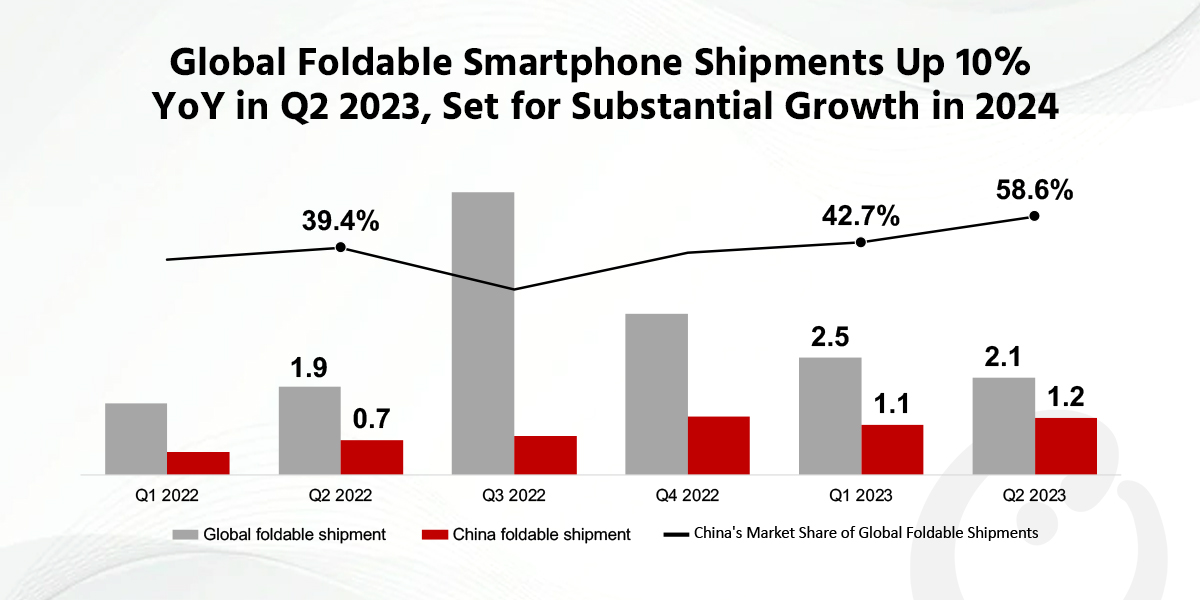

Although overall global smartphone shipments declined in Q2 2023, global foldable shipments rose.

2023年H2,竞争在全球可折叠的职业duct market is set to escalate significantly, driven by the earnest entry of Chinese companies like OPPO and HONOR.

The global foldable market is expected to experience substantial growth in 2024, driven by the introduction of entry-level foldable products.

The global foldable smartphone market increased 10% YoY in Q2 2023 to reach 2.1 million units, according to Counterpoint Research’s most recentglobal foldable smartphone tracker.This growth is in stark contrast to that of the global smartphone market, which showed a 9% decline in shipments during the quarter to reach 268 million units. Due to the prolonged Russia-Ukraine war and the ongoing high global inflation, the smartphone market is expected to grow sideways. Nevertheless, the foldable smartphone sector continues to exhibit robust and sustained growth.

Global and ChinaFoldable Smartphone Shipments, Q1 2022-Q2 2023

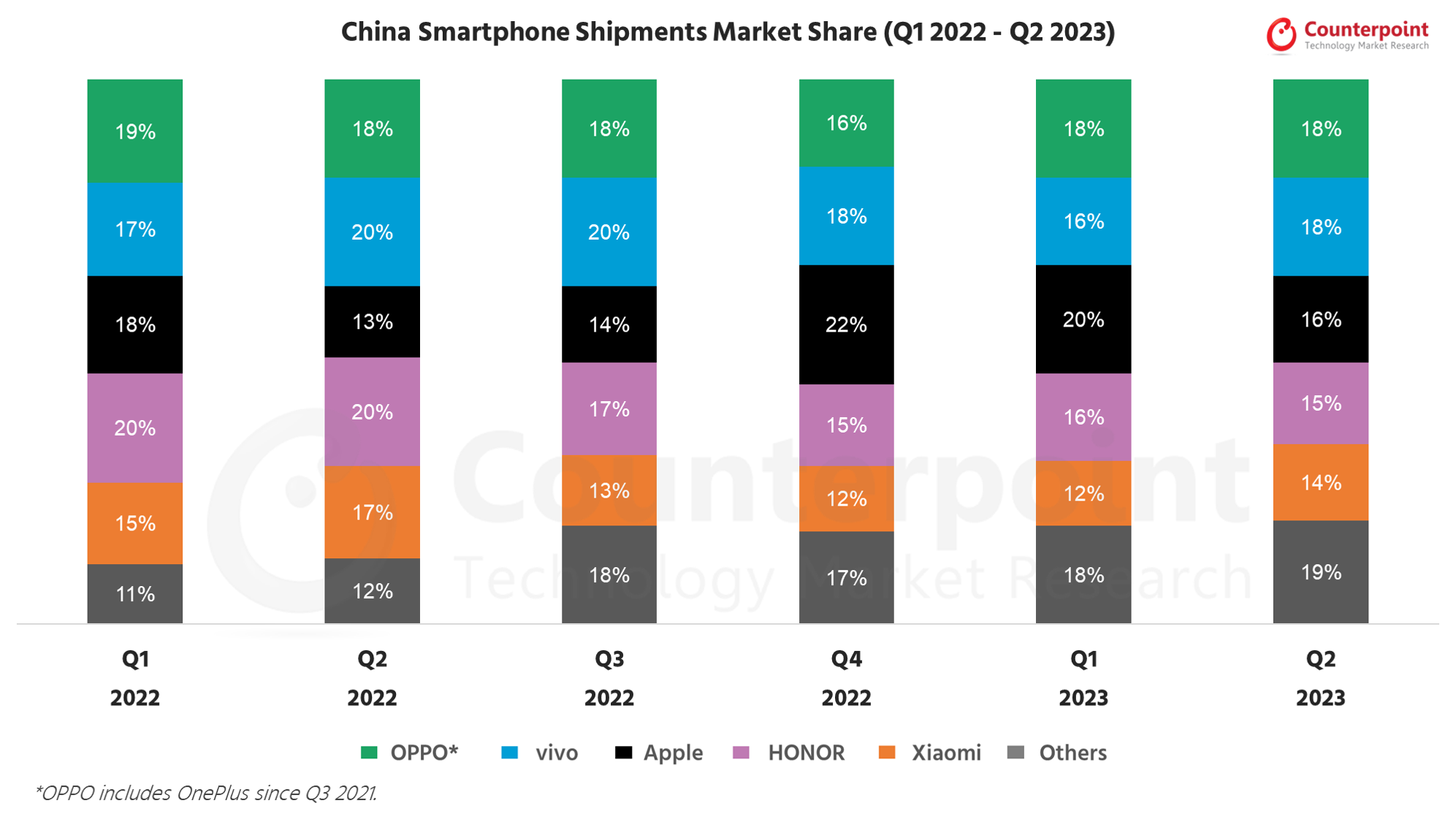

可折叠的智能手机景观在中国arket presents a particularly intriguing scenario. During Q2 2023, shipments in the overall Chinese smartphone market slipped 4% YoY to reach 61.9 million units, hurt by the recent economic challenges faced by the country, which led to a reduction in consumer spending. However, the Chinese foldable smartphone market achieved notable success, surging 64% YoY to reach 1.2 million units. China now commands the largest share of the global foldable smartphone market, with a 58.6% share.

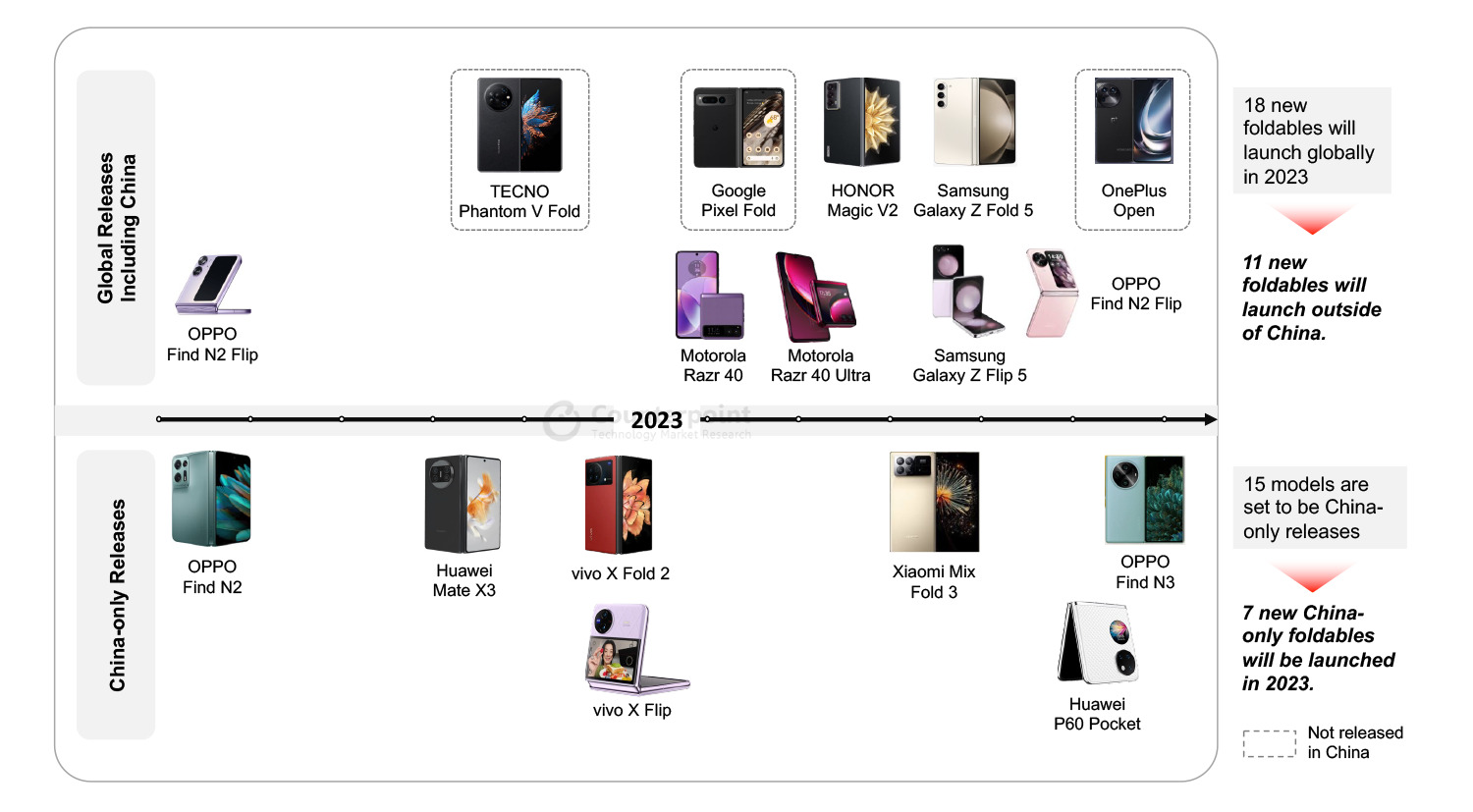

FoldableProduct Launch Status in 2023: Comparison of Global and Chinese Foldable Markets

The rapid growth of the Chinese foldable market is primarily attributed to the introduction of foldable products tailored for the Chinese market, coupled with a strong demand for these products among Chinese consumers. In Q2 2023, significant momentum is building for the continued growth of the foldable market. This surge was driven by the introduction of key products such as the Huawei Mate X3, vivo X Fold 2, and vivo X Flip, primarily targeting the Chinese foldable market. Additionally, the global (including China) launch of the Motorola Razr 40 and Razr 40 Ultra, further contributed to this growth trend. In Q2 2023, China saw the launch of five new foldable products tailored for its market, while the global market outside China only saw two foldable product launches during the same period.

Counterpoint Research Senior Analyst Jene Parksaid, “We believe that these frequent product launches (along with the marketing effects that accompany product launches) are changing Chinese consumers’ perception of foldable products. Consequently, Chinese consumers can access a variety of foldable products more easily and frequently than any other market in the world. The continuous release of various foldable products is recognized as one of the important reasons why the Chinese foldable market has continued to grow significantly compared to other markets.”

The global foldable smartphone market will undergo significant changes in H2 2023. Chinese manufacturers are expanding their presence internationally during this period, with notable releases including the HONOR Magic V2, OPPO Find N3 Flip, and the yet-to-be-named OnePlus foldable device. Notably, Samsung’s Galaxy Z Fold 5 and Galaxy Z Flip 5, considered to be some of the top-tier foldable offerings, were launched in August and are expected to capture a substantial market share in H2 2023.

Parkadded, “The global foldable smartphone market is set to see significant growth in the H2 2023, driven by the expansion of Chinese manufacturers. Although Samsung’s market share may dip due to increased competition, we believe that it will be a natural result. However, competition among manufacturers usually has the effect of increasing the size of the market for the product. We believe that the era of the mass foldable phone is expected to start in 2024, mainly led by Samsung and Huawei with their entry-level foldables. Entry-level foldables are expected to be priced around $600 to $700, making them more accessible to consumers.”

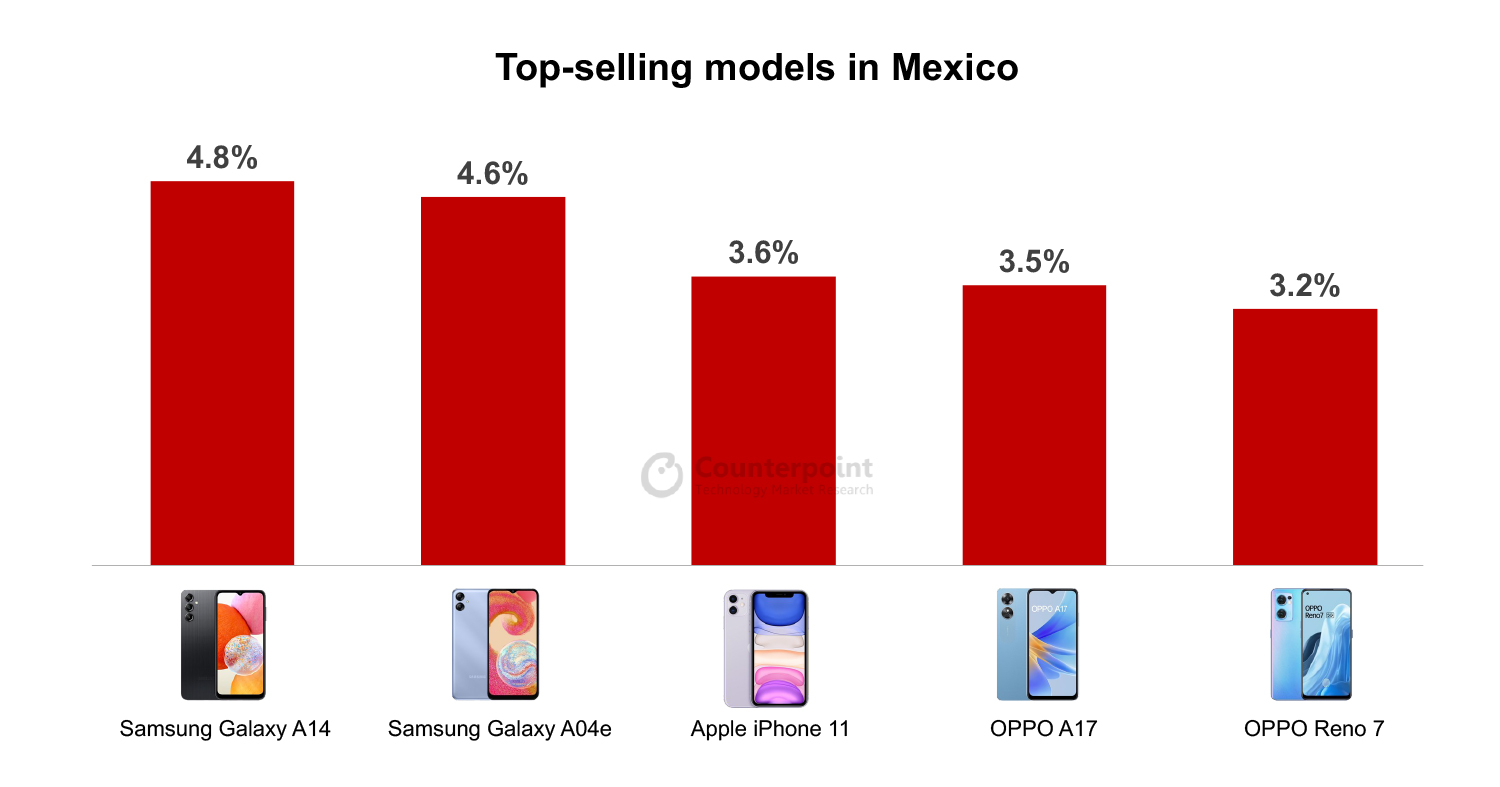

Apple’s iPhone 11 was the third best-selling model in Mexico in Q2 2023.

60% of the models in the top 10 list were priced below $150.

Samsung’s Galaxy A34, Galaxy A54 5G were the only two 5G models on the top 10 list.

Mexicois the second most important smartphone market in Latin America. The country has the second-highest population in the region and hosts an extremely competitive ecosystem. Mexico’s geographical size and lack of import barriers make it an extremely attractivesmartphonemarket.

The top-selling models accounted for 35% of Mexico’s total smartphonemarketin Q2 2023. The top 10 list almost appears like Samsung’s performance for the quarter as the brand dominated the top-selling chart in Mexico in Q2 2023. Five of the 10 best-selling models were fromSamsung. According to Counterpoint’s Market Pulse Report, Samsung’s share in Q2 2023 was slightly more than 30%.

OPPO and Motorola both had two models in the Q2 2023 top-selling list. Motorola, which has always been a strong player in theMexicanmarket, launched a few new models during the quarter that helped the brand increase its market share. OPPO, a relatively new entrant in theLATAMmarket, managed to retain its third position in market share with two of its models in the top-selling list.

Source: Counterpoint Research Market Pulse, Q2 2023

60% of the models in the top 10 list were priced below $150. This price band accounts for 52% of the overallsmartphonemarket in Mexico. However, premiumization is infiltrating the Mexican market, and the number of models in the >$150 band is increasing in the top-selling list. This trend is accelerating slowly but will surely lead to a higher overall smartphone ASP.

Apple’s four-year-oldiPhone11 has been part of the Mexican bestseller list for a few quarters now. It was the third best-selling model in the Mexican market in Q2 2023. The iPhone 11, which is a 4G model, was the most expensive model on the list. The massive sales of this model reflect the strength of Apple’s branding.

The 4G version of OPPO’s Reno 7 was another model in the bestsellers list priced more than $150. This is quite an achievement for the brand, which arrived in the region just three years ago.OPPOis still building its branding in the Mexican market. The Reno 7 has been in the Mexican top-selling chart since December 2022.

值得注意的是只有两个模型图are 5G phones – the Samsung Galaxy A34 and the Samsung Galaxy A54 5G. The latter one is also the most expensive Samsung model in the top-selling list. Meanwhile, Telcel has been pushing its subscriber base to replace their phone with a 5G one. Mexican consumers are still not ready for5Gtechnology. They would rather get more specs than access the technology.

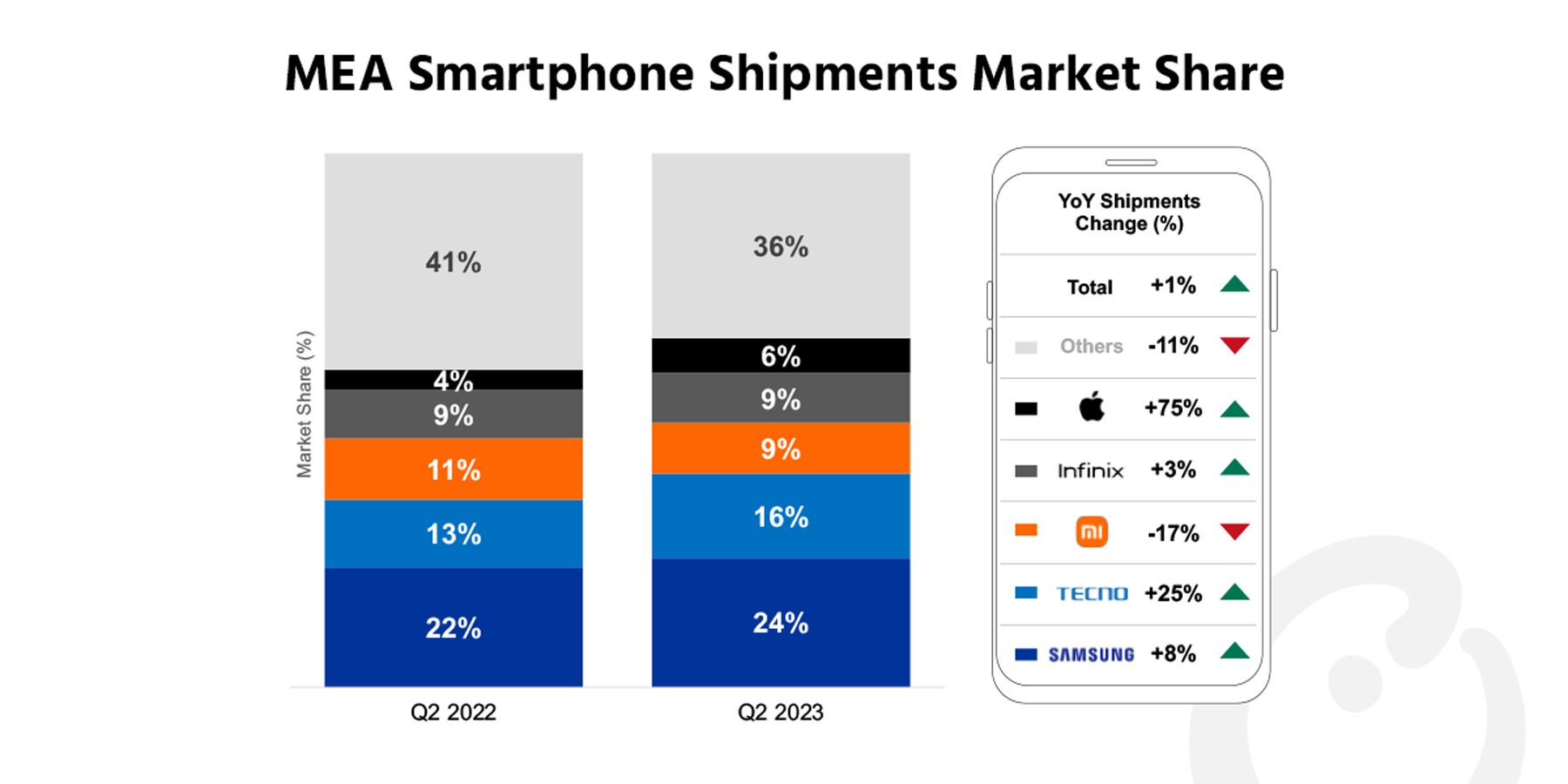

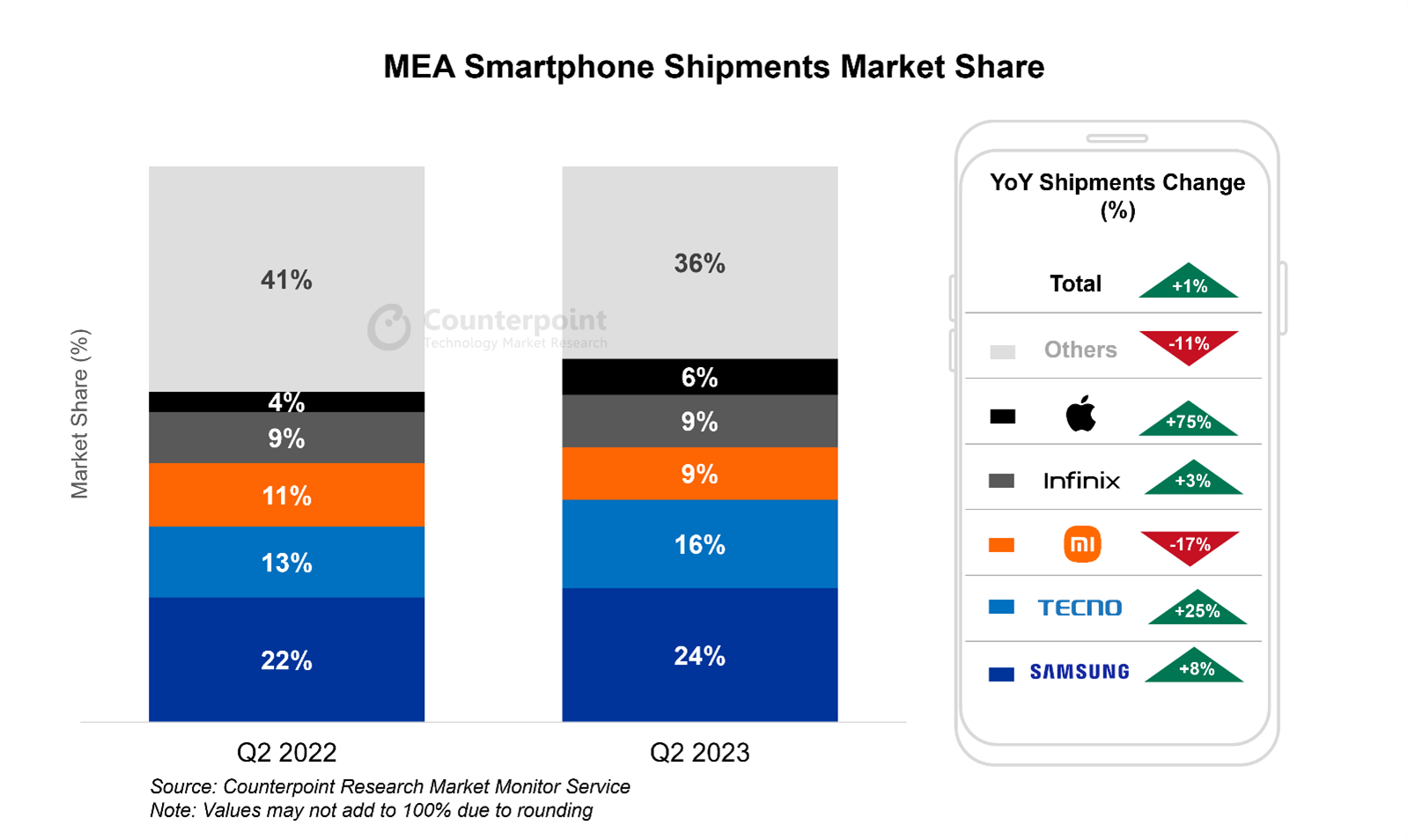

MEA smartphone shipments increased 1% YoY and 7% QoQ in Q2 2023.

Consumer sentiment picked up during the quarter with falling inflation rates and stabilizing local currencies. These boosted demand for ‘big ticket’ items like smartphones.

Samsung saw a rebound in its shipments and market share during the quarter.

Transsion Group’s shipments grew 2% YoY, or an impressive 14% QoQ, in a typically weak quarter.

Apple continued its steep rise, with shipments up 75% YoY in Q2.

London, Boston, Toronto, New Delhi, Hong Kong, Beijing, Taipei, Seoul – September 5, 2023

Smartphoneshipments in the Middle East and Africa (MEA) region increased 1% YoY and 7% QoQ in Q2 2023, according to the latest research from Counterpoint’sMarket Monitor Service. This was the MEA smartphone market’s first meaningful rebound in five quarters, or since the global inflation crisis started. Consumer sentiment improved materially during the quarter, as inflation rates fell and local currencies stabilized. This came as a welcome relief for embattled OEMs, which had been sitting on an alarming level of inventory in 2022. They utilized the opportunity to destock and return to a more normal pattern of inventory and product launches.

Commenting on the market’s performance,Senior Analyst Yang Wangsaid, “TheMEAregion seems to be the first to come out of the global downturn in thesmartphonemarket. Market activity picked up during the quarter on better macroeconomic environment and consumers could afford to be more optimistic about ‘big ticket’ item purchases. This was reflected in robustRamadanand Easter sales and throughout the quarter. The encouraging performances show once again that the MEA region could be the last remaining untapped smartphonemarket.There is still significant potential for large segments of the population to upgrade to smartphones.”

Looking at individual brands, Samsung, TECNO andApplewere the biggest winners.Samsung’s rebound can be attributed to the lower-pricedGalaxyA series’ strong sales, while new 5G and premium-end models also did well.TECNO, and sister brandInfinixto some extent, performed very well due to better economic conditions, particularly for lower income groups, and aggressive market entries in the Middle East. TECNO andInfinix’ssuccesses, however, can be partly attributed to the cannibalization ofitel’s market share. Lastly,Applehad an outstanding quarter to round off a very strong iPhone 14 series cycle. TheOEMmanaged to increase penetration in key Middle East markets with the higher-priced Pro and Pro Max models getting good reception.

On the other hand,Xiaomiretreated 17% YoY as it faced strong competition from Samsung and Transsion brands in the mid-range. Outside of the top 10,OPPOandvivocontinued to slide as the availability of the brands’ stock contracted and market penetration activities shrank. However,realmemaintained positive momentum due to increasing product availability in new markets.

Commenting on pricing trends in the MEA smartphone market, Wang said, “The premium end is usually an afterthought for the MEA market, but the segment was an outperformer of Q2 2023. The sales of smartphones priced above $800 grew 93% YoY, largely due to Apple’s high-end models in the iPhone 14 series. The OEM’s share increased in key GCC markets, while it was seen making efforts to expand distribution channels in Africa. Apple’s success in the MEA region is another proof of the brand’s strong global appeal. As the process of urbanization and industrialization continues across the region, Apple can expect to remain one of the topOEMsin the region.”

Counterpoint Research’s market-leadingMarket Monitor,MarketPulseandModel Salesservices for mobile handsets are available for subscribing clients.

在press@counterpointresea随时联系我们rch.com for questions regarding our in-depth research and insights.

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

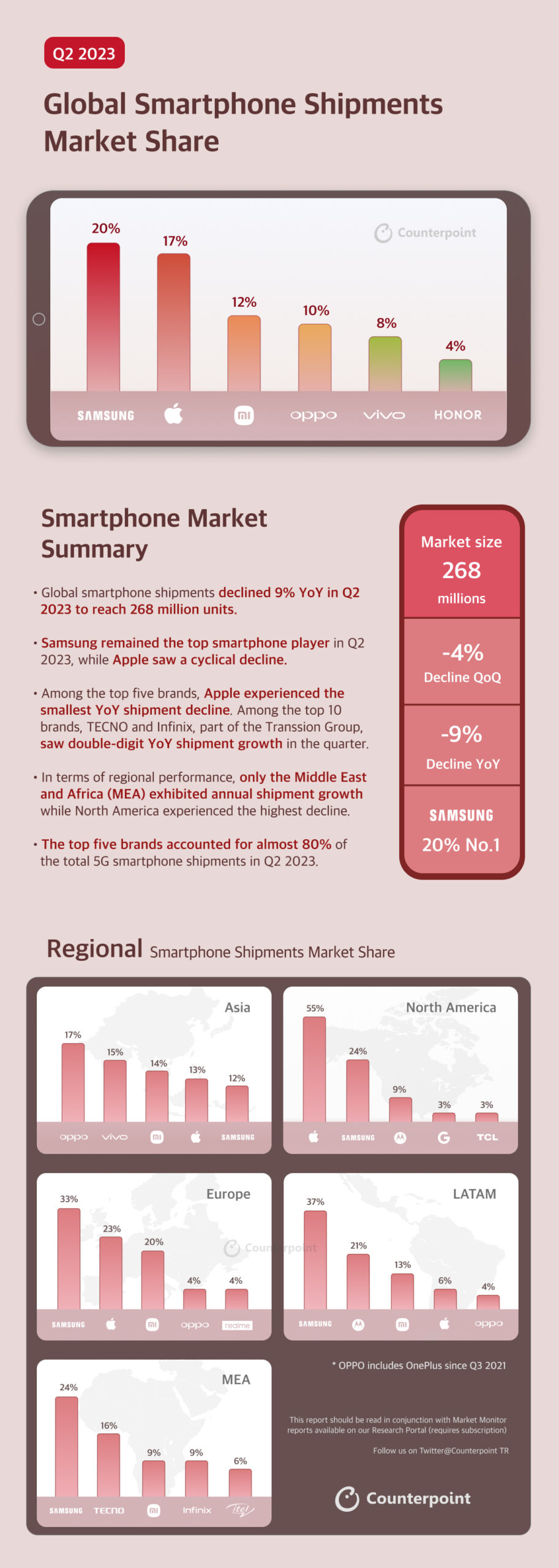

Our Q2 2023 Market Monitor report has been published. We release one infographic each quarter to summarize the global smartphone market activities in a single page.

Some quick observations on the smartphone market:

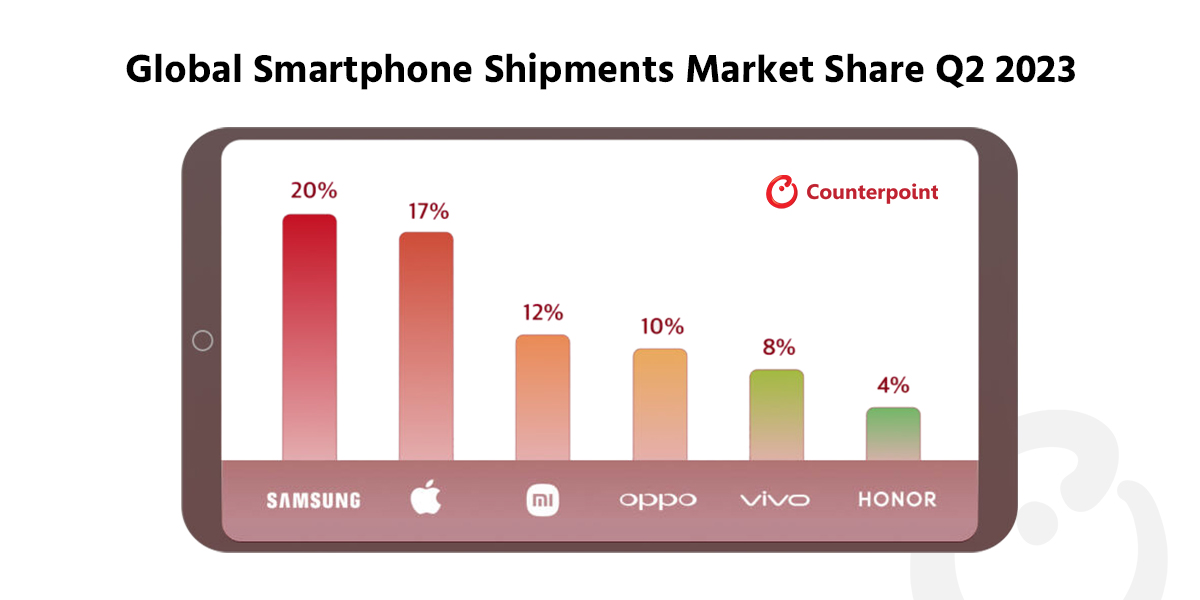

Global smartphone shipments declined 9% YoY in Q2 2023 to reach 268 million units.

Samsung remained the top smartphone player in Q2 2023, while Apple saw a cyclical decline.

Among the top five brands, Apple experienced the smallest YoY shipment decline. Among the top 10 brands, TECNO and Infinix, part of the Transsion Group, saw double-digit YoY shipment growth in the quarter.

In terms of regional performance, only the Middle East and Africa (MEA) exhibited annual shipment growth while North America experienced the highest decline.

The top five brands accounted for almost 80% of the total 5G smartphone shipments in Q2 2023.

Use the button below to download the high resolution PDF of the infographic:

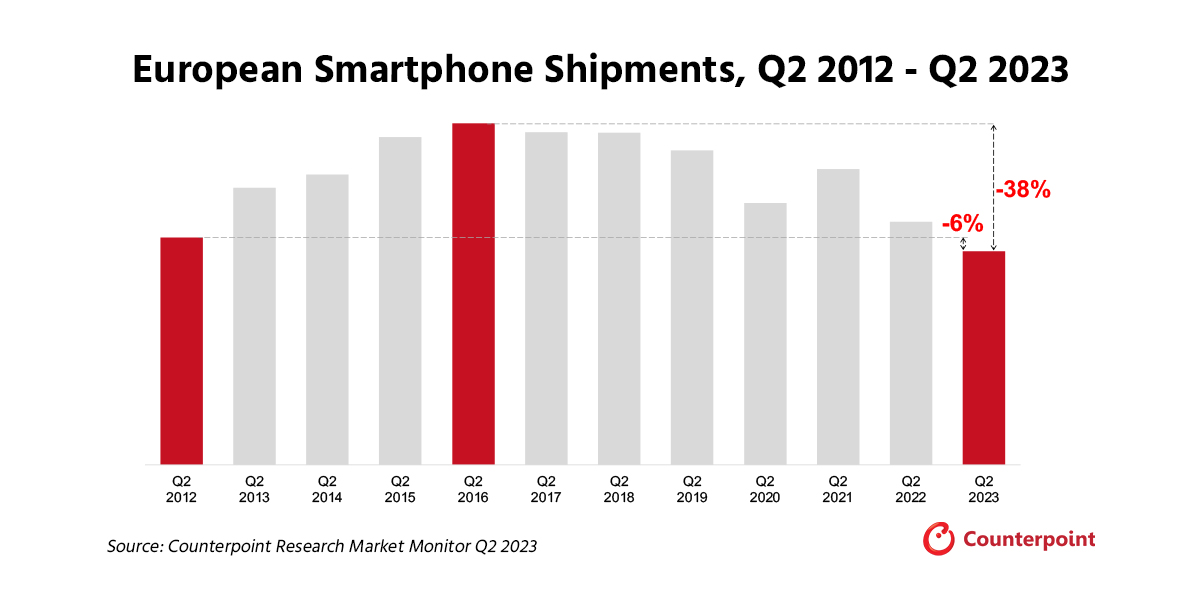

Europe smartphone shipments fell 12% YoY in Q2 2023 to reach lowest since 2012.

Russia only major market to register growth at 4% YoY.

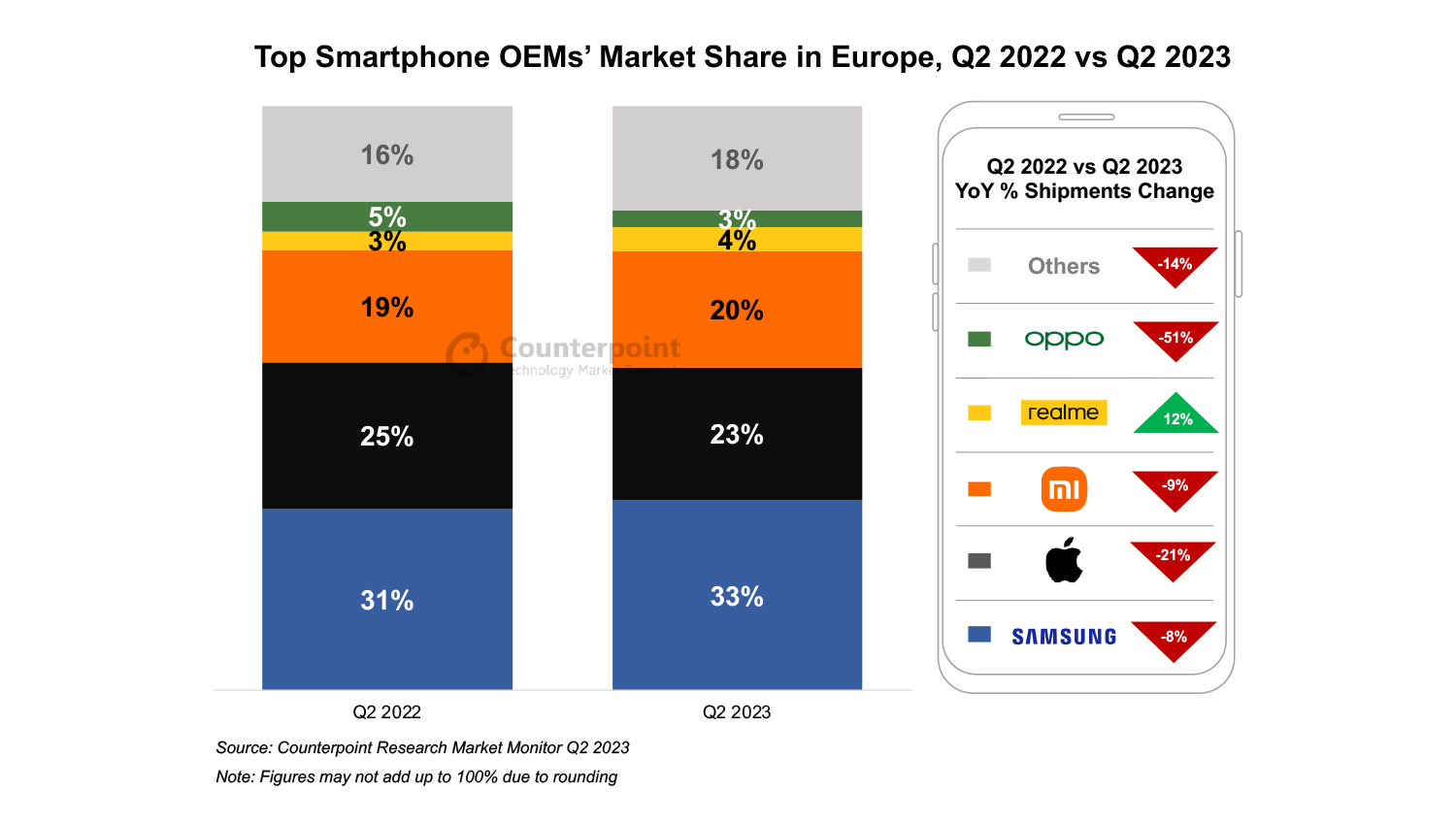

OPPO’s shipments fell 51% YoY hurt by patent issues and difficult market conditions.

2023 smartphone shipments are set to be lower than in 2022.

London, Boston, Toronto, New Delhi, Jakarta, Beijing, Taipei, Seoul – September 1, 2023

European smartphone shipments declined 12% YoY in Q2 2023, marking the lowest quarterly shipment volume since Q1 2012, according to the latest report from Counterpoint Research’s Market Monitor Service.

Western Europe declined by 14% YoY during the quarter while Eastern Europe limited its fall to 8% YoY, despite being in an already battered state. All major European nations performed weakly in Q2 2023, except Russia, which conversely registered 4% YoY growth. However, this was primarily due to lower shipments in Q2 2022 – the first full quarter after Russia’s invasion of Ukraine and the resulting sanctions and market exits of prominent smartphone players.

OPPO had a difficult time in Q2 2023 with patent disputes and uncertainty in several countries, due to which the brand’s shipments dropped 51% YoY. The uncertainty is likely to persist which will result in further shipment declines in the coming quarters.

realme grew 12% YoY, driven primarily by Russia, which accounted for 55% of the brand’s shipments in the region. In Russia, realme benefitted from Samsung and Apple’s market exit, which allowed the company to fill the void left by these heavyweights. Additionally, realme has remained in the second position in Russia for five straight quarters and has been closing the gap with the market leader Xiaomi.

HONOR registered 9% YoY growth during the quarter due to the base effect and its ongoing expansion outside China.

Commenting on the current market dynamics,Research AnalystHarshit Rastogisaid, “Despite falling shipment volumes, the higher price bands (wholesale prices exceeding $600) have been capturing a larger share of the market each year. They also have a longer replacement cycle compared to mid-segment and lower-price band smartphones, which further dampens demand. Consequently, OEMs are likely to focus on increasing their ASP and concentrate on services to drive revenue growth in the coming quarters.”

Commenting on market outlook,Associate Director JanStryjakcommented, “The market is unlikely to make a full recovery `this year and 2023 smartphone shipments are set to be lower than in 2022, marking consecutive decade-low shipments in both 2022 and 2023. While the economic conditions are partly to blame, consumer buying behaviour is also changing, suggesting that a lower level of sales will set a new baseline. However, despite the low shipment volumes, upcoming iterations of Apple’s iPhone and Samsung’s foldables are likely to fare well, prompting a bump in sales volumes in the coming quarters.”

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

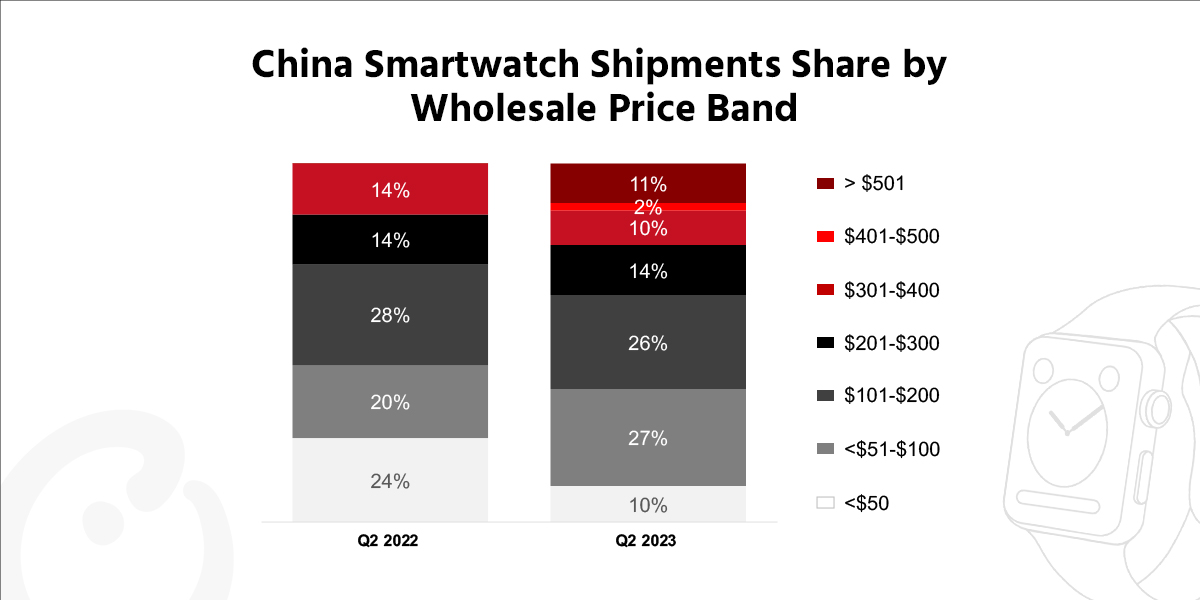

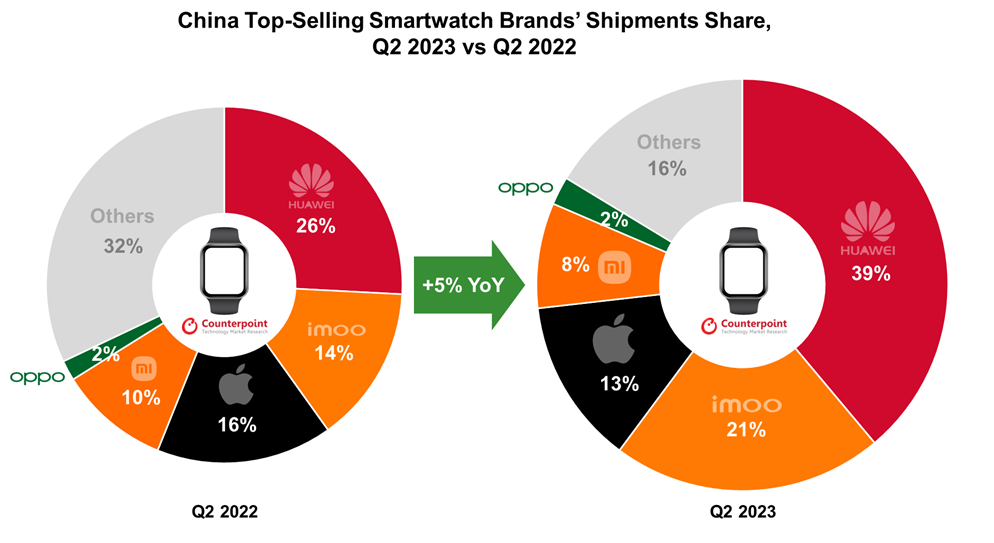

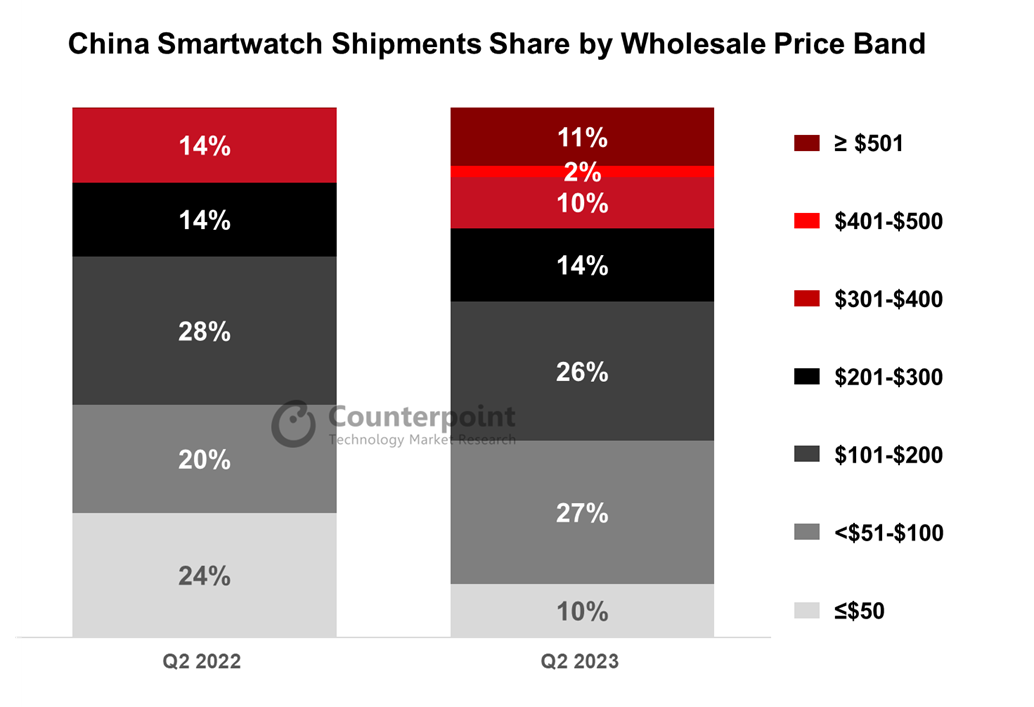

China’s smartwatch shipments rose 5% YoY in Q2 2023 to mark the market’s gradual recovery.

Huawei remained the best-selling brand with a 39% market share.

imoo (BBK) surpassed Apple to rank second in market share.

The≥$500 price band’s share increased significantly, while the ≤$50 price band’s share decreased significantly.

Beijing, New Delhi, Seoul, Hong Kong, London, Buenos Aires, San Diego – August 30, 2023

Marking a gradual recovery in Q2 2023, China’s smartwatch shipments increased 5% YoY, according to Counterpoint Research’s latestGlobal Smartwatch Model Tracker.

Senior Analyst Shenghao Baisaid, “The YoY rise in Q2 came on a low base of the same period last year. At the same time, the holiday travel in Q2 and the 618 e-commerce festival also boosted consumer demand for smartwatches. The market has recovered slightly better than we had predicted.”

Source: Counterpoint’s Global Smartwatch Model Tracker

Note: Figures may not add up to 100% due to rounding

Market summary

Huaweirecorded a 58% YoY growth, maintaining its good reputation among consumers. The newly launched Huawei Watch 4 and Huawei Watch 4 Pro series models were popular with consumers, while old models such as the Huawei Watch GT 3 series still sold well. Another newly launched model, the Huawei Watch Ultimate, contributed to the brand’s performance in the ultra-premium segment.

imoo(BBK) benefited from the demand in the first full back-to-school quarter after the pandemic lockdown was lifted in China. Its multiple offline retail stores also contributed to the brand’s growth.

Applerecorded a 15% YoY decrease in Q2 2023. Although the Apple Watch Series 8 was the best-selling model family in China during the quarter, its shipments decreased 25% compared to that of its predecessor Apple Watch Series 7 in Q2 2022. With new product launches expected in Q3 2023, Apple is likely to increase its market share in the quarter.

Xiaomirecorded a decrease of 15% YoY but an increase of 7% QoQ. The brand still took the biggest share in the ≤$50 segment. Waning consumer interest in entry-level products contributed to the decline in Xiaomi’s market share.

OPPOachieved a 28% YoY increase in Q2 2023. Promotions during the 618 e-commerce festival helped the OPPO Watch 3 and OPPO Watch 3 Pro’s sales.

Source: Counterpoint’s Global Smartwatch Model Tracker

Note: The price refers to the wholesale price

In terms of wholesale price bands, the ≤$50 band’s share significantly dropped compared to the same period last year. This price band’s share has been recording YoY drops in the past several quarters. On the other hand, the ≥$500 segment’s share rose significantly to 11% from almost negligible in Q2 2022.

Research Analyst Alicia Gongsaid, “The entry-level products with simple features are not as popular with consumers as they once were. A growing number of consumers are gravitating toward smarter devices with more health monitoring, sports tracking and guidance functions. Since the Apple Watch Ultra’s release last year, the share of premium segments has been growing. The promotions during the 618 e-commerce festival also contributed to these segments’ growth.”

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Entry of Chinese brands stirring up regional market.

Samsung remains regional leader with 36.9% share, followed by Motorola with 21.4% share.

Apple’s growth mainly sustained by the iPhone 11.

One in four smartphones shipped in the region is a 5G smartphone.

Buenos Aires, San Diego, Denver, New Delhi, Hong Kong, Seoul, London, Beijing – August 24, 2023

Smartphoneshipments in Latin America (LATAM) dropped 15.6% YoY but climbed 2.4% QoQ in Q2 2023, according to the latest data fromCounterpoint Research’s Market Monitorservice. The decline was due to the negative impacts of the regional economic crises and weak global smartphone shipments.

Commenting on the market dynamics,Principal Analyst Tina Lusaid, “LATAM’s economic growth in 2023 is actually slightly higher than forecast. However, this recovery has not yet inspired an increase in the rate of smartphone replacement. Lowconsumerdemand continued to affect the region during the quarter. Although most countries in the region are seeing declininginflation, consumer confidence is yet to bounce back, as political turmoil continues to constrain the general economy.”

Research Analyst Andres Silva added,“Seasonal factors such as Mother’s Day and Father’s Day promotions helped the market grow slightly QoQ in Q2 2023, although the market declined YoY. The entry of manyChinesebrands at once is stirring up the market as they aim for growth, pushing other brands to become more aggressive. However, the YoY decline affected all the top sixcountriesin the region.”

Top Smartphone OEMs’ Market Share in Latin America, Q2 2022 vs Q2 2023

Source: Counterpoint Research Q2 2023 Market Monitor Note: Figures may not add up to 100% due to rounding

Commenting on the ASP performance in the region,Lu added: “There is a slight premiumization trend going on in the region. Compared to last year, LATAM’s total smartphoneASPonly grew around 4%. This has been a consistent trend. Inflation has some influence on it. However, established brands such as Samsung are pushing to increase the ASP in the region with5Gmodels.”

Market Summary

Samsungwas once again the absolute leader in the LATAM market in Q2 2023. However, itsshipmentsand market share declined YoY with weakened performance in most of the countries in the region.

Samsung has been very aggressive in offering extra discounts during the promotions. But not enough as its shipments were hurt by the Brazilian market and the entry ofChinesebrands.

Since Samsung is focusing more on premium models now, the availability of its models in the lower price bands is becoming restricted. Thus, its overall value dropped -2% YoY.

摩托罗拉的出货量同比下降,但其市场share increased slightly. It increased the number of models in the entry-segment E series. It also increased its brand awareness with the launch of theMotorolaEdge 40 Pro in May with an aggressive advertising campaign.

Xiaomi lost share slightly during the quarter but remained stable due to the launch of the Redmi Note 12 during the first week of April. This increased its Q2 2023 shipments and sales.Xiaomialso increased its Poco brand shipments in the open channels in the region.

Xiaomi recovered slightly from its position in Mexico. The participation of the grey market in the southern part of the LATAM region continued to grow.

Apple’sshipments and market share both grew YoY in Q2 2023, mainly sustained by the iPhone 11. The4Gsmartphones are still driving Apple’s volume in the region.

OPPOcontinued to be a strong fifth player in the region and ranked third in Mexico. Its volume increased by more than 70% in Q2 2023, while its share more than doubled YoY. Despite the growth, its shipments dropped QoQ.

HONOR did not make it to the list, but its growth in LATAM has been notable.HONORwas the brand with the most aggressive growth during the quarter. However, it still needs to build on its branding.

“Others”, mainly composed of regional brands, continued to decrease YoY. This category was most affected by the entry of low-price-band Chinese brands.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the technology, media and telecom (TMT) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

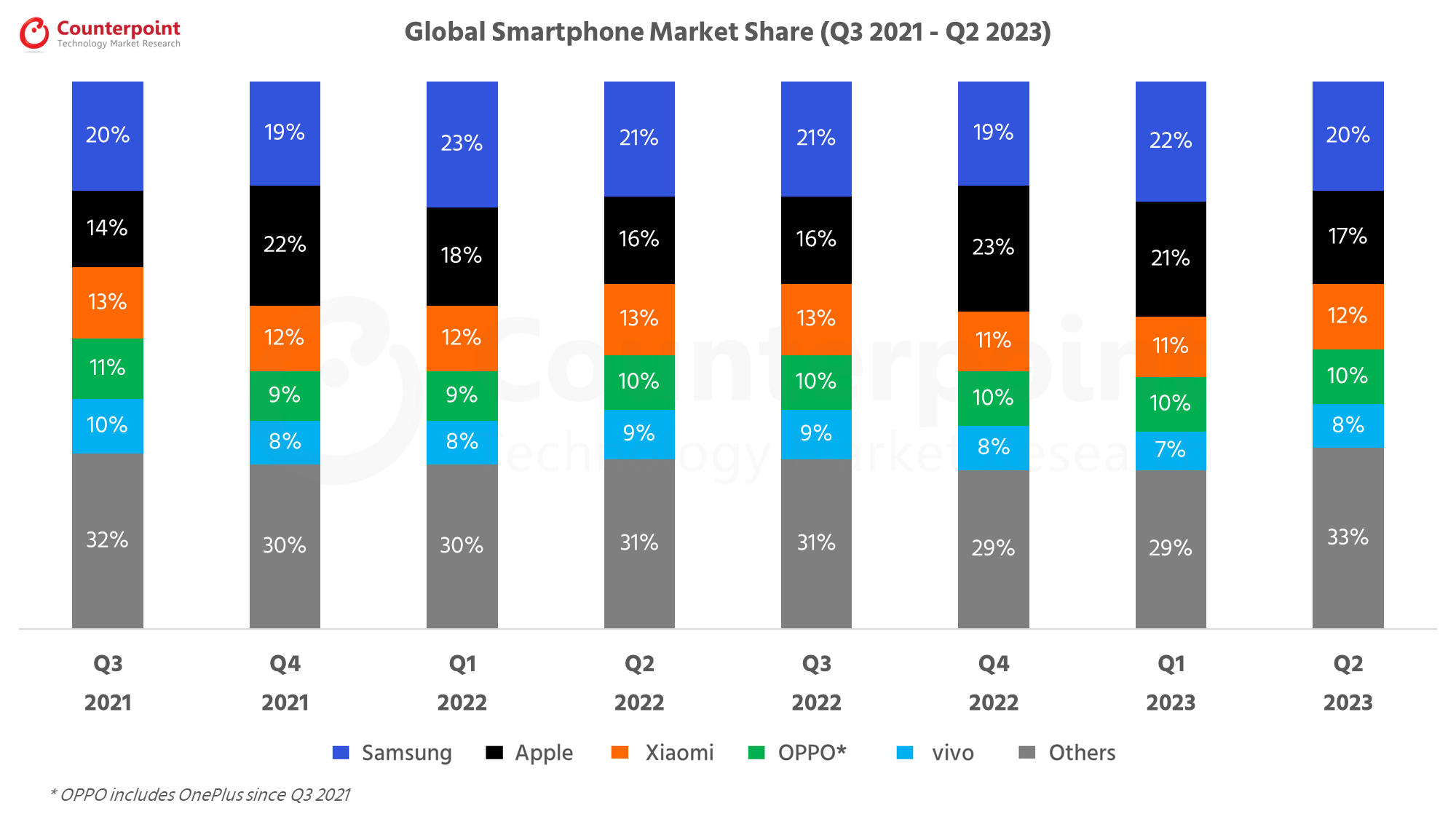

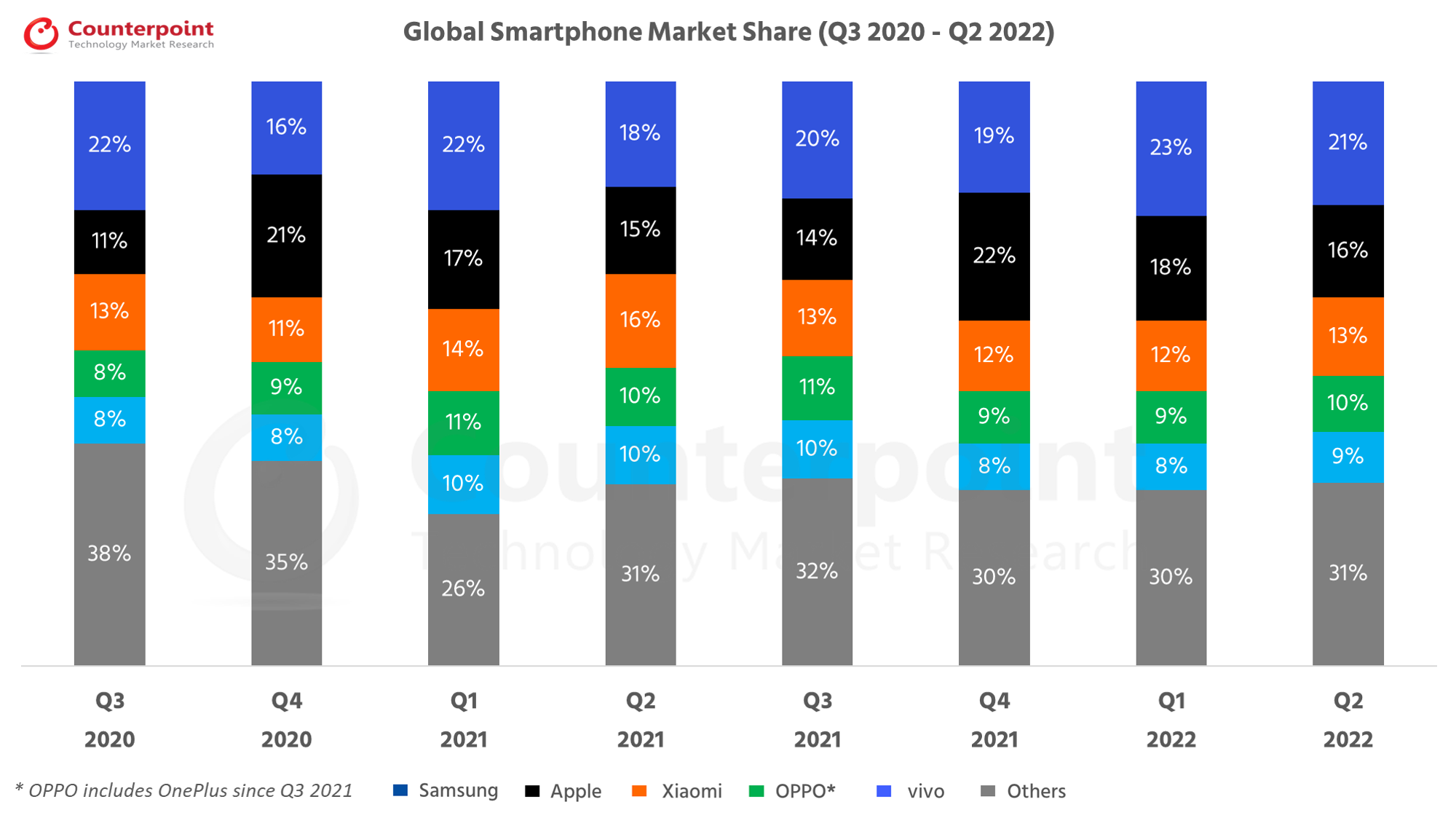

Global Smartphone Shipments Market Data (Q3 2021 – Q2 2023)

Published Date: August 17, 2023

A repository of quarterly data for the global smartphone market. This data is a part of a series of reports which track the mobile handset market:Smartphone and Feature Phone shipmentsevery quarter for more than 140 brands covering more than 95% of the totaldevice shipmentsin the industry.

Global smartphone market share Q2 2023 highlights:

The global smartphone market declined by 9% YoY to reach 268 million units in Q2 2023.

Samsung retained its position as the top smartphone player in Q2 2023, as Apple saw cyclical decline.

Among the top five brands, Apple experienced the least YoY shipment decline. Among the top 10 brands, Tecno and Infinix, part of the Transsion Group, saw double digit annual growth.

在中东地区表现方面,和Africa (MEA) exhibited the only annual shipment growth while North America experienced the highest decline.

The top 5 brands contributed to almost 80% of the total 5G shipments in Q2 2023.

The global smartphone market share numbers are from:

MOBILE DEVICES MONITOR – Q2 2023 (Vendor Region Countries)

这个报告是一系列的报告的一部分track the mobile handset market: Smartphone and Feature Phone shipments every quarter for more than 140 brands covering more than 95% of the total device shipments in the industry.

The deliverable includes

• Single pivot format giving in-depth analysis of theglobal handset market • Covers140 +品牌now in comparison to 95 brands earlier • Break out of3 key countriesin each regionto give a further granular view of the regions •18 countries viewas compared to six earlier • Covers more than95% of the global handset shipments • More visuals and analysis by country and by regions

This robust quarterly report with fact-based deep analysis covering multiple dimensions will help players across the handset value chain to holistically analyze the current state of the global handset market and plan ahead of the competition.

This data represents the global smartphone market share by quarter (from 2021-2023) by top OEMs. Global smartphone shipments by market share and millions of units are provided.

For detailed insights on the data, please reach out to us atsales(at)www.arena-ruc.com. If you are a member of the press, please contact us atpress(at)www.arena-ruc.comfor any media enquiries.

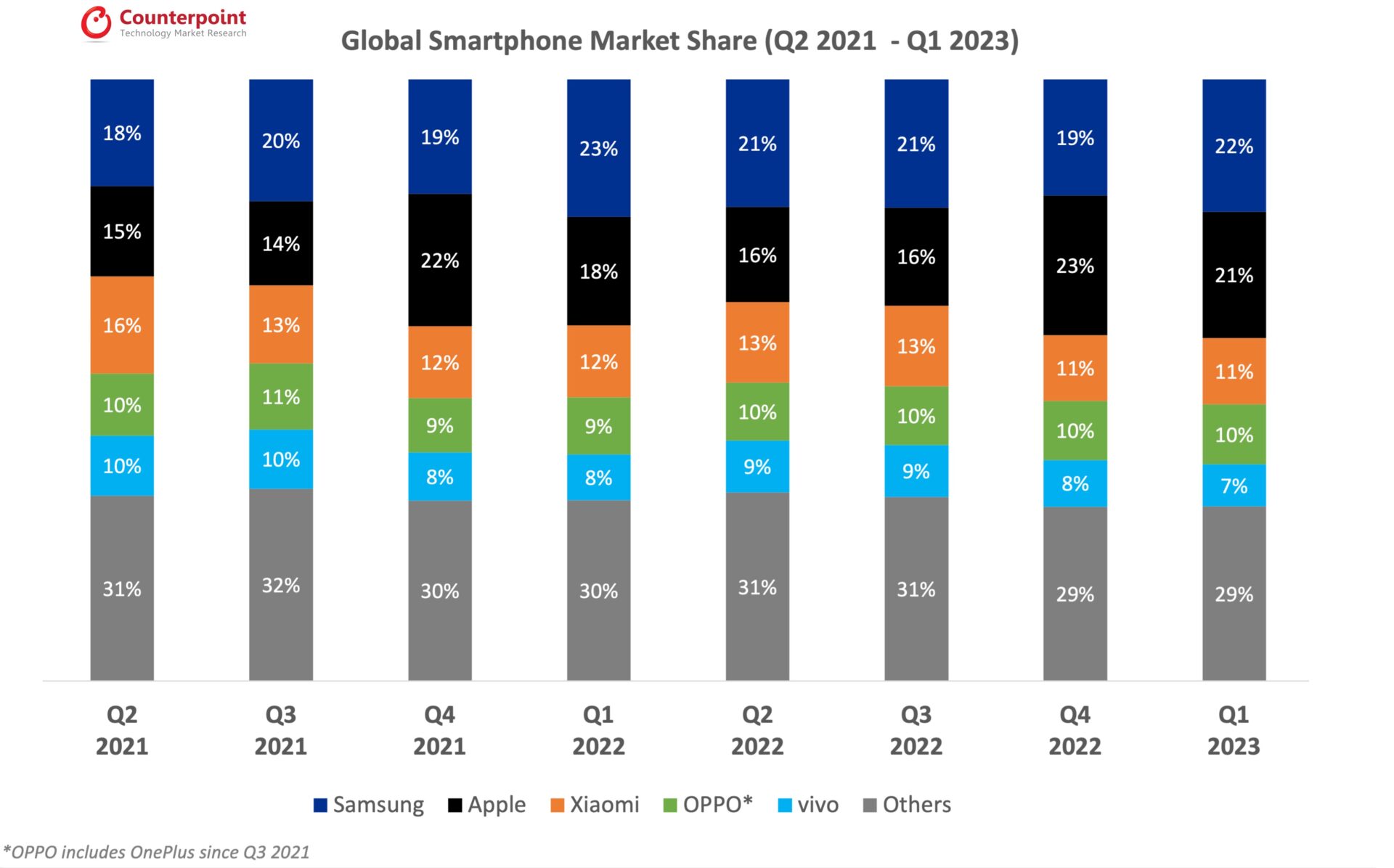

Q1 2023 Highlights

Published Date: May 9, 2023

Highlights:

The global smartphone market declined by 14% YoY and 7% QoQ to record 280.2 million unit shipments in Q1 2023.

Samsung replaced Apple as the top smartphone player in Q1 2023, driven by its mid-tier A Series and the recently launched S23 series.

Apple’s YoY shipment decline was the least among the top five brands. Consequently, it recorded its highest-ever Q1 share of 21%.

Global smartphone revenues declined by 7% YoY to around $104 billion. Apple, Samsung, Xiaomi increased their Average Selling Prices YoY.

*OPPO includes OnePlus since Q3 2021 **Ranking is according to the latest quarter.

Frequently asked question (FAQs):

• What’s the global market size for smartphones? The global smartphone market shipments declined to reach 280.2 million units in Q1 2023.

• What is the global market for mobile phones? The 2022 global smartphone shipments declined to 1.2 billion units, the lowest since 2013.

• Who dominates the smartphone market? Apple dominated the smartphone market in 2022 by achieving its highest-ever global shipments, revenue and operating profit share.

• How fast is the smartphone market growing? The global smartphone shipments declined by 12% in 2022.

*OPPO includes OnePlus since Q3 2021 **Ranking is according to the latest quarter.

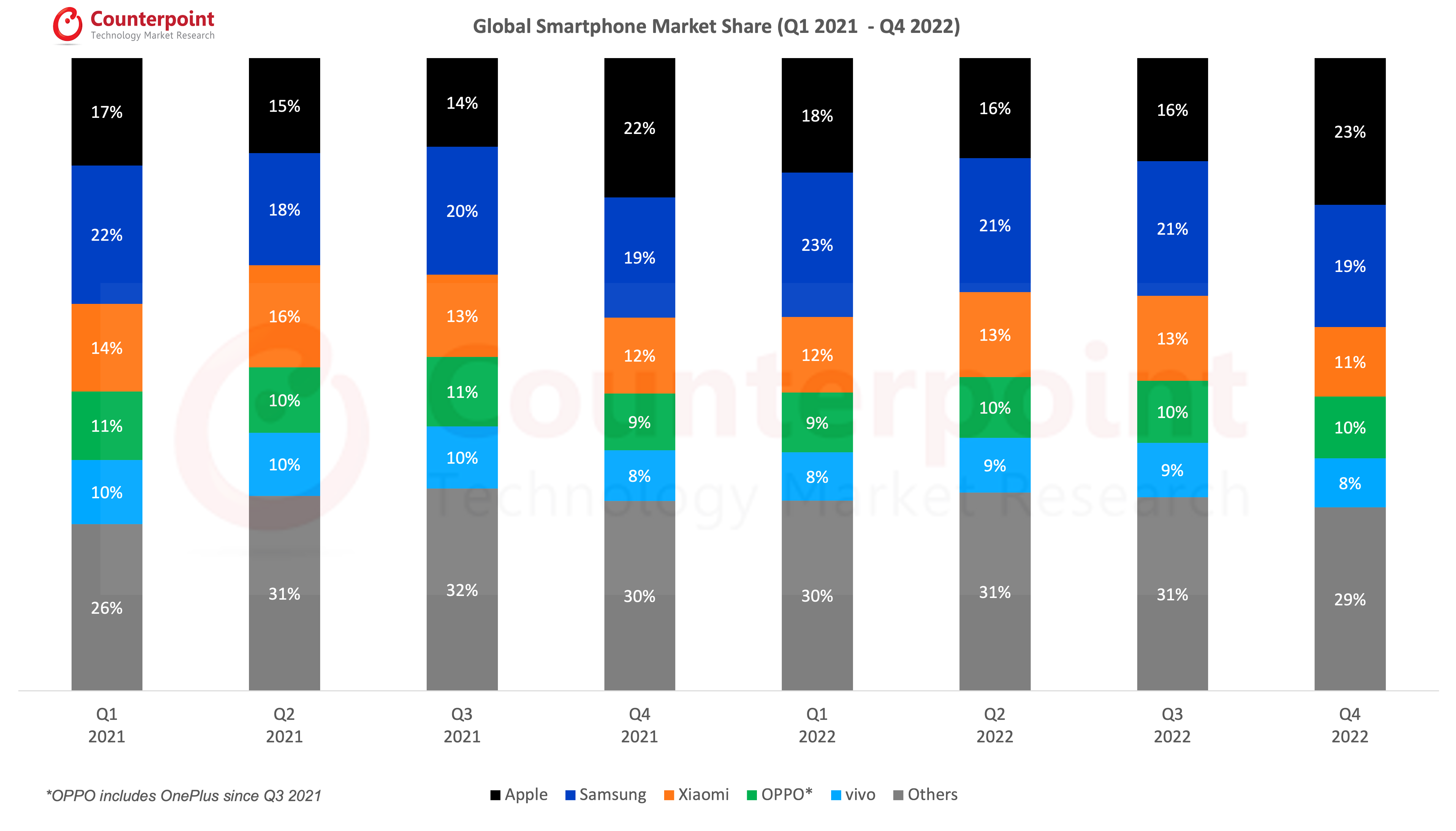

Q3 2022 Highlights

Published Date: December 20, 2022

The global smartphone market declined by 12% YoY even as it grew by 2% QoQ to reach 301 million units in Q3 2022.

While quarterly growth in Apple and Samsung pushed the global smartphone market above 300 million units, a level it failed to reach last quarter, political and economic instability drove negative consumer sentiment.

Apple was the only top-five smartphone brand to grow YoY, with shipments increasing 2% YoY, growing market share by two percentage points to 16%.

Samsung’s shipments declined by 8% YoY but grew 5% QoQ to 64 million.

Xiaomi, OPPO* and vivo, recovered slightly after receiving heavy beatings due to lockdowns in China in Q2, and as they captured more of the market ceded by Apple and Samsung’s exit from Russia.

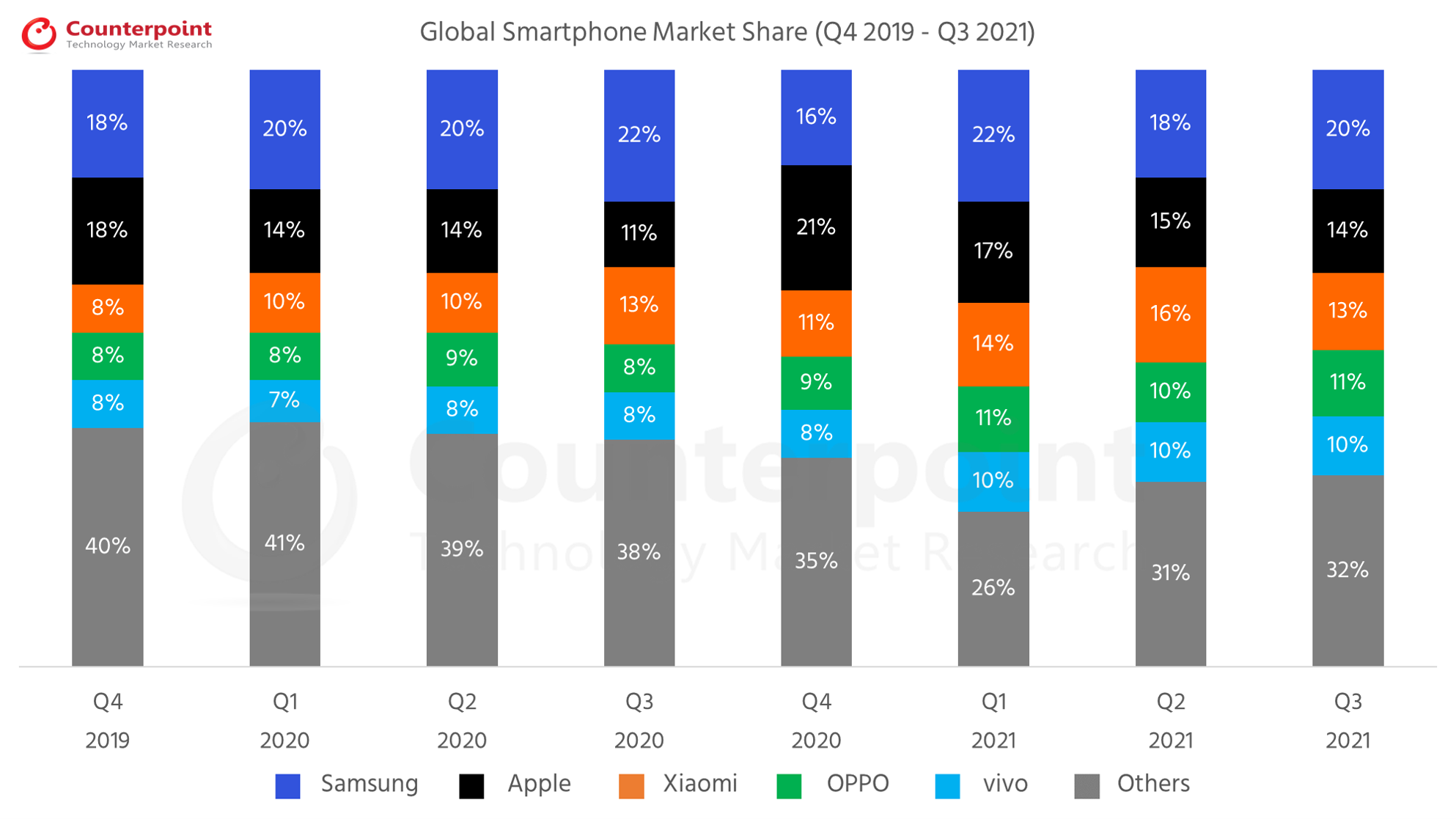

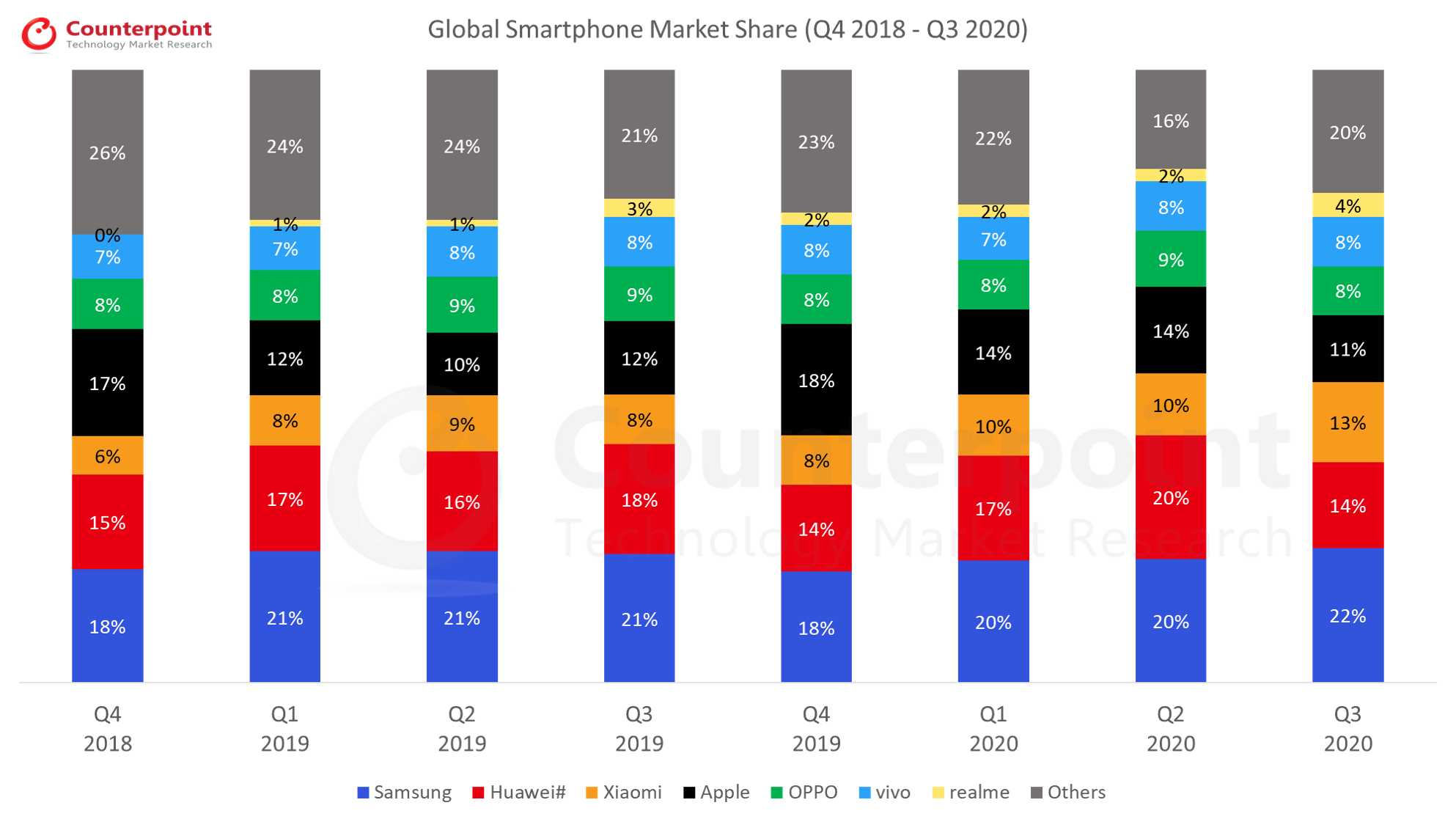

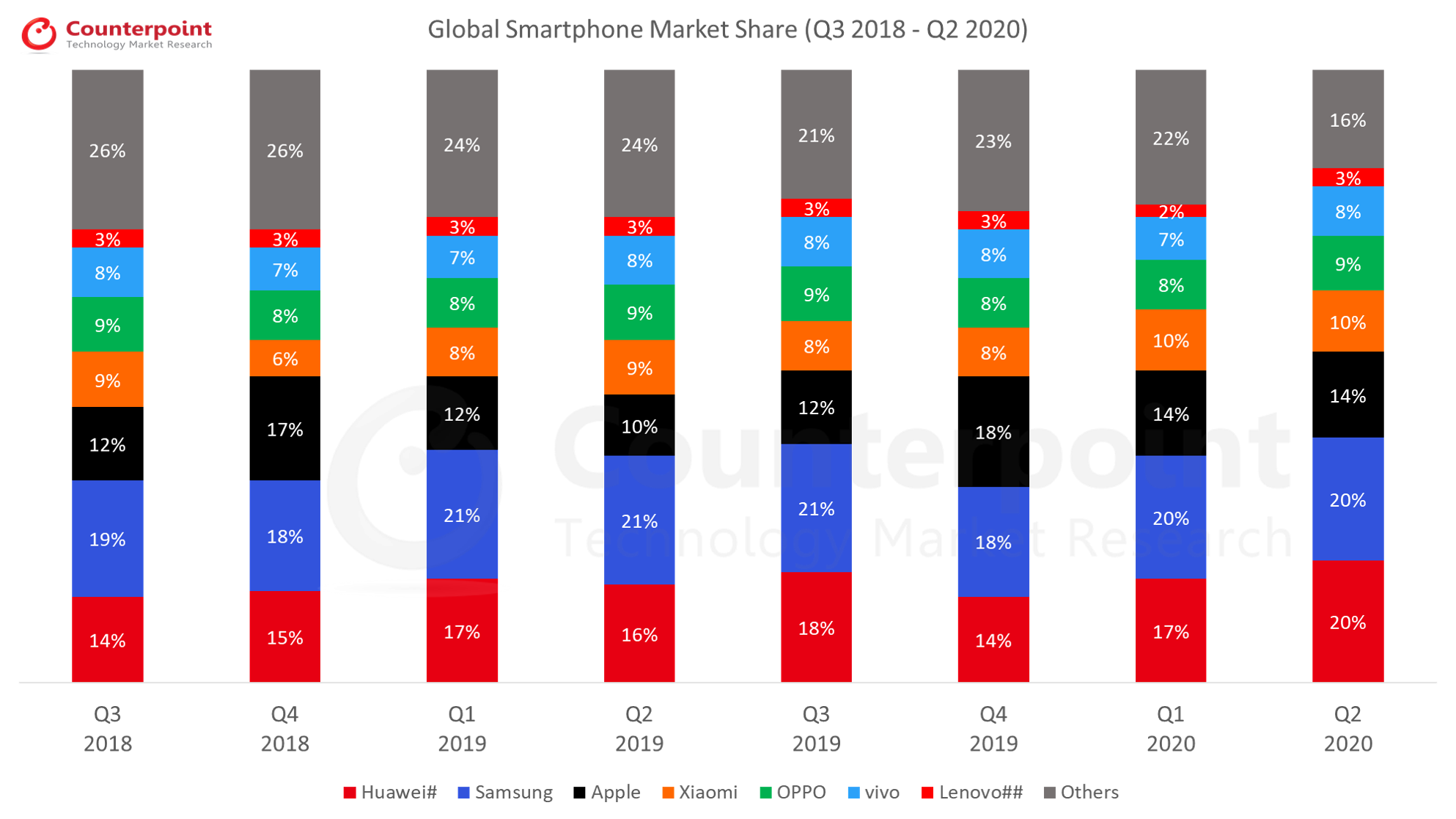

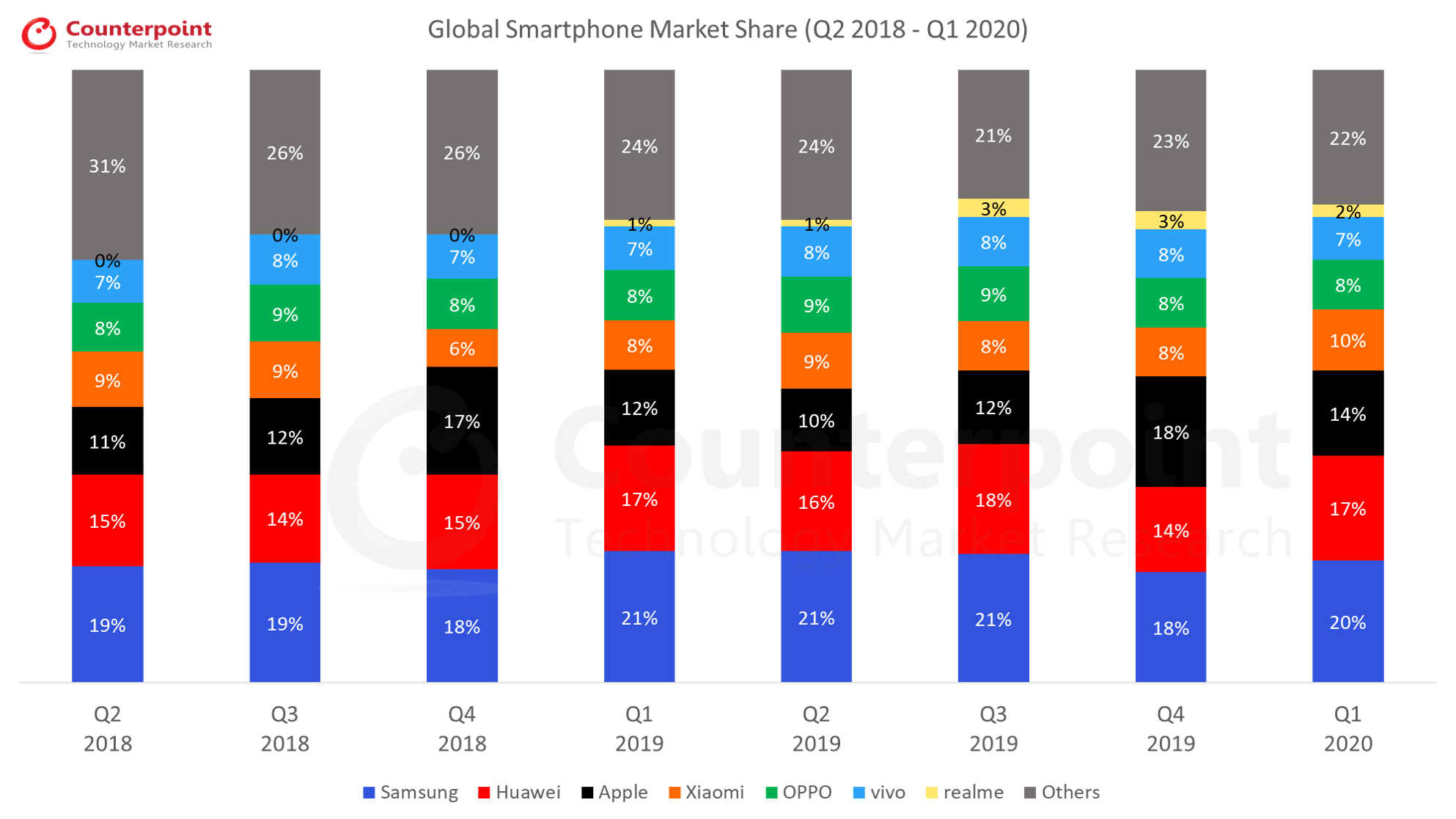

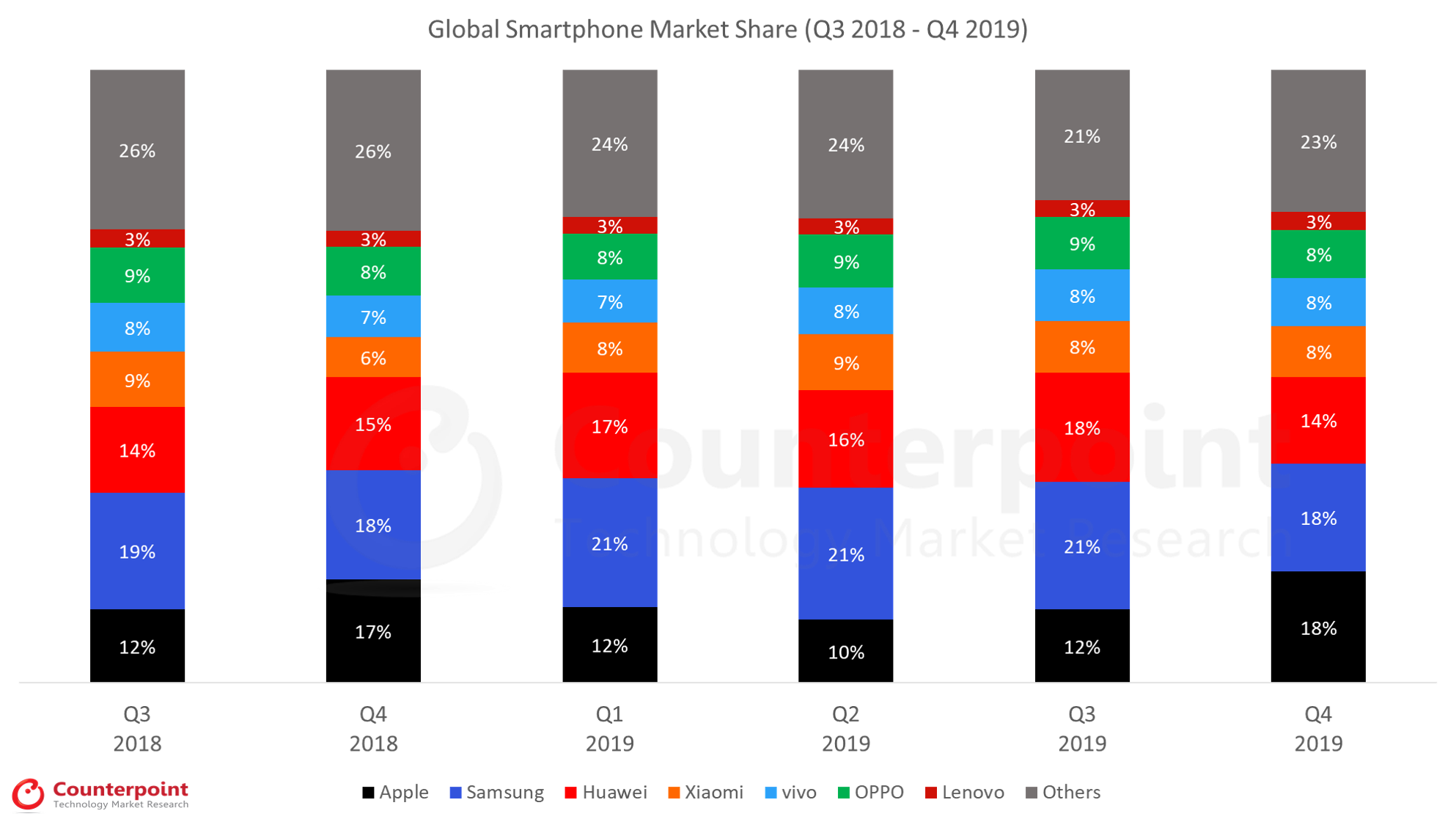

Global Smartphone Shipments Market Share (%)

Brands

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Q1 2022

Q2 2022

Q3 2022

Samsung

16%

22%

18%

20%

19%

23%

21%

21%

Apple

21%

17%

15%

14%

22%

18%

16%

16%

Xiaomi

11%

14%

16%

13%

12%

12%

13%

13%

OPPO*

9%

11%

10%

11%

9%

9%

10%

10%

vivo

8%

10%

10%

10%

8%

8%

9%

9%

Others

35%

26%

31%

32%

30%

30%

31%

31%

Global Smartphone Shipments(in Millions)

Brands

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Q1 2022

Q2 2022

Q3 2022

Samsung

62.5

76.6

57.6

69.3

69.0

74.5

62.5

64.3

Apple

81.9

59.5

48.9

48.0

81.5

59.0

46.5

49.2

Xiaomi

43.0

48.5

52.5

44.4

45.0

39.0

39.5

40.5

OPPO*

34.0

38

33.6

38.1

33.9

30.9

28.2

29.5

vivo

33.4

35.5

32.5

33.7

29.3

24.8

25.2

26.0

Others

139.8

96.8

98.0

108.5

112.7

98.1

92.3

92.4

Total Market

394.6

354.9

323.1

342.0

371.4

326.4

294.5

301.9

*OPPO includes OnePlus since Q3 2021 **Ranking is according to the latest quarter.

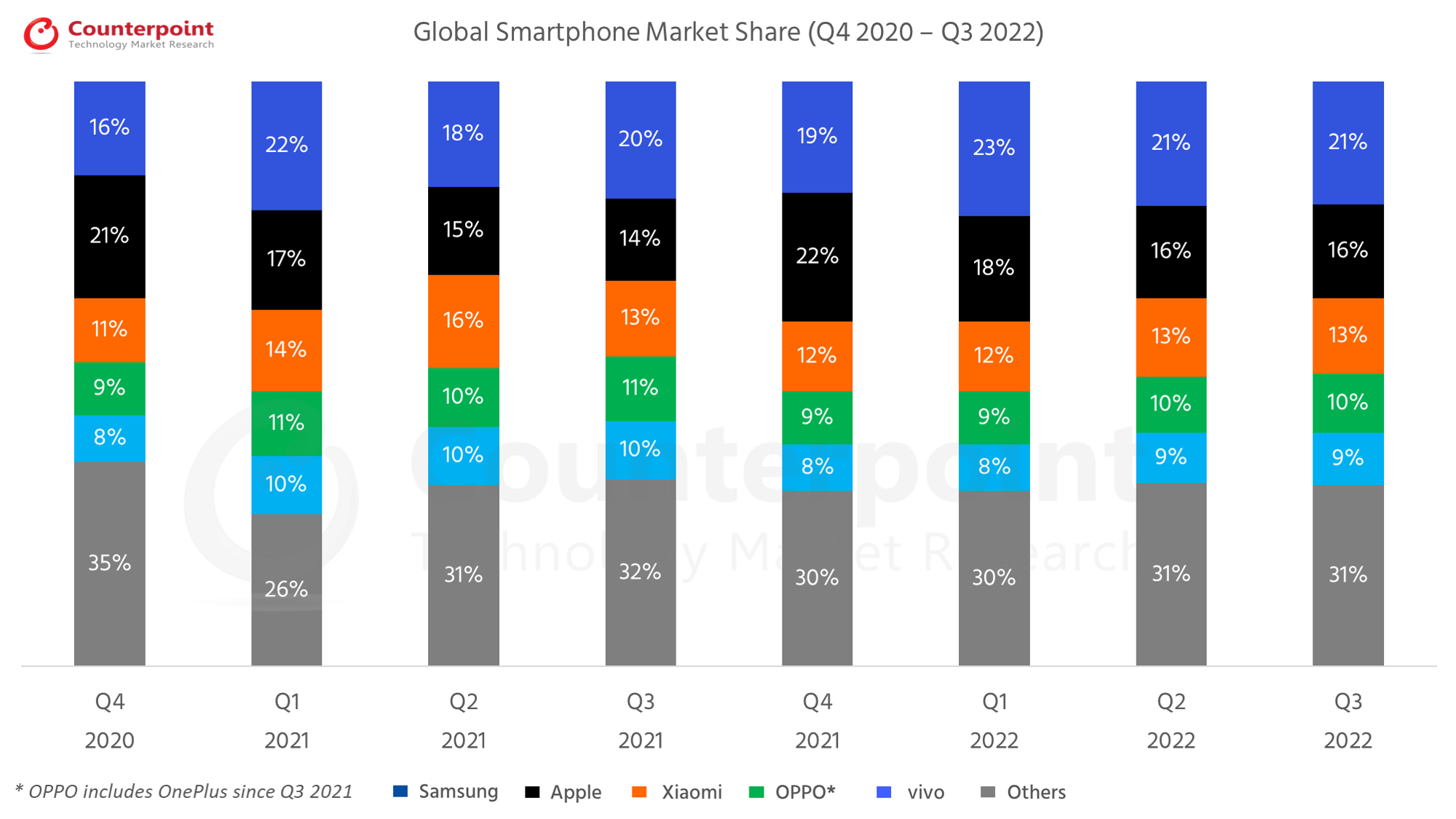

Q2 2022 Highlights

Published Date: August 16, 2022

• The global smartphone market growth saw a decline of 9% YoY and 10% QoQ to 294.5 million units in Q2 2022. • Global smartphone market share carries on consolidation, with top three brands commanding 50% share for three consecutive quarters. • This was the first time quarterly shipments dropped below 300 million units since Q2 2020 during the early part of the COVID-19 pandemic. • Samsung was the only top-five smartphone brand to grow YoY, increasing shipments by 8% YoY and growing market share by three percentage points to 21%. • Apple market share declined by 5% YoY in Q2 2022, although its share increased in a diminished market. • iPhone shipment market share continues to edge upwards, with Apple reaching its highest Q2 2022 shipment share ever • The Android vs iOS market share battle, traditionally contested by Apple in the US, Europe and Japan, is intensifying in markets like China, which is becoming a significant driver of iOS installed based globally. • Xiaomi, OPPO* and vivo, hit by China lockdowns, suffered double digit YoY declines in their respective shipments.

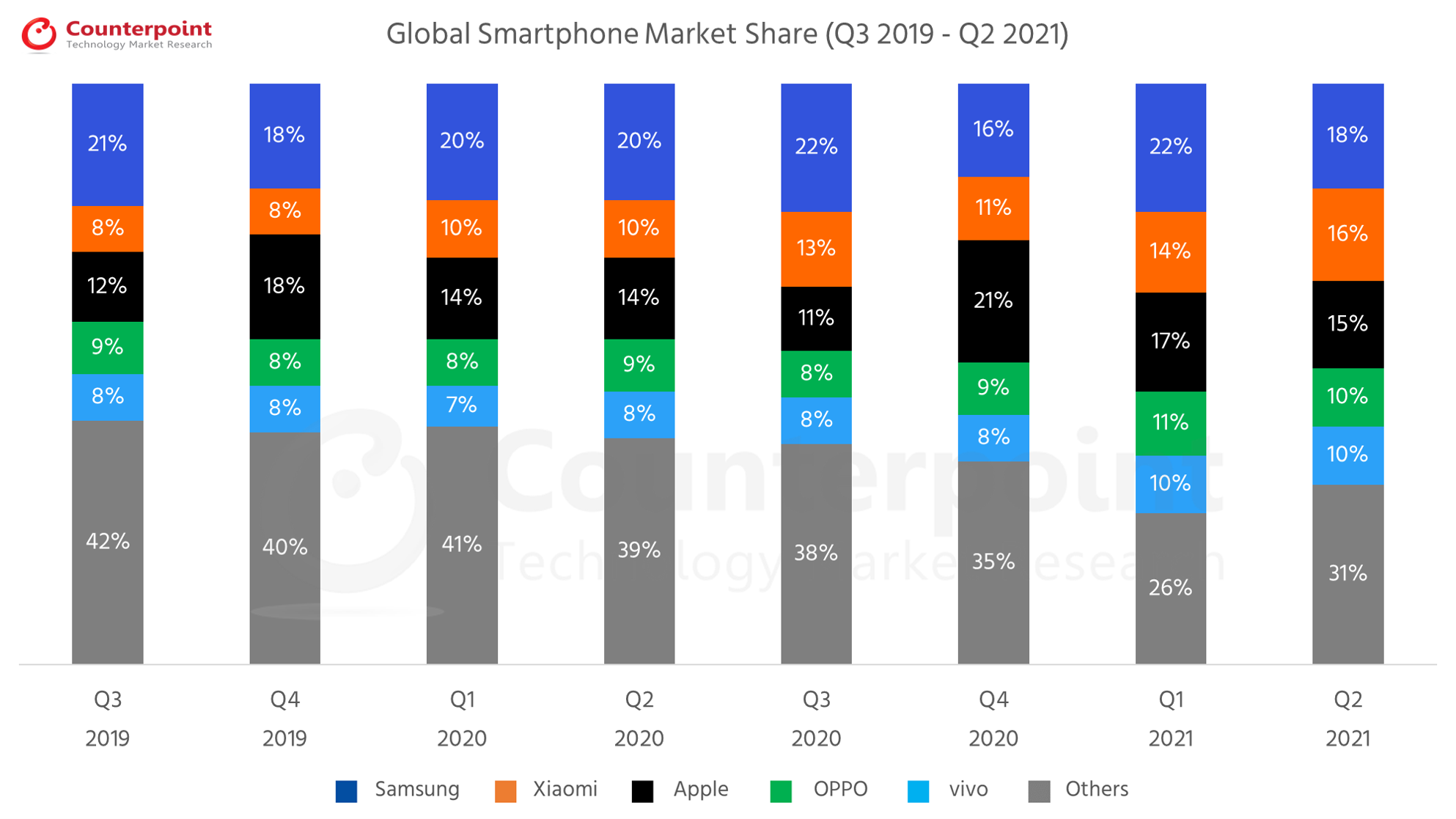

Global Smartphone Shipments Market Share (%)

Brands

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Q1 2022

Q2 2022

Samsung

22%

16%

22%

18%

20%

19%

23%

21%

Apple

11%

21%

17%

15%

14%

22%

18%

16%

Xiaomi

13%

11%

14%

16%

13%

12%

12%

13%

OPPO*

8%

9%

11%

10%

11%

9%

9%

10%

vivo

8%

8%

10%

10%

10%

8%

8%

9%

Others

38%

35%

26%

31%

32%

30%

30%

31%

Global Smartphone Shipments(in Millions)

Brands

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Q1 2022

Q2 2022

Samsung

80.4

62.5

76.6

57.6

69.3

69.0

74.5

62.5

Apple

41.7

81.9

59.5

48.9

48.0

81.5

59.0

46.5

Xiaomi

46.5

43.0

48.5

52.5

44.4

45.0

39.0

39.5

OPPO*

31.0

34.0

38.0

33.6

38.1

33.9

30.9

28.2

vivo

31.0

33.4

35.5

32.5

33.7

29.3

24.8

25.5

Others

135.0

139.8

96.8

98.0

108.5

112.7

98.2

92.3

Total Market

365.6

394.6

354.9

323.1

342.0

371.4

326.4

294.5

*OPPO includes OnePlus since Q3 2021 **Ranking is according to the latest quarter.

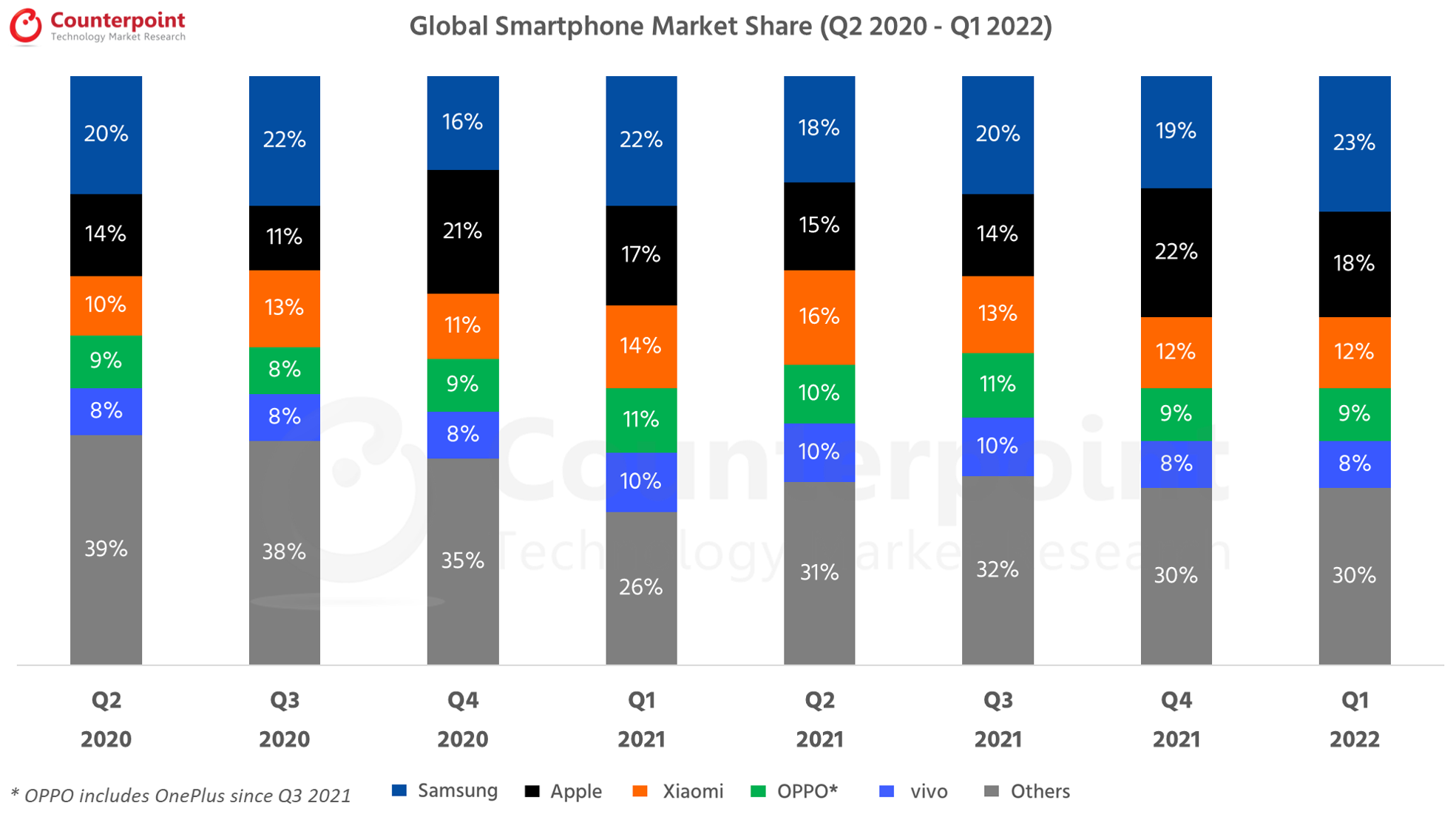

Q1 2022 Highlights

Published Date: May 16, 2022

• The global smartphone market declined by 7% YoY and 12% QoQ to 328 million units in Q1 2022. • While Samsung’s shipments declined 3% YoY, it was the only top-five smartphone brand to grow QoQ. Its market share rose to 23% from 19% last quarter, resulting in Samsung taking the top spot from Apple in Q1 2022. • Apple’s shipments declined by 1% annually to reach 59 million units in Q1 2022. This was after an expected seasonal quarterly shipment decline of 28%. • Xiaomi, OPPO* and vivo’s component struggles continued, causing a quarterly and annual decline in their respective shipments.

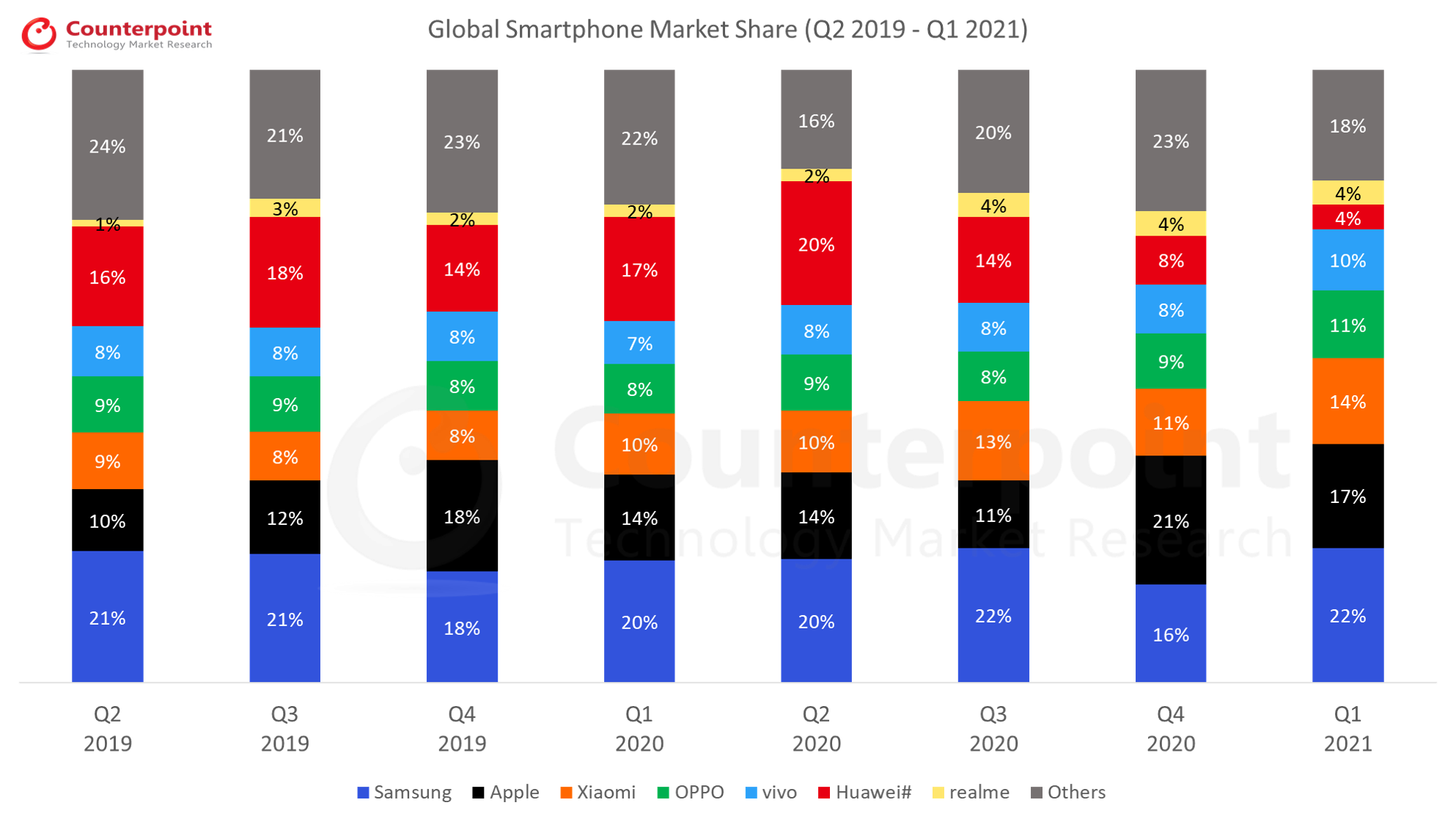

Global Smartphone Shipments Market Share (%)

Brands

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Q1 2022

Samsung

20%

22%

16%

22%

18%

20%

19%

23%

Apple

14%

11%

21%

17%

15%

14%

22%

18%

Xiaomi

10%

13%

11%

14%

16%

13%

12%

12%

OPPO*

9%

8%

9%

11%

10%

11%

9%

9%

vivo

8%

8%

8%

10%

10%

10%

8%

8%

Others

39%

38%

35%

26%

31%

32%

30%

30%

Global Smartphone Shipments (in Millions)

Brands

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Q1 2022

Samsung

54.2

80.4

62.5

76.6

57.6

69.3

69.0

74.5

Apple

37.5

41.7

81.9

59.5

48.9

48.0

81.5

59.0

Xiaomi

26.5

46.5

43.0

48.5

52.5

44.4

45.0

39.0

OPPO

24.5

31.0

34.0

38.0

33.6

38.1

33.9

30.9

vivo

22.5

31.0

33.4

35.5

32.5

33.7

29.3

24.8

Others

110.9

135.0

139.8

96.8

98.0

108.5

112.7

98.1

Total Market

276.1

365.6

394.6

354.9

323.1

342.0

371.4

326.4

*OPPO includes OnePlus since Q3 2021 **Ranking is according to the latest quarter.

Why is the smartphone market declining in Q1 2022?

The global smartphone market growth saw a decline of 7% YoY, shipping 328 million units in Q1 2022 caused by the ongoing component shortages, as well as COVID resurgence at the beginning of the quarter and the Russia-Ukraine war towards the end. The global smartphone market also, as expected, had a seasonal decline of 12% QoQ. The component supply crunch was felt more severely by major Chinese OEMs such as Xiaomi, OPPO* and vivo as compared with Samsung, which seems to have overcome component shortages that affected its supply last year, as evidenced by higher-than-expected growth in its shipments despite a late flagship launch.

Consequently, Samsung regained the top spot from Apple which had emerged as the biggest smartphone vendor globally in Q4 2021 thanks to its latest iPhone 13 series.

Which country has the highest market share of smartphones globally?

With its share at around 22.5% of the global smartphone shipments in Q1 2022,Chinaremains the world’s biggest smartphone market. This is down from around 25.6% in Q1 2021 as China’s economy grew slower than expected due to COVID-related lockdowns and shipment volumes declined by over 19% YoY. While China’s share of global smartphone market growth (shipments) remains flat QoQ thanks to a small peak in demand during Chinese New Year and as the global smartphone market declined QoQ due to seasonality, in terms of absolute shipments, China saw a quarterly decline of over 12%.

HONOR has emerged as the biggest smartphone player in China, chipping into vivo and OPPO*’s shares and stepping into the position previously held by Huawei from which it recently separated. Although vivo did not succeed in regaining the top position due to HONOR’s rise at a time when it is itself facing component shortages, it did recover somewhat thanks to its newly launched mid-end S12 series that is popular with younger customers and the affordable the Y series which showed strong performance in the quarter.

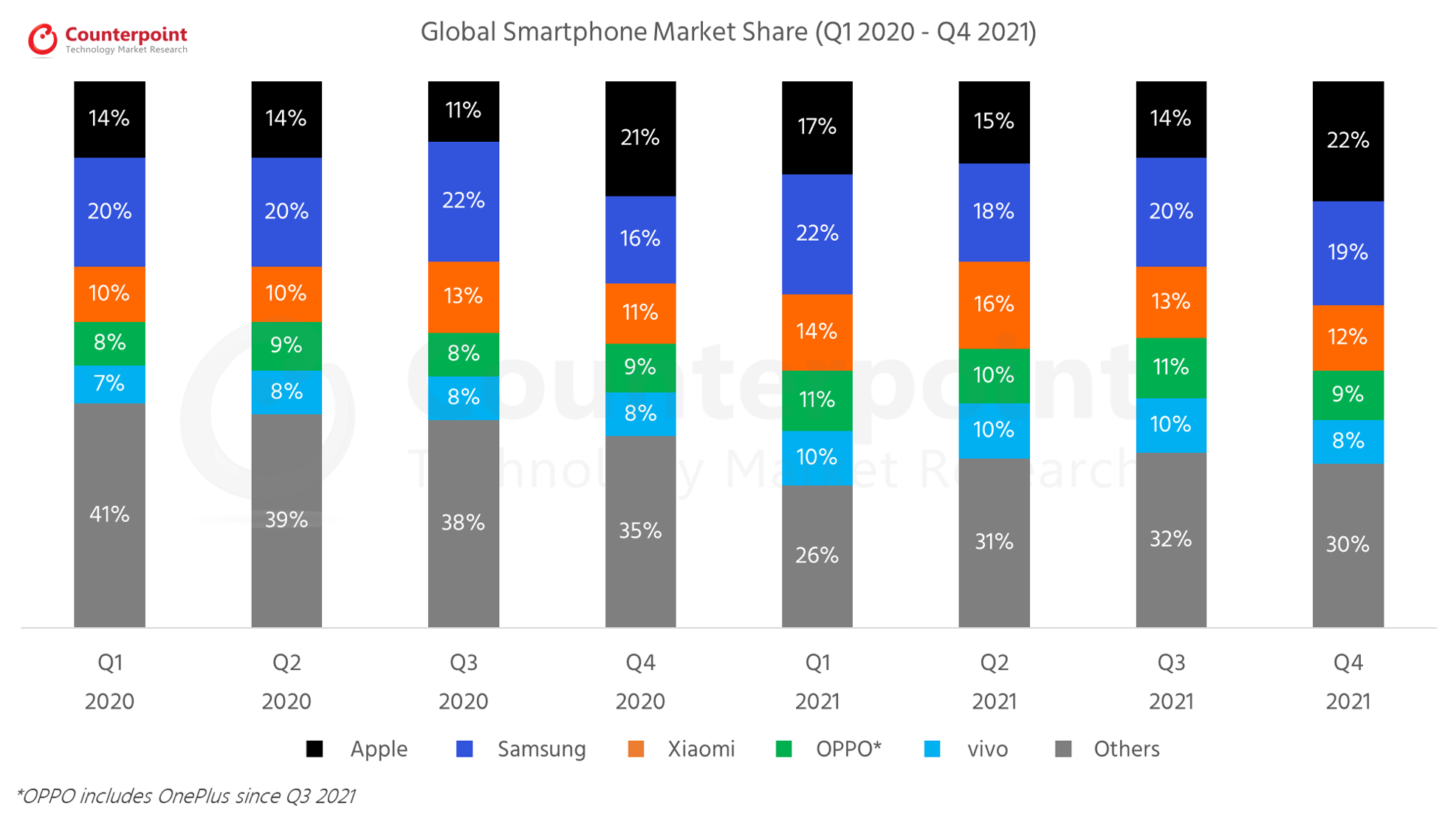

Q4 2021 Highlights

Published Date: February 16, 2022

• Global smartphone market growth saw an increase of 4% YoY to reach 1.39 billion units in 2021. Q4 2021 shipments declined 6% YoY to reach 371 million units. • Samsung led the global smartphone market in 2021 with annual shipments of 272 million units. • Apple, Xiaomi, OPPO^ and vivo recorded their highest-ever annual shipments. • The top five brands gained share due to a significant decline by Huawei, and LG’s exit from the market. • Apple surpassed Samsung to take the number one spot in Q4 2021 with smartphone shipments increasing by 70% QoQ to 81.5 million units in Q4 2021, despite remaining flat YoY. • Apple recorded their highest-ever annual shipments of 237.9 million units in 2021 driven by successful launch of iPhone 13 series and consistent performance of iPhone 12 series.

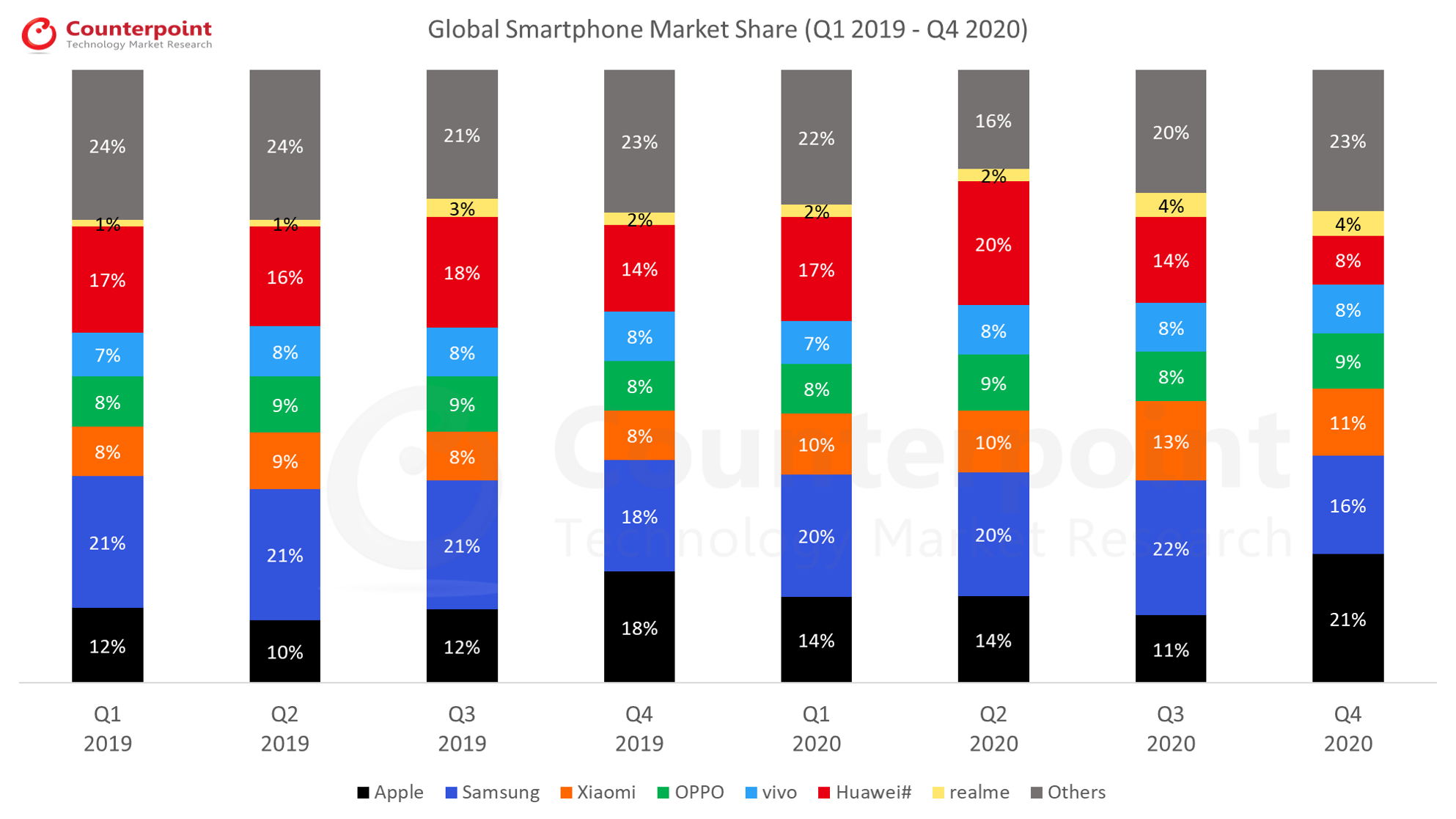

Global Smartphone Shipments Market Share (%)

Brands

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Apple

14%

14%

11%

21%

17%

15%

14%

22%

Samsung

20%

20%

22%

16%

22%

18%

20%

19%

Xiaomi

10%

10%

13%

11%

14%

16%

13%

12%

OPPO*

8%

9%

8%

9%

11%

10%

11%

9%

vivo

7%

8%

8%

8%

10%

10%

10%

8%

Others

41%

39%

38%

35%

26%

31%

32%

30%

Global Smartphone Shipments (in Millions)

Brands

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Apple

40.0

37.5

41.7

81.9

59.5

48.9

48.0

81.5

Samsung

58.6

54.2

80.4

62.5

76.6

57.6

69.3

69.0

Xiaomi

29.7

26.5

46.5

43.0

48.5

52.5

44.4

45.0

OPPO*

22.3

24.5

31.0

34.0

38.0

33.6

38.1

33.9

vivo

21.6

22.5

31.0

33.4

35.5

32.5

33.7

29.3

Others

122.8

110.9

135.0

139.8

96.8

98.0

108.5

112.7

Total Market

295.0

276.1

365.6

394.6

354.9

323.1

342.0

371.4

*OPPO includes OnePlus since Q3 2021 **Ranking is according to the latest quarter.

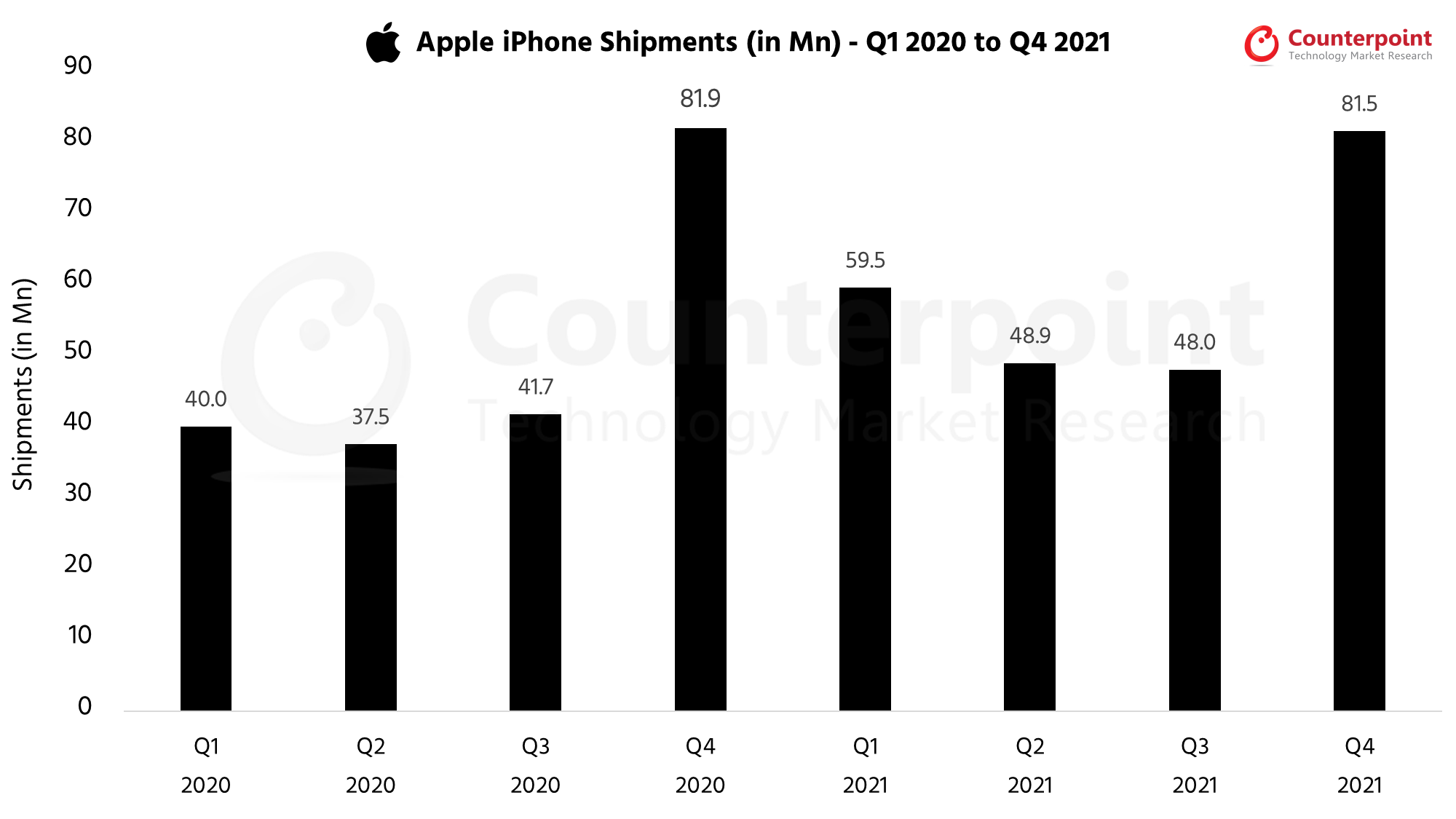

Apple Market Share: Q4 2021

Apple Market Share (iPhone Shipments in Millions)

Quarter

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Ship-ments (in Mn)

40.0

37.5

41.7

81.9

59.5

48.9

48.0

81.5

Q3 2021 Highlights

Published Date: November 16, 2021

• The global smartphone market growth saw an increase of 6% QoQ but declined by 6% YoY in Q3 2021, clocking global shipments of 342 million units, down from 365.6 million in Q3 2020. • Samsung retained the number one spot in Q3 2021 with smartphone shipments increasing by 20% QoQ to 69.3 million units in Q3 2021. • Xiaomi shipped 44.4 million units in Q3 2021, down 5% YoY and 15% QoQ as it was severely hit by the ongoing component shortages. • vivo grew 8% YoY and 3% QoQ to reach 33.7 million units. vivo continued to lead China’s smartphone market with 17.3 million units in Q3 2021. •realmeachieved its highest-ever shipment performance with 16.2 million units in Q3 2021. The record quarter came at a time when component shortages were at their peak. • Global handset market wholesale revenue grew 10% YoY and 6% QoQ in Q3 2021 to reach over $103 billion.

Global Smartphone Shipments Market Share (%)

Brands

Q4 2019

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Samsung

18%

20%

20%

22%

16%

22%

18%

20%

Apple

18%

14%

14%

11%

21%

17%

15%

14%

Xiaomi

8%

10%

10%

13%

11%

14%

16%

13%

OPPO

8%

8%

9%

8%

9%

11%

10%

11%

vivo

8%

7%

8%

8%

8%

10%

10%

10%

Others

40%

41%

39%

38%

35%

26%

31%

32%

Global Smartphone Shipments

Brands

Q4 2019

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Samsung

70.4

58.6

54.2

80.4

62.5

76.6

57.6

69.3

Apple

72.3

40.0

37.5

41.7

81.9

59.5

48.9

48.0

Xiaomi

32.9

29.7

26.5

46.5

43.0

48.5

52.5

44.4

OPPO

30.7

22.3

24.5

31.0

34.0

38.0

33.6

38.1

vivo

31.5

21.6

22.5

31.0

33.4

35.5

32.5

33.7

Others

163.4

122.8

110.9

135.0

139.8

96.8

98.0

108.5

Total Market

401.1

295.0

276.1

365.6

394.6

354.9

323.1

342.0

*Ranking is according to the latest quarter.

Q2 2021 Highlights

Published Date: August 16, 2021

• Global smartphone market grew 19% YoY but declined by 7% QoQ as 323 million units were shipped, led by Samsung. • Xiaomi eclipses 52 million smartphones, becoming the world’s second-largest smartphone brand for the first time ever. • Samsung retained the number one spot with shipments reaching 58 million units in Q2 2021, however, its market share declined to 18% as compared to 22% in Q1 2021 as its shipments declined by 24% QoQ. •realmegrew by 135% YoY and 17% QoQ, crossing cumulative shipments of 100 million smartphones since its entry into the smartphone market. • Global smartphone shipment revenues grew by 25% YoY to $96 billion in Q2 2021 setting a second-quarter record.

Global Smartphone Shipments Market Share (%)

Brands

Q3 2019

Q4 2019

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Samsung

21%

18%

20%

20%

22%

16%

22%

18%

Xiaomi

8%

8%

10%

10%

13%

11%

14%

16%

Apple

12%

18%

14%

14%

11%

21%

17%

15%

OPPO

9%

8%

8%

9%

8%

9%

11%

10%

vivo

8%

8%

7%

8%

8%

8%

10%

10%

Others

42%

40%

41%

39%

38%

35%

26%

31%

Global Smartphone Shipments

Brands

Q3 2019

Q4 2019

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Samsung

78.2

70.4

58.6

54.2

80.4

62.5

76.6

57.9

Xiaomi

31.7

32.9

29.7

26.5

46.2

43.0

48.5

52.5

Apple

44.8

72.3

40.0

37.5

41.7

81.9

59.5

48.9

OPPO

32.3

31.4

22.3

24.5

31.0

34.0

38.0

33.6

vivo

31.3

31.5

21.6

22.5

31.0

33.4

35.5

32.5

Others

161.7

162.6

122.8

110.9

135.3

139.8

96.8

97.7

Total

Market

380.0

401.1

295.0

276.1

365.6

394.6

354.9

323.1

*Ranking is according to the latest quarter.

Q1 2021 Highlights

Published Date: May 16, 2021

• Global smartphone shipment revenue crossed the $100 billion mark for the first time for a March-ending quarter to reach $113 billion. • Global shipments grew 20% YoY, reaching 354 million units, led by OPPO, vivo, Xiaomi and Apple. • Samsung regained its top spot as the world’s biggest OEM, with shipments reaching 76.8 million units in Q1 2021. • Apple iPhone active installed base reached a new high this quarter.

Global Smartphone Shipments Market Share (%)

Brands

Q2 2019

Q3 2019

Q4 2019

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Samsung

21%

21%

18%

20%

20%

22%

16%

22%

Apple

10%

12%

18%

14%

14%

11%

21%

17%

Xiaomi

9%

8%

8%

10%

10%

13%

11%

14%

OPPO

9%

9%

8%

8%

9%

8%

9%

11%

vivo

8%

8%

8%

7%

8%

8%

8%

10%

Huawei#

16%

18%

14%

17%

20%

14%

8%

4%

realme

1%

3%

2%

2%

2%

4%

4%

4%

Others

24%

21%

23%

22%

16%

20%

23%

18%

Global Smartphone Shipments

Brands

Q2 2019

Q3 2019

Q4 2019

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Samsung

76.3

78.2

70.4

58.6

54.2

80.4

62.5

76.6

Apple

36.5

44.8

72.3

40.0

37.5

41.7

81.9

59.5

Xiaomi

32.3

31.7

32.9

29.7

26.5

46.2

43.0

48.5

OPPO

30.6

32.3

31.4

22.3

24.5

31.0

34.0

38.0

vivo

27.0

31.3

31.5

21.6

22.5

31.0

33.4

35.5

Huawei#

56.6

66.8

56.2

49.0

54.8

50.9

33.0

15.0

realme

5.0

10.2

7.8

7.2

6.4

14.8

14.0

12.8

Others

92.8

84.7

98.6

66.6

49.7

69.6

92.8

69.0

Total

Market

357.1

380.0

401.1

295.0

276.1

365.6

394.6

354.9

*Ranking is according to the latest quarter.

#Huawei includes HONOR in all quarters except Q1 2021 reflecting the separation of the two brands.

Q4 2020 Highlights

Published Date: February 16, 2021

• The global smartphone market continued to recover in Q4 2020, rebounding 8% QoQ to 395.9 million units. • Apple’s 8% YoY and 96% QoQ growth helped it lead the market in Q4 2020. • Samsung slipped to the second spot with 62.5 million units in Q4 2020, However, it led the overall market in CY 2020. • For the first time, OPPO and vivo surpassed Huawei to capture the fourth and fifth spots respectively, Huawei slipped to the sixth spot. •realmeemerged as the fastest growing brand in CY 2020 with 65% YoY growth.

Global Smartphone Shipments Market Share (%)

Brands

Q1 2019

Q2 2019

Q3 2019

Q4 2019

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Apple

12%

10%

12%

18%

14%

14%

11%

21%

Samsung

21%

21%

21%

18%

20%

20%

22%

16%

Xiaomi

8%

9%

8%

8%

10%

10%

13%

11%

OPPO

8%

9%

9%

8%

8%

9%

8%

9%

vivo

7%

8%

8%

8%

7%

8%

8%

8%

Huawei#

17%

16%

18%

14%

17%

20%

14%

8%

realme

1%

1%

3%

2%

2%

2%

4%

4%

Others

24%

24%

21%

23%

22%

16%

20%

23%

Global Smartphone Shipments

Brands

Q1 2019

Q2 2019

Q3 2019

Q4 2019

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Apple

42.0

36.5

44.8

72.3

40.0

37.5

41.7

81.9

Samsung

72.0

76.3

78.2

70.4

58.6

54.2

80.4

62.5

Xiaomi

27.8

32.3

31.7

32.9

29.7

26.5

46.2

43.0

OPPO

25.7

30.6

32.3

31.4

22.3

24.5

31.0

34.0

vivo

23.9

27.0

31.3

31.5

21.6

22.5

31.0

33.4

Huawei#

59.1

56.6

66.8

56.2

49.0

54.8

50.9

33.0

realme

2.8

5.0

10.2

7.8

7.2

6.4

14.8

14.0

Others

87.7

92.8

84.7

98.6

66.6

49.7

69.6

92.8

*Ranking is according to the latest quarter. #Huawei includes HONOR.

Q3 2020 Highlights

Samsung regained the top spot, shipping 80.4 million units with 48% QoQ and 3% YoY growth with the highest ever shipment in the last three years.

Realme shipment grew 132% QoQ, becoming the world’s fastest brand to hit 50 million shipments since inception.

Xiaomi grew 75% QoQ contributing 13% in total smartphone shipment. Notably, this was also the first time when Xiaomi surpassed Apple to capture the third spot.

The market share for BBK Group (OPPO, Vivo, Realme, and OnePlus) has increased from 20% in Q2 to 22% in Q3 2020. The group is close to becoming the largest smartphone manufacturer group globally with three of its brands in the top 10.

Global Smartphone Shipments Market Share (%)

Brands

Q4 2018

Q1 2019

Q2 2019

Q3 2019

Q4 2019

Q1 2020

Q2 2020

Q3 2020

Samsung

18%

21%

21%

21%

18%

20%

20%

22%

Huawei#

15%

17%

16%

18%

14%

17%

20%

14%

Xiaomi

6%

8%

9%

8%

8%

10%

10%

13%

Apple

17%

12%

10%

12%

18%

14%

14%

11%

OPPO

8%

8%

9%

9%

8%

8%

9%

8%

vivo

7%

7%

8%

8%

8%

7%

8%

8%

realme

–

1%

1%

3%

2%

2%

2%

4%

Others

26%

24%

24%

21%

23%

22%

16%

20%

Global Smartphone Shipments

Brands

Q4 2018

Q1 2019

Q2 2019

Q3 2019

Q4 2019

Q1 2020

Q2 2020

Q3 2020

Samsung

69.8

72.0

76.3

78.2

70.4

58.6

54.2

80.4

Huawei#

59.7

59.1

56.6

66.8

56.2

49.0

54.8

50.9

Xiaomi

25.6

27.8

32.3

31.7

32.9

29.7

26.5

46.2

Apple

65.9

42.0

36.5

44.8

72.3

40.0

37.5

41.7

OPPO

31.3

25.7

30.6

32.3

31.4

22.3

24.5

31.0

vivo

26.5

23.9

27.0

31.3

31.5

21.6

22.5

31.0

realme

–

2.8

5.0

10.2

7.8

7.2

6.4

14.8

Others

115.8

87.7

92.8

84.7

98.6

66.6

48.6

69.6

*Ranking is according to the latest quarter.

#Huawei includes HONOR.

Q2 2020 Highlights

The share of the top 10 brands reached 88% compared to 80% last year. Brands outside of the top 10 declined 55% YoY. The impact of COVID-19 was more severe on smaller brands that tend to have lower online presence and that tend to cater more to the entry-level segments.

Huawei continued its push in China and surpassed Samsung to lead the global smartphone market. Huawei’s shipments declined only 3% YoY globally as it grew 11% YoY in China.

Samsungdeclined 29% YoY as its core markets including LATAM, India, the USA and Europe were struggling from the effects of the pandemic and lockdowns.

realmewas the only major brand achieving double-digit annual growth. realme grew 11% YoY in the quarter as several markets in Europe and India recovered in June. realme was also the fastest-growing brand in the quarter and was number 7th in terms of sales.

Apple iPhone shipments grew 3% YoY and revenues grew 2% YoY. The company saw sustained momentum of the iPhone 11 and a great sales start of the iPhone SE. All regions saw revenue growth.

Global Smartphone Shipments Market Share (%)

Brands

Q3 2018

Q4 2018

Q1 2019

Q2 2019

Q3 2019

Q4 2019

Q1 2020

Q2 2020

Huawei#

14%

15%

17%

16%

18%

14%

17%

20%

Samsung

19%

18%

21%

21%

21%

18%

20%

20%

Apple

12%

17%

12%

10%

12%

18%

14%

14%

Xiaomi

9%

6%

8%

9%

8%

8%

10%

10%

OPPO

9%

8%

8%

9%

9%

8%

8%

9%

vivo

8%

7%

7%

8%

8%

8%

7%

8%

Lenovo##

3%

3%

3%

3%

3%

3%

2%

3%

Others

26%

26%

24%

24%

21%

23%

22%

16%

Global Smartphone Shipments

Brands

Q3 2018

Q4 2018

Q1 2019

Q2 2019

Q3 2019

Q4 2019

Q1 2020

Q2 2020

Huawei#

52.0

59.7

59.1

56.6

66.8

56.2

49.0

54.8

Samsung

72.3

69.8

72.0

76.3

78.2

70.4

58.6

54.2

Apple

46.9

65.9

42.0

36.5

44.8

72.3

40.0

37.5

Xiaomi

33.3

25.6

27.8

32.3

31.7

32.9

29.7

26.5

OPPO

33.9

31.3

25.7

30.6

32.3

31.4

22.3

24.5

vivo

30.5

26.5

23.9

27.0

31.3

31.5

21.6

22.5

Lenovo##

11.0

10.1

9.5

9.5

10.0

11.7

5.9

7.5

Others

110.9

115.8

87.7

92.8

84.7

98.6

66.6

48.6

*Ranking is according to the latest quarter. #Huawei includes HONOR. ##Lenovo includes Motorola.

Q1 2020 Highlights

The global smartphone market declined its fastest ever, down 13% YoY in Q1 2020.

This is the first time since Q1 2014, that the smartphone market has fallen below 300Mn units in a quarter.

The COVID-19 pandemic has disrupted the signs of any recovery that the market started showing in Q4 2019.

Samsungled the smartphone market during the quarter capturing one-fifth of the global smartphone shipments. The OEM declined 18% YoY during the quarter and is expected to see a steeper decline in Q2 2020.

Huawei continued its push in China and surpassed Apple again during the quarter. The OEM declined 17% YoY during the quarter. Over half of the smartphone shipments for Huawei are now in China.

Apple remained resilient even during the COVID-19 as iPhone shipments declined only 5% YoY during the quarter. The iPhone revenues were down 7% YoY for the same period. The impact on some European and Asian countries was mild.

Xiaomi grew 7% YoY during the quarter. The OEM continued to lead theIndiasmartphone market reaching its highest ever market share (30%) since Q1 2018.

Compared to other major OEMs, Vivo declined less (10% YoY) during the quarter. A strong performance in the Indian Smartphone Market partially offset declines in other markets.

Global smartphone shipments reached 401 million units in Q4 2019 showing a 2% YoY growth as compared to Q4 2018.

The top three brands,Samsung, Huawei and Apple, captured more than 50% of the smartphone market, with the rest of the market left for hundreds of other brands to compete fiercely.

Samsung remained flat during 2019 Q4 while grew 2% YoY for CY 2019.Samsung has been oneof the leading players in 5G in 2019, shipping over 6.5 Million 5G capable devices in 2019.

苹果iPhone在第四季度出货量同比增长10%2019 even without a 5G variant.The iPhone 11 seriesreceived an excellent consumer response in all regions. The dual-camera and lower pricing of iPhone 11 helped propel sales.

realme continued its growth streak and remained the fastest growing brand during the quarter (163% YoY) as well as the year (453% YoY). The brand entered the top five in the Indian market for the full year, which contributed to its strong growth.

The top three brands, Samsung, Huawei and Apple, together cornered almost half of the smartphone market, with the rest of the market left for hundreds of other brands to compete fiercely.

Samsungcontinued its growth at 8.4%YoY, capturing over one-fifth of the global smartphone market. This is due to strong Note 10 and Galaxy A series sales.

Huawei一个非常健康的全球同比28.5%增长。它捕获d a record 40% market share in the Chinese smartphone market.

Apple iPhone shipments were down 4%,and as a result revenues fell 11% YoY.

BBK Group (OPPO, Vivo, Realme, and OnePlus) is close to becoming the largest smartphone manufacturer groupglobally, accounting for over 20% of the global smartphone market and three of its brands in the top 10.

For Q4 2018,Huawei, OPPO and vivocontinue to dominate with strong performances in China, India, Asia and parts of Europe. The trio have multiple regions to enter and grow moving forward into 2019.

SamsungandApplesaw a tough quarter and tough 2018 as demand for their flagship phones have waned due to competition from affordable premium and more cutting-edge phones from Chinese brands such as Huawei and OnePlus.

Xiaomireached a record fourth position for the full year after two years of setbacks thanks to immense growth in India. It has surpassed OPPO globally to take back the fourth position.

Smartphone shipments declined 2% annually to 360 million units in Q2 2018.

The top 10 brands accounted for 79% of the smartphone volumes in Q2 2018.

Samsung led the smartphone market by volume with a market share of 20% in Q2 2018 even though it registered an annual decline of 11% due to weak sales of its flagship Galaxy S9 series smartphones.

Huawei shipments grew 41% annually in Q2 2018. The company managed to be the fastest growing (21%) smartphone brand amid a declining China smartphone market and grew fully 71% overseas.

Apple shipped 41.3 million iPhones during Q2 2018, up 1% compared to the same quarter last year. iPhone X remains the top seller for Apple during the quarter.

Smartphone shipments declined 3% annually reaching 360 million units in Q1 2018.

The China market decline in Q1 2018, affected the overall growth of some of the key Chinese brands including OPPO and vivo. Both saw a decline in the quarter as a result of the China market slowdown.

智能手机普及率的所有手机域名下降到76%le phones shipped in the quarter. This was partly due to an increase in feature phone shipments by some key brands such as Nokia HMD and Reliance Jio who both saw YoY growth.

Top 10 brands accounted for 76% of the smartphone volumes in Q1 2018.

A repository of quarterly data for the China smartphone market. This data is a part of a series of reports which track the mobile handset market:Smartphone and Feature Phone shipmentsevery quarter for more than 140 brands covering more than 95% of the totaldevice shipmentsin the industry.

Smartphone shipments in China fell 4% YoY in Q2 2023 though OEMs provided big promotions during the 618 festival. This was due to weak demands resulting from economic headwinds.

Apple saw the biggest YoY growth in Q2 as the OEM offered generous price-cuts for the iPhone 14 series during the 618 period. Besides, it still has no competitors in the high-end market which has proven to be more resilient during market headwinds.

OPPO’s share grew slightly (YoY) as OnePlus showed strong growth piggybacking of the channel support from OPPO. OnePlus compensated for OPPO’s limited online presence by using its online-centric business model to effectively tap into the segment.

HONOR’s share dropped significantly (YoY) partially because Huawei’s growth posted a challenge for HONOR.

We anticipate an improvement in smartphone shipments during H2 compared to H1, a strong rebound does not seem to be on the horizon as challenges that affected the performance in H1 are likely to persist.

Note: HONOR separated from Huawei in Q4 2020 and its market share does not include Huawei brand family volumes starting Q1 2021. * OPPO includes OnePlus since Q3 2021.

For our detailed research on the China smartphone sales market share Q2 2023, clickhere.

The smartphone market share numbers are from:

MOBILE DEVICES MONITOR – Q2 2023 (Vendor Region Countries)

这个报告是一系列的报告的一部分track the mobile handset market: Smartphone and Feature Phone shipments every quarter for more than 140 brands covering more than 95% of the total device shipments in the industry.

The deliverable includes

• Single pivot format giving in-depth analysis of theglobal handset market • Covers140 +品牌now in comparison to 95 brands earlier • Break out of3 key countriesin each regionto give a further granular view of the regions •18 countries viewas compared to six earlier • Covers more than95% of the global handset shipments • More visuals and analysis by country and by regions

This robust quarterly report with fact-based deep analysis covering multiple dimensions will help players across the handset value chain to holistically analyze the current state of the global handset market and plan ahead of the competition.

This data represents the Chinese smartphone market share by quarter (from 2020-2023) by top OEMs.

For detailed insights on the data, please reach out to us at联系(在)www.arena-ruc.com. If you are a member of the press, please contact us atpress(at)www.arena-ruc.comfor any media enquiries.

Q1 2023 Highlights

Published Date: May 16, 2023

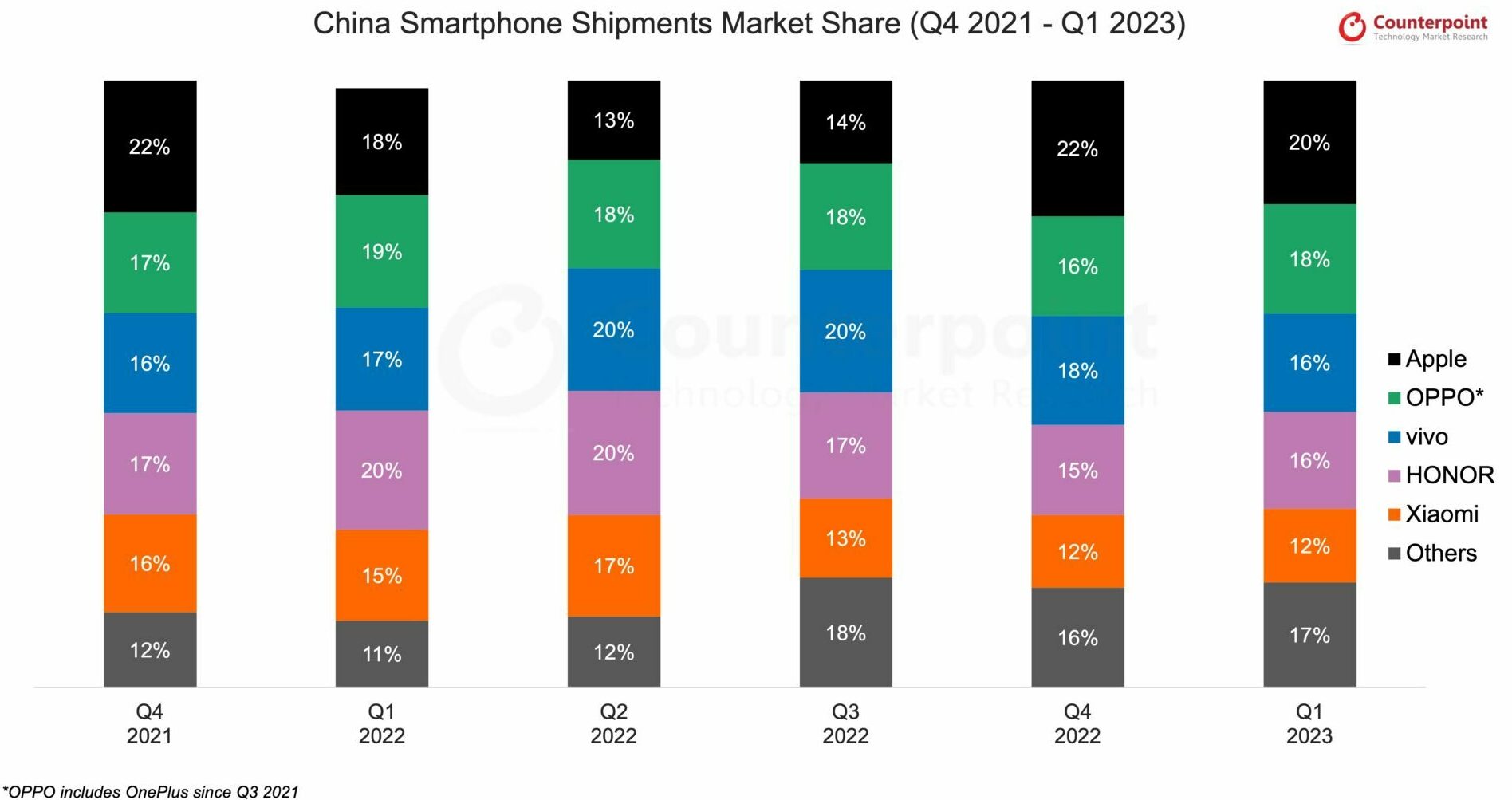

China’s smartphone shipments declined 8% YoY in Q1 2023, reaching their lowest level since Q1 2020. However, this was an improvement from the double-digit YoY declines seen in previous quarters as well as a sign of bottoming out.

Apple’s market share in China increased to 20% in Q1 2023 from 18% in Q1 2022. This was driven by its continued expansion in China’s premium segment with more aggressive promotion and marketing campaigns for the iPhone 14 series.

In contrast, all the major Android OEMs saw YoY declines as demand in the mass market remained weak. OEMs remained cautious in ramping up production to manage demand carefully and avoid any unhealthy inventory build-up in the market.

Despite this caution, we expect the market to further recover in H2 2023, as inventory pressure continues to ease and consumer sentiments improve.

For our detailed research on the China smartphone sales market share Q1 2023, clickhere.

China Smartphone Market Share (Shipments %)

Brands

Q4 2021

Q1 2022

Q2 2022

Q3 2022

Q4 2022

Q1 2023

Apple

22%

18%

13%

14%

22%

20%

OPPO*

17%

19%

18%

18%

16%

18%

vivo

16%

17%

20%

20%

18%

16%

HONOR

17%

20%

20%

17%

15%

16%

Xiaomi

16%

15%

17%

13%

12%

12%

Others

12%

11%

12%

18%

16%

17%

*Ranking is according to latest quarter.

Note: HONOR separated from Huawei in 2020 Q4 and its market share does not include Huawei brand family volumes starting Q1 2021. OPPO includes OnePlus since Q3 2021.

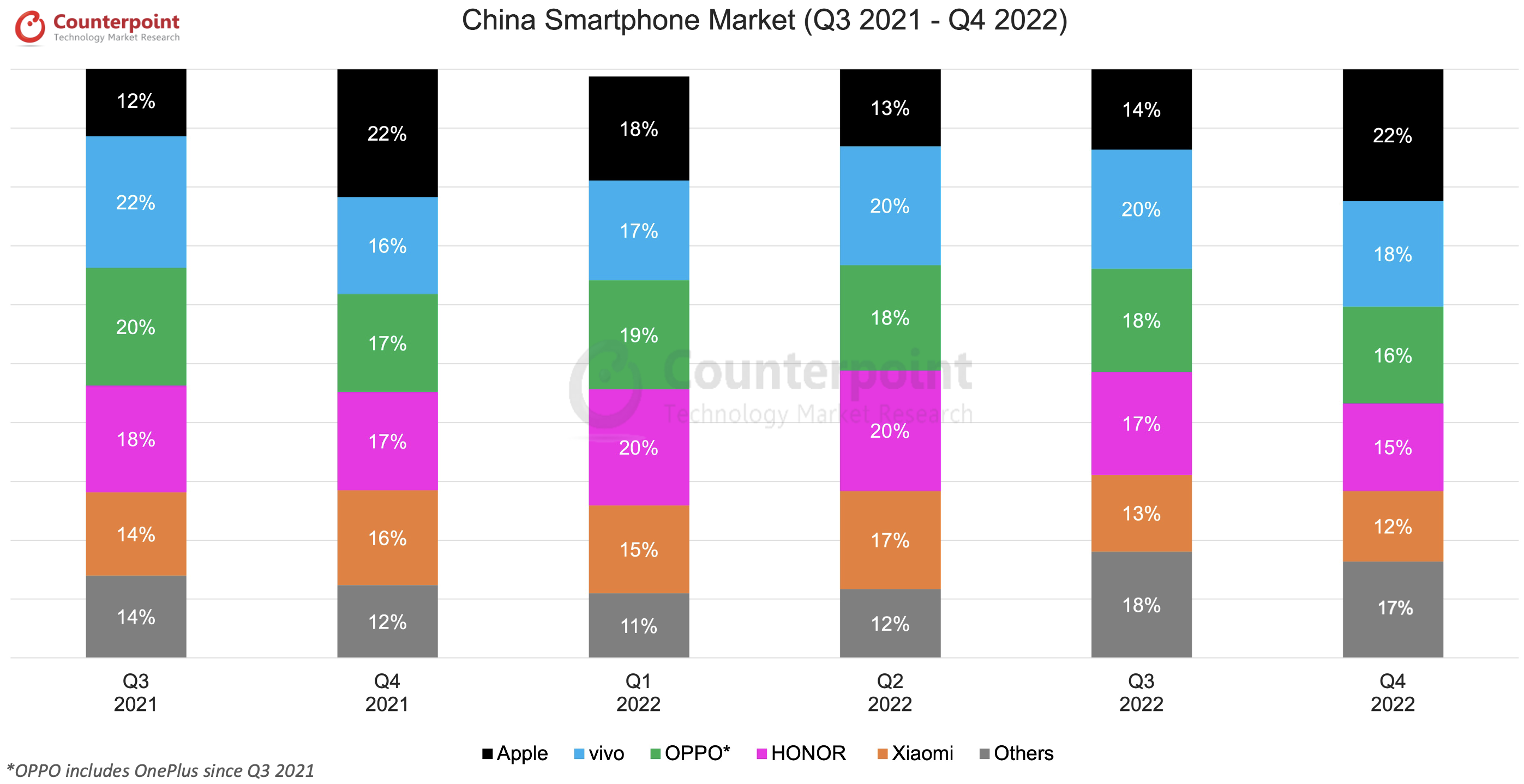

Q4 2022 Highlights

Published Date: February 18, 2023

Apple registered a QoQ growth of 67% due to the high demand for new iPhone 14 series. Apple market share in China has now reached 22% in Q4 2022.

vivodropped to the 2nd position as the OEM’s market share fell to 18%.

Major Chinese phone market share (Chinese OEMs) saw YoY shipment declines due to overall market instability due frequent COVID lockdowns and weak economic conditions.

Xiaomi retained its position in the top five even as its market share fell to its lowest in over two years. Xiaomi market share in China reached 12% in Q4 2022.

Huawei saw a growth of 25% in it’s shipment that helped it capture 8.7% of Chinese market.

For our detailed research on the China smartphone sales market share Q4 2022, clickhere.

China Smartphone Market Share (Shipments %)

Brands

Q3 2021

Q4 2021

Q1 2022

Q2 2022

Q3 2022

Q4 2022

Apple

12%

22%

18%

13%

14%

22%

vivo

22%

16%

17%

20%

20%

18%

OPPO*

20%

17%

19%

18%

18%

16%

HONOR

18%

17%

20%

20%

17%

15%

Xiaomi

14%

16%

15%

17%

13%

12%

Others

14%

12%

11%

12%

18%

17%

*Ranking is according to latest quarter.

Note: HONOR separated from Huawei in 2020 Q4 and its market share does not include Huawei brand family volumes starting Q1 2021. OPPO includes OnePlus since Q3 2021.

Q3 2022 Highlights

Published Date: December 20, 2022

Apple was the only major OEM in China to see a YoY increase mainly driven by strong demand for the iPhone 14 Pro models.

Other major Chinese OEMs saw YoY sales declines due to overall market plunge resulting from frequent COVID lockdowns and weak economic environment.

Despite sales declines compared to last year, vivo, OPPO and HONOR remained the top 3 brands in China, while Xiaomi dropped one rank to reach 5thplace.

Although facing sanctions, Huawei also saw a YoY increase due to strong demand for its mid-end Nova 10 and premium foldable smartphones.

For our detailed research on the China smartphone sales market share Q3 2022, clickhere.

中国智能手机的红灯区ts Market Share (%)

Brands

Q2 2021

Q3 2021

Q4 2021

Q1 2022

Q2 2022

Q3 2022

vivo

24%

22%

16%

17%

20%

20%

OPPO*

21%

20%

17%

19%

18%

18%

HONOR

9%

18%

17%

20%

20%

17%

Apple

12%

12%

22%

18%

13%

14%

Xiaomi

17%

14%

16%

15%

17%

13%

Others

17%

14%

12%

11%

12%

18%

*Ranking is according to latest quarter.

Note: HONOR separated from Huawei in 2020 Q4 and its market share does not include Huawei brand family volumes starting Q1 2021. OPPO includes OnePlus since Q3 2021.

Q2 2022 Highlights

Published Date: August 15, 2022

Huge smartphone market share gains were made by HONOR in Q2 2022 as the OEM capitalized onstrength in the premium market

iPhone market share continued to eke upwards, with Apple doing extremely well in the ultra-premium segment

Clickhereto read about the China smartphone sales market in Q2 2022.

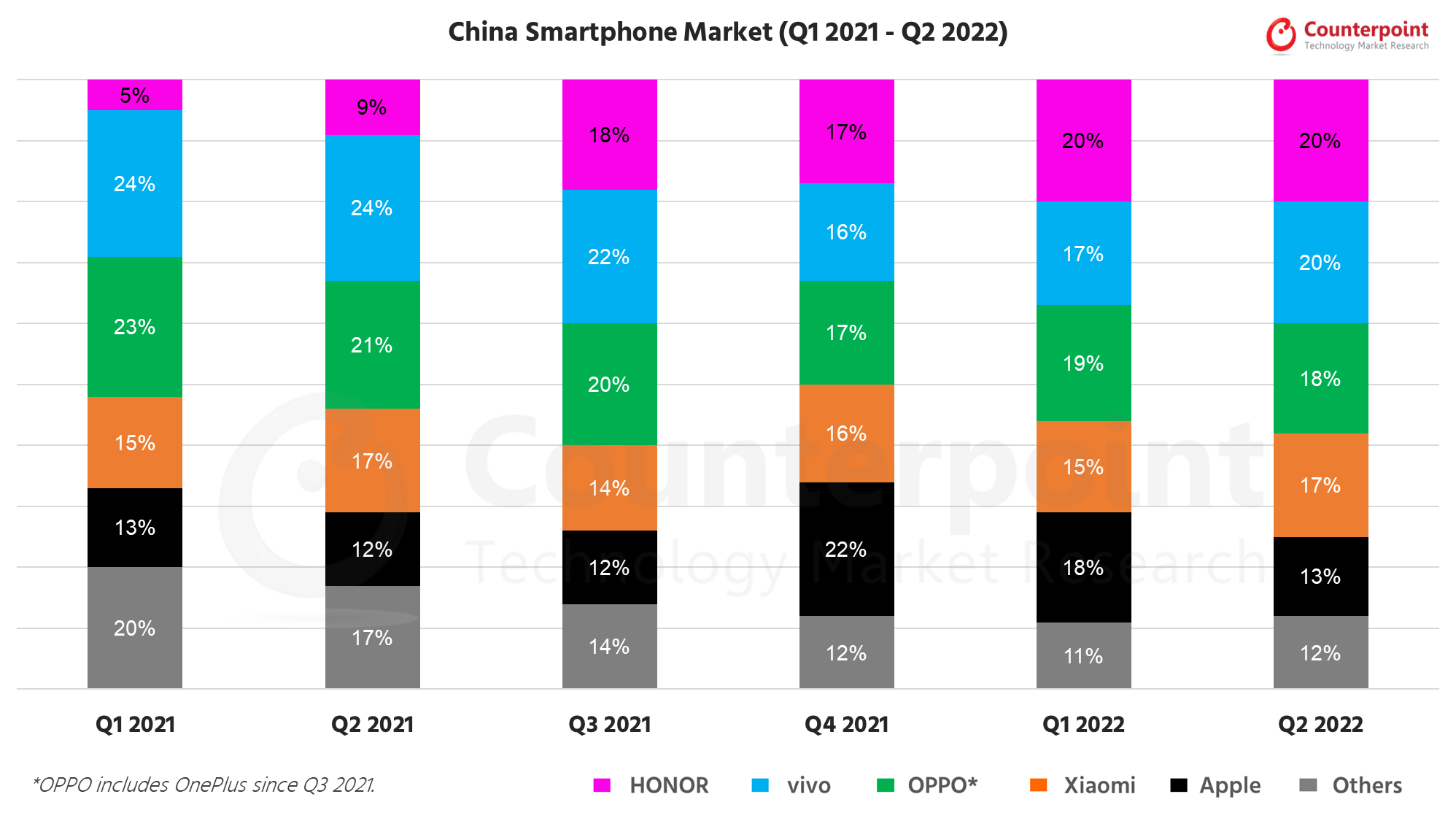

中国智能手机的红灯区ts Market Share (%)

Brands

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Q1 2022

Q2 2022

HONOR

5%

9%

18%

17%

20%

20%

vivo

24%

24%

22%

16%

17%

20%

OPPO*

23%

21%

20%

17%

19%

18%

Xiaomi

15%

17%

14%

16%

15%

17%

Apple

13%

12%

12%

22%

18%

13%

Others

20%

17%

14%

12%

11%

12%

*Ranking is according to latest quarter.

Note: HONOR separated from Huawei in 2020 Q4 and its market share does not include Huawei brand family volumes starting Q1 2021. OPPO includes OnePlus since Q3 2021.

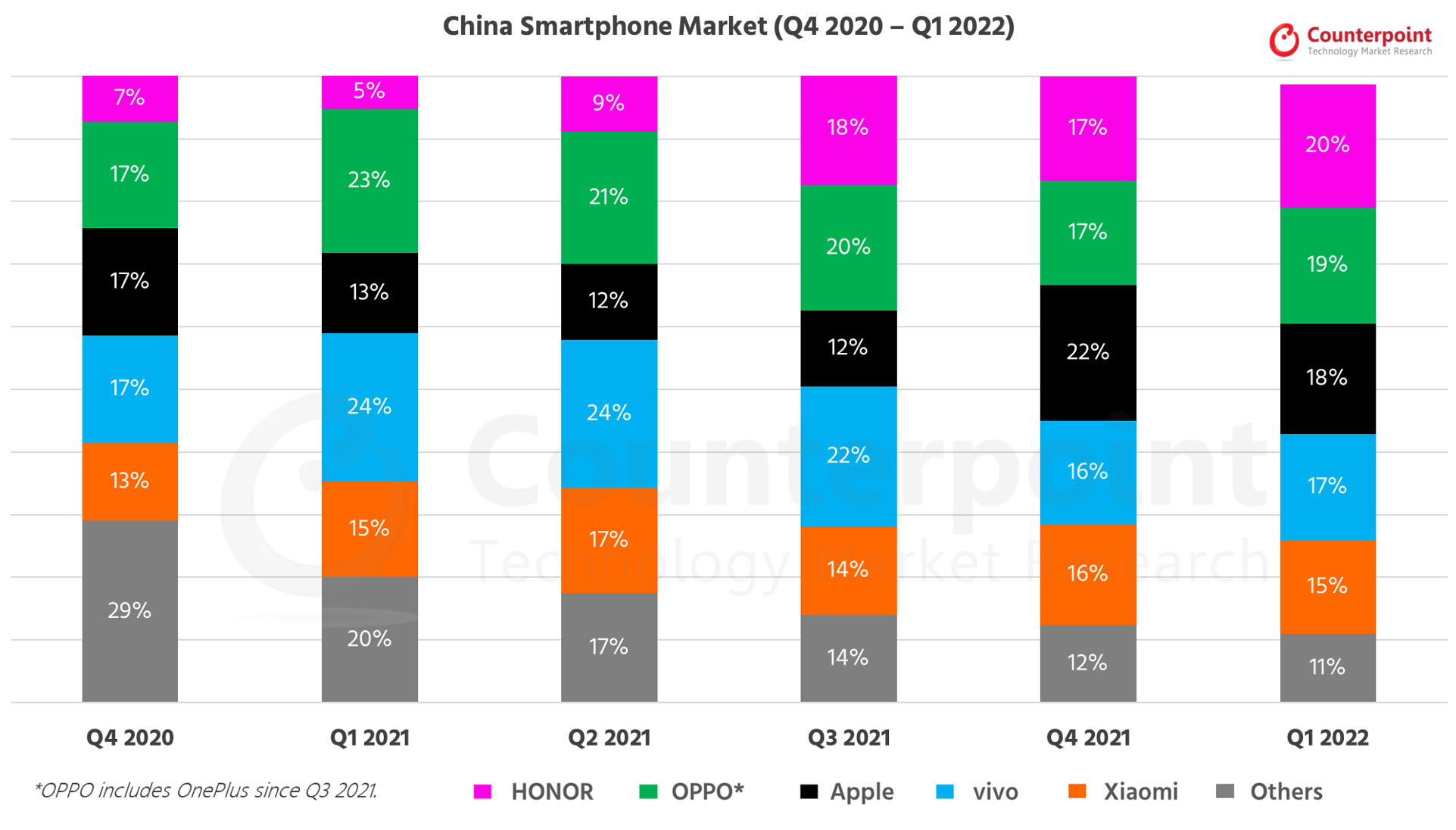

Q1 2022 Highlights

Published Date: May 15, 2022

In 2022 Q1, China smartphone shipments declined 19% YoY and 12% QoQ to reach 73.7 million units.

HONOR continued to outperform the market with shipment growing 190% YoY and 4% QoQ in Q1 2022. HONOR led the market during this quarter and captured 20% market share.

OPPO (including Oneplus) held the second spot with 13.7 million units in Q1 2022.

Apple slipped to the third spot with 13 million units in Q1 2022. Although Apple’s shipment fell compared to Q4 2021, Apple still registered 11% YoY growth driven by strong demand for iPhone 13 series.

Dropping to the fourth spot, vivo declined 42%YoY and 9% QoQ to 12.5 million units in Q1 2022. Q1 2022 was its worst performing quarter since the severe pandemic-hit Q1 2020.

Clickhereto read about the China smartphone market in Q1 2022.

中国智能手机的红灯区ts Market Share (%)

Brand

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Q1 2022

HONOR

7%

5%

9%

18%

17%

20%

OPPO*

17%

23%

21%

20%

17%

19%

Apple

17%

13%

12%

12%

22%

18%

vivo

17%

24%

24%

22%

16%

17%

Xiaomi

13%

15%

17%

14%

16%

15%

Others

29%

20%

17%

14%

12%

11%

*Ranking is according to latest quarter.

Note: HONOR separated from Huawei in 2020 Q4 and its market share does not include Huawei brand family volumes starting Q1 2021. OPPO includes OnePlus since Q3 2021.

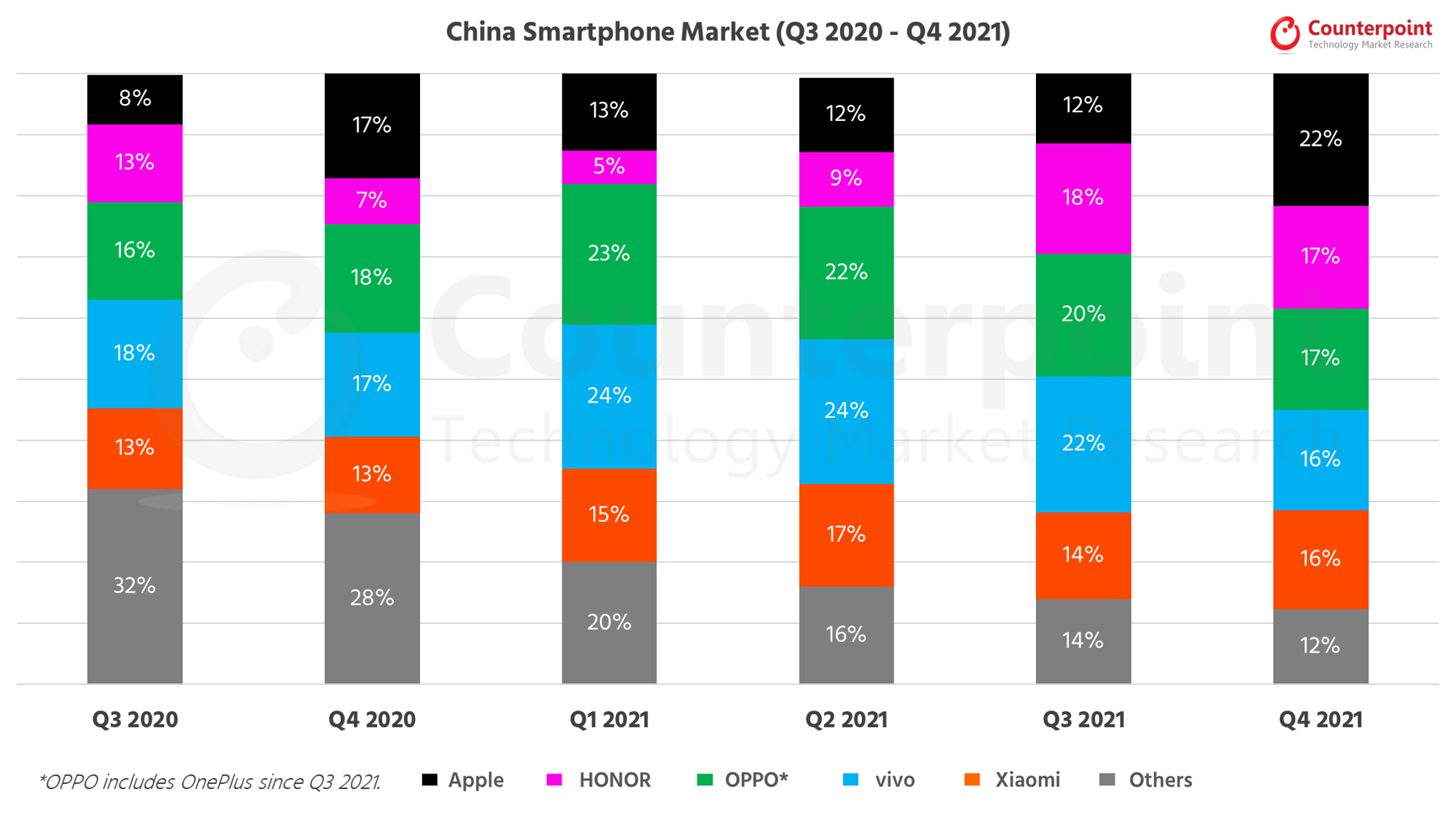

Q4 2021 Highlights

Published Date: February 15, 2022

China smartphone shipments declined 11% YoY to reach 84 million units. However, the market increased 9% QoQ in Q4 2021.

Apple’s 13% YoY and 95% QoQ growth helped it lead the China market, capturing 22% market share in Q4 2021.

For the first time, HONOR reached the second spot after becoming an independent brand. It grew 100% YoY to reach 14 million units.

vivoslipped to the fourth spot with ~14 million units in Q4 2021, However, it led the overall China smartphone market in CY 2021.

Clickhereto read about the China smartphone market in Q4 2021.

China Smartphone Market Share (%)

Brands

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Q3 2021

Q4 2021

Apple

8%

17%

13%

12%

12%

22%

HONOR

13%

7%

5%

9%

18%

17%

OPPO*

16%

18%

23%

22%

20%

17%

vivo

18%

17%

24%

24%

22%

16%

Xiaomi

13%

13%

15%

17%

14%

16%

Others

32%

28%

20%

16%

14%

12%

*Ranking is according to latest quarter.

Note: HONOR separated from Huawei in 2020 Q4 and its market share does not include Huawei brand family volumes starting Q1 2021. OPPO includes OnePlus since Q3 2021.

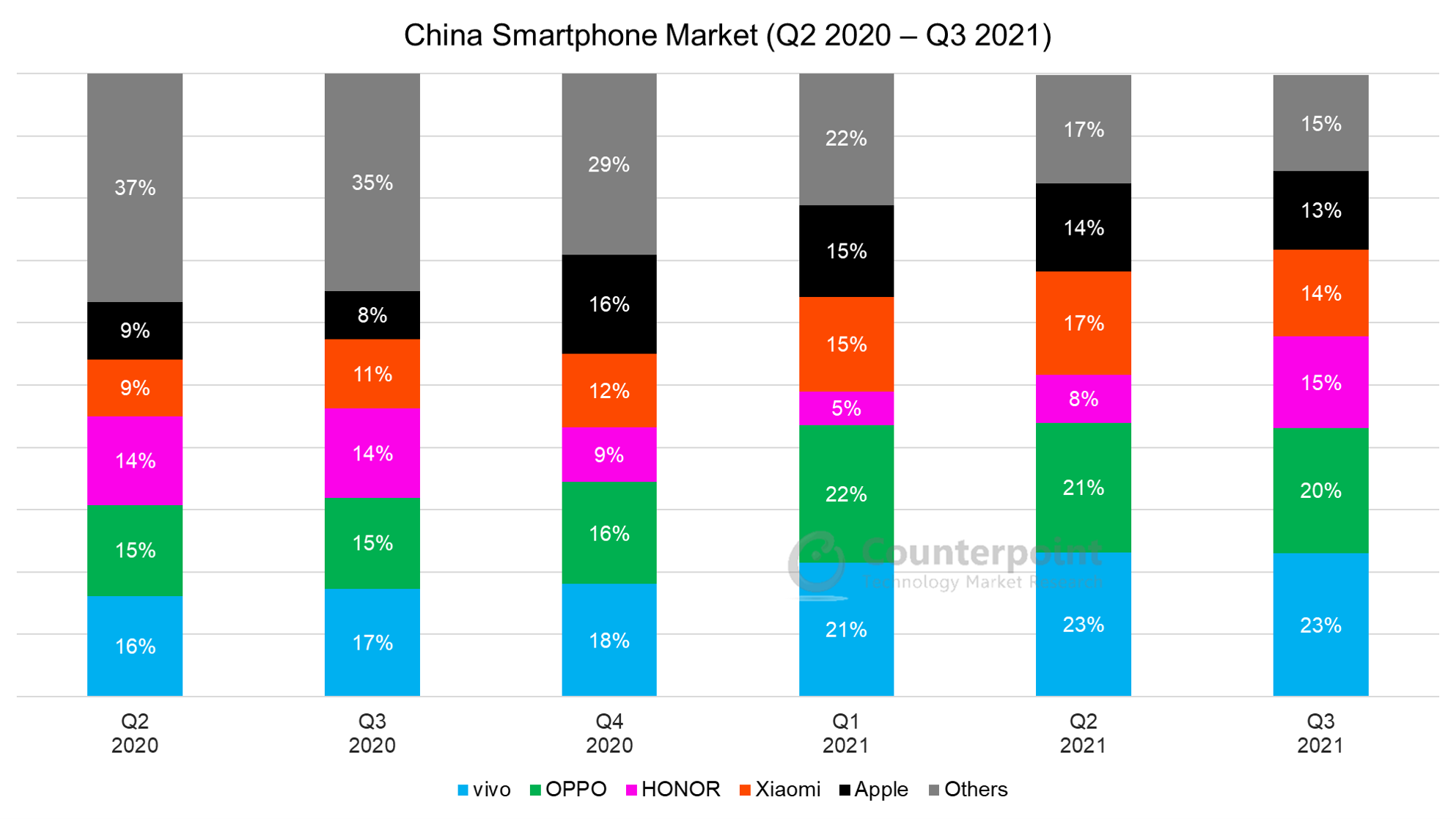

Q3 2021 Highlights

Published Date: November 15, 2021

Smartphone sales in China increased 3% QoQ but declined 9% YoY in Q3 2021.

vivoled the market in Q3 2021, capturing a 23% share, followed by OPPO (20%) and HONOR (15%).

HONOR was the fastest-growing OEM (96% QoQ) in China during the quarter.

China’s 5G smartphone sales accounted for 79% of total smartphone sales in Q3 2021.

中国智能手机的红灯区ts Market Share (%)

Brands

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Q2 2021

Q3 2021

vivo

16%

17%

18%

21%

23%

23%

OPPO

15%

15%

16%

22%

21%

20%

HONOR

14%

14%

9%

5%

8%

15%

Xiaomi

9%

11%

12%

15%

17%

14%

Apple

9%

8%

16%

15%

14%

13%

Others

37%

35%

29%

22%

17%

15%

*Ranking is according to latest quarter.

Note:HONOR separated from Huawei in 2020 Q4 and its market share does not include Huawei brand family volumes starting Q1 2021.

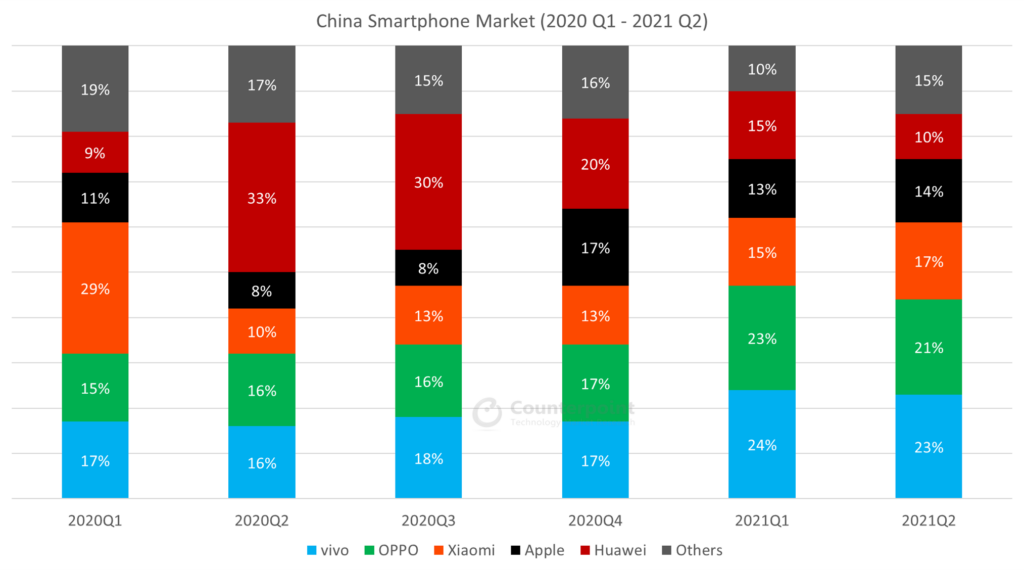

Q2 2021 Highlights

Published Date: August 15, 2021

Smartphone sales in China declined 13% QoQ and 6% YoY in Q2 2021.

vivoled the market in Q2 2021, capturing a 23% share, followed by OPPO (21%) and Xiaomi (17%).

Xiaomi was the fastest-growing OEM (70% YoY) in China, followed by Apple (43%) and OPPO (37%).

中国智能手机的红灯区ts Market Share (%)

Brands

Q1 2020

Q2 2020

Q3 2020

Q4 2020

Q1 2021

Q2 2021

vivo

17%

16%

18%

17%

24%

23%

OPPO

15%

16%

16%

17%

23%

21%

Xiaomi

29%

10%

13%

13%

15%

17%

Apple

11%

8%

8%

17%

13%

14%

Huawei

9%

33%

30%

20%

15%

10%

Others

19%

17%

15%

16%

10%

15%

*Ranking is according to latest quarter. #Huawei includes HONOR

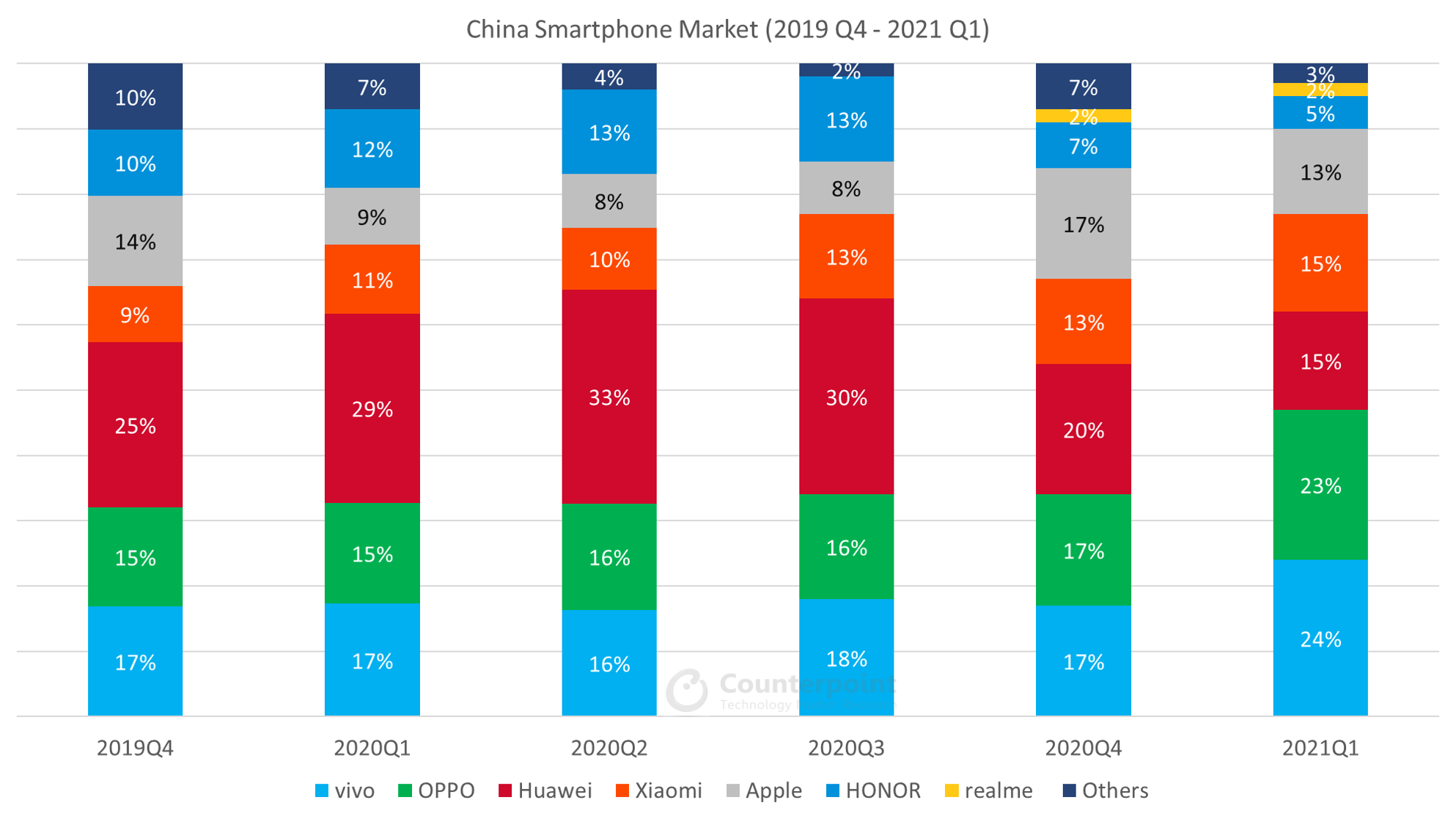

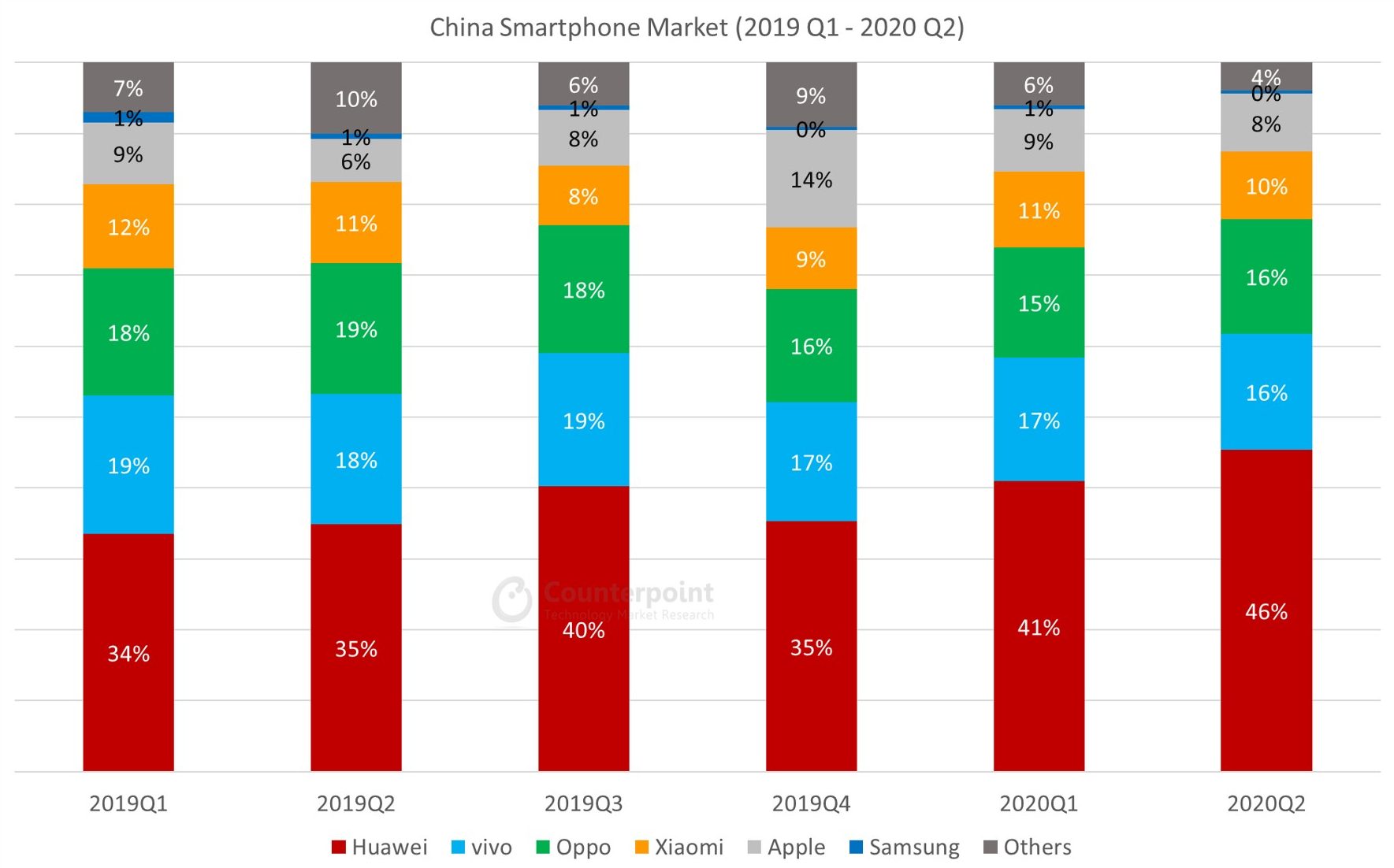

Q1 2021 Highlights

Published Date: May 15, 2021

Smartphone shipment growth in China turned positive in Q1 2021.

Smartphone shipments grew 36% compared to last year’s COVID-impacted first quarter to register 90.7mn shipments.

The quarter marked the inevitable succession of Huawei’s leadership, as the beleaguered handset maker struggled to maintain shipments.

vivoand OPPO emerged as clear leaders, accounting for nearly half of all smartphones shipped during the period.

中国智能手机的红灯区ts Market Share (%)

Brands

2019Q4

2020Q1

2020Q2

2020Q3

2020Q4

2021Q1

vivo

17%

17%

16%

18%

17%

24%

OPPO

15%

15%

16%

16%

17%

23%

Huawei

25%

29%

33%

30%

20%

15%

Xiaomi

9%

11%

10%

13%

13%

15%

Apple

14%

9%

8%

8%

17%

13%

HONOR

10%

12%

13%

13%

7%

5%

realme

0%

0%

0%

0%

2%

2%

Others

10%

7%

4%

2%

7%

3%

*Ranking is according to latest quarter. #Huawei includes HONOR

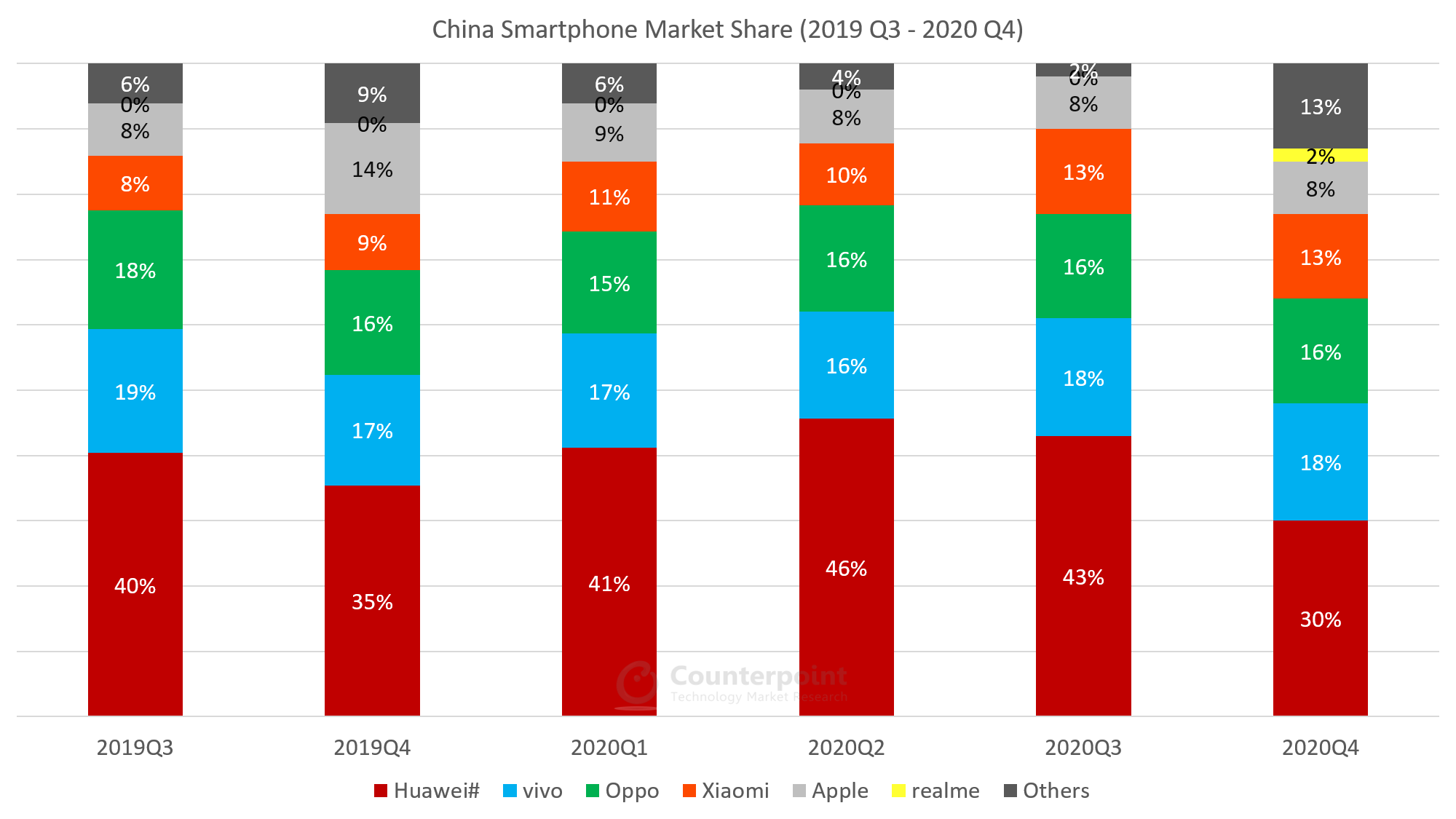

Q4 2020 Highlights

Published Date: February 15, 2021

China’s smartphone market declined 17% YoY in 2020.

China’s 5G smartphone sales accounted for more than 60% of total smartphone sales in Q4 2020.

Huaweiand HONOR combined took the top spot in the market, capturing 41% share in 2020.

Apple was the only brand to witness a positive YoY growth in the market in 2020.

中国智能手机的红灯区ts Market Share (%)

Brands

2019Q3

2019Q4

2020Q1

2020Q2

2020Q3

2020Q4

Huawei#

40%

35%

41%

46%

43%

30%

vivo

19%

17%

17%

16%

18%

18%

Oppo

18%

16%

15%

16%

16%

16%

Xiaomi

8%

9%

11%

10%

13%

13%

Apple

8%

14%

9%

8%

8%

8%

realme

0%

0%

0%

0%

0%

2%

Others

6%

9%

6%

4%

2%

13%

*Ranking is according to latest quarter. #Huawei includes HONOR

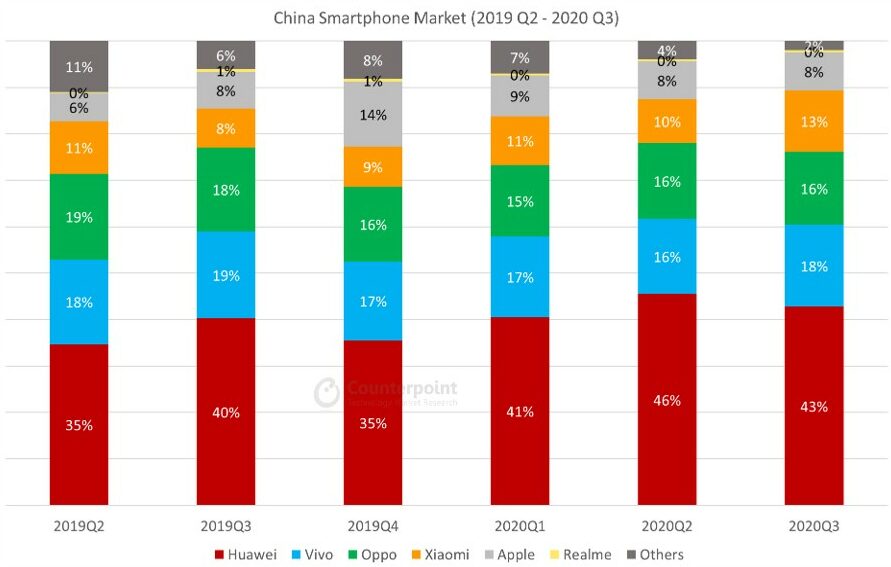

Q3 2020 Highlights

Smartphone sales in China recovered slowly with 6% QoQ growth in Q3. But the growth was still down 14% YoY.

Xiaomi outperformed the market as the only major OEM to achieve a positive YoY growth in Q3 in China.

Huawei continued to lead the market with 45% share in Q3 (in smartphone sales). However, its sales have started to decline.

中国智能手机的红灯区ts Market Share (%)

Brands

2019

Q2

2019

Q3

2019

Q4

2020

Q1

2020

Q2

2020

Q3

Huawei#

35%

40%

35%

41%

46%

43%

Vivo

18%

19%

17%

17%

16%

18%

Oppo

19%

18%

16%

15%

16%

16%

Xiaomi

11%

8%

9%

11%

10%

13%

Apple

6%

8%

14%

9%

8%

8%

Realme

0%

1%

1%

0%

0%

0%

Others

11%

6%

8%

7%

4%

2%