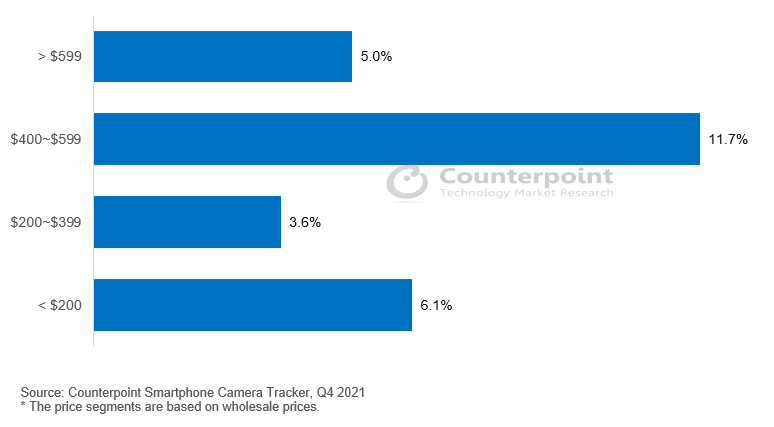

- India’s premium smartphone segment now contributes a record 17% to its overall shipments.

- With an 18% share, Samsung led India’s smartphone market for the third consecutive quarter.

- Samsung also surpassed Apple to become the top premium segment (>INR 30,000 or ~ $366) brand.

- Apple continued to lead the ultra-premium segment (>INR 45,000 or ~$549) with a 59% share.

- vivo maintained its second position. It was the only brand among the top five to experience YoY growth.

- OnePlus was the fastest-growing brand in India’s smartphone market in Q2 with 68% YoY growth.

New Delhi, Hong Kong, Seoul, London, Beijing, San Diego, Buenos Aires – July 28, 2023

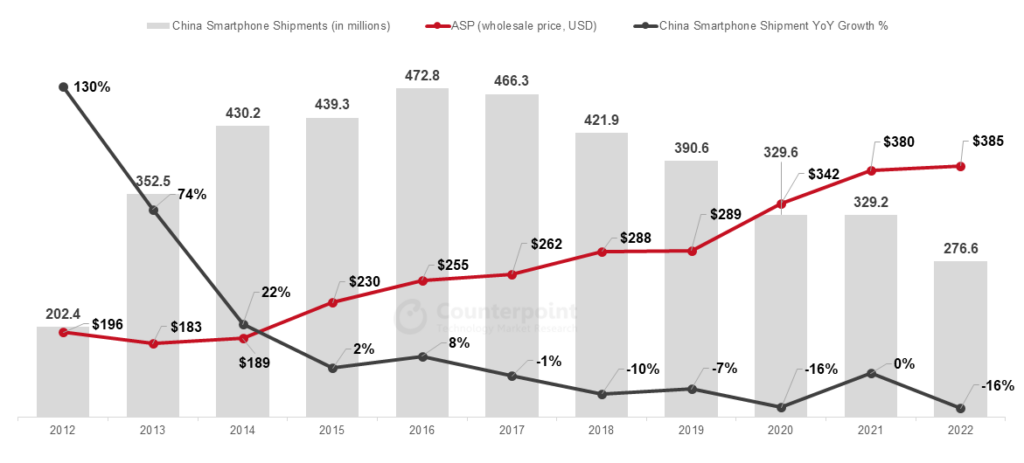

印度的智能手机出货量declined 3% YoYin Q2 2023 (April-June), according to the latest research from Counterpoint’sMonthly India Smartphone Tracker。Though this decline was the fourth consecutive quarterly decline, its magnitude reduced significantly, from19% in Q1to 3% in Q2. Base effect, pent-up demand and improving macroeconomic conditions helped the market close at less than the expected decline. However, the premium smartphone segment presented a different picture, growing 112% YoY in Q2 to contribute a record 17% to the overall shipments.

在评论马克t dynamics,Senior Research AnalystShilpi Jainsaid, “In Q2 2023, OEMs saw improvement in the inventory and demand situation ahead of the coming festive season. Aggressive measures were implemented by OEMs as well as channels during the quarter to clear existing inventory through multiple sales and promotions. At the consumers’ end, falling inflation and better growth prospects facilitated demand recovery.5Gupgrades also played a major role as OEMs kept launching 5G devices in the INR 10,000-INR 15,000 (~$122-$244) segment for a wider reach. We believe brands will be coming up with interesting launches and offers to lure consumers during the festive season and 5G will be a big growth driver here.”

Source: Counterpoint Research Market Monitor

Notes: Xiaomi includes POCO; OPPO excludes OnePlus; vivo includes iQOO; Figures not exact due to rounding

Commenting on the competitive landscape and brand-level analysis,Research Analyst Shubham Singhsaid, “Samsungremained at the top position for the third consecutive quarter with an 18% market share. The brand also surpassed Apple to regain its top position in the premium smartphone segment (>INR 30,000, ~$366) after one year with a 34% share. Aggressive offers on theZ Flip3and S21 FE, Samsung Finance+ and high demand for the latest premium A-series and F-series devices drove this growth. However,Applecontinued to lead the ultra-premium segment (>INR 45,000 or ~$549) with a 59% share. India is now among Apple’s top-five markets.”

“vivo maintained its second spot in the overall market and was the only brand among the top five to experience YoY growth. Strong offline presence, growth of sub-brand iQOO in online, and multiple launches across price tiers facilitated this growth。OPPOhas been consistently expanding its shipments in the higher-tier segments, with a particular focus on the upper mid-tier range (INR 20,000-INR 30,000 or ~$244-$366), showcasing its strategy to cater to diverse consumer needs. OPPO emerged as the top brand in this segment with a 21% market share.OnePluswas the fastest growing brand in India’s smartphone market in Q2 with 68% YoY growth.”

Other key insights

- 5G smartphone growth: In Q2 2023, 5G smartphone shipments in India crossed the 100-million cumulative mark as 5G upgrades picked up pace driven by the expansion of 5G networks and availability of affordable devices. 5G smartphone shipments grew 59% YoY during the quarter.

- Premiumization trend: The premiumization trend gained momentum as the segment grew at a faster rate of 112% YoY. Rise of a value-based incentive system for retailers, aggressive promotions, availability of credit through various financing schemes, and OEMs’ focussed approach are driving premiumization in India.

- Channel dynamics: Offline channel share has been growing and is expected to rise to 54% in 2023. Online-heavy brands like Xiaomi, realme and OnePlus are now emphasizing offline expansion to enhance customer engagement and ecosystem development. Samsung and Apple are also increasing their offline presence to cater to diverse consumer preferences. This shift reflects a more comprehensive approach, leveraging both online and offline channels to create a seamless and personalized customer experience.

- 4 g功能手机成长th: 4G feature phone share in the overall feature phone shipments increased to 10% in Q2 2023 driven by the JioBharat and itel Guru series’ launch. We believe this share will increase to 18% by the end of 2023. Growing demand for UPI, multiple launches from OEMs and Reliance push will help the segment grow further.

- Inventory levels: The market was able to exit Q2 2023 with eight weeks of inventory as Xiaomi and realme managed to clear most of their inventory through multiple sales and promotions.

- Other notable brandswhich grew during Q2 2023 were Apple (56% YoY), Transsion (34%), Lava (53% YoY) and Nokia (6% YoY).

The comprehensive and in-depth ‘Q2 2023 Market Monitor’is available for subscribing clients.

Feel free to contact us atpress@www.arena-ruc.comfor questions regarding our latest research and insights.

The Market Monitor research relies on sell-in (shipments) estimates based on vendors’ IR results and vendor polling, triangulated with sell-through (sales), supply chain checks and secondary research.

You can alsovisit our Data Section(updated quarterly) to view the smartphone market shares forWorld,US,ChinaandIndia。

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Analyst Contacts

Shilpi Jain

![]()

Shubham Nimkar

![]()

Tarun Pathak

![]()

遵循对比研究![]()