- 2022 was a record-breaking year for NXP with solid profit growth and healthy free cash flow generation.

- Accelerated growth drivers (except UWB) are on track within the expected revenue growth range (∼25%) to help take NXP’s total revenue to $15 billion by 2024.

- For Q1 2023, the company expects revenue of about $3 billion. This would mean a deceleration of 4% YoY with a 9% downside sequentially.

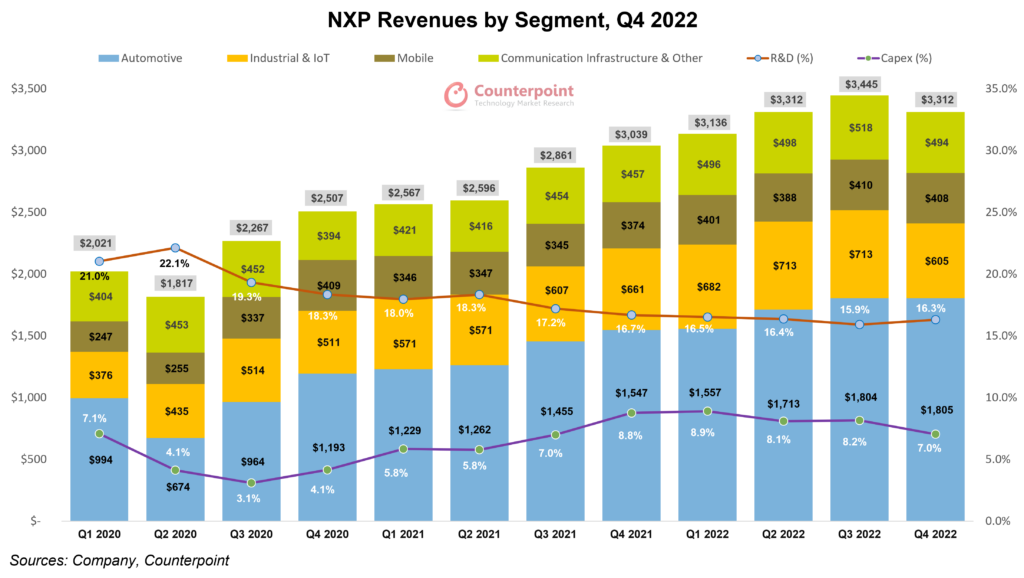

NXPSemiconductors reported record revenues of $13.21 billion in 2022, a yearly growth of 19.4% on account of increased revenues in all end markets, unprecedented design wins across the entire portfolio and higher pricing (due to input cost inflation).Automotiveand coreIoTmarkets witnessed robust demand throughout 2022, outstripping the company’s supply capabilities.Consumer IoTand mobile markets experienced softening demand environment in the latter half of the year. In Q4 2022, NXP delivered revenues of $3.31 billion, up 9% YoY and down 4% QoQ. The Q4 revenues were $12 million better than the midpoint of the guidance with all markets performing in line or better than expected except the communication and infrastructure segment. The full-year non-GAAP gross profit was $7.64 billion with non-GAAP gross margin standing at 57.9%, an increase of 180 basis points YoY due to higher internal factory utilization and follow-through on higher revenues.

Automotive

- NXP’s automotive business captured 52.1% of the total revenue in 2022, an increase of 2.4% from the previous year. Revenue for the full year stood at $6.88 billion, a yearly growth of 25.2%. This growth was driven by higher pricing, record customer design wins (forxEV解决方案——电池管理解决方案,逆变器controls, other xEV control processors, etc.), and strong traction of company-product drivers owing to accelerated content increases within xEVs andpremiumcar models.

- 第四季度revenues were $1.81 billion, up 17% YoY and flat QoQ, in line with the company’s guidance. Due to supply constraints, NXP couldn’t ship more in Q4.

- NXP emphasized on its auto-specific accelerated growth drivers, which will help it with increased yearly revenues in the future. Theyinclude 77-gigahertzradarsolutions, electrification systems, and the S32 domain and zonal processors. Customer enthusiasm for S32 processors continues to grow, far exceeding expectations. A major automotive OEM has selected the S32 family of automotive processors and microcontrollers for use across its fleet of vehicles beginning next decade.

- In Q4, NXP introduced the high-performanceS32K39series MCUs for electrification applications like traction inverter control, BMS and OBC, and announced its collaboration withDelta Electronicsin which the latter will utilize NXP’s S32 automotive platform and S32K39 MCUs to develop next-generation EV platforms. At theCESthis year, it unveiled theSAF85xxSoC, the industry’s first 28-nanometer RFCMOS radar one-chip IC family forADASapplications.

- For Q1 2023 revenues, the company is estimating this segment to be up in the mid-teens and flattish on a YoY and QoQ basis respectively.Increasedglobal automotive production and growing penetration of xEVs would prove beneficial for future revenue growth.

Industrial & IoT

- The industrial andIoTsegment’s revenue for 2022 was $2.71 billion, up 13% YoY. The growth can be attributed to higher pricing and demand for its industrialprocessors, and analog, connectivity, and security solutions. Specifically, its secureconnectededge solutions (accelerated growth driver), which include bothcrossoverandi.MX application familiesofprocessors,grew nearly 50% YoY in 2022.

- 第四季度revenues were better than their earlier guidance at $605 million, down 8% YoY and 15% QoQ respectively. Due to lockdowns inChinaand uncertain macro conditions, consumer-exposed IoT businesses saw a deceleration in revenue.

- In Q4, the company launched its new analog front-end (N-AFE) family of devices targetingindustrialapplications, specifically software-defined factories. It will help with high-precision data acquisition and condition monitoring systems for factory automation.Schneider Electricis incorporating the N-AFE family in its industrial solutions. NXP also launchedMCX N seriesMCUs for secure intelligent edge industrial andIoTapplications and expanded its portfolio of end-to-end Matter solutions by announcing theRW612andK32W148wireless MCUs. Both are targeted toward智能homeapplications such as garage doors, thermostats, smart plugs, and smart lighting.

- For Q1 2023, the industrial and IoT segment is expected to be in the negative territory in both YoY (low 30% range) and QoQ (low 20% range) terms. The core industrial business remains supply constrained in some areas while consumer IoT is expected to experience cyclical weakness in demand and potential correction of customer inventory.

Mobile

- For 2022,Mobilesegment revenues stood at $1.61 billion, an increment of 14% YoY due to higher pricing and continued traction of the secure mobile wallet.

- In Q4, it reportedrevenuesof $408 million, up 9% YoY and down 0.5% QoQ, and faring better than the company’s guidance. As observed in theprevious quarter, weakness in the Android mobile market continued to persist, affecting the largely channel-driven mobile business.

- NXP’s mobile segment-specific accelerated growth driverUltra-Wideband(UWB) was below the expected revenue growth range since NXP’s UWB solutions are aimed at the Android market, which is experiencing softening demand. However, the company is optimistic about this growth driver in the near future as it continues to build out its ecosystem and register more design wins both in the mobile and automotive sectors.

- For Q1 2023, NXP is expecting this segment to be down in the mid-40% range both in YoY and QoQ terms. The mobile segment is dependent on a cyclical rebound and is expected to improve performance as and when theAndroidhandset market fares better.

Communication infrastructure and other

- The ‘communication infrastructure and other’ segment’s revenue in 2022 was $2 billion, up 15% YoY. This growth was driven by higher pricing and sales of in-demand solutions likenetworkprocessors, secure transit and access products and RF-powered products for the cellularbase stationmarket.

- 第四季度revenuesstood at $494 million, up 8% YoY but down 5% QoQ and below the company’s guidance. Weakness in this quarter had nothing to do with demand but was primarily due to operational issues and supply constraints.

- NXP’s accelerated growth driver –RFpower amplifiers– was on track as per its expected revenuegrowthrange. The industry transition from LDMOS technology to gallium nitride happened faster than expected and the company’s revenue doubled YoY with respect to gallium nitride-based solutions. However, the demand continues to outstrip even its increasing supply capabilities.

- In January 2023, NXP launched a new wideband GaN RFtransistor–MMRF5018HS– primarily for aerospace and defense communications.

- For Q1 2023, the guidance expects the revenues to be flat both in YoY and QoQ terms. NXP will try to improve its supply capabilities to cater to the pent-up demand in RFID packing solutions, e-government identification, 5G base station market build-out especially inIndia, and more.

Capex overview and inventory

- Cash flow from operations stood at $3.9 billion in 2022. Netcapexinvestments were $1.06 billion or 8% of overall revenue, a 1% jump from the previous year. Due to softening demand in consumer-oriented markets, internal front-end utilization rates have dropped for non-auto industrial products. From running in the high 90s in Q3 to touching 90% in第四季度2022and in Q1 2023, it is expected to go down to 85%. Despite this, NXP is confident of keeping itsgross marginwithin its long-term range of 55%-58% as it has a disciplined inventory management approach and a better grip on its cost structure, which is more variable in nature now than it was in past.

- NXP continues to face shortages in certainnodesand other technologies like 180 nanometers, 9055 gallium nitride and the high-voltage analog mixed-signal (which are proprietary to NXP). This can lead to significant customer escalations which thecompanyhopes will moderate by the end of this year. However, it remains optimistic about its supply capabilities in the future as its ability to cater to risk-adjusted backlog has gone up from 85% in 2022 to 90%-95% in 2023.

- DOI has increased to 116 days, a 17-day sequential increment, and distribution channelinventoryhas been deliberately restricted to 1.6 months as opposed to its long-term target of 2.5 months. China’s market is experiencingweakersell-through and NXP is being prudent about shipping more in the channel as it might not meet the true end demand and lead to an unnecessary inventory build-up. Since more than 50% of the company’s revenue goes through the channel, it is taking a very vigilant inventory management approach and keeping more than enough products in hand to fill the channel as and when required.

Conclusion

Input cost inflation due to supply chainconstraintsled to higher pricing for NXP solutions in 2022, a trend that will continue this year as well. Dynamicmacrotrends continue to pose an uncertain general demand environment and a potential rebound in theChinesemarket could significantly improve end markets’ revenues, which is why managing internal and channel inventory is an important topic for the company. Overall, NXP is prepared for market uncertainties and will continue to execute diligently on its accelerated growth drivers and be disciplined with its operating expenses while protecting long-term R&D investments.