enter the top five brands lists. India’s TWS and smartwatch shipments grew 66% and 173% YoY respectively in Q1 2022 but still, Xiaomi was left out. It could have done better in its second-biggest revenue contributor.”

Xiaomi’sinternet servicesbusiness grew to 9.7% of the company’s total revenue in Q1 2022, registering an 8.2% YoY increase and 2.2% QoQ decrease. The QoQ decrease is due to poor smartphone sales. Commenting on Xiaomi’s internet services segment,Research Analyst Archie Zhangsaid, “Xiaomi’s internet services segment is continuously bringing positive news against the backdrop of Google grabbing a big portion of such revenue in overseas markets. Xiaomi just passed the500-million installed basemark to join Samsung and Apple, but it needs to take innovative approaches to monetize the traffic from its products sold overseas.”

In its financial statement, Xiaomi had little information to share on its smart electric vehicle project, the R&D spending on which stands at 12.2% of the overall R&D expense. The statement also mentioned an ongoing investigation by India’s government into some allegations against the company.

Xiaomi Q4 2021 Update

Xiaomi Wraps Up 2021 on a Strong Footing, Despite Challenges

March 23, 2022

我连续增加总收入9.6%n Q4 2021, Xiaomi has partially recovered from its underwhelming performance in Q3. In terms of segment performance, its smartphone revenues increased 18.4% YoY. IoT and Lifestyle products and Internet services also saw 19.1% and 17.7% YoY increases respectively.

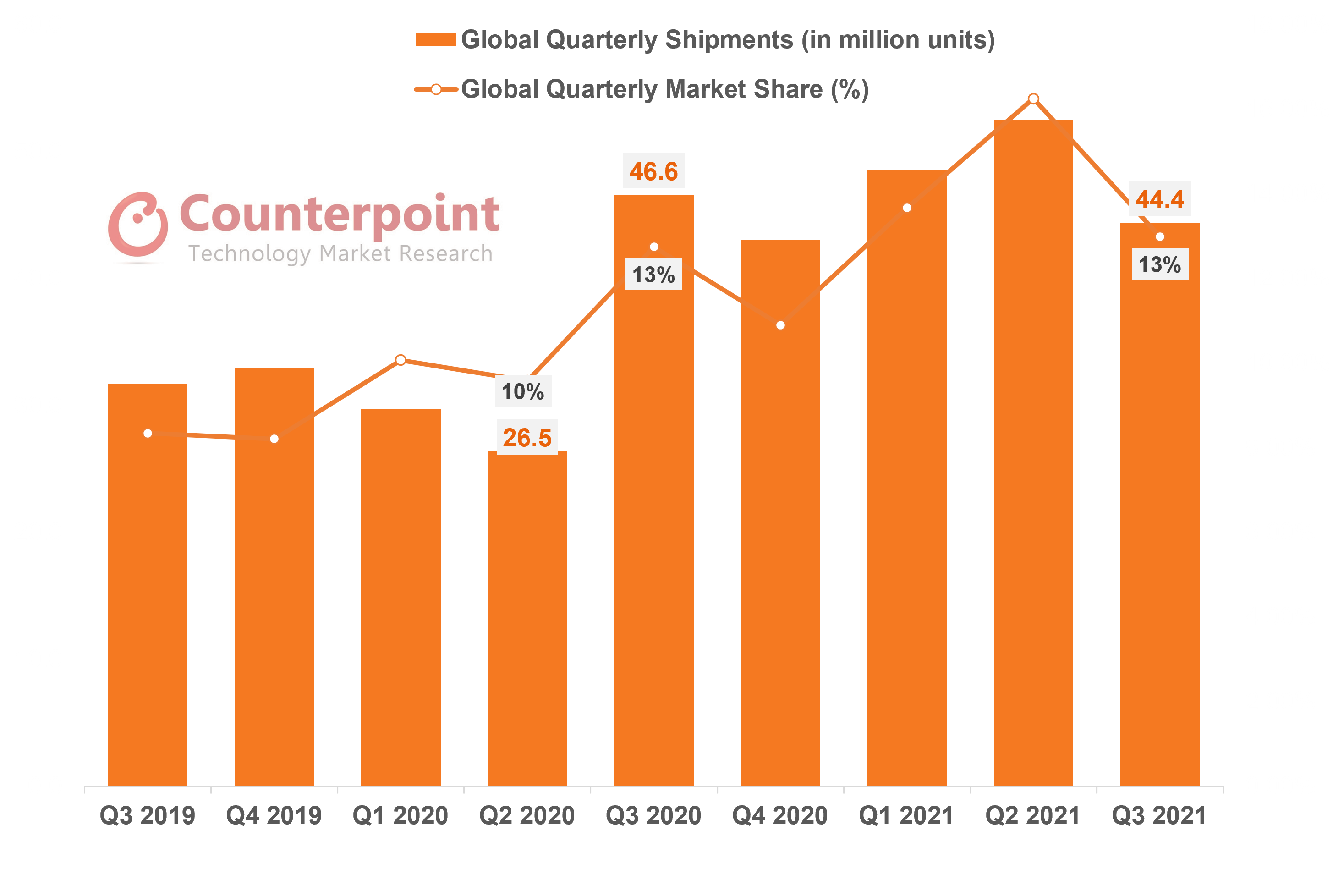

The company’s latest financial data is also in line withCounterpoint’s Market Monitordata, which shows Xiaomi’s smartphone shipments increased 4.7% YoY and 1.4% QoQ in Q4 2021. The slower increase in smartphone shipments growth as compared to revenue growth illustrates that Xiaomi has made fairly good progress upgrading its portfolio and improving its smartphone average selling price (ASP). Correspondingly, Xiaomi’s gross margin from smartphones improved from 8.7% in 2020 to 11.9% in Q4 2021.

Xiaomi’s Global Shipments and Market Share, Q4 2019-Q4 2021

Source: Counterpoint Market Monitor Data

Commenting on Xiaomi’ssmartphone sales,Senior Analyst Ivan Lamsaid, “Counterpoint’s Market Monitor data shows that Xiaomi’s smartphone shipment growth has underperformed the global market total in Q4 2021. Key component shortages, especially in LTE, constrained Xiaomi’s low-end smartphones sales. However, the increase in ASP helped Xiaomi to keep up with revenue growth. The company is moving in the right direction as it has tried to contain the share of entry-level smartphones.”

Xiaomi’sIoTand Lifestyle products segment saw record performance in 2021, with revenue coming in at RMB 25 billion in Q4, up 19% YoY. Commenting on the performance of this segment,Senior Analyst YangWangsaid, “IoT and Lifestyle products are becoming more and more important to leading smartphone OEMs. Those products can be sold into the same channels as smartphones in most regions, and can therefore be boosted by the same marketing halo effect, such as bundled sales, promotions and new product launches. Notably, Xiaomi’sTVs, laptops, tablets, wearables, and home appliances saw good sales, due to Xiaomi’s affordable pricing strategy.”

Last but not least, Xiaomi’s internet services revenue reached a record RMB 7.3 billion in Q4 2021, translating into a growth of 17.7% YoY. This was attributed to the advertising business, as well as a 79.5% YoY growth in overseas markets.

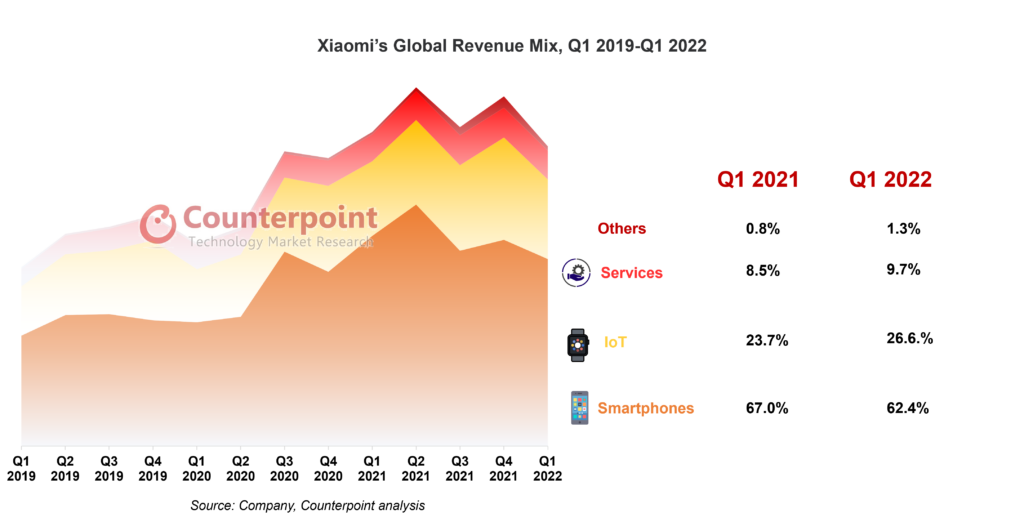

Xiaomi’s Global Revenue Mix and Share, Q4 2018-Q4 2021

During the earnings call, Xiaomi disclosed that revenue from the smartphone segment grew 37%, and was still the biggest contributor to the company in 2021 at 63.6%. Smartphones’ cost of sales remained stable at 56.0% in 2021, as compared to 56.5% in 2020. The cost structure has thus improved by pushing up the ASP.

Internet servicesmade 8.6% of total revenue in 2021. Commenting on Xiaomi’s internet services segment,Research Analyst Archie Zhangsaid, “Xiaomi’s internet services segment has shown decent growth momentum. Notably, overseas services revenues grew 18.8% YoY in 2021. However, Xiaomi faced several challenges, including more stringent regulations around targeted advertising and privacy, and a weak home market due to sluggish performance of the big internet companies in China.”

Xiaomi closed the buy-out of the 50.09% stake of Zimi International Incorporation that it does not already own. By bringing the ‘ecosystem’ company under its control, Xiaomi can boost its offers in accessories such as mobile power banks, wireless chargers, and smart home accessories. Xiaomi also acquired Deepmotion Tech Limited, a company specializing in advanced driver-assistance systems (ADAS) andautomateddriving applications. Xiaomi announced that the mass production of its smart electric vehicle will officially begin in the first half of 2024.

Xiaomi Q3 2021 Update

Xiaomi’s Growth Pegged Back by Component Shortages

November 24, 2021

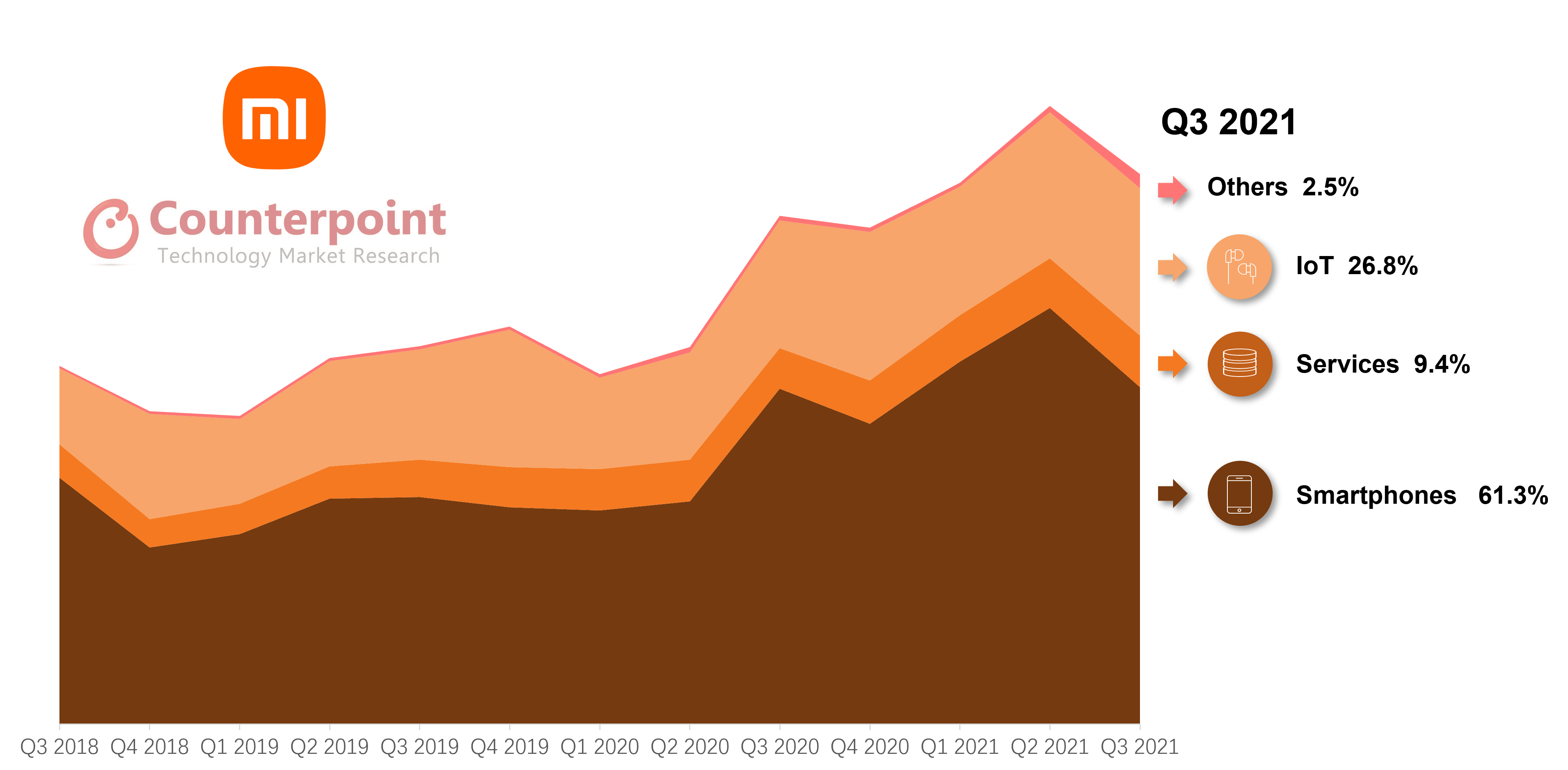

Hit by the ongoing global component shortages, Xiaomi’s smartphone revenues nearly came to a halt in Q3 2021, growing just 0.5% YoY and falling 19% QoQ. Therefore, the strong momentum and fast expansion seen in Xiaomi’s smartphone segment after Huawei’s fall ended after a year. Xiaomi’s internet services segment provided a silver lining but its average revenue per user (ARPU) continued to fall.

The company’s latest financial data is also in line withCounterpoint’s Market Monitordata, which shows Xiaomi’s smartphone shipments dropping 4.7% YoY and 15.3% QoQ in Q3 2021. The slower decrease in smartphone revenue growth compared to shipments illustrates that Xiaomi made fair progress in improving its smartphone average selling price (ASP).

Xiaomi’s Global Shipments and Market Share, Q3 2019-Q3 2021

Source: Counterpoint Market Monitor Data

Commenting on Xiaomi’s smartphone sales,Senior Analyst Ivan Lamsaid, “Counterpoint’s Market Monitor data shows that Xiaomi’s smartphone ASP increased more than 7% YoY to $180 in Q3 2021 but dropped about 3% QoQ. The increase in ASP helped Xiaomi to keep revenue flat from the figure of Q3 2020. Since Xiaomi aims to double down on its premium product strategy, we can expect its ASP to continue to increase. On the other hand, component shortages will also play out, especially for Xiaomi products, which boast to have ultra-low profit margins.”

Xiaomi did have some good news in Q3 2021. The company’s internet services revenue reached a record RMB7.3 billion, translating into a growth of 27.1% YoY and 4.3% QoQ, fastest among all segments.

At an earnings call, Xiaomi disclosed that its overseas services revenue accounted for 19.9% of its whole internet services segment. The share was more than 500 basis points higher from the previous quarter.

Commenting on Xiaomi’s internet services segment,Senior Analyst YangWangsaid, “Xiaomi’s internet services segment has shown a great growth momentum. Especially, the overseas services revenue grew more than 110% YoY in Q3 2021. We believe India will continue to be thekey growth region. The revenue from mainland China will face more uncertainties given sluggish advertising growth at major internet companies. Xiaomi can partner with these internet companies, providing them key data for ad personalization. We think this downturn in China advertising will reflect in Xiaomi’s earnings in the coming quarters.”

Moreover, Xiaomi’s ARPU has dropped for five quarters to RMB15.1. This has been due to the difficulty in competing against Google in the global market. Xiaomi still can’t commercialize data as efficiently as it does in China.

Xiaomi Q2 2021 Update

Smartphone Sales Soar as Company Reports Best Quarter on Record

September 8, 2021

Xiaomi saw a record-setting Q2 2021 with revenues growing 64% and net income surging 80% from the same period a year ago. This performance was driven largely by strong smartphone sales, which reached 52.5 million units in Q2, according to Counterpoint Research’s Market Monitor service.

Smartphone sales growth was broad-based for Xiaomi across most regions. The company has focused on emerging markets such as Southeast Asia, Middle East and Africa, and Latin America, where sales grew 99%, 206% and 229% respectively in YoY terms. Even in the more developed European markets, Xiaomi’s sales grew 109% YoY.

Commenting on Xiaomi’s smartphone product strategy,Senior Analyst Ivan Lamsaid, “Our numbers show the average selling price (ASP) of Xiaomi phones reached the highest ever at $185 in Q2 2021. This is an increase of 7.3% in YoY terms, driven mainly by the performance of premium products such as the Mi 11 series. We expect Xiaomi to double down on premium segments to uplift its brand in home market China, and high ASP markets like Western Europe, where Huawei’s fall has left a vacuum in the premium range.”

Looking at Xiaomi’s revenue growth by business type, the smartphones, services and IoT segments grew 86.8%, 19,1% and 35.9% respectively in YoY terms. The company’s business is now more than ever dependent on its smartphone segment, which accounts for two-thirds of the total revenue.

Commenting on Xiaomi’s services segment performance,Analyst Archie Zhangsaid, “While Xiaomi’s smartphone business performed extremely well, there still is a lot of potential to tap into its services segment. During a period when smartphone sales almost doubled, services revenue growth lagged. The average revenue per user (ARPU) in Q2 2021 actually dropped 10% to RMB 15.5, suggesting that monetizing user traffic on smartphones in new geographies is not as straightforward.”

Within Xiaomi’s services segment, advertising revenue was up 46.2%, while gaming revenue dropped 10.7% and value-added services (VAS) revenue dropped 10.3%. Gaming and VAS are likely to face further pressure due to online gaming and financial services regulatory controls in China. Therefore, advertising will become crucial to Xiaomi’s services success, and we expect it to beef up collaborations with leading internet companies and expand partnerships abroad.

Despite these challenges, the services segment’s gross profit margin soared to 74.1% compared to 60.3% a year ago. With a revenue contribution of only 8%, the segment contributed to 35% of the company’s gross profit. Given the company’s stated intention to keep smartphone margins low, we expect services to continue to do the heavy weightlifting for Xiaomi’s bottom line in the future.

* Key Southeast Asia countries include Indonesia Thailand Philippines and Vietnam

The US overtook China in Q2 2022 to lead the global connected car market.

The top five groups – Volkswagen, Toyota, GM, Stellantis and Hyundai – captured half of the market.

5G car sales surpassed half a million, though 4G accounted for 90% of connected car sales.

London,San Diego, Buenos Aires, New Delhi, Hong Kong, Beijing, Seoul – September 29, 2022

Globalconnected car sales* remained flat YoY in Q2 2022 despite ongoing turbulence in the automotive industry, according to the latest research from Counterpoint’sConnected Car Services.The US led followed by China and Europe. The top three regions accounted for nearly 80% of connected car sales in the quarter.

The connected car penetration surpassed that of non-connected cars for the first time ever, capturing almost 50.5% share in Q2. Non-connected cars have been steadily declining as automakers prefer to upgrade their portfolio with factory-fitted embedded connectivity even in base model variants. Luxury brands like BMW, Mercedes and Audi were the first to introduce connected cars with inbuilt Wi-Fi, even before the initial push towardsconnected vehiclescame from government mandates like eCall.

Commenting on the regional dynamics,Senior AnalystSoumen Mandalsaid, “TheUSmarket trailed China in terms of connected car sales in the first quarter of this year. However, with the resurgence of COVID-19 and plant shutdowns in China from March onwards, the US overtook China.Chinawas the first country to introduce 5G cars back in 2020 with models like the Arcfox Alpha-T, Roewe Marvel R and Great Wall Motors Haval HG. Major automakers such as Audi and BMW entered the market in 2021 and 2022 by launching models like the Audi A7L/A6L and BMW iX respectively. Government initiatives along with a push from state-owned telecom operators regarding the deployment of 5G networks have given China the first-mover advantage.”

Mandal added, “Europe, including major countries like Germany, UK and France, saw its overall sales dip in the first half of the year due to persistent problems like the Russia-Ukraine war and supply chain disruptions. However, the region managed to increase its connected car penetration to almost 60% in the second quarter owing to growing connected car technology in the portfolios of incumbent players like Stellantis, Volkswagen, BMW and Mercedes. From a global perspective, Volkswagen, Toyota and General Motors groups lead the market due to large volumes and high connectivity penetration within their portfolios.”

The automotive industry is going through multiple simultaneous transitions such as connected mobility,electrification,autonomous driving, and software-based services. And connectivity is fundamental for all. However, it is creating pressure on supply chains to support these transitions.

Connected cars surpassing non-connected cars is a significant milestone toward achieving success in the automotive industry transformation. Now the use cases of connectivity within cars are expanding from telematic services to becoming more software-centric, delivering features likedigital cockpitthrough to autonomous driving. As a result, automakers are focusing on using powerful on-board computers for next-generation connected mobility. Currently, connected cars typically use a singleNADmodule to provide infotainment and predictive analytics. But some Chinese brands and luxury automakers are using two NADs in a technology called Dual SIM Dual Active (DSDA) to provide, for example, uninterrupted infotainment to passengers while simultaneously uploading critical vehicle data on to the cloud for analytics.

Keeping the technology evolution in mind,Research Vice-PresidentPeter Richardsonadded, “4G cars still dominate the global connected car market, capturing 90% of shipments in Q2 2022, whereas 5G cars accounted for around 7%. Although 5G’s share will continue to increase, 4G will see increased sales on a yearly basis until 2027. There are several factors hindering the proliferation of 5G for cars, such as high prices of 5G NAD/TCU, and patchy network coverage even where 5G has been launched, which in turn means limited availability of 5G capable cars. Furthermore, there is only nascent adoption ofADAS/AD levels– currently, there are few Level 3 capable models and all use 4G. We expect that mass adoption of 5G connectivity will only occur after 2025, when most of these issues will have been resolved”.

*Sales here refer to wholesale figures, i.e. deliveries out of factories by respective brands, and consider only passenger cars with embedded connectivity.

For detailed research, refer to the following reports available for subscribing clients and individuals:

Counterpoint tracks and forecasts on a quarterly basis around 50 automakers’ sales in key geographies like China, US, UK, Germany, France, Japan, South Korea, Rest of Europe and Rest of World, and by technology/connectivity – 2G, 3G, 4G and 5G.

Feel free to reach us at press@www.arena-ruc.com for questions regarding our latest research and insights.

Background

市场研究是一个世界人口对位技术l research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

In order to access Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not. Personal Information When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

你可以请求终止您的帐户或到凶手scribe to any email subscriptions or mailing lists at any time. In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company. – Passwords are for user’s individual use – Passwords may not be shared with others – Users may not store documents in shared folders. – Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified. Accuracy of Information: While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links: This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience. This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.

Global Passenger Electric Vehicle Market Share, Q3 2021 – Q2 2023

Global Passenger Electric Vehicle Market Share, Q3 2021 – Q2 2023