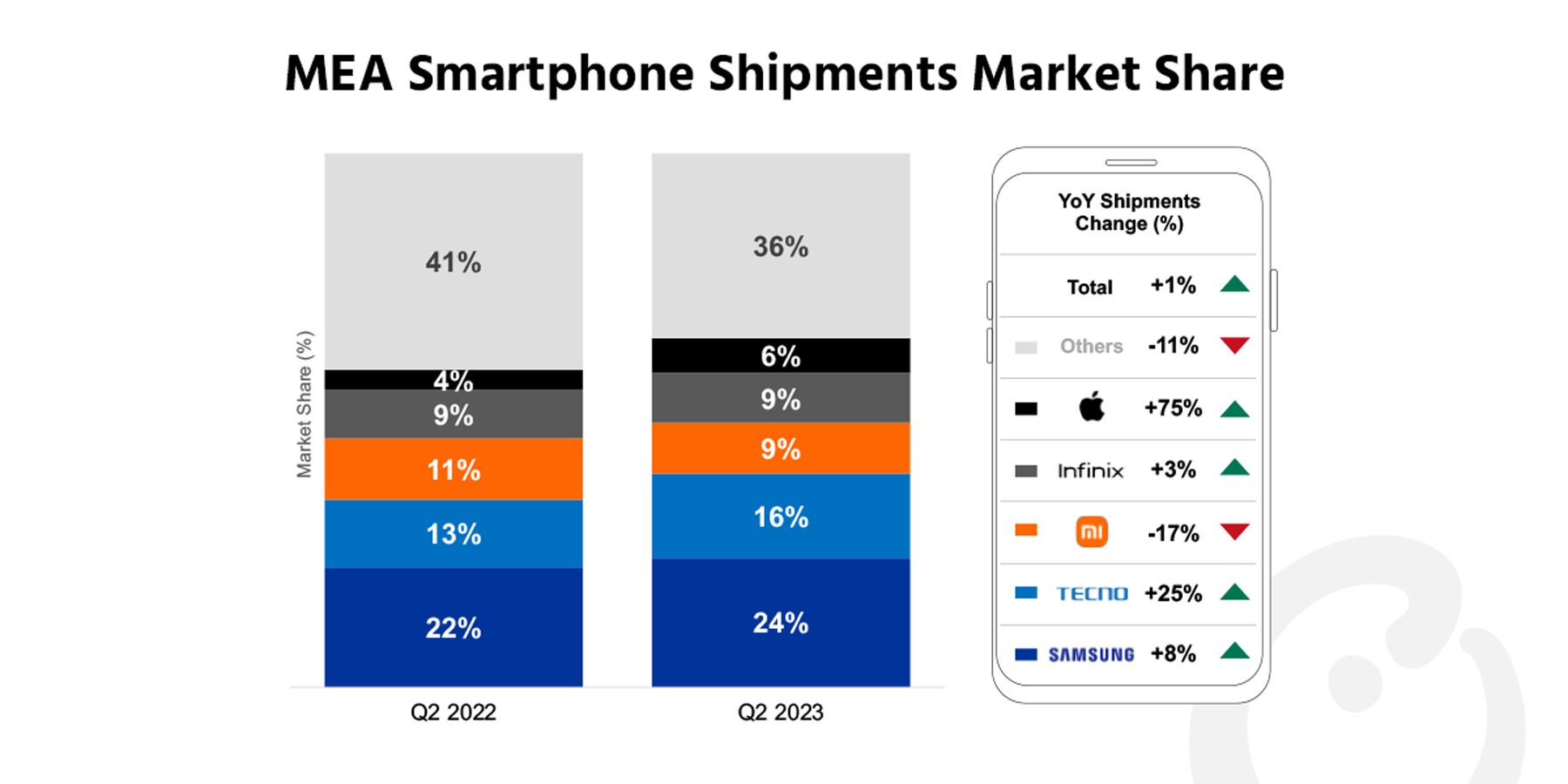

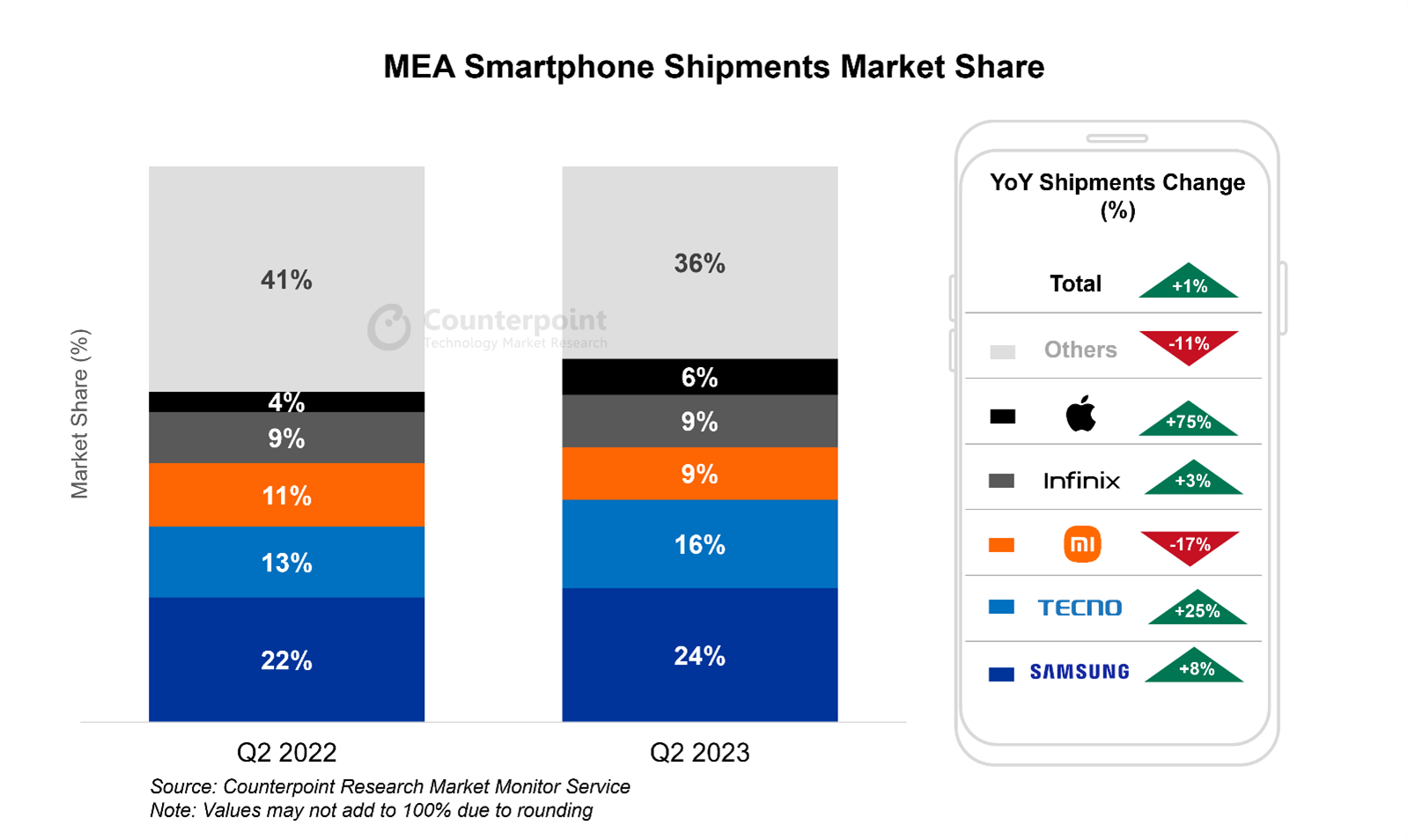

意味着智能手机shipments increased 1% YoY and 7% QoQ in Q2 2023.

Consumer sentiment picked up during the quarter with falling inflation rates and stabilizing local currencies. These boosted demand for ‘big ticket’ items like smartphones.

Samsung saw a rebound in its shipments and market share during the quarter.

Transsion Group’s shipments grew 2% YoY, or an impressive 14% QoQ, in a typically weak quarter.

Apple continued its steep rise, with shipments up 75% YoY in Q2.

London, Boston, Toronto, New Delhi, Hong Kong, Beijing, Taipei, Seoul – September 5, 2023

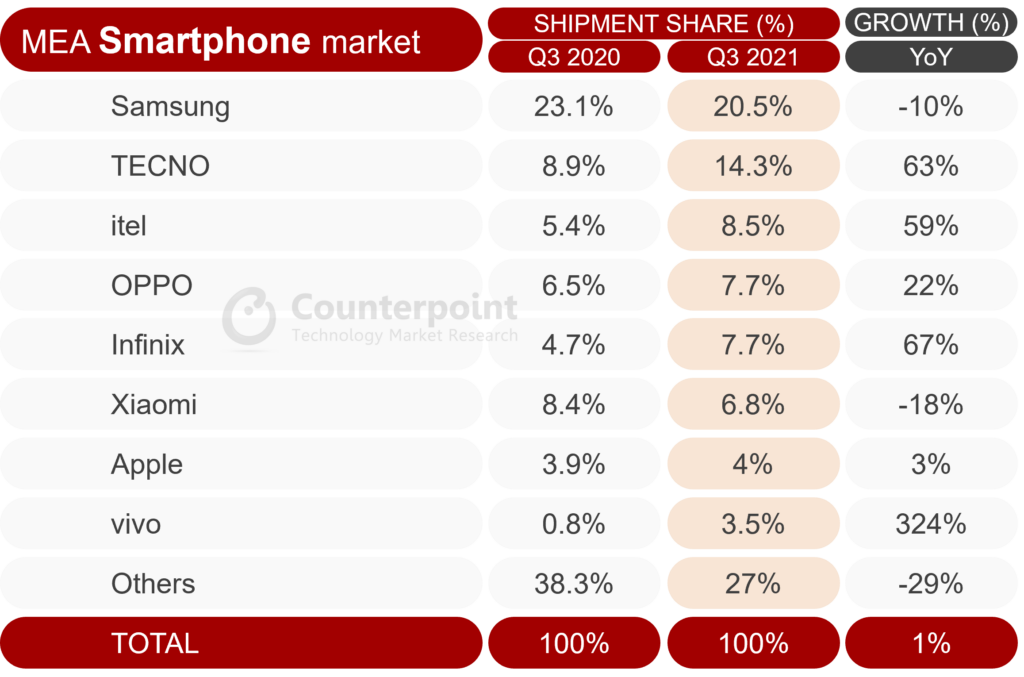

Smartphoneshipments in the Middle East and Africa (MEA) region increased 1% YoY and 7% QoQ in Q2 2023, according to the latest research from Counterpoint’sMarket Monitor Service. This was the MEA smartphone market’s first meaningful rebound in five quarters, or since the global inflation crisis started. Consumer sentiment improved materially during the quarter, as inflation rates fell and local currencies stabilized. This came as a welcome relief for embattled OEMs, which had been sitting on an alarming level of inventory in 2022. They utilized the opportunity to destock and return to a more normal pattern of inventory and product launches.

Commenting on the market’s performance,Senior Analyst Yang Wangsaid, “The意味着region seems to be the first to come out of the global downturn in the智能手机market. Market activity picked up during the quarter on better macroeconomic environment and consumers could afford to be more optimistic about ‘big ticket’ item purchases. This was reflected in robustRamadanand Easter sales and throughout the quarter. The encouraging performances show once again that the MEA region could be the last remaining untapped smartphonemarket.There is still significant potential for large segments of the population to upgrade to smartphones.”

Looking at individual brands, Samsung, TECNO andApplewere the biggest winners.Samsung’s rebound can be attributed to the lower-pricedGalaxyA series’ strong sales, while new 5G and premium-end models also did well.TECNO, and sister brandInfinixto some extent, performed very well due to better economic conditions, particularly for lower income groups, and aggressive market entries in the Middle East. TECNO andInfinix’ssuccesses, however, can be partly attributed to the cannibalization ofitel’s market share. Lastly,Applehad an outstanding quarter to round off a very strong iPhone 14 series cycle. TheOEMmanaged to increase penetration in key Middle East markets with the higher-priced Pro and Pro Max models getting good reception.

On the other hand,Xiaomiretreated 17% YoY as it faced strong competition from Samsung and Transsion brands in the mid-range. Outside of the top 10,OPPOandvivocontinued to slide as the availability of the brands’ stock contracted and market penetration activities shrank. However,realmemaintained positive momentum due to increasing product availability in new markets.

Commenting on pricing trends in the MEA smartphone market, Wang said, “The premium end is usually an afterthought for the MEA market, but the segment was an outperformer of Q2 2023. The sales of smartphones priced above $800 grew 93% YoY, largely due to Apple’s high-end models in the iPhone 14 series. The OEM’s share increased in key GCC markets, while it was seen making efforts to expand distribution channels in Africa. Apple’s success in the MEA region is another proof of the brand’s strong global appeal. As the process of urbanization and industrialization continues across the region, Apple can expect to remain one of the topOEMsin the region.”

Counterpoint Research’s market-leadingMarket Monitor,MarketPulseandModel Salesservices for mobile handsets are available for subscribing clients.

Feel free to contact us at press@www.arena-ruc.com for questions regarding our in-depth research and insights.

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Expansion, Premiumization Drive Transsion’s Record Quarter

September 4, 2023

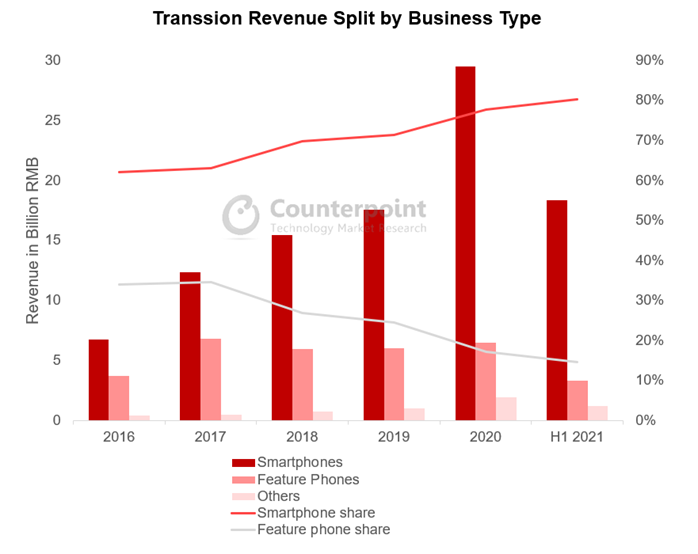

Transsion Holdings reported revenues of RMB 25.03 billion for the first half of 2023, registering a growth of 8.3% YoY. Net profit grew 27.2% YoY primarily due to better product mix (higher proportion of智能手机sas compared to feature phones, with the former accounting for 92% of group revenues) and geographical expansion into higher-value markets.

Q2 2023 was the bright spot as revenues were up 30.7% while net profit grew 83.9%. It was the best quarter in Transsion’s history in both revenue and net profit terms. Gross margins also improved to 24.5%, up 2.4% from a year ago.

Much of Transsion’s turnaround in the key financial metrics above can be attributed to a rebound in macroeconomic fundamentals in theAfricanhome market and beyond. Most importantly, inflation rates have come down while food prices have stabilized. Local currencies have also found a stronger footing while several indebted countries across theemergingmarkets have managed to secure restructuring packages with lenders. As Africa’s most entrenched handset company, thanks to its deep channel penetration and marketing heft, Transsion once again benefitted the most from the upturn.

Transsion’s operating cost in H1 2023 increased 5% YoY as the company is ramping up its operations, particularly in newer markets. It has been aggressive with sales and marketing despite the cyclical downturn, with the spending on these activities increasing 23.6% YoY in H1 2023. R&D spending was also up 20.6% YoY to drive premiumization efforts and develop higher-value products to target the new markets. Costs attributed to management grew 6% YoY, whereas cash flow from operating activities turned positive, primarily due to the reduction in the cost of components and materials, as the company is reducing its inventory and moving towards a leaner operating model.

According to Counterpoint Research, Transsion’s smartphone sales volume grew 3% YoY in the first half of 2023 and 17% YoY in Q2 2023 as demand for TECNO智能手机sincreased globally, especially in the company’s newer markets. This helped Transsion’s cash flow, as cash on hand increased 61% YoY to reach an all-time high of RMB 12.79 billion. The number of inventory days dropped further to 61, from 86 a year ago. Therefore, the inventory problem that has been troubling the company for the past year has successfully been managed.

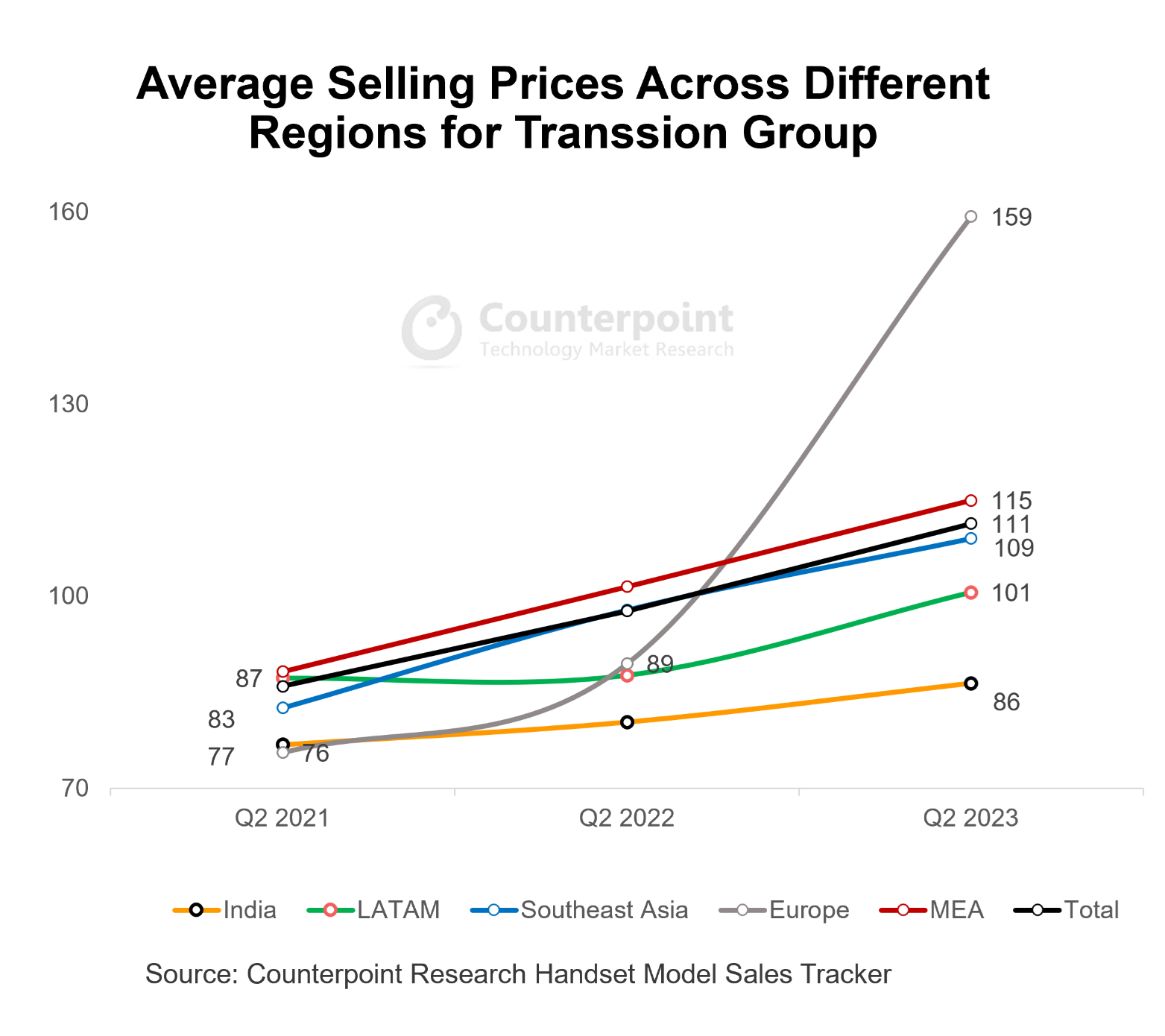

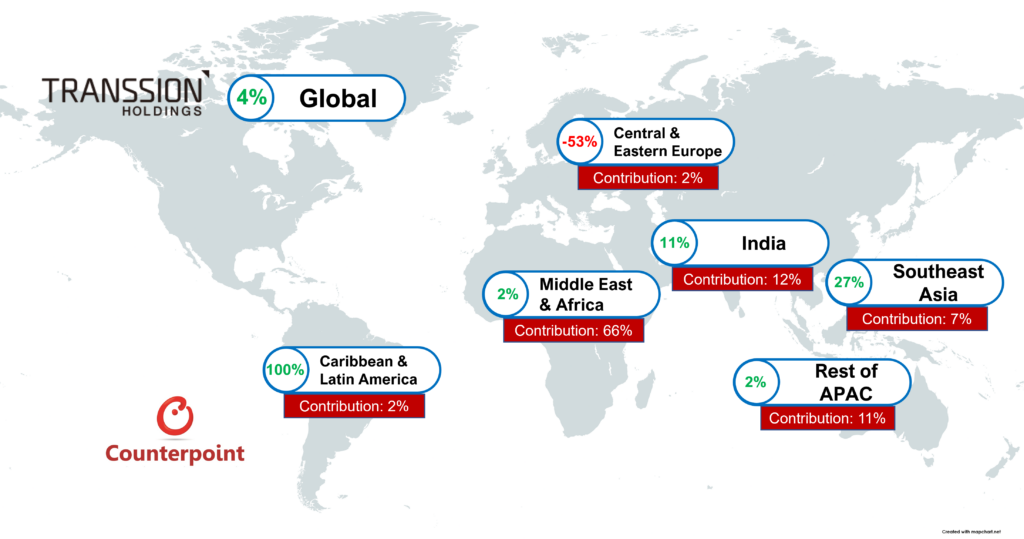

Much of Transsion’s financial successes can be attributed to its continued commitment to entering new markets. In Q2 2023, Africa accounted for 57% of Transsion’s smartphone sales volume, a net drop of 8% from a year ago. Outside Africa, Transsion smartphone sales grew 35% in Q2 2023, most notably in Latin America, EasternEurope,Indiaand Southeast Asia.

The reason for Transsion’s big increase in profitability is found in its ability to upsell to customers. Average selling prices (ASP) for Transsion smartphones rose by 14% YoY for two years in a row. The MEA region anchored the increase as a big expansion into the Middle East was the main factor. In a bid to replicate its success in Africa, Transsion has targeted the low end when entering new markets, but there is potential for the company to grow beyond the current level.

While Transsion continues to enjoy stable gross margins of around 30% in Africa, the company does face a more competitive landscape in the rest of the world, with gross margins of 15%-20%. However, there is room for improvement as the company continues with its premiumization strategy. In a recent interview, Transsion VP Qi Zhang said the company would be launching a flipfoldablein September in another attempt to showcase its technical prowess in the premium segment.

Q3 Revenue Stays Resilient, But Profit Declines Sharply as Costs Balloon

December 13, 2022

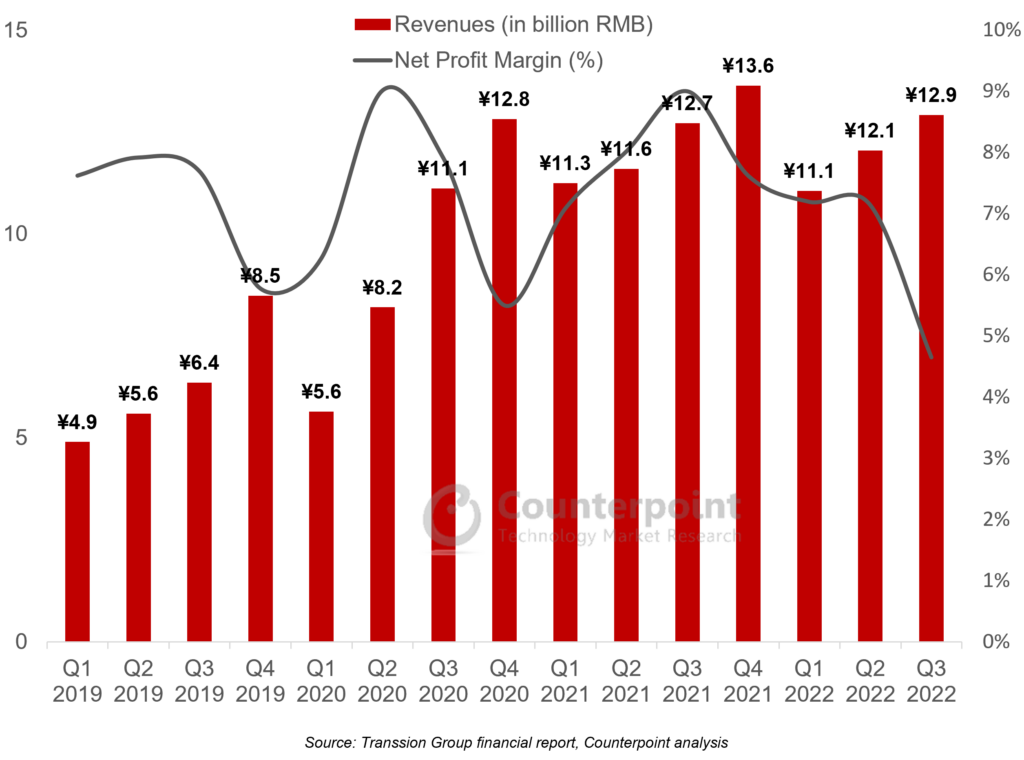

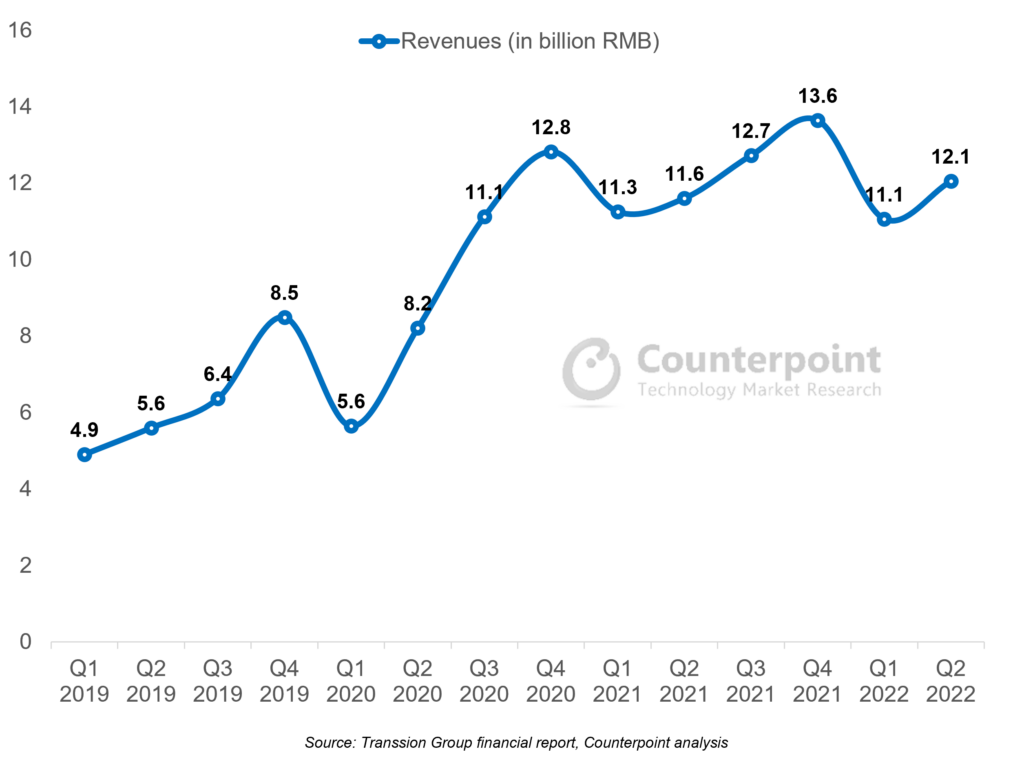

Transsion Holdings has reported flat revenue growth for Q3 2022 at 12.9 billion RMB. However, net profit slumped 47.4% YoY due to macroeconomic headwinds, inventory destocking initiatives, competitive pressures, and higher R&D and market expenditure.

Transsion Group Quarterly Revenue and Net Profit Margin

Transsion’s Q3 smartphone shipments fell 18% YoY, as emerging market demand was hammered by macroeconomic concerns. Inflation rates ticked higher, continuing the pressure on lower-income consumers with high food and energy prices. Local currencies too continued to depreciate against the US dollar.

Despite the big drop in shipment numbers, Transsion’s revenues still achieved positive growth. This was due to a big increase in smartphone selling prices. TECNO and Infinix’s average selling prices (ASPs) rose 26% and 28% YoY respectively. Transsion was able to achieve this due to successful iterations of mainstream devices across TECNO and Infinix, while launching more sophisticated devices that have gathered popularity among aspiring switchers. On the other hand, bringing higher-value products to more mature markets in India and Southeast Asia meant higher contribution from higher-end products to the company’s revenue mix.

Transsion Group Financials Deep Dive – Sales, R&D and Inventory

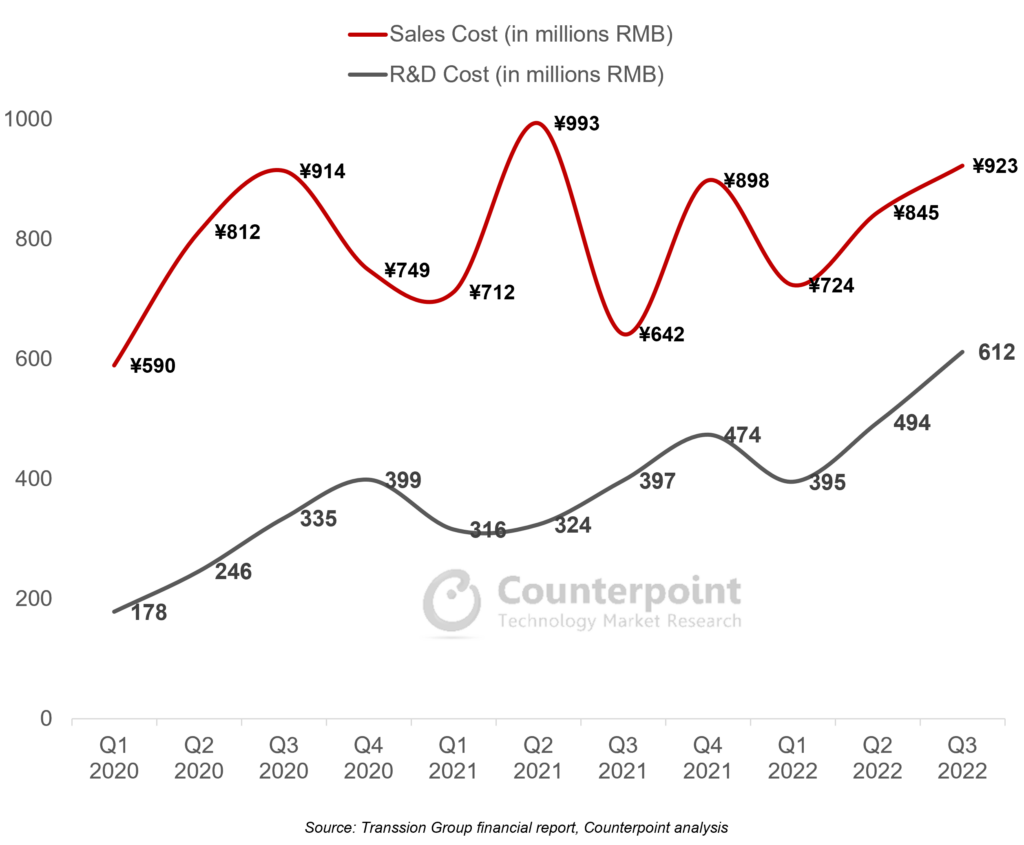

Three items, in particular, caught our attention in Transsion’s Q3 report:

Inventory:Since the COVID-19 lockdowns, Transsion has moved decidedly away from the feature phone business and into the smartphone business. In parallel, inventory levels have also crept up, reaching an all-time high of 80% of quarterly revenues in Q2 2022, which caused discomfort for the management. In Q3, this level was brought down to a more manageable 57%, which put pressure on margins in the quarter but removed a significant uncertainty for future quarters, as the smartphone market is not expected to rebound until well into 2023.

Sales cost:除了销货成本,销售成本的代表resent the biggest cost item in Transsion’s income statement. In a year when Transsion has reported slowing revenue growth, its sales costs have increased significantly as the company paves the way for an aggressive expansion into other regions. Transsion will be hoping the global smartphone market recovers quickly in 2023, but its investment case could come into doubt if smartphone shipments and market share do not pick up meaningfully in its key markets in the next few quarters.

R&D:Transsion is spending heavily on R&D, which is an encouraging sign as the company aspires to move into higher-value smartphone segments and other smart device categories. We expect this trend to continue as the window of opportunity for entry-level devices narrows, considering device costs are expected to creep up, in line with the inflation rate.

Last quarter, we discussed Transsion’s stock options plan for 2022, which is linked to 2024 financial metrics. We expect the company to target 20-25% annual revenue growth rates for both 2023 and 2024. Much of this will depend on the company continuing to move up the smartphone value chain with 5G-capable devices, entry into IoT segments and monetization initiatives for its wide user base. Above all, the recovery of the global economy and smartphone market will be pivotal for Transsion as it gradually becomes more exposed to a wide range of different geographical locations.

Resilient Q2 Performance Driven by Pivot to Value, But Macroeconomic Challenges Remain

August 29, 2022

Transsion Holdings reported a 3.7% YoY increase in its Q2 2022 revenue to RMB 12.1 billion and a 4.5% YoY decline in net profit to RMB 1.04 billion. Considering the macroeconomic headwinds in Transsion’s core markets, the increase in revenue was a bright spot, especially compared with Q1 when the company posted a quarterly revenue drop for the first time since its market debut in September 2019.

Transsion Group Quarterly Revenue

Transsion’s Q2 smartphone shipments grew 4.1% YoY, an impressive performance despite a shrinking global market, whichretreated 9%YoY during the quarter. Geopolitical tensions and high inflation rates have hurt the global smartphone market in general. Further, companies exposed to the low- to mid-end segments and emerging markets are more prone to secondary impacts, such as the strain on customers from high food and energy prices, weaker local currencies against the US dollar, and higher government taxes and levies on ‘non-essential’ imports like consumer electronics.

Transsion defied these global trends through resilient performance in its Africa home market and strong growth in other regions, most noticeably in India and Southeast Asia. In both these regions, Transsion is ranked sixth in terms of shipments, helped by the company’s double-digit annual growth rate. Gaining a foothold in these new markets helps the company diversify its revenue sources and also allows the company to move up the pricing curve. According to Counterpoint’s Model Sales Service, Transsion’s smartphone average selling prices (ASP) increased 14% YoY, mainly driven by the success of the company’s TECNO and Infinix brands. The brands’ latest products received good market reception and are edging closer to the $150 mark.

Due to the increased pricing, Transsion’s Q2 normalized gross profit margin reached 22.9%, up 1.4% YoY, to reverse a six-quarter slump. However, the bottom line retreated, mainly due to a significant 40% increase in R&D spending. In our view, this is a positive sign that the company is moving out of its comfort zone of focusing only on pricing competitiveness in its African home market and committing to make more sophisticated products for the higher value markets.

Despite our positive commentary, we also recognize the significant challenges brought on by the macro environment, which is not likely to ease in the near term. In Q2 2022, we observed inventory challenges across handset and component makers, including Transsion. The company’s inventories reached RMB 9.6 billion as at the end of Q2, 27% higher than that in Q4 2021 and 73% more than in Q4 2020. Currently, inventory levels are 19% of the company’s 12-month trailing revenue, which could become an issue if it remains high or if revenue declines in the coming months.

We also note that the company’s recently announced stock options plan for 2022 is linked to its targeted 2024 financial metrics. The plan suggests that the company forecasts revenue and net profit to increase 15% and 32.25% respectively as a baseline case, or 20% and 44% respectively as a bull case by 2024. The targets are compared with the metrics from 2021, which was a strong financial year for Transsion, indicating that the company is extremely bullish about the next couple of years.

Growth Worries in Africa, India See First Revenue Drop Since COVID-19, But Diversification Efforts on Track

June 6, 2022

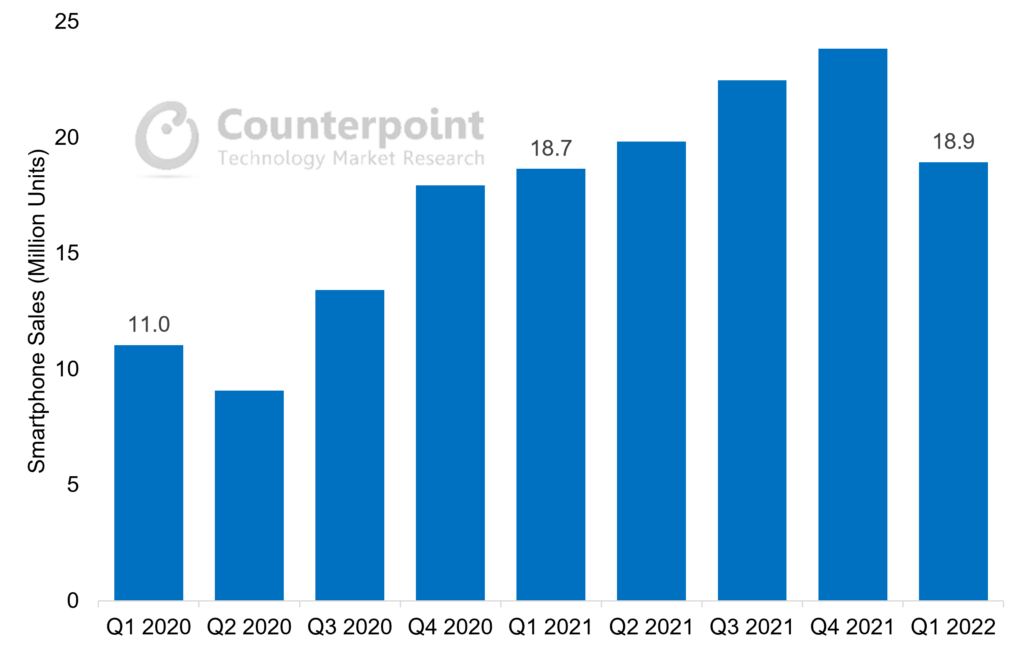

Transsion Holdings reported Q1 2022 earnings that saw revenues and net profit drop 1.8% and 7.6% YoY respectively. This is Transsion’s first revenue and profit drop since it went public in September 2019. The company’s performance during the quarter was impacted mainly by the stalled growth in its home market Africa and in India, which saw inflationary pressures hitting lower-income consumers significantly. Smartphone sales were down in the region for the first time since the pandemic. However, the company was cushioned by growth in other regions, and margins remained intact despite inventory build-up.

According to Counterpoint Research’sMarket Pulseservice, cumulative Transsion smartphone shipments reached 18.9 million units in Q1 2022. This was a small increase of 1.6%, the slowest YoY growth rate since the pandemic.

Transsion Group Quarterly Smartphone Sales

Source: Counterpoint Market Pulse Service

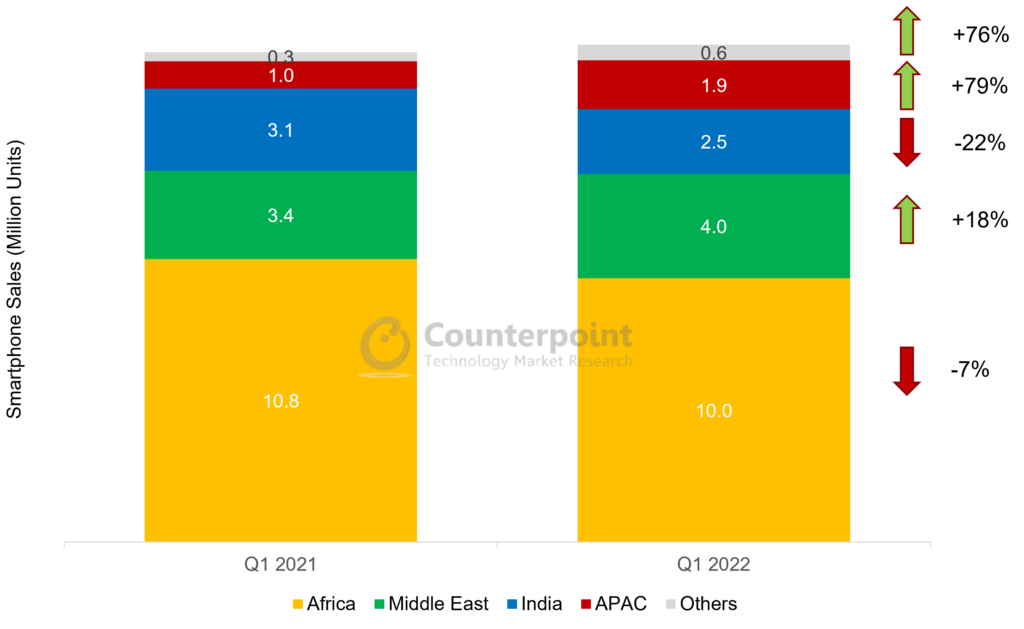

Looking further under the hood, there are significant regional disparities, however. In Africa, Transsion saw a 7% decline in smartphone sales in Q1 2022, mainly due to the inflationary impact on consumer sentiment. Most large African markets were already running double-digit inflation during 2021, but the Ukraine war had far-reaching consequences as food imports were hampered, affecting lower-income consumers more. Depreciating local currencies also put pressure on the company’s supply chain and margins.

在印度,类似宏的问题和影响Omicron wave saw the smartphone market record the first Q1 drop ever. Here, Transsion smartphone sales dropped 22%. The market sentiment in India is expected to remain weak in Q2, but sales are likely to see growth due to the low base of Q2 2021 when the market was hit hard by the Delta wave.

On the other hand, Transsion had resilient performances in the Middle East and APAC, which show its diversification efforts are working. In both regions, the company is finding success in penetrating the entry-level segment in key countries like Pakistan and Bangladesh. Transsion’s 79% sales increase in APAC runs counter to the broader market. In the Middle East, the 18% sales increase is likely to extend further in 2022, as the region is expected to be the best-performing smartphone market due to the economic growth driven by oil revenue increases, mainly in Gulf Cooperation Council (GCC) countries.

Transsion Group Smartphone Sales by Region, Q1 2022 vs Q1 2021 (In million units)

Source: Counterpoint Market Pulse Service

Transsion Q1的规范化的毛利率2022 decreased to 21.4%, or 2% less than the same period in the previous year. Significant cost pressures persisted due to lingering supply chain disruptions, component shortages and high inventory levels. Rising revenues from other regions are also likely to cap the company’s margins, as it enjoys far higher margins in its home market Africa. However, Transsion now derives 87% of its revenues from the smartphone business, and as feature phone-to-smartphone migration continues for its emerging market customers, we see further room for the company’s revenues and margins to grow.

Transsion 2021迹象风格:智能手机et share continues to increase in emerging markets

April 28, 2022

Transsion Holdings reported 2021 results with revenues up 31.8% YoY and net profit up 45.5% YoY. These results were driven mainly by increasing smartphone sales and market share, which widened in the core African market, while achieving breakthroughs in key South Asian countries like Pakistan, Bangladesh and India. IoT and internet services, which accounted for 6.5% of the group’s revenues in 2021, also saw robust triple-digit growth.

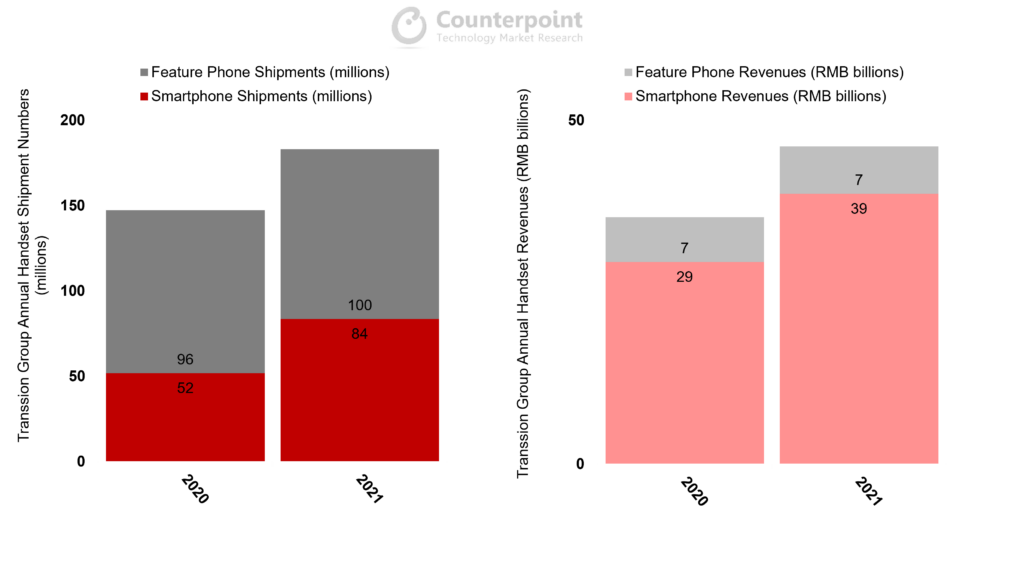

According to Counterpoint Research’sMarket Monitorservice, cumulative Transsion handset shipments reached 184 million units in 2021, an all-time high. Smartphones, in particular, grew 61%.

Transsion Group Handset Shipment and Revenue Analysis

Sources: Counterpoint Market Monitor Service, Transsion Group financial statements

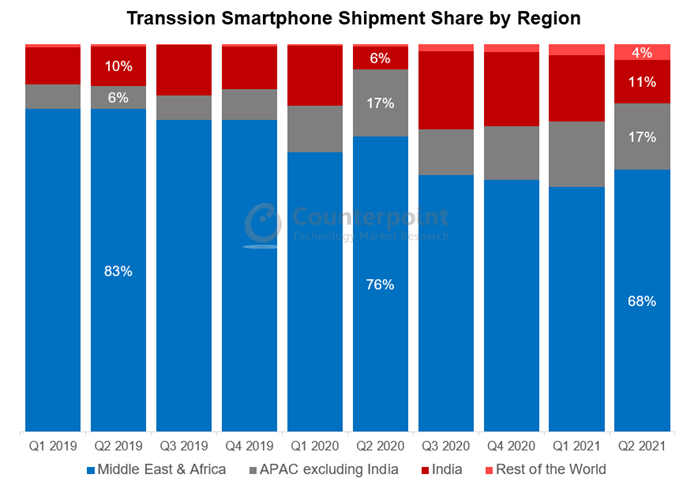

Transsion continued to do well in its home market Africa, where it already dominates with close to 45% share across its three brands. However, Africa accounted for only half of the shipment increases in 2021. In India, Transsion almost doubled its smartphone sales in one year, while the company is already the biggest smartphone OEM in Pakistan. As such, Transsion smartphone sales attributed to Africa decreased from 67% in 2020 to 56% in 2021. A widening geographical footprint, accompanied by an enriched portfolio, can help the company diversify its customer base and increase its technical prowess.

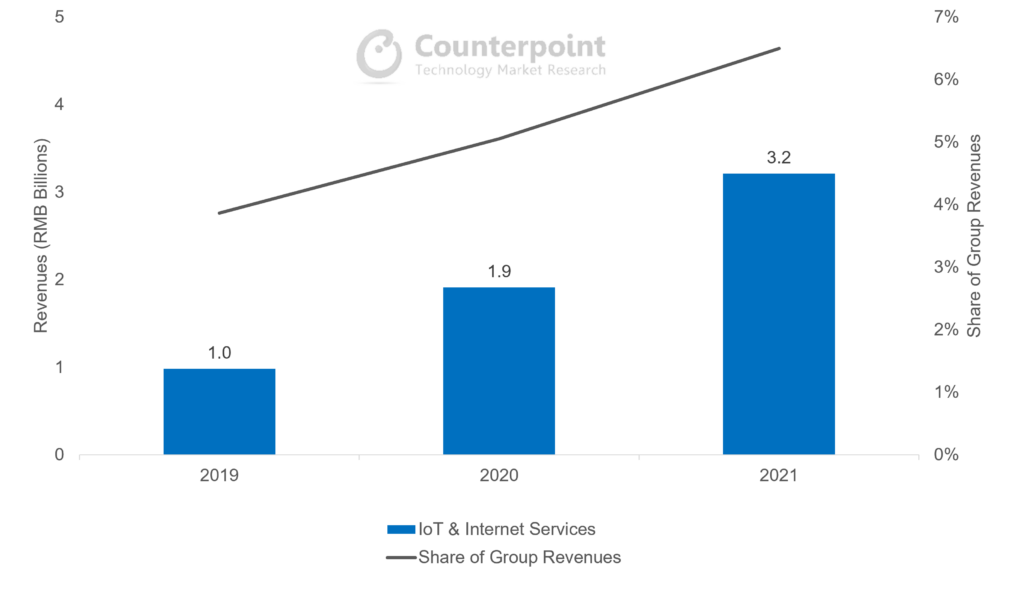

The company also reported surprisingly good revenue growth from other businesses. Revenues not attributed to handsets, which mainly include IoT and internet services, grew 68% YoY to RMB 3.2 billion. Their contribution to group revenues now stands at 6.5%. This is due to new products in the wearables, TWS, notebook and TV categories. But more importantly, Transsion’s ‘Matrix of Internet Products’ became meaningful growth engines. Apps under the Transsion umbrella saw installations increase 240% YoY, with three apps – Phoenix, Boomplay and Scooper (with MAUs of 100 million, 68 million and 27 million respectively) – becoming main gateways to the internet for African users. User and eventually revenue growth from apps will become ever more important factors in Transsion’s future strategy, particularly in Africa, as its handset business will inevitably hit road bumps in the future.

Transsion IoT & Internet Services Analysis

Source: Transsion Group Financial Statements

Transsion’s normalized gross profit margins decreased to 21.3% for the year, after staying above 23% for the first three quarters of 2021. There were significant cost pressures in the second half of the year, especially due to supply chain disruptions and component shortages. We expect these issues to gradually ease in 2022 as the supply and demand dynamics in the semiconductor industry improve, and supply chains become more resilient to shocks. However, foreign exchange fluctuations and inflationary pressures in key markets will be the new destabilizing factors for the company, as risks shift from the supply to the demand side in the wider global handset market.

Transsion handset sales, profit continue to improve despite cost pressures

November 24, 2021

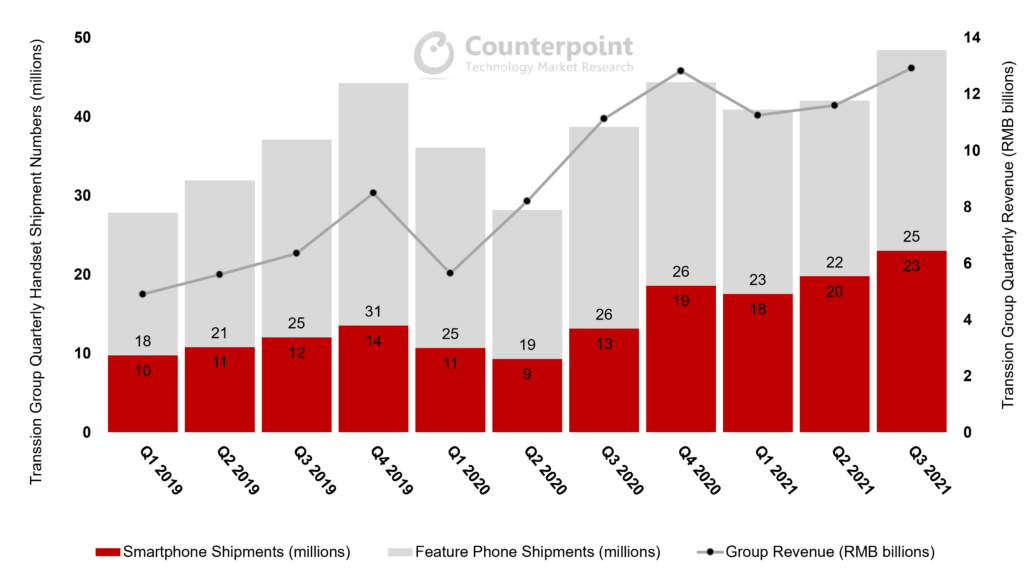

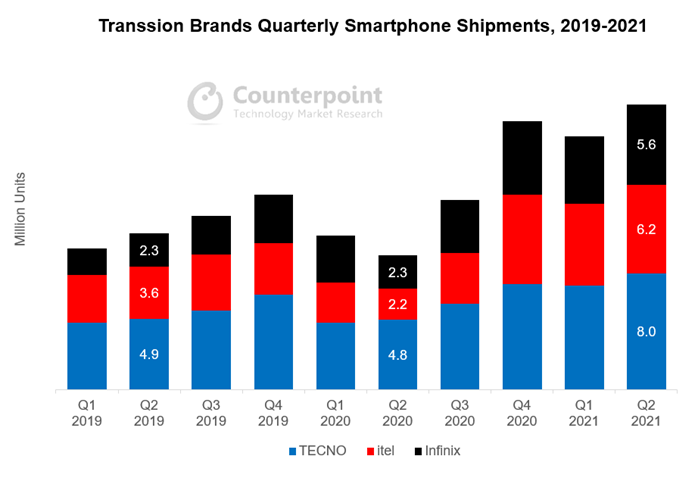

Transsion Holdings reported Q3 2021 results with revenues up 16% YoY and net profit up 33% YoY. These positive results were driven once again by further pivoting to smartphone sales, especially in the core African market. According to Counterpoint Research’sMarket Monitorservice, cumulative Transsion smartphone shipments surpassed 20 million units for the first time ever, coming in at 23 million. This represents a growth rate of 75% YoY.

Transsion Group Handset Shipment and Revenue Analysis

Sources: Counterpoint Market Monitor Service, Transsion Group financial statements

While feature phone shipment growth moderated in Q3 2021, the bulk of Transsion’s revenue growth was driven by smartphones. Heading into the Q4 holiday shopping season and 2022, we may see Transsion’s smartphone shipments overtake feature phones for the first time.

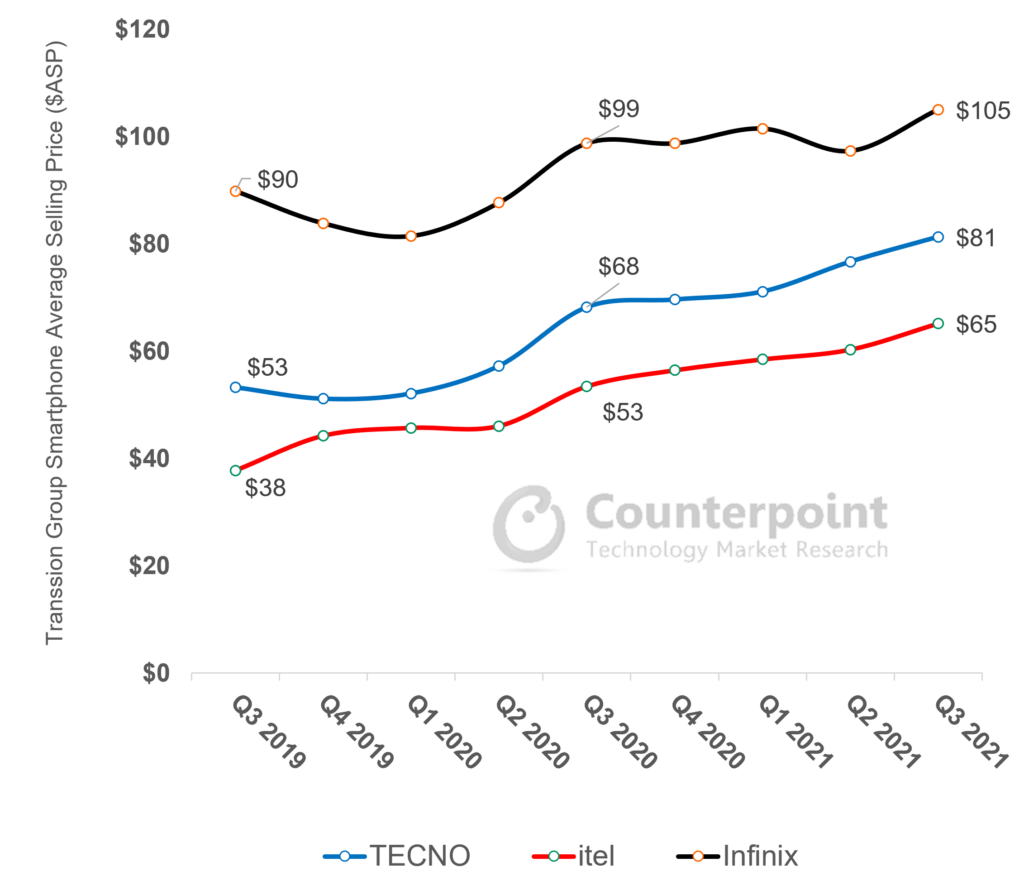

Over the past couple of years, as Transsion smartphones penetrated more markets, the average selling price (ASP) saw a noticeable increase. While the ASP showed a mixed trend in the second half of 2019, it increased decisively during 2020 and is showing no signs of slowing down in 2021. Looking at Transsion’s brands closely, TECNO, itel and Infinix saw ASP increases of 56%, 43% and 29% respectively over the past 18 months. These point to positive consumer sentiment and changing perception of digital and mobile services. More consumers in emerging markets now recognize that a decent smartphone is an important component of their daily lives.

Transsion Group Smartphone Average Selling Price ($)

Source: Counterpoint Handset Model Sales Service

Transsion’s normalized gross profit margins increased to 25.3% in Q3, compared to 25% in Q2 and 23% in Q1. The company managed to navigate the ongoing component shortages well and was able to pass upstream cost increases to consumers. Selling, General & Administrative (SG&A) expenses and financing costs dropped as well. Furthermore, ventures outside sub-Saharan Africa, including in higher value markets in Southeast Asia and the Middle East, contributed to higher profit margins. Profitability may increase further as the supply chain situation stabilizes in 2022.

Smartphone Sales and Profitability Double Boost as Company Diversification Efforts Gather Pace

September 30, 2021

Transsion Holdings continued to see strong performance in H1 2021 with revenues and net income growing 65% and 59% YoY respectively, driven primarily by surging handset sales in its home market Africa, as well as successful ventures in other developing countries. According to Counterpoint Research’sMarket Monitor service, cumulative Transsion smartphone shipments in H1 2021 reached a record high of 37.3 million, taking the company’s share in the global smartphone market to 5.5% from 3.5% a year ago.

Counterpoint Research – Market Monitor Service

Looking at Transsion’s overall product strategy, we can see that it is shifting materially from feature phones to smartphones in response to market changes. In 2019, 33% of the company’s handsets were smartphones, but in the latest quarter this number has gone up to 47%. In the company’s latest earnings release, smartphones account for over 80% of its revenues, a record high.

Transsion financial report, Counterpoint Research analysis

Commenting on Transsion’s commitment to smartphones,Senior Analyst Yang Wangsaid, “Transsion is rapidly transforming and upgrading its product portfolio. The move is driven by the accelerating demand for internet-capable phones in itshome market Africa, where the COVID-19 pandemic showed the value of the internet to consumers who were forced to stay at home. The region’s internet and mobile money services are also gathering steam along with a significant drop in data costs. While all OEMs stand to benefit from the consumer’s shift, Transsion gains the most as its distribution and pricing strategies are most ready to tap into new consumer clusters, which previously did not consider buying a smartphone.”

Counterpoint Research – Market Monitor Service

Apart from product transformation, the other significant shift in the Transsion strategy is geographical diversification. Compared to two years ago, Transsion’s share of smartphone shipments in the Middle East and Africa (MEA) region has dropped from 83% to 68%. On the other hand, shipments have increased rapidly in APAC countries such as India, Pakistan, Bangladesh, Indonesia and Thailand.Indiaspecifically has been the growth engine for Transsion, with shipments almost reaching 20% of the company’s global total in H2 2020, before the Delta wave halted the progress.

Commenting on Transsion’s moves in India,SeniorAnalyst Prachir Singh说,“Transsion品牌,尤其是TECNO,en focusing on a hybrid channel strategy in India, with an increased emphasis on online channels. This was executed with great success as Transsion brands contributed to 7% of the online smartphone market in India in Q2 2021, compared to 2% in Q2 2020. TECNO’s online smartphone shipments grew almost 20x YoY in Q2 2021, while itel increased its online share by launching online exclusive models like the Vision 1 Pro and A47. From a product positioning point of view, Transsion brands have been focusing on providing specs like higher display size, multi-camera capability and bigger battery, which are the top spec preferences for consumers in the sub-$150 segment.”

Going forward, Transsion’s fundamentals are expected to remain solid, as it continues to hold enormous clout in its Africa home market. Smartphone penetration will gradually expand, with new users continuing to be brought into the internet world. On the other hand, Chinese brands such as Xiaomi, OPPO and vivo are strengthening their market penetration efforts in certain African markets to address the medium-range segment (<$200). This price band is above Transsion’s typical playing field, so the newcomers are unlikely to affect its market share in the short term. However, we have seen in recent years Transsion’s effort to produce more premium phones and enter the <$200 price band. Therefore, there may be a time in the future when Transsion competes directly with the likes of Xiaomi, OPPO and vivo.

The Saudi Arabia smartphone market was among the few to record YoY growth in Q1 2023.

Even as many economies struggled in 2022 amid macroeconomic and geopolitical pressures, Saudi Arabia was bolstered by its highest oil revenues in decades, all-time-low unemployment rates, all-time-high non-oil economic activity and strong private consumption.

Among OEMs, Samsung and Apple continued to take over half of the total smartphone shipments in Q1 2023, with Samsung taking the #1 spot.

We expect the Saudi Arabia smartphone market to continue its growth momentum in 2023, with annual shipments likely to grow in low single digits.

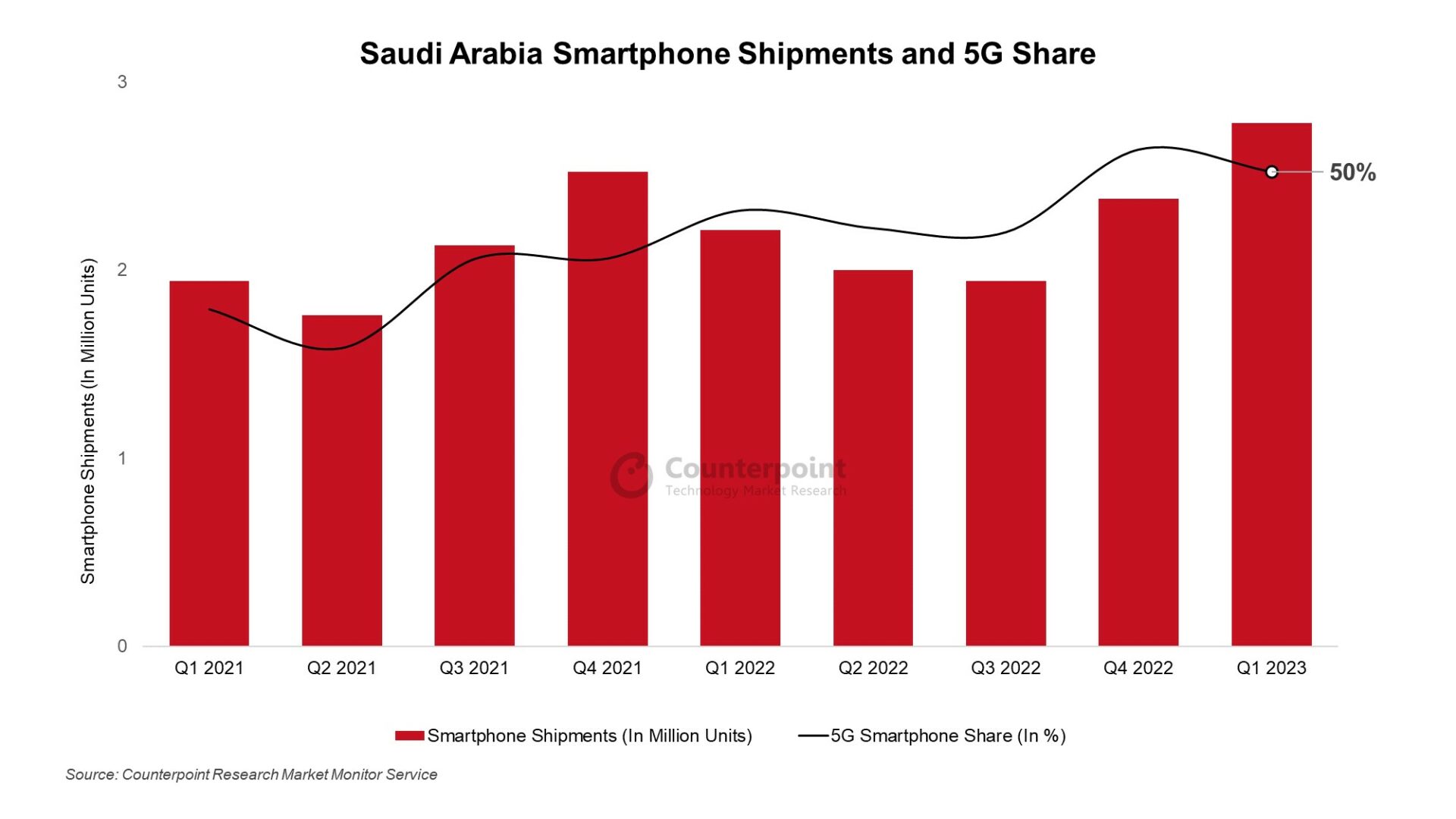

The Saudi Arabia smartphone market was among the few to record YoY growth in Q1 2023, with shipments growing 26% YoY largely due to strong macroeconomic fundamentals, accelerating digitalization, and growing device financing options. In QoQ terms, the shipments grew 17% as OEMs filled channels for the Easter and Ramadan sales season, towards the end of the quarter.

Growth drivers

As manyglobal economies struggled in 2022amid macroeconomic and geopolitical pressures, Saudi Arabia was among the few to buck the trend. Bolstered by its highest oil revenues in decades as global oil prices soared, Saudi Arabia was the fastest-growing economy in 2022, with all-time-low unemployment rates, all-time-high non-oil economic activity and strong private consumption. PoS (Point of Sale) transactions, e-commerce activity and digital payments have also been on the rise in Saudi Arabia, all pointing to growing digitalization and private consumption. Some of the market momentum at the end of 2022 was carried into Q1 2023, especially after the economic boost provided by the FIFA World Cup in Qatar and the year-end and holiday season of Q4 2022.

Saudi Arabia Smartphone Shipments and 5G Share – Q1 2021 to Q1 2023

While the feature phone to smartphone migration has slowed down in Saudi Arabia, a growing digital economy and an aspirational customer have become key growth drivers. Commercial and private 5G use is also increasing in the country, pushing 5G smartphone sales. 5G technologies are a key part of Saudi Arabia’s digitalization and growth push under the Vision 2030 plan. The country has partnered with major 5G infrastructure players likeHuaweiandEricsson, and5G networksare now available in most major cities, covering around 80% of the country’s population. Saudi Arabia has also been hailed as a 5G pioneer in the region in terms of coverage, speed and consistency. 5G smartphone share remained above half of total smartphone shipments for the second consecutivequarterin Q1 2023 and is likely to grow further in 2023.

Competitive landscape

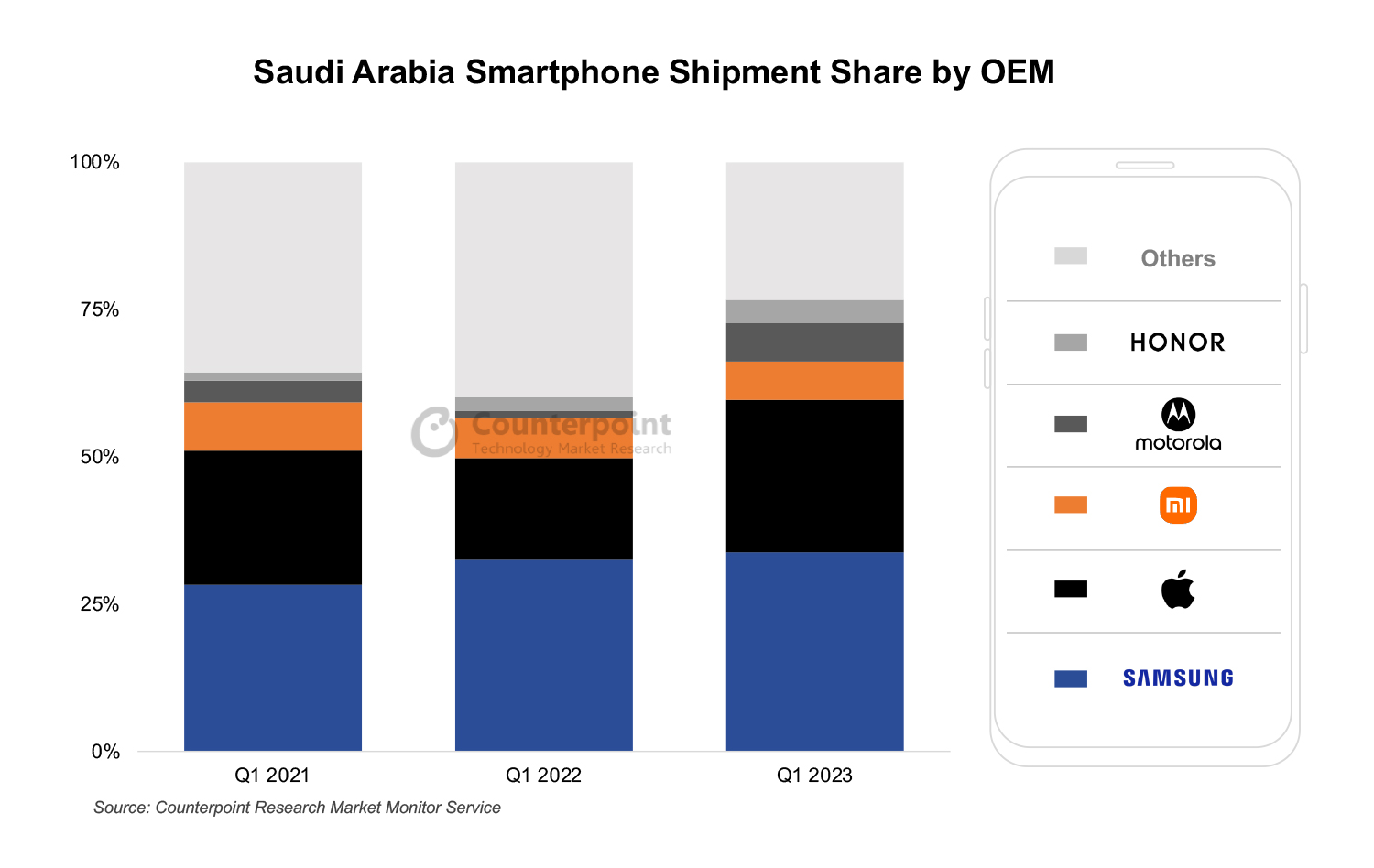

沙特阿拉伯oem fo智能手机出货量的前5位r Q1 2021, Q1 2022, Q1 2023

Among OEMs, Samsung and Apple continued to take over half of the total smartphone shipments in Q1 2023, with Samsung taking the #1 spot. Xiaomi and Motorola were distant third, with HONOR rounding out the top five for Q1 2023.

Samsunggrew YoY as its supply normalized in the region. The brand’s 5G models have been leading growth, especially the new affordable 5G M-series and A-series iterations. The Galaxy M53 was the best-selling Android device in the country in Q1. Samsung’s newest flagshipGalaxy S23series was shipped slightly earlier than theS22 series in 2022to meet the pre-order demand triggered by aggressive marketing and promotions in the country, with most channels and offline stores participating.

Apple’s智能手机出货量同比由几乎翻了一番popularity of itsiPhone 14 series, especially thePro versions, and as older models became affordable and available. Apple reached its highest-ever Q1 shipment share in Saudi Arabia in 2023. The brand has greatly benefitted from therise of financing options, like the ‘Buy Now, Pay Later’ model, in Saudi Arabia, making its devices accessible to a greater demographic. Besides, a rising mean wage and stable exchange rates increased the average Saudi Arabian consumer’s purchasing power in 2022. iPhones took four of the top five spots in the bestseller list for Q1 2023, with the iPhone 14 Pro coming out on top.

WhileXiaomi’sshipments grew YoY in Q1, it lost share marginally, as Motorola and HONOR gained share driven by new launches. Xiaomi has been able to maintain share largely due to its broad portfolio across price bands, innovative marketing strategies, and a strong presence across both offline and online channels.

Motorolahas been gaining share, led by its offerings in the $150-$249 price band, particularly its G series, which accounted for nearly three-quarters of its total sales in Q1. Motorola has benefitted from improved product availability, especially for new launches, and strong brand pull, especially for middle-income customers looking for upgrades to their lower-segment devices.

HONORwas among the fastest-growing brands in Q1, with its shipments more than doubling YoY. HONOR’s growth is largely due to focused expansion efforts, aggressive launch campaigns and an attractive mid-tier to high-end portfolio. HONOR has also benefitted from utilizing Huawei’s earlier distribution and channel relationships. The HONOR 70 and the X series were the top volume drivers for the OEM in Saudi Arabia for Q1 2023.

Smartphone sales grew YoY across all price bands in Q1 2023 but declined QoQ largely due to seasonality. All price bands except thepremiumband (≥$600) lost share YoY as consumers moved up the price bands. But thepremiumband was the fastest-growing band in Q1, led by Apple and Samsung. Apple captured around 85% of the total premium smartphone sales in Q1. The mid-tier ($100-$249) remained the largest price band in Saudi Arabia, capturing nearly half of the total smartphone sales in Q1, with Samsung and Xiaomi taking the top spots in the price band. Thelower (<$100) segmentgrew YoY but, like other non-premium segments, lost sales share during the same period, as customers continued to buy higher-ASP devices with improving affordability and rising aspirations.

Market outlook

We expect the ASP of smartphones sold in Saudi Arabia to continue to rise in 2023, as wage rates improve, financing options become more accessible, and customers move towards better devices. Currently, Apple and Samsung remain best equipped to capture more share of the aspirational Saudi Arabia smartphone market, but the quest for the #3 spot continues. While Xiaomi remains comfortably in the #3 spot, other Android OEMs have been mounting pressure with bolder promotions and marketing activities and aggressive launch strategies. Motorola, HONOR and Transsion Group brands Infinix and TECNO are likely candidates outside the top three to capture market growth.

Going forward, we expect the Saudi Arabia smartphone market to continue its growth momentum, with annual shipments likely to grow in low single digits in 2023. Increasing 5G use, ramping up of digitalization, greater access to financing options and growing aspirations of customers are expected to drive growth.

Note:

ASP & Priceband Analysis done using Wholesale Prices

意味着智能手机shipments retreated 18.4% YoY in Q4 2022 and 12.1% YoY in 2022.

At 148 million units, 2022 shipments were the lowest since 2015.

Samsung performed resiliently in 2022, with shipments and market share increasing YoY.

Transsion Group’s 2022 shipments dropped 13% YoY. This was mainly due to a 27% drop of itel.

Xiaomi saw a flat year but much better performance than in 2021.

5G shipments increased 47% YoY to account for 18% of the overall shipments.

London, Boston, Toronto, New Delhi, Hong Kong, Beijing, Taipei, Seoul – February 23, 2023

Smartphone shipments in the Middle East and Africa (MEA) region fell 12.1% YoY in 2022 to 148 million units, the lowest shipment level since 2015, according to the latest research from Counterpoint’sMarket Monitor Service. After a bright start to the year, the rise in energy and agricultural goods prices caused by the Ukraine war dampened consumer sentiment in the region, with themacroeconomic situationgradually worsening as the year went on.

Looking at the fourth quarter, smartphone shipments dropped 18.4% YoY, a slightly better reading than the record low of the 20.4% drop recorded in Q3 2022. Consumer sentiment may have picked up marginally as the inflationary pressure and foreign currency headwinds receded. Still, the market environment remained very challenging.

Commenting on the market’s performance,Senior Analyst Yang Wangsaid, “The MEA smartphone market closed the year with another tough quarter. Much of the difficulties, such as high inflation rates, energy and food prices, and depreciating domestic currencies against the US dollar, were caused by factors outside of the control of market participants. With the drop in consumer sentiment, OEMs were put under enormous pressure and had to take drastic measures such as destocking, cutting marketing and channel spending, and taking a very careful approach to pricing.”

Source: Counterpoint Research Market Monitor, Q4 2022 Notes: Xiaomi includes POCO and Redmi; OPPO includes OnePlus; Figures may not add up to 100% due to rounding.

Market leaderSamsungsaw YoY volume and market share growth in 2022, a terrific performance given the market realities. This was due to the success of the Galaxy A series in capturing the market for aspirational upgraders, particularly those that may be getting their first 5G devices. The company also benefitted from a significantly improved supply chain position, giving distributors clarity and certainty in a time of turbulence.

TranssionGroup brands continued to take the MEA region’s biggest share of smartphone shipments, with an unchanged market share of 32%. However, the company endured a volatile year, withTECNOanditelboth shedding shipment volumes in double digits due to exposure to the price-sensitive entry segment, whileInfinix’s strong momentum from the first half of 2022 retreated towards the end of the year. Aggressive destocking initiatives mostly bore fruit, as TECNO and Infinix returned to launching higher-end devices during the shopping season.

Xiaomifinished the year at the third spot among OEMs in the MEA region. It was a relatively successful year for the company with volume and market share gains. Supply issues largely disappeared, and the company saw good traction in the mid-range segment, particularly for the Redmi Note 11 and Redmi 10 series. Xiaomi is expected to take the competition to Samsung’s A series as it broadens the availability of affordable 5G devices across the region.

Apple的出货量同比下降,但品牌看到了马rket share increase due to broadened distribution in the region and the success of the iPhone 13 series. The iPhone 14 series launch has not been as successful as the iPhone 13 series. However, sales have concentrated towards the higher-end iPhone 14 Pro and Pro Max models, thus replicatingApple’s value gains seen in other more developed markets.

Source: Counterpoint Research Market Monitor, Q4 2022

One of the spotlights in the MEA smartphone market in 2022 was the growth of the 5G segment. 5G smartphone shipments grew 47% to reach an 18% share of the overall shipments against our forecast of 16.5% at the beginning of 2022. While 5G networks are only available in the GCC countries and certain pockets of Africa’s urban areas, the enthusiasm for 5G devices has been noted across the largest markets. Samsung, having overtaken Apple as the biggest 5G OEM in the region, is well positioned to grow further with its large portfolio of mid-range 5G A-series devices. Xiaomi is also seeing momentum for its mid-range devices, and we are likely to see Transsion brands TECNO and Infinix make a serious play in the 5G market in 2023. While globally 5G smartphone prices are coming down due to the availability of more affordable models, the proliferation of 5G devices in MEA will actually boost the average selling price (ASP) in the region, as customers upgrade to more sophisticated devices. This, in turn, is likely to increase the dollar value of the MEA smartphone market, despite little to no growth in volume expected in 2023.

Counterpoint Research’s market-leadingMarket Monitor,MarketPulse andModel Salesservices for mobile handsets are available for subscribing clients.

Feel free to contact us at press@www.arena-ruc.com for questions regarding our in-depth research and insights.

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

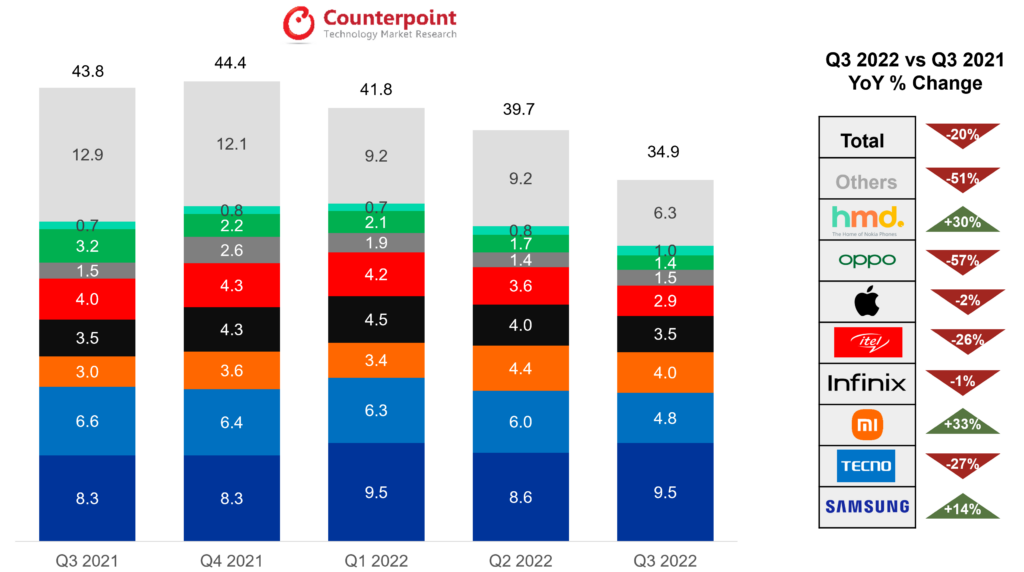

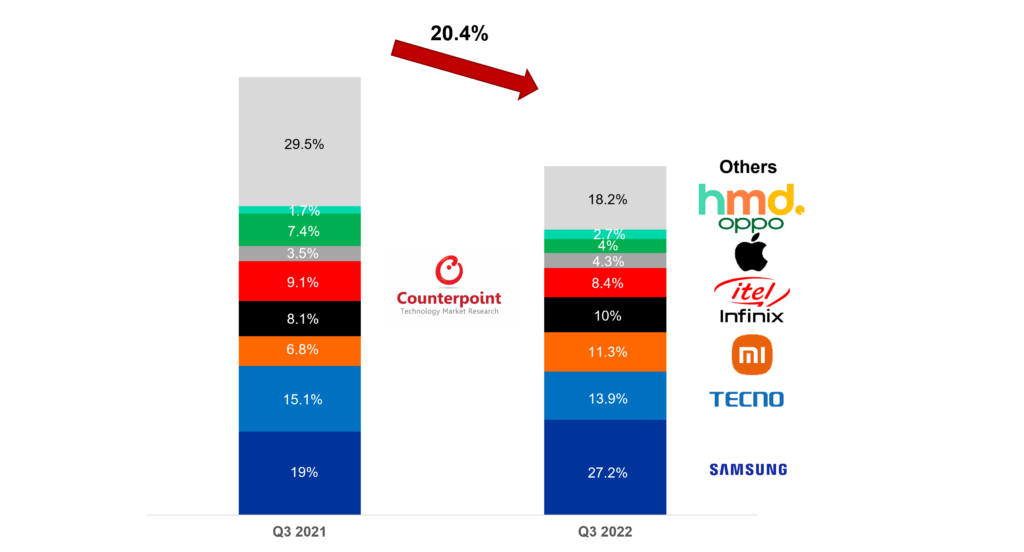

意味着智能手机shipments retreated 20.4% YoY and 12% QoQ in Q3 2022 to 35 million units.

This was the lowest level since Q2 2020, or since the startof the COVID-19 pandemic.

Samsung’s shipments and market share increased YoY as the new A-series models continued to gain momentum.

Transsion Group’s shipments led the market downturn, mainly due to TECNO and itel’s aggressive destocking efforts. Infinix, on the other hand, remained resilient to market headwinds.

Xiaomi returned to growth as product availability improved, while its exposure to the Middle East market benefitted from improving sentiment.

London, Boston, Toronto, New Delhi, Hong Kong, Beijing, Taipei, Seoul – December 19, 2022

Smartphone shipments in the Middle East and Africa (MEA) region fell 20.4% YoY and 12% QoQ to 35 million units in Q3 2022, according to the latest research from Counterpoint’sMarket Monitor Service. Compared to the previous quarter, the macro situation continued to worsen as inflation undermined consumer sentiment, while OEMs became ever more cautious in areas such as distribution expansion, marketing efforts and stock management.

意味着Smartphone Quarterly Unit Shipments

Source: Counterpoint Research Market Monitor, Q3 2022 Notes: Xiaomi includes POCO and Redmi; OPPO includes OnePlus; Figures may not add up to 100% due to rounding.

Commenting on the market’s performance,Senior Analyst Yang Wangsaid, “The biggest issue in the smartphone market, and indeed any consumer market, this year has been macro issues. We saw no let-up in inflationary pressures and currency headwinds in the MEA market in Q3 2022. Consumer sentiment continued to be bleak, leading to OEMs and distributors cutting market spending. On the other hand, high inventory levels forced market participants to adopt destocking measures, hurting profit margins. Despite this, the 20% YoY drop probably exaggerated the gloominess in the market, as Q3 2021 was an especially successful period for the region.”

Within the MEA region, the Middle East fared better due to the GCC countries’ resilience. High inflows of energy revenues buttressed state coffers, which strengthened local currencies and kept inflation down. The region was also boosted by sales events associated with the World Cup, which is being held in Qatar since November. On the other hand, roughly 8 in 10 countries in Africa saw inflation accelerating in Q3, according to Counterpoint estimates. Persistent energy supply issues, as well as worries about another round of food shortages, kept consumers ever more cautious. We believe there is further room for inflation rates to rise in Africa towards the end of the year.

意味着Smartphone Unit Shipments Share, Q3 2022 vs Q3 2021

Source: Counterpoint Research Market Monitor, Q3 2022 Notes: Xiaomi includes POCO and Redmi; OPPO includes OnePlus; Figures may not add up to 100% due to rounding.

In terms of the MEA smartphone market’s competitive landscape, the biggest takeaway from the quarter was that while the economic downturn hurt most players, smaller brands disproportionately suffered more, as seen from the dramatic loss of market share. During this period of rising costs and worsening market sentiment, smaller brands faced mounting supply challenges. Maintaining cost discipline meant slashing spending elsewhere, such as marketing and distribution, and smaller players were unable to keep up with the bigger OEMs.

Market leaderSamsungsaw YoY volume and market share growth, as its supply issues subsided, while the Galaxy A series’ 2022 iterations continued to gain momentum. Samsung continues to be the best-placed OEM in the region as its broad product portfolio covers every customer segment. The brand is well-positioned to capture market volume when the economic issues ease.

TranssionGroup brands continued to take the MEA region’s biggest share of smartphone shipments. However, its exposure to the lower-value segments, particularly in Sub-Saharan Africa, meant that it faced the strongest headwinds among the big brands. We noted aggressive destocking efforts during the quarter, mostly concentrated within the lower-endTECNOanditelbrands. On the other hand,Infinixcontinued to perform well as its 2022 models ticked all the boxes. We believe Transsion may stage a rebound towards the end of the year, as the company prepares for higher-end launches for the TECNO and Infinix brands.

Xiaomicaptured the third spot among OEMs, as supply issues disappeared in the rear-view mirror. The company’s affordable mid-range products, particularly the Redmi Note 11 and Redmi 10 series, remained popular among price-conscious customers, while its business received a boost due to favorable conditions in the Middle East region.

Applecontinued to gain market share in the region, largely due to improving distribution across the region. The iPhone 13 series appeared regularly among the best-selling models in the region, even during the last months of the iPhone 13 cycle. We expect Apple’s volume and market share to increase further in the next quarter as the iPhone 14 sales begin to gain momentum.

While the end-of-year shopping season is expected to deliver a boost to the smartphone market, sales increases are unlikely to match the levels seen last year, as affordability will continue to be first and foremost among customers’ concerns. Macroeconomic headwinds and geopolitical uncertainties may well persist into 2023, but we do expect a small rebound in the MEA smartphone market next year. Economies in MEA have fared better than those in developed countries, and the second half of 2023 may see a release of pent-up demand, just as post-COVID-19 reopening spurred a period of consumer optimism.

Counterpoint Research’s market-leadingMarket Monitor,MarketPulse andModel Salesservices for mobile handsets are available for subscribing clients.

Feel free to contact us at press@www.arena-ruc.com for questions regarding our in-depth research and insights.

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

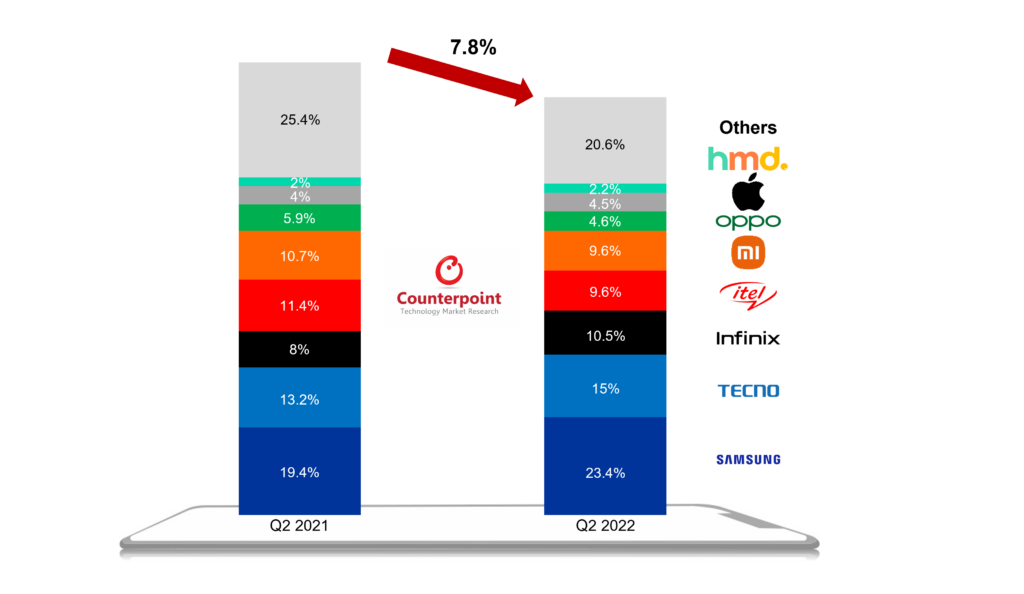

是智能手机出货量同比回落7.8%,10% QoQ in Q2 2022 to 38 million units.

This was the lowest level since Q2 2020, or since the depth of the COVID-19 pandemic.

Samsung’s shipments and market share increased YoY as the mid-range A series gained popularity in the region.

Transsion Group’s shipments were generally flat YoY. Infinix and TECNO gathered pace while itel struggled.

New Chinese entrants Xiaomi, OPPO, vivo and realme trended down sharply due to caution stemming from demand issues elsewhere.

London, Boston, Toronto, New Delhi, Hong Kong, Beijing, Taipei, Seoul – August 8, 2022

Smartphone shipments in the Middle East and Africa (MEA) region fell 7.8% YoY and 10% QoQ to 38 million units in Q2 2022, according to the latest research from Counterpoint’sMarket Monitor Service. Worsening macro headwinds on the economic and geopolitical fronts undermined consumer demand as well as brands’ enthusiasm to expand their footprint across the region.

意味着Smartphone Quarterly Unit Shipments

Source: Counterpoint Research Market Monitor, Q2 2022

Commenting on the market’s performance,Senior Analyst Yang Wangsaid, “The biggest drag on the market was, unsurprisingly, macro issues. Inflation induced by food and fuel shortages dampened consumer demand while declining domestic currencies against the US dollar reduced the purchasing power of consumers.”

There were also secondary macro factors that impacted the market. For example, some governments imposed food export bans or ‘non-essential’ goods import bans to stem the outflow of foreign currency reserves. Taxes on electronics products were also increased, adding more hurdles to the market’s smooth operation.

Given the pessimistic global macro sentiment, we also saw some brands becoming cautious about activities in the region. Difficulties elsewhere meant that brands were under pressure to streamline budgets and activities, which were redirected to more strategic markets and regions. This meant that incentives to push brand penetration in MEA were scaled back, which in turn forced distributors and resellers to raise prices to defend their margins. These headwinds led to declining shipments for many OEMs.

意味着Smartphone Unit Shipments Share, Q2 2022 vs Q2 2021

Source: Counterpoint Research Market Monitor, Q2 2022 Notes: Xiaomi includes POCO and Redmi; OPPO includes OnePlus; Figures may not add up to 100% due to rounding

The market leader,Samsung, grew YoY from a relatively low base in Q2 2021 when it faced COVID-19 disruptions at its Vietnam production facilities. The new and revamped Galaxy A-series devices have performed well and were among the best-selling devices during Q2. Samsung’s shipments are expected to grow in H2 with the upcoming launch of its new generation of foldables and as end-of-year sales approach.

TranssionGroup’s brands continued to take the biggest share of smartphone shipments in the MEA region. Transsion Group brands’ shipment share grew YoY, largely driven by a strong performance ofInfinixandTECNOdevices. Multiple stylish and feature-rich new launches, like Infinix’s Hot series and TECNO’s Pova and Spark series, helped the brands weather adverse market forces. On the other hand, as the asymmetric impact of inflationary pressures on the low and entry tiers mounted during the quarter,itel’s smartphone shipments declined 23% YoY in Q2. itel is in a tough spot with regard to rising component prices, an underwhelming product portfolio revamp and customers migrating to the more upmarket TECNO and Infinix devices.

Apple’s shipments also grew 2% YoY, largely due to better distribution and product availability in GCC countries. The iPhone 13 series has the best-selling premium devices in the region since its launch.OPPO,realme,vivoandXiaomisaw steep YoY declines in their Q2 shipments. The OEMs continue to struggle in establishing a foothold in the region, as weak distributor incentives and supply issues have plagued the brands throughout H1 2022. Furthermore, stiff competition from regional stalwarts Samsung and Transsion Group’s TECNO and Infinix has curtailed market share for the challenger brands. However, the ramping up of local production in Pakistan, specifically for OPPO, vivo and Xiaomi, could help ease supply issues in the region. But it is unlikely to have any substantial effect in 2022.

Despite the underwhelming market performance in the first half of the year, there are some reasons to be cautiously optimistic about the rest of the year. Though inflation has reached double digits in many countries across MEA, it is not a new phenomenon and most customers have experienced these episodes in the recent past. This has brought them the ability to adapt quickly to the new economic realities. Also, we noticed that the average selling prices (ASP) of smartphones are continuing to trend up in the region, suggesting increasing digitization and customers’ need for more sophisticated handsets. The easing of the global semiconductor shortage, which led to severe product availability issues for MEA in 2021, is also expected to help the market find a stronger footing once the economic issues subside.

Counterpoint Research’s market-leadingMarket Monitor,MarketPulse andModel Salesservices for mobile handsets are available for subscribing clients.

Feel free to contact us at press@www.arena-ruc.com for questions regarding our in-depth research and insights.

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

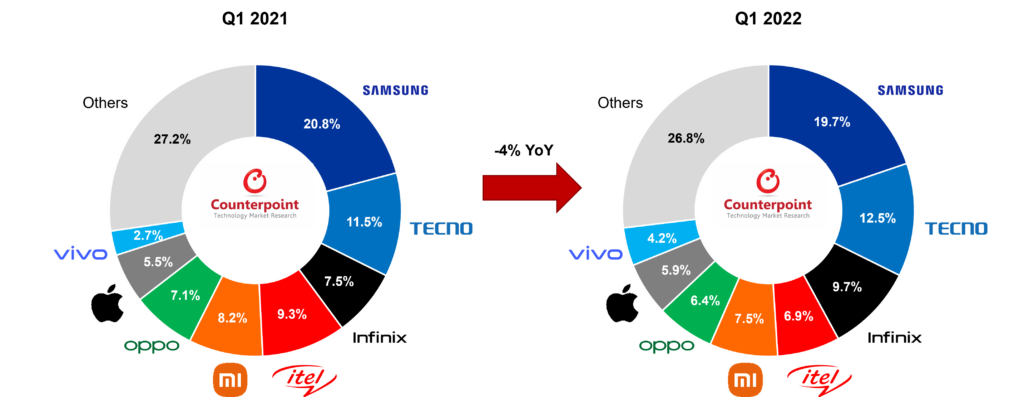

意味着智能手机sales retreated 4% YoY in Q1 2022, mainly due to macro concerns.

Samsung sales dropped YoY but saw their market share rebound from the lows of H2 2021 due to renewed popularity of low-to-mid range devices.

Transsion brands saw their first sales drop since the COVID-19 pandemic, mainly due to weakness in Africa’s lower-segment markets.

New Chinese entrants Xiaomi and OPPO had a resilient quarter as the supply situation improved.

London, Boston, Toronto, New Delhi, Hong Kong, Beijing, Taipei, Seoul – June 8, 2022

智能手机销量意味着(中东和非洲的a) region fell 3.7% YoY in Q1 2022, according to the latest research from Counterpoint’sMarket Pulse Service. Sales were expected to drop during Q1, which is typically a soft quarter, but demand was also dented by geopolitical worries elsewhere and increasing pressure on consumers due to commodity and food price increases.

意味着Smartphone Unit Sales Share, Q1 2022 vs Q1 2021

Source: Counterpoint Research Market Pulse, Q1 2022 Notes: Xiaomi includes POCO and Redmi; OPPO includes OnePlus; Figures may not add up to 100% due to rounding

Commenting on the performance of OEMs,Senior Research Analyst Yang Wangsaid, “Most key OEMs saw sales drop YoY, but this needs to be interpreted in the context of economic reopening in Q1 2021, which led to pent-up demand that manifested in an unusually high base effect. MEA leaderSamsungsaw sales and market share losses in Q1 2022, but this was a much more optimistic performance than what the numbers suggest. Despite lingering supply issues, Samsung’s new affordable A-series models proved to be popular in the region. Compared to other OEMs, the brand is best positioned in terms of supply chain and product mix, and we expect to see Samsung taking more market share from rivals in the next few quarters.”

“Transsionbrands saw their market share increase from 28% to 29% in Q1 2022, but they also saw a sales drop of 7.5% YoY during the quarter, their first sales drop since the beginning of the COVID-19 pandemic. This was mainly due to the weakness seen byitel,the brand that is skewed heavily towards entry-level, lower-income African customers. On the other hand,Infinixcontinued to grow strongly on the back of impressive performance of its mass-market models in the Hot and Smart series. Looking ahead, customer demand in Transsion’s home market Africa is a reason for worry. Local currency depreciation may also put Transsion’s price competitiveness under pressure.”

“XiaomiandOPPOwent through a tumultuous H2 2021 and are evidently still influenced by supply chain issues. But despite macro concerns, the two brands performed resiliently in Q1 2022. We expect their market share retreat to bottom out during the middle of the year.”

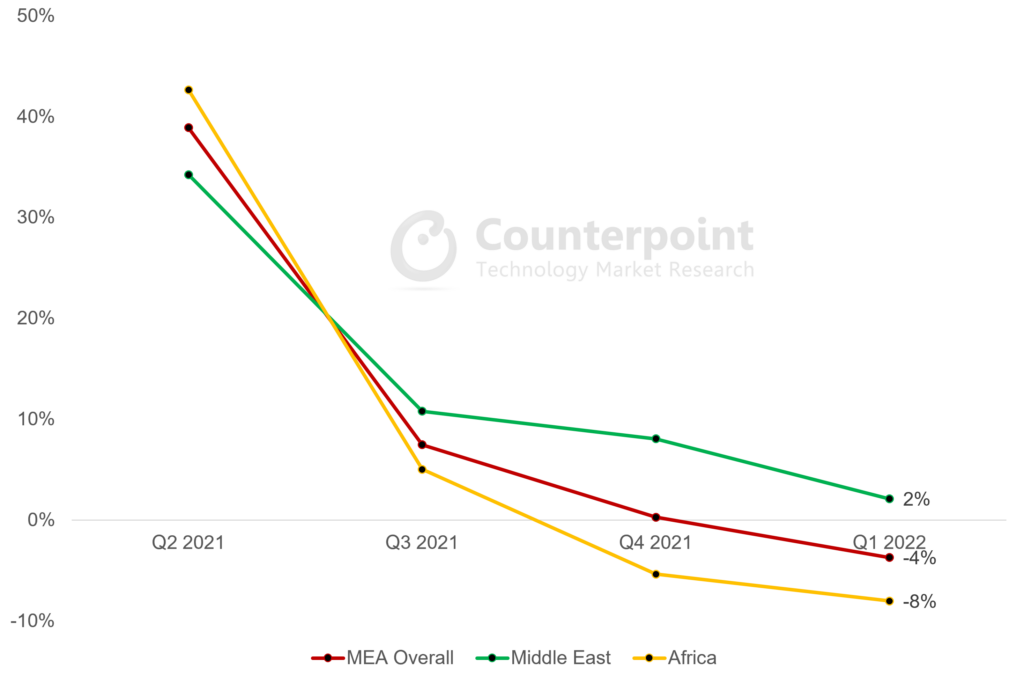

Source: Counterpoint Research Market Pulse, Q1 2022

While growth has inevitably flattened across the MEA market in recent quarters, it is important to emphasize the regional differences within. In Q1 2022, the Middle East market managed to grow despite the economic headwinds. On the other hand, Africa is becoming a point of concern, having underperformed since H2 2021.

Since the start of theRussia-Ukraine war,markets across the world have been pegged backby inflationary and foreign currency pressure. But the Middle East is an exception, with Gulf Cooperation Council (GCC) countries benefiting from increased oil revenues. The IMF has revised upwards its 2022 and 2023 GDP forecasts for the region by 1%. With the resumption of tourism, migrant population movements and business travel, the region’s smartphone market is poised to be the outperformer for the rest of 2022.

Weakness in Africa may persist throughout the year, as food price increases will force consumers to pause spending on big-ticket items like smartphones. At the same time, high levels of inflation are not foreign to most consumers in Africa. Consumer sentiment will certainly be hit, but drastic lifestyle changes are unlikely. And given the trend of urbanization, digitization and smartphone adoption across the continent, we can expect the African market to resume growth after the current situation eases.

Counterpoint Research’s market-leadingMarketPulse andModel Salesservices for mobile handsets are available for subscribing clients.

Feel free to contact us at press@www.arena-ruc.com for questions regarding our in-depth research and insights.

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

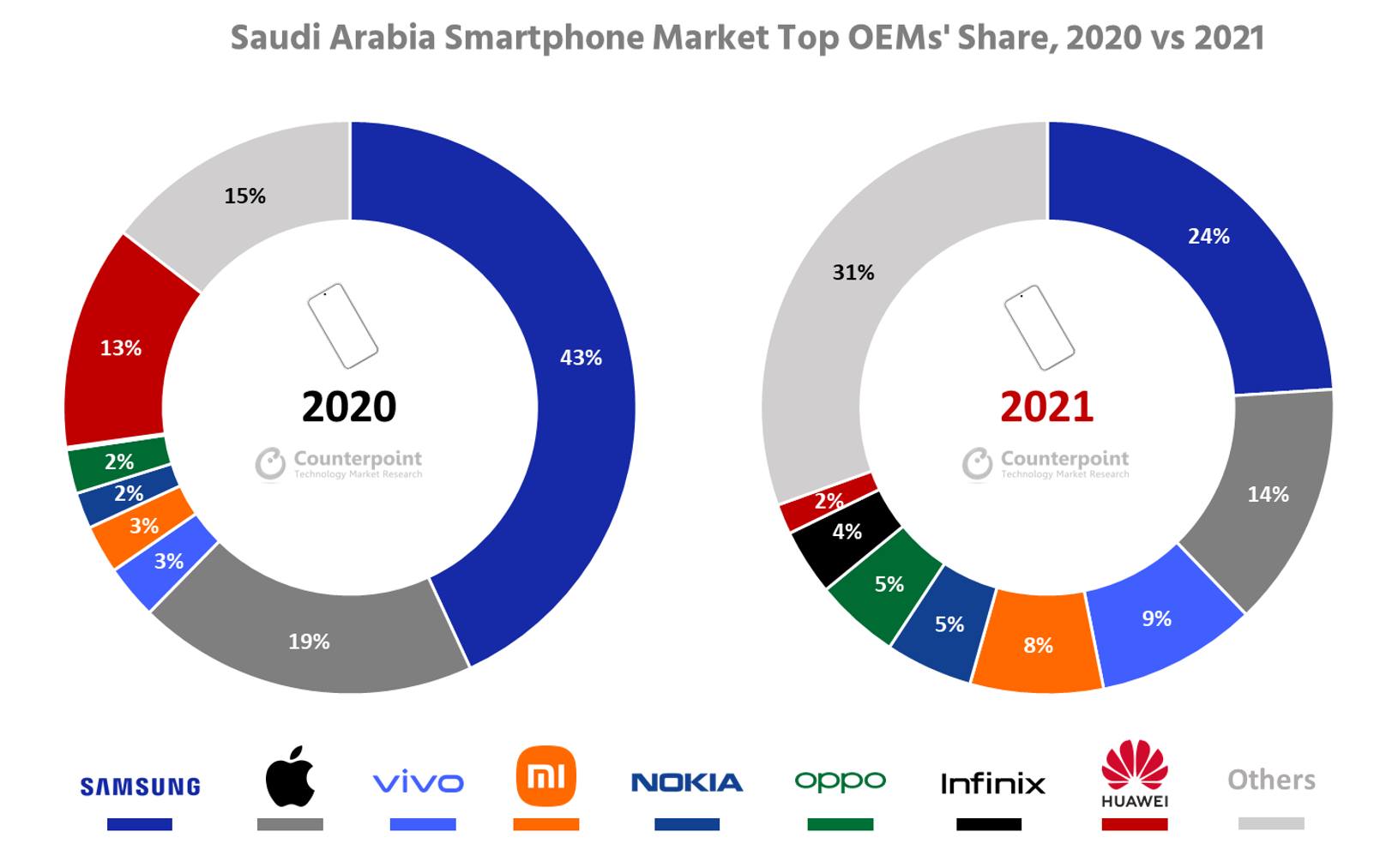

Saudi Arabia’s smartphone market grew 49% YoY in 2021, a 14% increase from the pre-pandemic 2019.

Samsung led the market despite losing share. Apple came in second.

Chinese OEMs’ share grew to 41% in 2021, capitalizing on Huawei’s exit.

5G smartphone sales penetration in Saudi Arabia grew to 35% in 2021. One in every three 5G phones sold was an iPhone.

New Delhi, Seoul, Hong Kong, Beijing, London, Buenos Aires, San Diego – March 31, 2022

Saudi Arabia’s annual smartphone sales grew 49% YoY in 2021 to cross the pre-pandemic level of 2019, according toCounterpoint Research’sGlobal Monthly Handset Sales Tracker. Post-COVID-19 recovery and pent-up demand were the key growth drivers. After a difficult 2020 that saw high COVID-19 rates and a struggling economy, the Saudi Arabia smartphone market benefitted from overall economic growth in 2021, which was driven by high oil exports, rising employment and falling inflation.

Commenting on the market dynamics,Senior Analyst Yang Wangsaid, “Saudi Arabia’s smartphone market benefitted fromimproving consumer demand due to a recovering economy and an increased pace of digitalization, partly induced by the COVID-19 pandemic. Furthermore, the market has gradually adjusted to the statutory 15% VAT increase from June 2020, which had dampened sales in 2020. Huawei’s exit threatened to hit growth in 2021, but Chinese brands like vivo, Infinix and Xiaomi were not only quick to step up, they also grew to increase the share of Chinese brands to 41% in 2021, compared to 29% in 2020.”

Source: Counterpoint Research Handset Model Sales, Jan 2022 Note: Figures may not add up to 100% due to rounding

Samsungled the Saudi Arabia smartphone market in 2021 despite a decline in its share due to supply issues and increasing competition.Applecame in second, with vivo andXiaomifollowing next. Xiaomi may have ended ahead of vivo if not for a weak Q4 due to supply woes.

Chinese OEMs like vivo and OPPO ramped up in 2021 and were able to capitalize on Huawei’s exit to grow their market share. Transsion group OEMs also saw modest success in a bid to expand their operations in the Middle East.

With its portfolio targeting the budget segment and new launches during the sales season, Infinix entered the top five rankings for the $200 and below price band in 2021.

Nokia took the fifth spot overall, clocking modest YoY growth after capitalizing on a revamped portfolio, consumer loyalty and improved availability during seasonal sales events.

5G smartphone sales also grew in 2021.复位arch Associate Ravyansh Yadavsaid, “While smartphone penetration continues to be a growth driver,5G smartphone penetration took off in 2021, growing from 7% in 2020 to 35% in 2021. Apple, Samsung and vivo were the 5G smartphone market leaders. 5G penetration reached its highest level ever at 44% in Q4 2021 driven by the launch of the iPhone 13 series. In 2021, one in every three 5G phones sold in Saudi Arabia was aniPhone. With 5G coverage in the country having crossed 70% in 2021 and operators nearing the end of their respective 5G deployment roadmaps, upgradation to 5G smartphones will be an important growth driver for the Saudi smartphone market in 2022 as well.”

While the distribution across price bands remained largely the same as in 2020, sales growth was driven by the $300 and below and $600 and above price segments in 2021. Sales in the $300 and below band grew 55% YoY in 2021 driven by new launches from OEMs and consumer upgrades. Sales in the entry tier also grew driven by the continued transition of consumers to smartphones. Overall, Samsung held the top spot in the price segment.

As incomes rose and inflation stabilized at low levels,sales in the premium segment($600 and above) grew 44% YoY, with Apple and Samsung grabbing more than 90% of the sales in the price band. Sales in this segment are, however, yet to cross the pre-pandemic level of 2019. With salaries expected to grow again in 2022, the premium segment in Saudi Arabia presents an opportunity for OEMs. Huawei’s exit has further opened an opportunity for the third spot in thepremium segment, which other OEMswill battle to capture.

As incomes and employment continue to grow, digital initiatives and e-commerce activity ramp, and 5G connectivity improves, the Saudi Arabia smartphone market is set to record another year of double-digit growth, albeit much lower than in 2021. Market growth will be dependent on supply and economic strains arising from the global semiconductor shortages, an unforeseen COVID event andthe currently unstable global political climate.

Notes:The analysis is based on wholesale ASPs; OPPO excludes OnePlus.

Please reach out to us at press(at)www.arena-ruc.com for press comments and enquiries.

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

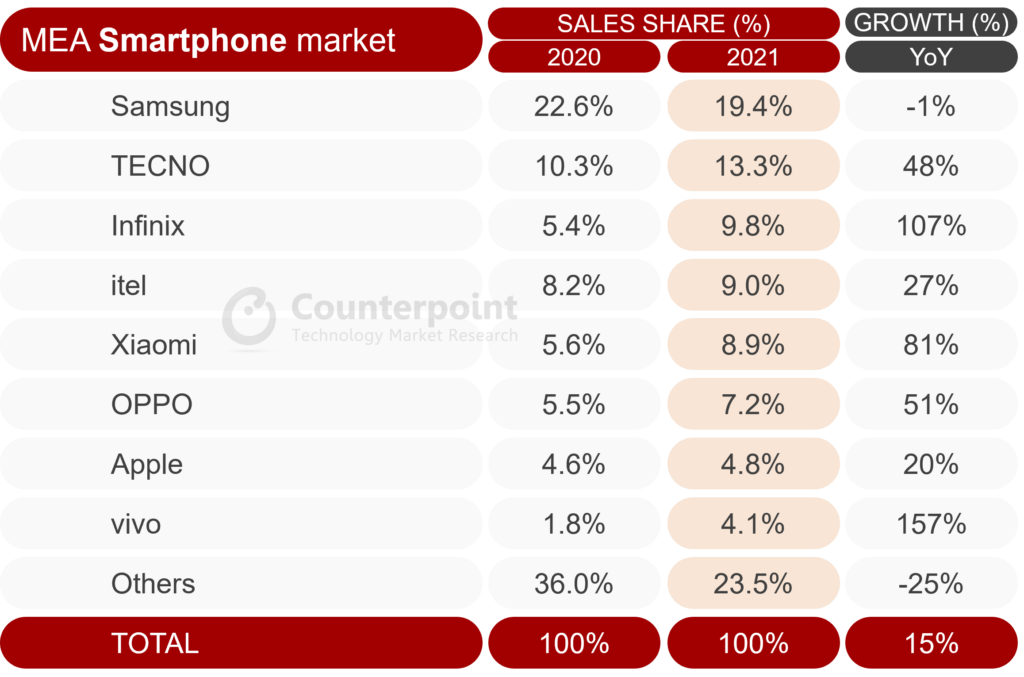

意味着智能手机sales grew 15% YoY in 2021, marking the best year ever for the market.

Samsung continued to top the market, though its lead was reduced due to supply chain and product availability issues.

Transsion brands accounted for 32% of the market. TECNO solidified its second position by capturing a market share of 13%. Its sales increased 48% YoY.

New Chinese entrants Xiaomi and OPPO performed well, but their growth slowed in the second half of the year due to supply issues.

London, Boston, Toronto, New Delhi, Hong Kong, Beijing, Taipei, Seoul – February 8, 2022

智能手机销量意味着(中东和非洲的a) region grew 15% YoY in 2021, according to the latest research from Counterpoint’s Market Pulse service. After crossing the post-pandemic phase of pent-up demand, smartphones remained in high demand throughout the year, despite the market facing many difficulties, including macroeconomic worries, supply chain issues and the emergence of new COVID-19 variants. Growth was seen across all areas and consumer groups, underpinning the accelerating adoption of digital services in the region.

意味着Smartphone Unit Sales Share, 2021 vs 2020

Source: Counterpoint Research Market Pulse, Q4 2021 Notes: Xiaomi includes POCO and Redmi; OPPO includes OnePlus; Figures may not add up to 100% due to rounding

Commenting on the performance of OEMs,Senior Research Analyst Yang Wangsaid, “All major brands except Samsung saw annual volume growth of more than 20%.Samsungwas hampered throughout the year, having to deal with product availability issues due to factory closures in Southeast Asia and component shortages. However, the company kept its number one position in the MEA after seeing a recovery during the Q4 shopping season. It is expected to face a less dramatic 2022.”

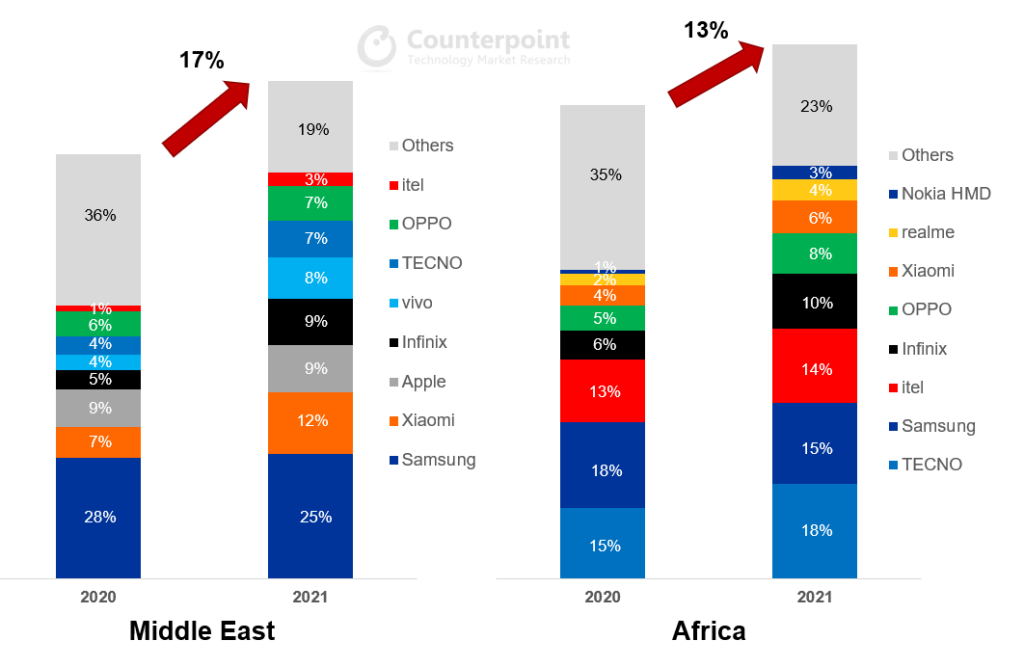

“TheTranssionbrands, namelyTECNO,Infinixanditel, continued to gain strength to record another fantastic year. The three brands together accounted for 32% of the smartphones sold in 2021, up from 24% in the previous year. Mass-market models from TECNO and Infinix have been a big hit, while more pricey models have also been positively received. More importantly, the Transsion brands have found success away from the African home market. Their market share in the Middle East almost doubled in 2021, while sales increased 127%.”

“XiaomiandOPPOstarted the year strongly due to substantial investments in channel penetration and product availability. However, both were hit hard in the second half of the year by component shortages. While the situation has improved somewhat, the two brands are likely to take a more careful approach in the first half of 2022.”

Smartphone Unit Sales Breakdown Within MEA, 2021 vs 2020

Source: Counterpoint Research Market Pulse, Q4 2021 Notes: Xiaomi includes POCO and Redmi; OPPO includes OnePlus; Figures may not add up to 100% due to rounding

虽然是地区经济增长明显,the Middle East did the heavy lifting both in terms of volume and value. Governments in both Africa and the Middle East did generally well in combating the pandemic, but vaccination rates were far higher in the Middle East. Africa was also hamstrung by the emergence of new COVID-19 variants. This meant that the Middle East saw a quicker reopening of the international travel and services sectors. Both Africa and the Middle East benefitted from the commodities boom, but Africa faced higher inflationary pressures due to governments being in worse fiscal positions during the pandemic. As such, smartphone affordability was a bigger issue for Africa, especially in the lower-priced segment, as lower-income consumers struggled more. Despite this, smartphone market fundamentals remain strong across the MEA as consumers continue to adopt digital services.

Counterpoint Research’s market-leadingMarket PulseandModel Salesservice for mobile handsets is available for subscribing clients.

Feel free to contact us at press(at)www.arena-ruc.com for questions regarding our in-depth research and insights.

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

意味着智能手机shipments grew 1% YoY and 7.5% QoQ in Q3 2021. The quarter was the best Q3 on record, registering shipments of 46.5 million devices.

Samsung managed to reverse its decline and achieved 8% QoQ growth. It continued to hold the top spot in the region with a 21% market share.

TECNO solidified its second position by capturing a market share of 14%. Shipments increased by an impressive 22% QoQ.

New Chinese entrants saw mixed fortunes with OPPO and vivo continuing to gain market share and Xiaomi falling 31% QoQ due to inventory management and supply issues.

London, Boston, Toronto, New Delhi, Hong Kong, Beijing, Taipei, Seoul – November 23, 2021

Smartphone shipments in the MEA (Middle East and Africa) region grew 1% YoY and 7.5% QoQ in Q3 2021, according to the latest research from Counterpoint’s Market Monitor service. Despite pent-up demand fading in the rear-view mirror, and the ongoing global component shortages, the smartphone market continues to strengthen as digital services, connectivity and mobile money become ever more important.

意味着Smartphone Shipments, Q3 2021

Source: Counterpoint Research Market Monitor, Q3 2021 Note: Xiaomi includes POCO and Redmi; OPPO includes OnePlus

Commenting on the overall market dynamics,Senior Research Analyst Yang Wangsaid, “The MEA smartphone market continues to trend upwards. After the passage of the re-opening related trade, a genuine positive shift in consumer perception towards mobile internet became the key catalyst for smartphone demand. As the market marched to the best Q3 on record, there was more competition between the big players and choices for consumers than ever.”

Commenting on the OEM dynamics, Wang further said, “Among the key OEMs in the MEA smartphone market, all except Samsung and Xiaomi recorded YoY gains.Samsungrebounded from Q2’s lows, as product availability issues were mostly resolved. We expect Samsung to further strengthen its hold at the top of the MEA smartphone table heading into the busy Q4 shopping season.”

“The Transsion brands, namelyTECNO,itelandInfinix, have been the big winners since the pandemic. Cumulatively, the company increased its market share from 19% in Q3 2020 to 30.5% in Q3 2021 on the back of strong sales in Africa and successful ventures in other regions. TECNO did especially well in the latest quarter as it continued to strengthen its leadership in the low-mid price segment, while its expanded product portfolio managed to tap into more segments.”

“OPPOandvivohave also made substantial gains over the past year, as the two brands continue to double down on efforts to improve channel penetration and device availability.Xiaomi, which enjoyed tremendous growth in the past year, fell hard in Q3 as it faced severe component shortages and inventory management issues.”

意味着Smartphone Average Selling Price ($), 2019-Q3 2021

Source: Counterpoint Research Model Sales service

It should be noted that as the big brands compete to win market share in the fledgling MEA smartphone market, the average selling price (ASP) has risen over the past three years as well, accelerating at the fastest pace in 2021. This is down to three reasons: first, the outperformance of premium brands such as Apple and Samsung, whose iPhone 12 and 13 series and Galaxy Z Fold 3 and Flip 3 series have proven to be especially popular in the more developed GCC countries; second, the entrance of the new Chinese brands, whose competitively priced medium segment handsets have convinced customers to upgrade; and third, Transsion, which dominates the lower price segment in sub-Sahara Africa, has seen early success for its branding and portfolio upgrade, delivering more sophisticated devices to entry-level users. We expect this trend to continue in the future, allowing big handset makers to gain not only market share but also profitability in the medium to long term.

Counterpoint Research’s market-leadingMarket MonitorandModel Salesservice for mobile handsets is available for subscribing clients.

Feel free to contact us at press(at)www.arena-ruc.com for questions regarding our in-depth research and insights.

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

In order to access Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not. Personal Information When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time. In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

这个网站是对位的财产和我s protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company. – Passwords are for user’s individual use – Passwords may not be shared with others – Users may not store documents in shared folders. – Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified. Accuracy of Information: While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links: This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience. This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. 饼干可能为了确定你和德termine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.

Looking at individual brands, Samsung, TECNO andApplewere the biggest winners.Samsung’s rebound can be attributed to the lower-pricedGalaxyA series’ strong sales, while new 5G and premium-end models also did well.TECNO, and sister brandInfinixto some extent, performed very well due to better economic conditions, particularly for lower income groups, and aggressive market entries in the Middle East. TECNO andInfinix’ssuccesses, however, can be partly attributed to the cannibalization ofitel’s market share. Lastly,Applehad an outstanding quarter to round off a very strong iPhone 14 series cycle. TheOEMmanaged to increase penetration in key Middle East markets with the higher-priced Pro and Pro Max models getting good reception.

Looking at individual brands, Samsung, TECNO andApplewere the biggest winners.Samsung’s rebound can be attributed to the lower-pricedGalaxyA series’ strong sales, while new 5G and premium-end models also did well.TECNO, and sister brandInfinixto some extent, performed very well due to better economic conditions, particularly for lower income groups, and aggressive market entries in the Middle East. TECNO andInfinix’ssuccesses, however, can be partly attributed to the cannibalization ofitel’s market share. Lastly,Applehad an outstanding quarter to round off a very strong iPhone 14 series cycle. TheOEMmanaged to increase penetration in key Middle East markets with the higher-priced Pro and Pro Max models getting good reception.

According to Counterpoint Research, Transsion’s smartphone sales volume grew 3% YoY in the first half of 2023 and 17% YoY in Q2 2023 as demand for TECNO

According to Counterpoint Research, Transsion’s smartphone sales volume grew 3% YoY in the first half of 2023 and 17% YoY in Q2 2023 as demand for TECNO Much of Transsion’s financial successes can be attributed to its continued commitment to entering new markets. In Q2 2023, Africa accounted for 57% of Transsion’s smartphone sales volume, a net drop of 8% from a year ago. Outside Africa, Transsion smartphone sales grew 35% in Q2 2023, most notably in Latin America, Eastern

Much of Transsion’s financial successes can be attributed to its continued commitment to entering new markets. In Q2 2023, Africa accounted for 57% of Transsion’s smartphone sales volume, a net drop of 8% from a year ago. Outside Africa, Transsion smartphone sales grew 35% in Q2 2023, most notably in Latin America, Eastern

沙特阿拉伯oem fo智能手机出货量的前5位r Q1 2021, Q1 2022, Q1 2023

沙特阿拉伯oem fo智能手机出货量的前5位r Q1 2021, Q1 2022, Q1 2023

Source: Counterpoint Research Market Monitor, Q4 2022

Source: Counterpoint Research Market Monitor, Q4 2022