Counterpoint is attending the IoT Tech Expo Europe on 27thSeptember, 2023

Our Associate DirectorMohit Agrawalwill be attending theIoT Tech Expo Europe, 2023. You can schedule a meeting with him to discuss the latest trends in the technology, media and telecommunications sector and understand how our leadingresearchandservicescan help your business.

When:September 26th – September 27th

Where:Rai, Amsterdam

About the event:

IoT Tech Expo is the leading event for IoT, Digital Twins & Enterprise Transformation, IoT Security IoT Connectivity & Connected Devices, Smart Infrastructures & Automation, Data & Analytics and Edge Platforms. With a myriad of groundbreaking exhibits, expert-led discussions, and networking opportunities, the IoT Tech Expo is your gateway to discovering the IoT landscape.

Click here(or send us an email at contact@www.arena-ruc.com) to schedule a meeting with them.

Counterpoint Research will be joiningIndustry of things World Europeas Media Partners. As part of this collaboration, our Associate DirectorMohit Agrawalwill be speaking about security and privacy considerations when managing IoT connectivity, and how do CMPs assist in enforcing security measures. You can schedule a meeting with him to discuss the latest trends in the IoT sector and understand how our leading research and services can help your business.

Topic: What are the security and privacy considerations when managing IoT connectivity, and how do CMPs assist in enforcing security measures?

At the Industry of Things World Europe more than 450 experts, decision-makers and providers from the industry will discuss use cases and business strategies from the Industry 4.0 universe. Latest technological trends, opportunities and risks as well as direct practical examples from the manufacturing industry – the Industry of Things World is designed to evaluate and discuss your technology strategy for a scalable, secure and efficient IIoT implementation around your production & your products. Don’t miss the opportunity to meet all relevant IIoT stakeholders under one roof. We look forward to welcoming you in Berlin! Your Industry of Things World Team.

The growing IoT ecosystem has brought forth its own set of challenges. One such challenge is permanent roaming.

虽然许多国家允许永久漫游无ut significant constraints, some big countries have implemented limitations on this practice.

There are multiple ways to circumvent the problem of permanent roaming. These includeeSIM, Multi-IMSI, aggregator platforms, and dynamic network selection algorithms.

The Internet of Things (IoT) has revolutionized the way we interact with the world around us. From smart homes to industrial automation,IoT在加强ef设备发挥着关键的作用ficiency and convenience. However, the growing IoT ecosystem has brought forth its own set of challenges. One such challenge is permanent roaming, a phenomenon that has gained significance due to the global nature ofIoTdeployments. In this blog, we will delve into the concept of permanent roaming for IoT, discuss the challenges it poses, and explore potential solutions.

Understanding permanent roaming for IoT

Permanent roaming in the context of IoT refers to the practice of utilizingcellularconnectivity across different geographical locations on a consistent basis. Unlike traditional mobile phones, which might roam temporarily when users travel, IoT devices often need to maintain connectivity across various regions for extended periods. This is a fundamental requirement for IoT devices used in logistics, remote monitoring,agricultureand other activities.

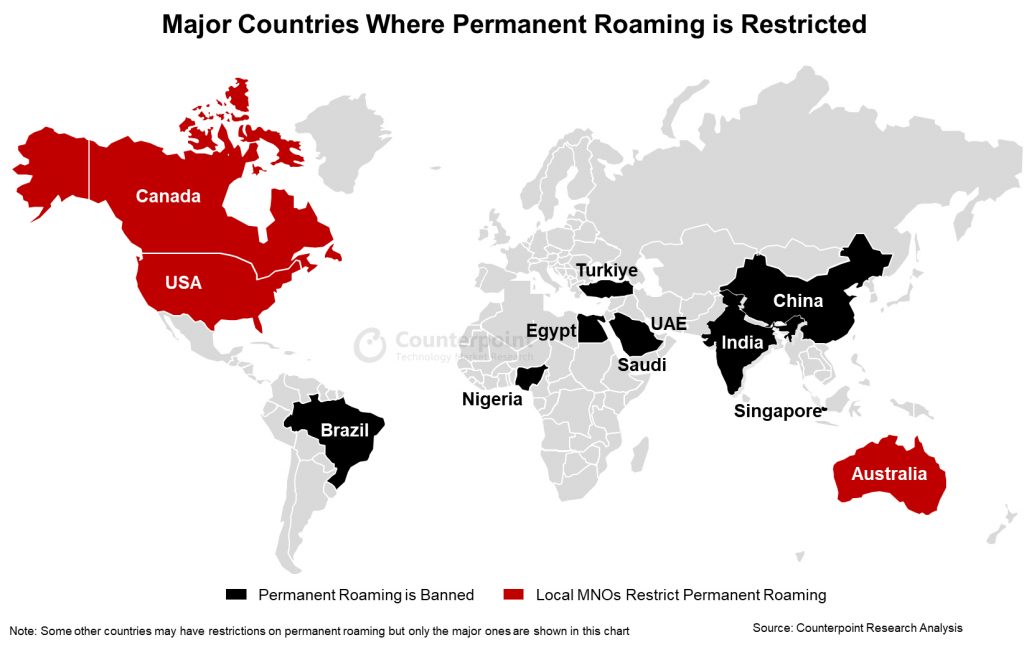

虽然许多国家允许永久漫游无ut significant constraints, some big countries have implemented limitations on this practice. The map below shows countries where permanent roaming is banned and those where local carriers have imposed restrictions.

Countries that prohibit permanent roaming includeIndia, China, Brazil, Saudi Arabia, Egypt, Nigeria, Turkiye (formerly Turkey), UAE and Singapore. Besides, mobile operators in the US, Canada and Australia have imposed restrictions on permanent roaming within theirnetworks, effectively imposing a ban on this practice in these countries. Remarkably, these 12 countries collectively cover more than 50% of the world’s population and account for well over three-quarters of the IoT market.

IoT devices are typically deployed on a global scale, leading to a complex scenario where these devices are connected to multiple mobile network operators (MNOs) across different countries. Imagine an electric car company that markets its vehicles across various regions. In countries where permanent roaming is not allowed, the company must procure local connectivity. This situation presents a host of challenges that ripple through the operational landscape:

Complex network management:Handling connections to multiple networks becomes really complex. Each network might have different prices, coverage areas and technical needs. The process of harmonizing such distinct facets is likely to be intricate and time-consuming.

Dealing with many partners:The company needs to work with different network partners. This means making deals, managing money and ensuring good service quality across networks. Besides, multiple networks means multiple bills and contracts. All of these tasks together can become very complicated and hard to manage as this activity is not core to the business.

Higher costs:Because of the rules against permanent roaming, the company has to pay more money to set up connections in each country. This extra cost can make things difficult and might affect how much the company can grow.

Less flexibility:Without the ability to use permanent roaming, the devices might not work as well when they move between countries. This can be a problem for customers who expect a consistent experience.

More planning needed:Since the company can’t rely on the same connection everywhere, it needs to plan ahead. This can slow things down and make expansion harder. There could be issues related to data sovereignty and compliance that may require additional planning.

Solutionsforpermanent roaming

There are multiple ways to circumvent the problems associated with permanent roaming. However, it is critical to select a managed service provider that has tie-ups with local MNOs/MVNOs. Alternatively, direct MNO relationships can be managed using aggregator connectivity management platforms.

eSIM (embedded SIM):eSIMtechnology is a game changer in the IoT landscape. It enables devices to have programmable SIM cards that can be remotely provisioned over the air. With eSIM, IoT devices can switch between different MNOs without requiring a physical SIM card replacement, thus simplifying the management of connectivity. UsingeSIM, it is possible to switch between a local profile and multiple roaming profiles every 90 days to avoid permanent roaming. Many managed service providers have this workaround to avoid permanent roaming. The new IoT eSIM specifications will further simplify the provisioning and orchestration of connectivity.

Multi-IMSI (International Mobile Subscriber Identity):Multi-IMSI solutions allow a single physical SIM card to have multiple IMSIs from different MNOs. This enables the device to seamlessly switch between networks while maintaining a single SIM card. By intelligently selecting the optimal IMSI based on factors like network quality and cost, Multi-IMSI solutions optimize connectivity and reduce operational complexities. However, the managed service provider needs to have a local presence or tie-ups.

Aggregator platforms:Aggregator connectivity management platforms (CMPs) act as intermediaries between IoT device owners and various MNOs. These platforms offer a unified interface for managing connectivity, provisioning,billing, and reporting across multiple networks. By consolidating these tasks, aggregator platforms simplify the management of permanent roaming for IoT devices. A new set of aggregator CMPs like IOTM and ConnectedYou is targeting enterprises instead of carriers to solve the problem of managing multiple networks.

Some of the aggregator platforms offer Dynamic Network Selection Algorithms. Smart algorithms can be implemented in IoT devices to dynamically select the most suitable network based on parameters such as signal strength, latency and cost.

Conclusion

With the IoT landscape continuing to expand globally, the challenges associated with permanent roaming are becoming more pronounced. However, with the advent of innovative solutions such aseSIM, Multi-IMSI, aggregator platforms, and dynamic network selection algorithms, these challenges can be effectively mitigated. These solutions not only simplify the management of connectivity but also enhance cost-effectiveness and operational efficiency for IoT deployments. The key is to find the right managed services partner, which has a platform that enables easy management of connectivity.

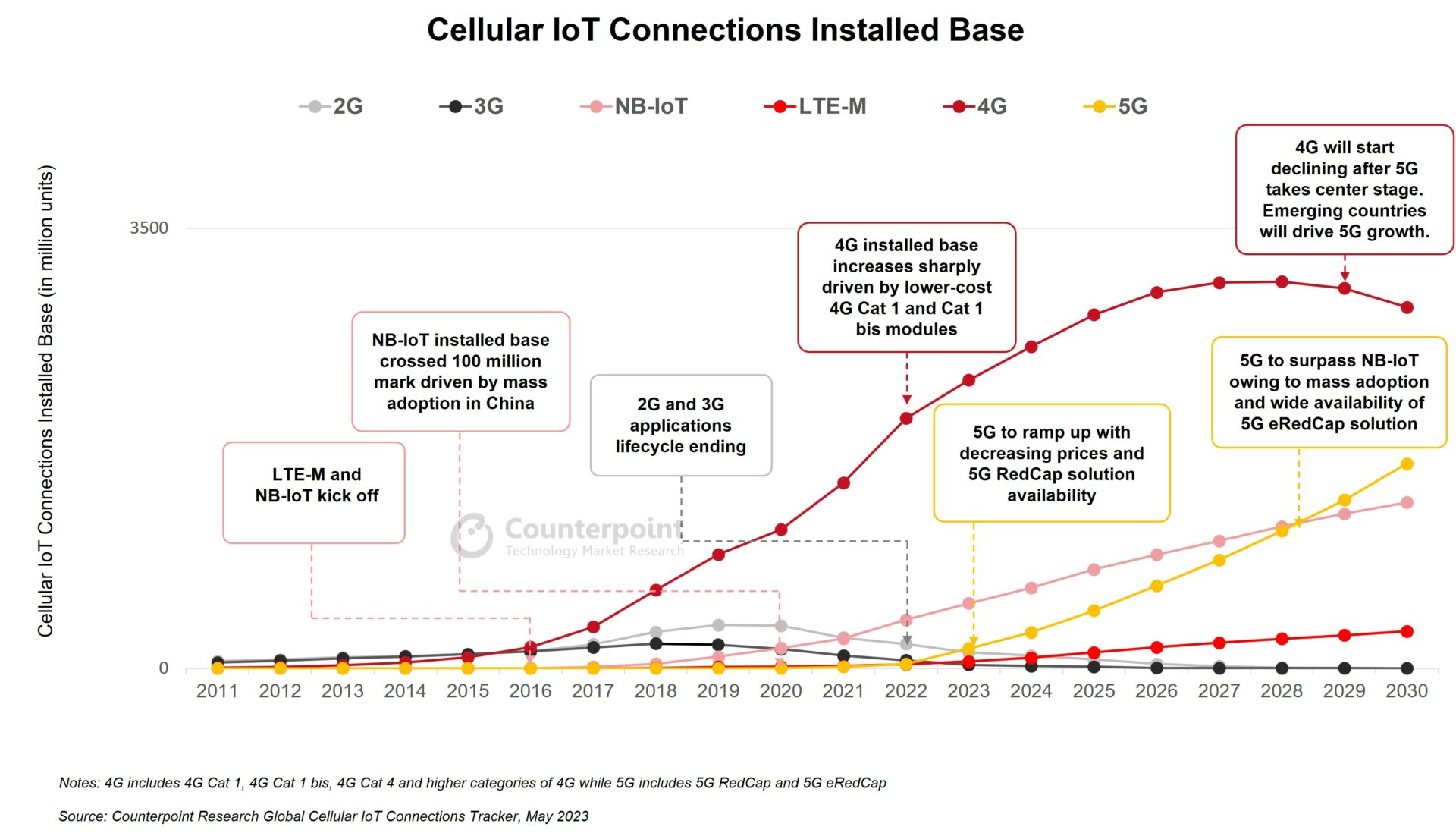

Global cellular IoT connections grew 29% YoY to reach 2.7 billion in 2022 with 4G continuing to grow its majority share.

China held more than two-thirds of total cellular IoT connections in 2022, followed by Europe and North America.

NB-IoT dominates in China, while LTE-M is preferred in Australia, Japan and North America; Europe supports both.

4G and NB-IoT are the most preferred technologies for cellular IoT applications.

5G is nascent as module prices and breadth of applications reflect early-stage dynamics.

IoT growth drivers are shifting, with the enterprise and transformation initiatives key in propelling IoT connections forward.

San Diego, Buenos Aires, London, New Delhi, Hong Kong, Beijing, Seoul – June 12, 2023

Global cellular IoT connections grew strongly at 29% YoY to reach2.7 billionin 2022, according to Counterpoint’s latestGlobalCellular IoT Connections Trackerreport. They are expected to grow at a CAGR of 10.8% to reach an installed base of over6 billionby 2030. China held more than two-thirds of total cellular IoT connections in 2022, followed by Europe and North America.

Amid the challenges faced by various industries, such as inflation,macroeconomicheadwinds and supply chain constraints, the cellular IoT market has experienced remarkable growth fuelled by thedigital transformationinitiatives undertaken by various industry applications like smart meters, automobiles and asset tracking in particular. Cellular IoT connectivity has played a significant role in enhancing productivity, streamlining operations, minimizing downtime, automating processes and generating cost savings for industries. The COVID-19 outbreak unexpectedly proved beneficial for enterprise IoT players, accelerating their digital transformation efforts.

Commenting on the cellular IoT connectivity technology dynamics,SeniorResearch AnalystSoumen Mandalsaid, “At the end of 2022, 4G and NB-IoT together accounted for nearly 90% of the installed base of cellular IoT connections. 4G emerged as the most preferred technology for cellular IoT connections after surpassing 2G and 3G-based IoT connections in 2016. NB-IoT has gained significant popularity in China, while Japan, Australia and North America prefer LTE-M technology for lower-end applications. Europe has adopted a combination of NB-IoT and LTE-M, supported by roaming services offered by most operators.

In recent times, 4G Cat 1 bis technology has gained significant popularity over NB-IoT due to its superior performance. Applications such asPOS, telematics andsmart metersare increasingly adopting this technology on a larger scale. The rising shipments of devices based on 4G Cat 1 and 4G Cat 1 bis technologies are contributing to the stagnant market growth of NB-IoT.

5Gis still nascent but we expect 5G-based applications to pick up as the module ASP (average selling price) drops to sub-$100 and more 5G RedCap-based solutions become available in the market. The introduction of5G RedCapand5G eRedCapwill play a crucial role in driving mass adoption of 5G, particularly in developing and underdeveloped countries.”

Commenting on the market outlook,Research Vice PresidentNeil Shahsaid, “The global cellular IoT connections installed base is expected to surpass 6 billion by 2030 with aCAGR of10.8%. The growth will be mainly driven by cellular connectivity adoption across various sectors such as utilities, automotive, industrial, retail and healthcare. Unlike the previous decade, where consumer devices like smartphones and PCs played a significant role in driving cellular connections, this decade will see a shift towards cellular connections being propelled by thedigital transformationinitiatives undertaken by enterprise IoT payers. The widespread adoption of cellular connectivity will also contribute to a further reduction in prices for cellular-connected devices, making them more competitive against alternative non-cellular connectivity technologies like LoRa, Sigfox and Wi-SUN. Over the past year, the cellular IoT industry has witnessed many consolidations, includingTelit’s acquisitionof Thales’ cellular IoT business, Semtech’s acquisition of Sierra Wireless, and Aeris Communications’ acquisition of Ericsson’s IoT accelerator and connected vehicle cloud business. As the cellularIoT module marketcontinues to mature, we can expect moreconsolidationsaimed at providing improved solutions and maintainingcompetitivenessagainst other non-cellular connectivity technologies.”

随时与我们达成press@www.arena-ruc.com for questions regarding our latest research and insights.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the technology, media and telecom (TMT) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

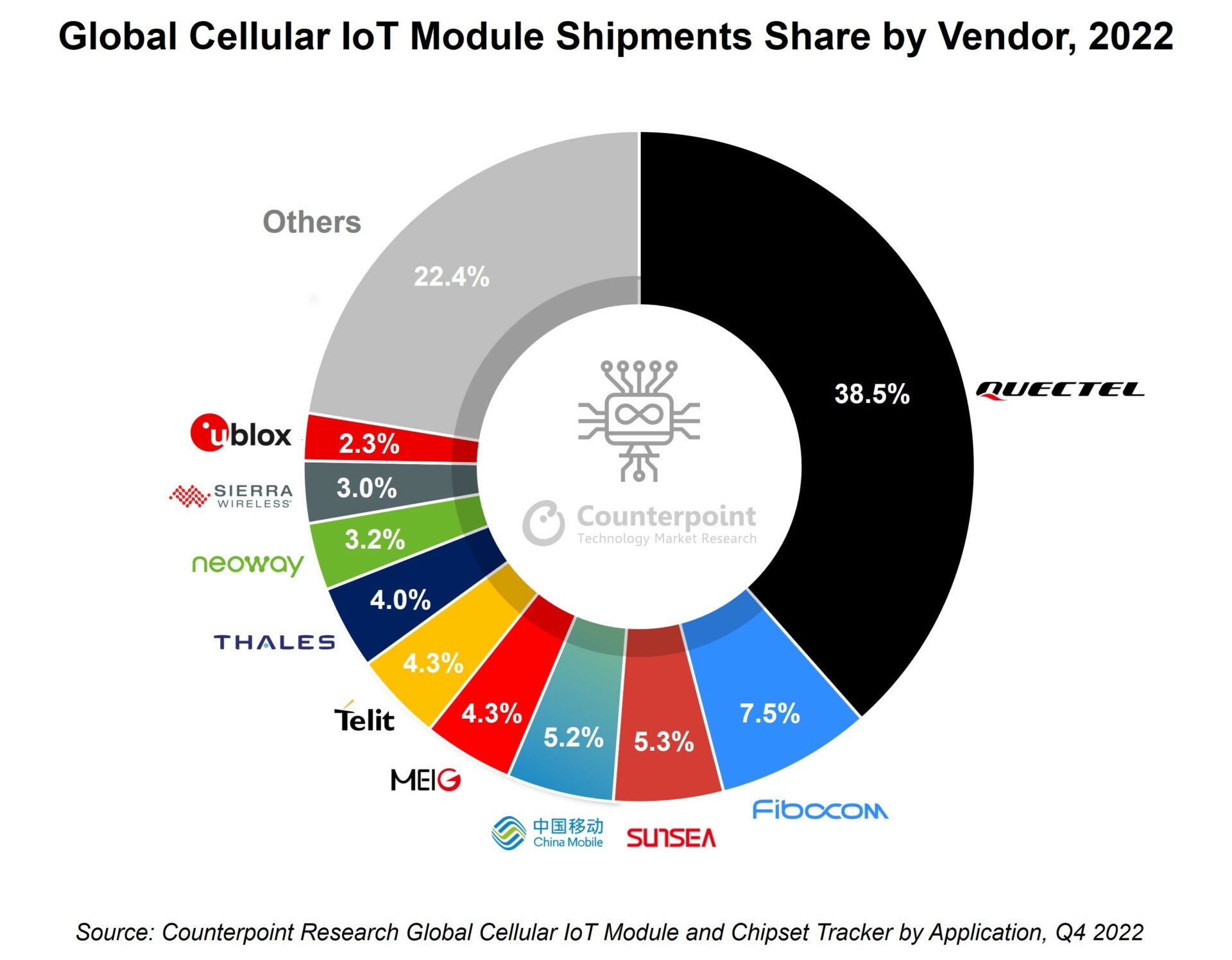

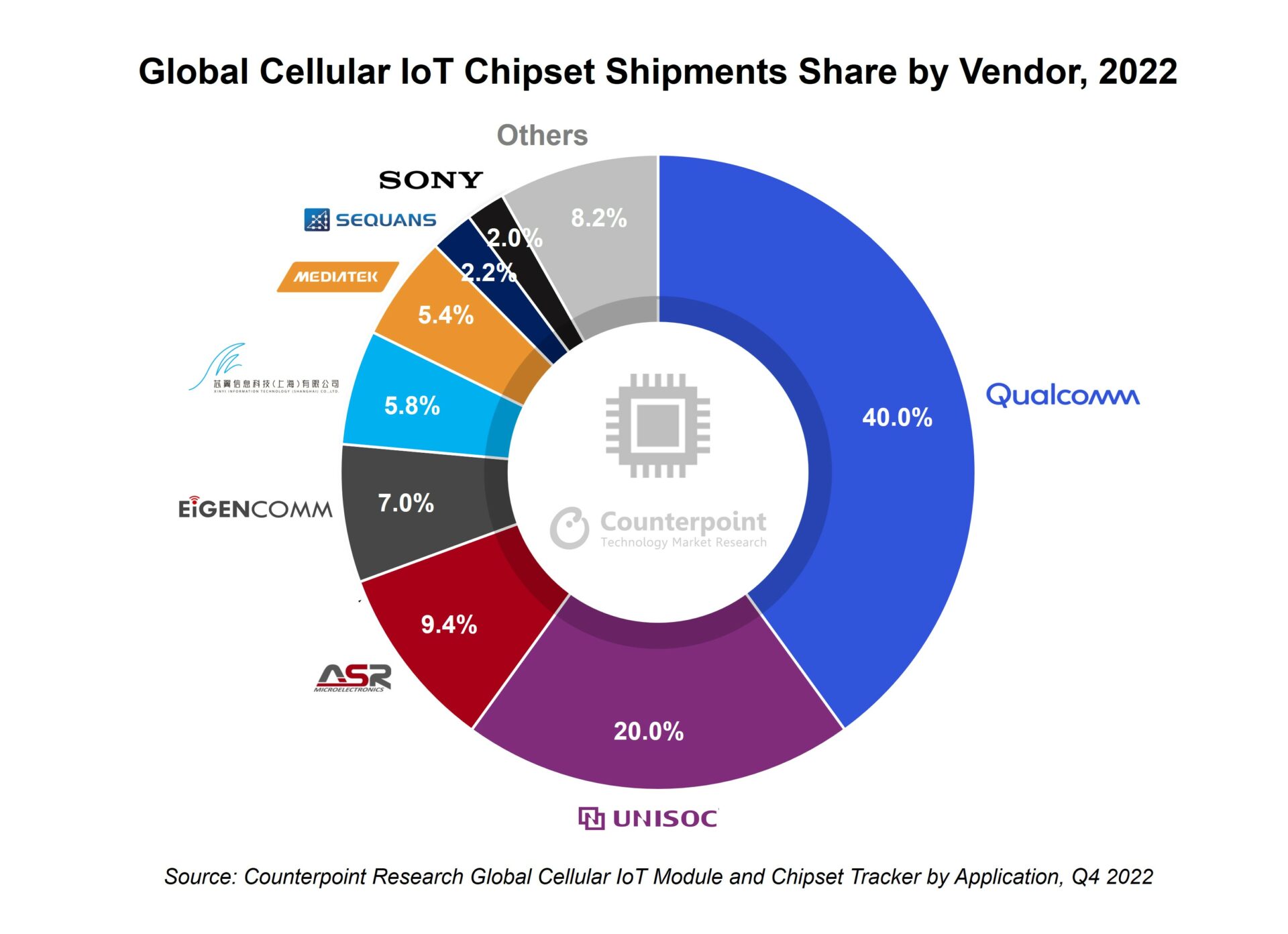

Quectel and Qualcomm dominated the cellular IoT module and chipset markets, respectively.

NB-IoT is still popular among technologies but is expected to lose some market share to 4G CAT1.bis in 2023.

5G adoption to get a boost in 2024 if ASP declines to sub-$100 and 5G RedCap-based solutions become available.

China continues to lead IoT module market, followed by North America and Western Europe.

San Diego, Buenos Aires, London, New Delhi, Hong Kong, Beijing, Seoul – March 29, 2023

Global cellular IoT module shipments grew 14% YoY in 2022 to register record high annual volume, despite macroeconomic headwinds, according to Counterpoint’s latestGlobal Cellular IoT Module and Chipset Tracker by Applicationreport. The resumption of smart meter implementation, ongoing retail POS upgrades, intelligentasset tracking和连接汽车由于持续增长progress in electrification and autonomous capabilities were some of the key drivers for the double-digit percentage growth in demand for IoT modules.

Chinacontinued to lead the global cellular IoT module market in terms of demand, followed byNorth AmericaandWestern Europe. Meanwhile,Indiawas the fastest growing market, followed by Latin America and North America. Although India has a smaller base, it has immense potential.Eastern Europewas the only region that registered a decline due to the prolonged Ukraine-Russia war.

Commenting on the competitive dynamics among cellular IoT module OEMs,Senior Research AnalystSoumen Mandalsaid, “In 2022, Quectel was the top cellular IoT module player inChina, the world’s largest market for these components. Meanwhile, China Mobile and Fibocom captured second and third place, respectively, enjoying their tremendous scale in the domestic market. Outside of China, Quectel remained the leader followed by Telit and Thales which have merged and will commence operations as a new brand,Telit Cinterion,starting Q1 2023.

Quectelincreased its focus in the consolidating automotive (NAD module)段,2022年获得多个设计获胜with major automakers. The competition in the NAD module market is intensifying as the industry transitions to 5G connectivity. With every transition of cellular technology, we have seen the market consolidate as it becomes increasingly challenging to serve the automotive segment, which requires heavy customization but garners a lower margin.

China Mobile, the world’s largest CSP and IoT connectivity player, is becoming more vertically integrated by leveraging its massive scale to capture maximum value. It has the potential to break into the top three global cellular IoT module rankings this year. However, the company primarily operates in China and will need to expand into other verticals and markets via a robust partnership model to maintain its momentum.”

Commenting on the IoT cellular connectivity chipset player dynamics,Associate DirectorEthan Qisaid, “Qualcommcontinued to dominate the cellularIoT chipsetmarket in 2022 with nearly 40% shipments share. Qualcomm strengthened its position in the LTE CAT 4 and higher technologies while also maintaining a dominant position in the 5G market. Qualcomm recently launched its latest 4G CAT1.bis chipset, QCX216, to compete head-on with the LTE CAT1.bis leaders UNISOC and Eigencomm.

Qiadded, “In 2022, UNISOCandASRmaintained their second and third positions due to strong adoption of the fast-growing LTE CAT1.bis and CAT 1 based modules, respectively. During the year, two new players from China,EigencommandXinyi Semiconductor,broke into the top five cellular IoT chipset vendor rankings, filling the gap left by Hisilicon. Eigencomm focuses on NB-IoT and 4G CAT1.bis applications while Xinyi Semiconductor focuses on NB-IoT chipsets, both being low-cost but high-volume segments.”

Commenting on the technology landscape,Mandaladded, “During 2022,NB-IoTremained the most popular LPWA IoT connectivity technology followed by the fast-growing 4G CAT 1 and 4G CAT 4 modules. Together, these contributed to 60% of the total IoT module market. For most of 2022, China was under lockdown due to the resurgence of COVID-19 which drove greater demand for products such as smart door locks, digital thermometers and wearables, mostly powered by NB-IoT.

NB-IoT saw strong adoption in China but has been less popular outside the country. In contrast,4G CAT.1bishas been gaining traction globally and has the potential to be an alternative to several NB-IoT and existing 2G/3G applications such as smart meters. However,5Gsaw slower adoption in IoT than in smartphones last year due to the higher module costs. The key initial 5G applications are PCs, CPEs and some industrial/enterprise applications.

We believe 5G will enter the mainstream market once the module ASP breaks the sub-$100 barrier and receives a further boost from the5G RedCapcommercialization in coming years.”

Commenting on the IoT market outlook for 2023,Associate DirectorMohit Agrawalsaid, “Global cellular IoT module shipments (including NAD modules) are expected to register robust growth of19%YoY in 2023. The growth of IoT module shipments in the high-value industrial segment will be key for the IoT projects that have struggled to move beyond the pilot stage and for companies that are focusing more on ROI in a tough macroeconomic environment. Nevertheless, shipments of IoT modules for thesmart meter,point of sale(POS) and theautomotivemarkets are expected to continue seeing strong growth, which will offset a slowdown in other segments.”

The market has been undergoingconsolidationacross theIoTvalue chain from module players andconnectivitymanagement to IoTplatformplayers. This has highlighted the importance of scale, choosing the right vertical and capturing value by striking the right partnerships or developing the right capabilities. We could see some more exits and mergers in 2023 because IoT, which is very vertical driven, has been seeing volatile growth due to internal or external factors.”

For detailed research, refer to the following reports available for subscribing clients and individuals:

Counterpoint tracks 1,500+ IoT module SKUs on a quarterly basis and provides forecasts on shipments, revenues and ASP performances for 80+ IoT module vendors, 12+ chipset players and 18+ IoT applications across 10 major geographies.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the technology, media and telecom (TMT) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Automotive and Transport & Logistics contributed to nearly half the total connections

AT&T continues to lead, accounting for almost 55% of the total cellular-IoT connections in the US

Seoul, Hong Kong, New Delhi, Beijing, London, Buenos Aires, San Diego

7th October 2019

Cellular-IoT connections in theUSgrew 20% year-on-year (YoY) in H1 2019, and we expect they will grow by 21% YoY for the full year 2019, driven by automotive, transport & logistics, and wearables with cellular connectivity, according to the latest research from Counterpoint’sIoT (Internet of Things)service. In the future,5Gwill play an increasingly important role in some high-bandwidth and low-latency applications such as autonomous cars,drones, high-definition smartsurveillancecameras, and industrial IoT, but for now, mostcellular IoTconnections are based on 2G/3G and 4G LTE technologies.

Commenting on the cellular service providers’ IoT deployment strategies, Counterpoint’sResearch Analyst,Satyajit Sinha, noted, “On average, for a cellular-IoT solution deployment,connectivityaccounts for around 12% of the value, whereas hardware components, modules, and devices make up 22%. The rest of the value in an IoT solution is captured by system integrators, middleware, software platforms, and cloud analytics vendors. Hence, AT&T, Verizon, Sprint and T-Mobile are looking to capture maximum value by providing end-to-end IoT solutions, bundling IoT devices, secure connectivity, platform, and data management to capitalize on the overall opportunity.”

Sinha, further added, “The trend for partnerships among players in the IoT ecosystem is not something new, however, the partnership of network operators and cloud players is creating headlines in 2019. AT&T andMicrosoftforged a multi-year alliance to provide cloud services and edge computing solutions. Through this alliance, AT&T’s objective is to migrate most non-network workloads to the public cloud by 2024 and focus on core network capabilities. Similarly, Sprint partnered withAWSto integrate cloud services with its Curiosity IoT platform foredgecomputing solutions.”

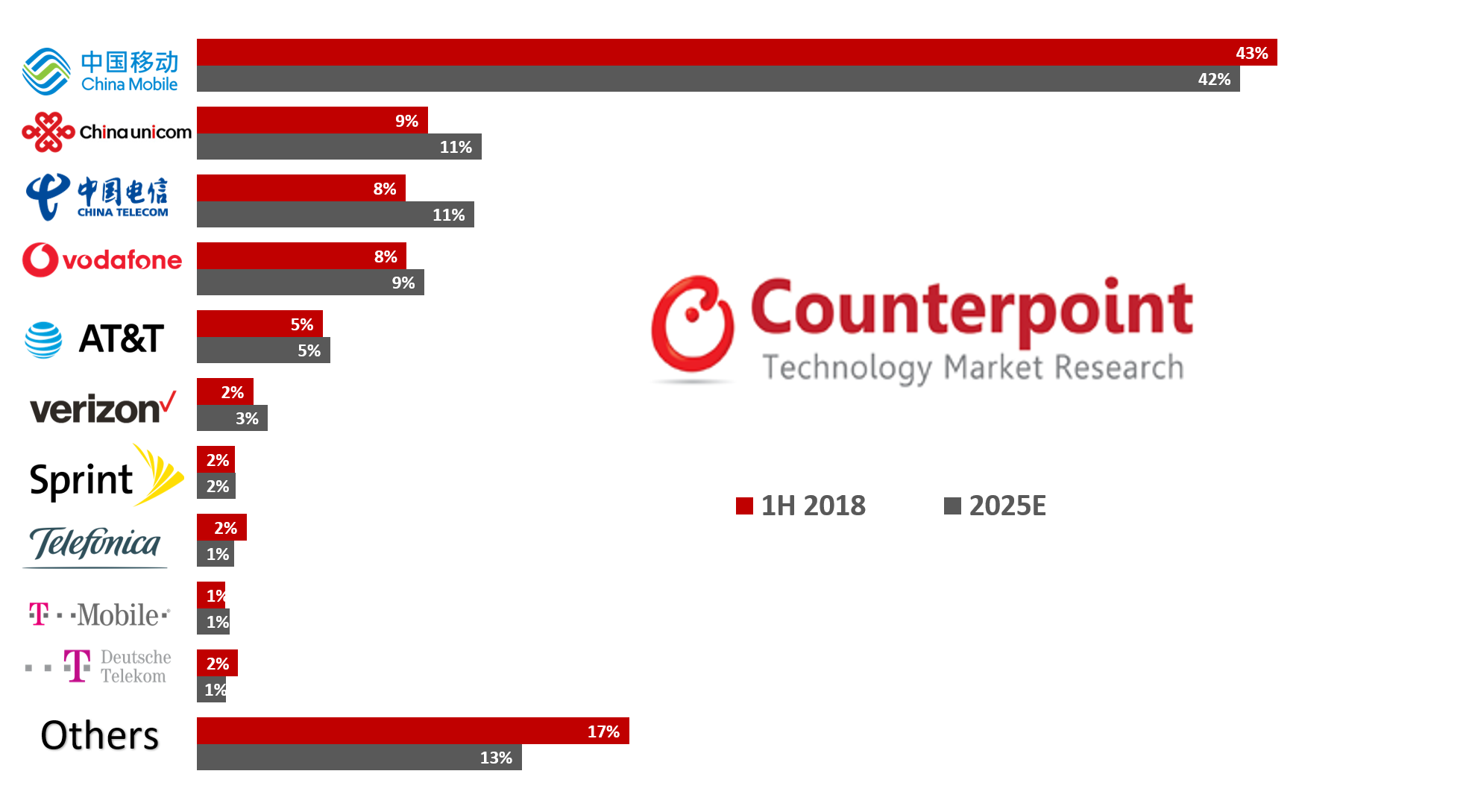

Exhibit 1: USCellular-IoT Connection Share by Service Provider, 1H 2019

Source: Counterpoint Research: 2010-2025 US Cellular-IoT Connection Tracker and Forecast

Adding his perspective,Research Director,Jeff Fieldhack, noted, “In the US, cellular IoT connectivity has been modest so far unlike in China. But we expect the dual-cellular LPWA (LTE-M + NB-IoT) strategy byUS service providerswill further drive cellular-IoT connections. We will see a decline in legacy connections (2G/3G), as most of the earlier M2M (machine-to-machine) type applications will migrate toLPWAnetworks. Further, we expect theautomotivesegment to continue to lead in terms of cellular IoT connections and the segment will leverage 4G LTE and upcoming connectivity.”

Exhibit 2: USCellular-IoT Connection by Application Market Share in 1H 2019

Source:Counterpoint Research: 2010-2025 US Cellular-IoT Connection Tracker and Forecast

The comprehensive and in-depth report on “ US Cellular-IoT Connection Tracker CY 2010-2025” is a part of our IoT (Internet of Things) service. This report is available for downloadhere

Background:

Counterpoint Technology Market Research is a global research firm specializing in Technology products in the TMT industry. It services major technology firms and financial firms with a mix of monthly reports, customized projects and detailed analysis of the mobile and technology markets. Its key analysts are experts in the industry with an average tenure of 13 years in the high-tech industry.

Seoul, Hong Kong, New Delhi, Beijing, London, Buenos Aires, San Diego

Sep 26th, 2018

China will continue to lead by contributing almost two-thirds of the global IoT Cellular Connections. Whereas,Vodafonewill continue to be the largest operator elsewhere globally if we excludeChina and Chinese operators.

According to the latest research from Counterpoint’s IoT (Internet of Things) service,Global IoT Cellular Connectiongrew 72 % in 1H18, a considerable increase from the same period last year.

Commenting on the future growth of connected IoT devices, Counterpoint Research Analyst, Satyajit Sinha, noted, “Smart manufacturing, smart utilities and smart mobility applications such as automotive, asset tracking will be the key growth drivers over the next five to seven years.Many of these applications will demand low-power, low-bandwidth, low-cost and ubiquitous cellular connectivity which will be initially satisfied by the emerging Low Power Wide Area Network (LPWAN) cellular technologies like LTE-M, NB-IoT, and EC-GSM-IoT. Further, futuristic applications such as autonomouscars,drones, connected healthcare, and mission-critical IoT applications will be powered by the upcoming5Gtechnology revolution which promises massive capacities, throughputs, and lower latencies.”

Mr. Sinha, further added, “Emerging markets like India, Brazil and in Africa while can offer tremendous scale but will likely be late followers compared to China in this path to connected everything. However, the massive growth opportunity remains in terms of cellular-IoT connections in emerging markets which will be possibly catalysed by operators such as Jio in India but more specifically from multi-market players such as Telefonica or MTN orVodafonewith plans to deploy LPWAN networks such as NB-IoT leveraging scale across their coverage markets.”

Adding his perspective, Research Director, Peter Richardson, noted, “Most of the IoT connections are still on 2G/2.5G networks. However, the shift to 4G LTE and cellular-LPWAN is already in motion and we expect an ongoing shift to these newer technologies in 2H 2018 and 2019.”

Mr Richardson, also added, “While cellular-LPWANbrings a number of advantages over unlicensed LPWA solutions – there are a number of use cases where unlicensed technologies offer a superior mix of cost and functionality. Over the short to medium term, we expect co-existence and even the combined use of both licensed and unlicensed LPWA technologies.”

Exhibit 1: GlobalCellular IoT Cellular Connection market share in 1H 2018 vs 2025

Source:Counterpoint Research: 2010-2025 Global IoT Cellular Connection Tracker

Highlighting the latest trends in IoT connectivity strategies, Research Director, Neil Shah added, “Revenue generation from theIoT ecosystemis not siloed to any one specific segment of the value chain, rather it is distributed among all segments. On an average for a cellular IoT solution deployment, connectivity represents around 12%, whereas hardware components,modulesand devices represent 22%. The rest of the bulk of the value in an IoT solution is captured by system integrators, middleware, software platforms, and cloud analytics vendors. Hence, if operators are looking to capture maximum value, the strategies need to provide an end-to-end IoT solutions by bundling IoT devices, secure connectivity,platform, and data management to capitalize on the overall opportunity.

一些大的运营商已经选择特定的IoT solutions and verticals to offer a comprehensive IoT solution, but it won’t be practical for the operator to offer similar end-to-end solutions across every vertical and hence partnerships across the IoT value chain will be the key to capture value.”

Mr Sinha, though highlighted, “Consumer IoT is still largely an untapped opportunity for cellular operators and probably the toughest one. This is partly due to device and connectivity costs and, to some degree, due to data privacy & security concerns. The continuous growth insecurityand data privacy policies, such asGDPR, will help and grow consumer confidence. We expect cellular consumer IoT will form an important revenue stream for operators starting with smart home andwearablesto be top IoT applications by 2025.”

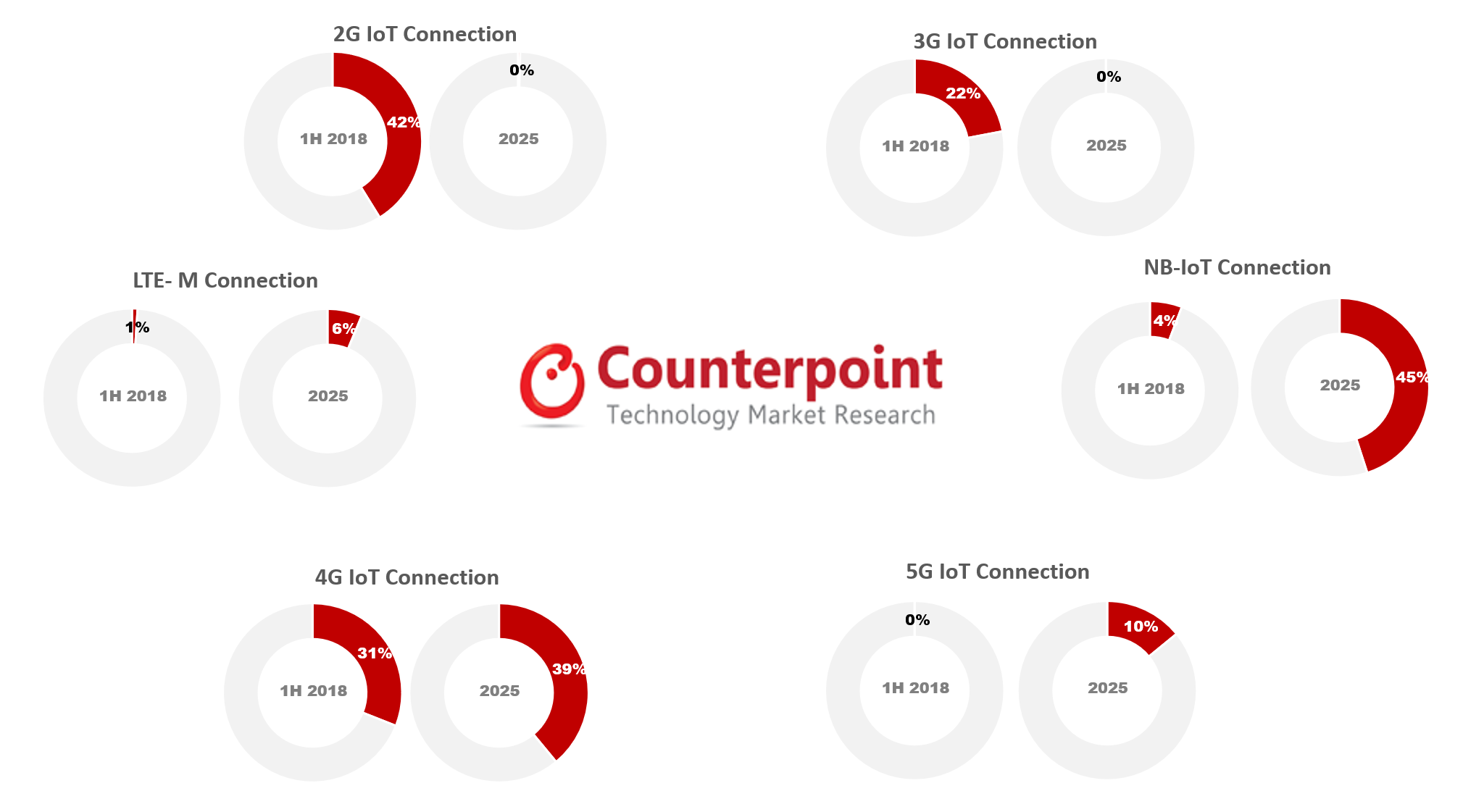

Exhibit 2: GlobalIoT Cellular Connection by Technology Market Share in 1H 2018 vs 2025

Source:Counterpoint Research: 2010-2025 Global IoT Cellular Connection Tracker

IoT Connectivity by Technology Market Analysis – By-2025

2G IoT connections will occupy less than 1% of global IoT cellular connections by 2025; increasingly being replaced by NB-IoT.

3G IoT connections face the same fate as 2G. However, 3G will go extinct much faster than 2G.

4G LTE IoT connections (high bandwidth & low latency) will grow at a much faster rate till 2022 due to global adoption of LTE Advanced and Advanced Pro. However, post-2022 we expect a smooth transition from 4G LTE family to 5G. 4G LTE IoT connections will hold slightly more than a third of global IoT cellular connections in 2025.

LTE-M Connection will have a presence until 2022. However, we expect its growth to be limited as both NB-IoT and unlicensed LPWA will take away its opportunity and share. LTE-M connections will be around 6% of global IoT cellular connections in 2025.

NB-IoT will dominate the market with 45% of global IoT cellular connections, due to the wide variety of application opportunities and faster adoption rates in the overall ecosystem.

5G will be crucial for some sectors, for example automotive, especially for V2V and V2X. The adoption of 5G cellular will depend on the availability, cost of modems from companies like Qualcomm and Huawei as well as coverage area. We expect 5G to account for around 10% of global IoT cellular connections in 2025.

Background:

Counterpoint Technology Market Research is a global research firm specializing in Technology products in the TMT industry. It services major technology firms and financial firms with a mix of monthly reports, customized projects and detailed analysis of the mobile and technology markets. Its key analysts are experts in the industry with an average tenure of 13 years in the high-tech industry.

In order to access Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not. Personal Information When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

你可以请求终止您的帐户或到凶手scribe to any email subscriptions or mailing lists at any time. In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company. – Passwords are for user’s individual use – Passwords may not be shared with others – Users may not store documents in shared folders. – Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified. Accuracy of Information: While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links: This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience. This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.