Colombian telecom operators and government are positive about the outcome of the 5G spectrum auction in December.

The government, telecom operators and regulatory bodies want to increase broadband penetration and provide training to Colombians to bridge the digital divide.

Telecom operators ETB and Claro shared their plans to leverage 5G to enhance verticals like education, mobility, and B2B services.

Even asColombialooks forward to holding its first 5G auction in December this year, it has much more basic and long-pending telecom sector-related issues that need the attention of all stakeholders, whether the operators or government departments. It is with this in mind that representatives from the Colombian government, regulatory bodies, telecom operators and manufacturers gathered in the nation’s capital, Bogota, at the end of June for the Conecta Colombia summit. The event, which is a part of the series that Conecta Latam organizes in the region, saw discussions on regulation, technology and, of course, business. A team of analysts from Counterpoint was also present at the event. Here are their key takeaways:5G and connectivity expansionThe potential of 5G technology and its impact on various sectors were essential discussion topics at the event. Telecom operators ETB and Claro shared their plans to leverage 5G to enhance verticals like education, mobility, and B2B services. Investments in broadband and 4G were also emphasized as ongoing priorities alongside the imminent 5G auction. The discussions also recognized the need to focus on network coverage and connectivity expansion, ensuring that before the widespread adoption of 5G.

Main 5G verticals to be developed in Colombia, including a $166 billion opportunity until 2035 as per Hugo Chang at Nokia.

Security and digital transformation

Bridging the digital divide根据regulators, by the end of Q1 2023, Colombia had 9 million fixed broadband connections, which means that only approx. 61% of households in Colombia have access to fixed broadband. Highlighting Colombia’s digital divide, speakers at the summit emphasized the need to address challenges Colombians have such as lack of technical skills and connectivity. The government, telecom operators and regulatory bodies discussed strategies to increase broadband penetration, provide training to Colombians, involve regional stakeholders in the sector decision-making, and improve job formalization. The focus was on leveraging technology to narrow the digital divide and ensure equal access to digital opportunities.

“Centros Digitales” at the core of the solution to bridge the digital divide. MinTic aims to reach 85% broadband penetration by 2031 compared to 61% in Q1 2023.5G and connectivity expansionThe potential of 5G technology and its impact on various sectors were essential discussion topics at the event. Telecom operators ETB and Claro shared their plans to leverage 5G to enhance verticals like education, mobility, and B2B services. Investments in broadband and 4G were also emphasized as ongoing priorities alongside the imminent 5G auction. The discussions also recognized the need to focus on network coverage and connectivity expansion, ensuring that before the widespread adoption of 5G.

Main 5G verticals to be developed in Colombia, including a $166 billion opportunity until 2035 as per Hugo Chang at Nokia.Security and digital transformation

During 2022 there were 20 billion failed cyberattacks in Colombia as disclosed by a Fortinet study, based on that government officials and telecom operators highlighted the importance of cybersecurity for the industry. Panel discussions emphasized the need for a national entity to coordinate carrier efforts and use artificial intelligence (AI) as a defensive tool. Besides, the event explored the concept of digital transformation withintelecomcompanies, with discussions revolving around employee training, customer experience and the transformation of big data into “mega data” facilitated by 5G. The role of alternative revenue drivers such as VoLTE and MVNO products were also highlighted as options before the 5G benefits come to play.

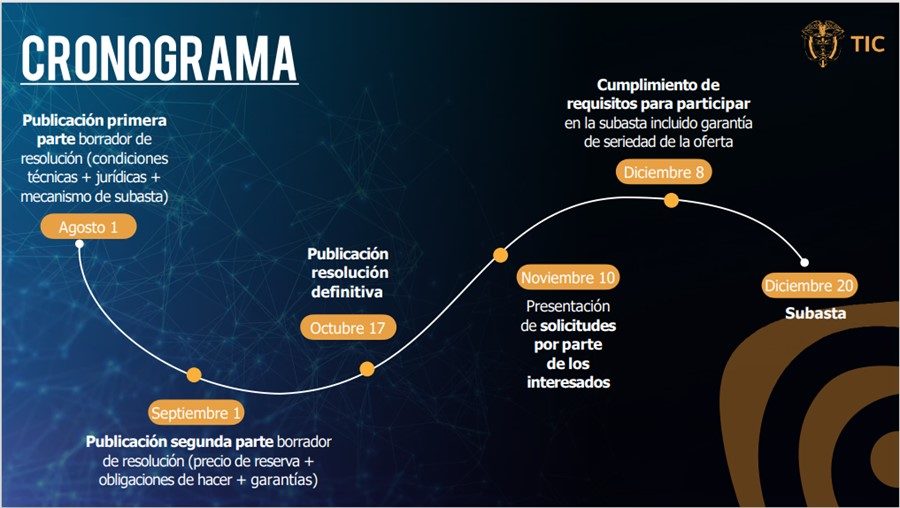

Saul Kattan, technical consultant of the Colombian presidency leads the panel discussion on the role of a national cybersecurity entity sponsored by the government.What is next?On August 1, the regulator will publish the first draft of the auction process, covering the mechanism to be followed and the required technical conditions for the applicants. The second draft will be released one month later and the final in October. In November and December, all the interested parties will submit their applications for the auction, which will start on December 20. 2024 can become the year of the 5G availability in the country.

5G auction and 4G spectrum renovations chronogram.Bridging the digital divide根据regulators, by the end of Q1 2023, Colombia had 9 million fixed broadband connections, which means that only approx. 61% of households in Colombia have access to fixed broadband. Highlighting Colombia’s digital divide, speakers at the summit emphasized the need to address challenges Colombians have such as lack of technical skills and connectivity. The government, telecom operators and regulatory bodies discussed strategies to increase broadband penetration, provide training to Colombians, involve regional stakeholders in the sector decision-making, and improve job formalization. The focus was on leveraging technology to narrow the digital divide and ensure equal access to digital opportunities.

“Centros Digitales” at the core of the solution to bridge the digital divide. MinTic aims to reach 85% broadband penetration by 2031 compared to 61% in Q1 2023.5G and connectivity expansionThe potential of 5G technology and its impact on various sectors were essential discussion topics at the event. Telecom operators ETB and Claro shared their plans to leverage 5G to enhance verticals like education, mobility, and B2B services. Investments in broadband and 4G were also emphasized as ongoing priorities alongside the imminent 5G auction. The discussions also recognized the need to focus on network coverage and connectivity expansion, ensuring that before the widespread adoption of 5G.

Main 5G verticals to be developed in Colombia, including a $166 billion opportunity until 2035 as per Hugo Chang at Nokia.Security and digital transformation

During 2022 there were 20 billion failed cyberattacks in Colombia as disclosed by a Fortinet study, based on that government officials and telecom operators highlighted the importance of cybersecurity for the industry. Panel discussions emphasized the need for a national entity to coordinate carrier efforts and use artificial intelligence (AI) as a defensive tool. Besides, the event explored the concept of digital transformation withintelecomcompanies, with discussions revolving around employee training, customer experience and the transformation of big data into “mega data” facilitated by 5G. The role of alternative revenue drivers such as VoLTE and MVNO products were also highlighted as options before the 5G benefits come to play.

Saul Kattan, technical consultant of the Colombian presidency leads the panel discussion on the role of a national cybersecurity entity sponsored by the government.What is next?On August 1, the regulator will publish the first draft of the auction process, covering the mechanism to be followed and the required technical conditions for the applicants. The second draft will be released one month later and the final in October. In November and December, all the interested parties will submit their applications for the auction, which will start on December 20. 2024 can become the year of the 5G availability in the country.

5G auction and 4G spectrum renovations chronogram.

Boston, Toronto, London, New Delhi, Hong Kong, Beijing, Taipei, Seoul – June 10, 2021

LATAM smartphone shipments surged by 22.1% YoY in Q1 2021 but decreased by 4.8% QoQ due to seasonality, according to the latestMarket Monitor reportfrom Counterpoint Research. The competition fuelled by Samsung and Motorola launching refreshed models and new Chinese OEMs entering the region drove the market growth.

Commenting on the market dynamics, Principal AnalystTina Lusaid, “In Q1 2021, the region’s smartphone market saw an extraordinary 22.1% growth, as last year it was impacted by a shortage of products coming from China, andCOVID-19lockdowns by the end of the quarter. This year, it still faced some product shortages due to inadequate component supplies, especiallythe chipset。But this impacted mainly the ‘Local Kings’ and smaller brands, as their negotiating power is lower.”

Lu added, “The first quarter of the year is usually a slow one, as most of the Southern Hemisphere is on summer holidays. But fierce competition fuelled by new Chinese OEMs entering the region and Samsung launching new models in the A-series while increasing advertising to announce the S-series, drove the market growth. This shows that the smartphone market is resilient in the face of tough conditions due to the pandemic. Brazil ranks third globally in terms of most number of COVID-19 cases while Mexico ranks fourth among countries with the highest number of COVID-19 deaths.”

Smartphone Shipment Market Share, Q1 2021

Source: Counterpoint Research Market Monitor, Q1 2021

Commenting on the regional performance, Research AnalystParv Sharmasaid, “All major LATAM countries except Chile saw double-digit growth. Argentina, Peru and Brazil drove the region’s overall growth. The economic recession due to the pandemic failed to diminish the volume of smartphones sold in the region, partly because of the smartphone becoming an essential gadget and partly due to the OEMs driving the market. However, the pandemic did impact the consumer’s smartphone purchase budget, which the OEMs were fast to react to and increase their entry-level models.”

Smartphone Shipment Growth by Country, Q1 2021 vs Q1 2020

Source: Counterpoint Research Market Monitor, Q1 2021

Market summary

Samsungremained the region’s leading brand. It was aggressive on the sell-in front. Four out of ten smartphones sold in the LATAM market were from this OEM.

Samsung’svolume increased QoQ despite the seasonality factor. It started 2021 by renewing part of its A-series portfolio. It also advertised heavily during the launch of new flagship models —Galaxy S21, Galaxy S21 Plus and Galaxy S21 Ultra— in February. This drove higher sales for all the other lines from this brand.

Motorolavolume increased more than 88% YoY. This growth came from the ground gained from Huawei and due to supply constraints faced by the OEM last year following the COVID-19 outbreak in China.

Motorolaremained a solid second player in the region, although closely challenged by Xiaomi and even OPPO in Mexico.

Xiaomicontinued its YoY growth. However, the growth reached a plateau during the quarter as Xiaomi has no local manufacturing in Brazil. At the same time, it is still building its brand in the rest of LATAM.

Xiaomi’sgrowth has been slightly challenged by new Chinese entrants in some countries, such as Colombia, Chile and Mexico.

Applecontinues to grow. It leads the introduction of5G handsets in the regionwith the iPhone 12 model. However, the iPhone 11 still takes a large portion of its volume.

ZTEdoubled its volume and increased its share YoY. The brand expanded its participation in the LATAM market by entering the open channel. It is also growing its footprint in Peru and Colombia.

LGalso managed to increase its volume and share, which is a breakthrough for the OEM that has been experiencing YoY declines for almost two years. The announcement that it plans toexit the mobile device marketdid not impact its performance during Q1 2021.

‘Others’saw a dramatic decrease as ‘Local Kings’ are now playing mostly in the 3G smartphone space. This group was most impacted by the chipset shortage.

The comprehensive and in-depth Q1 2021 Market Monitor is available for subscribing clients. Feel free to contact us atpress@www.arena-ruc.comfor further questions regarding our in-depth research and insights, or for press enquiries.

Background:

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

The sales channel landscape for the LATAM mobile devices market has been going through significant changes in the last few years. Just two years ago, nearly 70% of the quarterly mobile device sales in LATAM came from operators. Today, the open channel has a more even share (43%) of the market. And it is growing fast.

In a market where sales of mobile devices have grown at a CAGR of only 0.24% between 2016 and 2018, the open channel has grown at almost 8% CAGR. As a result, operators have been slowly pivoting towards being a service provider after years of being device driven business.

Exhibit 1: Open Channel Mobile Devices Market Share 2016Q1 vs. 2019Q1

Source: Counterpoint Market Monitor Q1 2019

At Counterpoint, we have been mapping the top three operators’ share in mobile device sales for more than three years. The findings reveal starkly different strategies of LATAM’s two biggest operators, America Movil, and Telefonica, resulting in very distinct outcomes and share of the mobile device market. America Movil, which operates under the brands Claro and Telcel, and Telefonica, which operates under the brands Movistar and Vivo, still account for 70% of the mobile handsets sold through the operator channel. Counterpoint’s latest research tracks the changing trends of the sales channel and OEMs for mobile devices in the LATAM region over the last few years in great detail. The comprehensive and in-depth report is available exclusively for clientshere.

We believe the LATAM mobile devices market is heading towards an open channel ecosystem. Every other quarter, operators do regain some share. However, in peak season, the open channel claws back its lost share and even gains marginally. Over time, operators will continue to lose share. This forces OEMs to negotiate with the retail sector directly.

The open channel, which consists of big retail chains as well as small shops, in some instances, can be tougher to work with than an operator. However, the rise of the open channel has allowed more brands to enter the region. All the top five selling brands, that account for 78% share in LATAM, have a different approach to the operators and open channel when it comes to their channel strategy. Huawei is extremely strong within operator channels. Samsung, on the other hand, the leader of the market in LATAM, and its participation across different sales channels is very similar to that of the market.

This is why we believe that the increasing importance of the open channel is positive for OEMs. Although the operator channel was large, operators were often very selective about the models they stocked. For example, Claro (America Movil) Brazil would only range four brands. However, the same company in Mexico, under the brand name Telcel, would offer more than 22 brands. An increasing share of open channel sales removes such arbitrariness of distribution. But the open channel requires a more aggressive turnover than operators. We examine this and much more in our latest analysis, exclusively for clients, titled.‘LATAM Mobile Devices Sales Channel Analysis: The Rise of the Open Channel’。

Recently, the International Monetary Fund (IMF) projected that economic growth in emerging markets, during 2019, will be faster (4.7%) than developed markets (2.1%). This is a good omen for the smartphone market, which is still reeling from itsfirst ever annual decline in 2018。

Although the economic strength of emerging markets will not be good enough to bring back growth to theoverall smartphone market, they can certainly help arrest the decline. This is why we believe that the smartphone supply chain will keep a close eye on the emerging markets in 2019.

The IMF defines emerging markets (Exhibit 1) based on the GDP and other economic parameters.

Exhibit 1: Emerging Markets as defined by the IMF

LATAM

APAC

MEA

EU

Argentina

Bangladesh

South Africa

Bulgaria

Brazil

India

Turkey

Hungary

Chile

Indonesia

Poland

Colombia

Malaysia

Russia

Mexico

Pakistan

Ukraine

Peru

Philippines

Romania

Venezuela

Thailand

China

Impact on the Global Smartphone Markets

Emerging markets alone contribute to 59% of global smartphone shipments. Even if one excludesChina, they contribute to 32% of theglobal smartphone market。As perCounterpoint’s Market Outlook, emerging markets excluding China (EMXC) will grow faster (6%) than in 2018 (4%). The growth rate continues to be faster than the overall smartphone market, which is likely to see a second successive year of decline in 2019. Therefore, growth in emerging markets is a positive indicator for certain OEMs looking to expand in these markets.

In 2018, 14 out of 23 emerging markets show positive year-on-year (YoY) smartphone growth. This year, 18 out of 23 emerging markets are likely to grow YoY. The markets which will drive the smartphone growth includeBangladesh(37%),India(11%),Colombia(9%), andPhilippines(9%)。我们相信互联网普及率较低in these countries, in terms of unique subscribers, and a healthy GDP growth predicted for 2019 will propel smartphone sales. The internet penetration in these countries, in terms of unique subscribers, is still below 50%. Other factors which will work in favor of these countries is a healthy mix of sub-US$100 installed base of smartphone users who are likely to upgrade.

Bright Spots Among Emerging Markets

Asian emerging markets will lead the growth and are also likely to benefit from the ongoingUS-China trade war。如果公司决定重新思考他们的供应茶in, countries like Malaysia, India, Indonesia, Thailand, and India will stand to benefit.

Moreover, the Indian economy continues to perform well with healthy domestic consumption. The 2019 general elections brought a strong government. This is likely to bring in certainty in regulatory and policy frameworks which will aid overall economic growth.Bangladesh, at the same time, is pushing is domestic manufacturing and focusing on financial and digital inclusion of its citizens. An uptick in employment levels drives thePhilippines’ growth. This will have a positive impact on the replacement cycle of the smartphones, especially in the sub-US$100 segment.

Overall, the LATAM regionis recovering with high growth rates estimated for countries like Peru, Chile, and Colombia.Colombia’s market is undergoing positivesmartphone growthwith the new government at the center betting big on a digital economy.

Other markets which are likely to see smartphone growth includeIndonesia, Pakistan, Peru,Russia, Thailand, and Ukraine.

Of course, not all emerging markets have a positive outlook. Some will fare better than others. There are certain emerging markets which will continue to undergo macroeconomic, regulatory, and political challenges. These markets includeArgentina,Brazil, Mexico, and Turkey.Brazil’s economyis not picking up so far, and it will most likely not happen throughout 2019. However, the decline will not be as steep the one it experienced in 2018.

Turkey is bracing for a long recession ahead with inflation reaching a 15-year high. Currency in these markets remains volatile too.Argentinais unlikely to grow too, and the upcoming general election in late 2019 will be key in terms of providing a roadmap for certain reforms and economic policies. Mexico remains in the shadows of ongoingtrade warand concerns over any upcoming tariffs. However, the US has recently scrapped plans to increase tariffs as part of an agreement between the two countries on immigration issues. But uncertainty still looms over the future.

EmergingEuropeis facing a slowdown driven by a recession in Turkey. Russia is likely to grow, but Ukraine faces tighter monetary conditions. The inflationary pressure for emerging European markets will remain throughout the year.

To summarize, we believe that emerging markets will exhibit stronger growth in 2019 as compared to last year. This is a positive trend for the top five OEMs in these markets as their combined share has been steadily increasing over the past few quarters. Users in these emerging markets are now empowered and becoming digitally literate. Financial inclusion is happening, and dissemination of information for users is stronger than before.

Huawei has been building momentum in LATAM with record volumes and a growth of 51% year-on-year (YoY) during 2018. Its growth came at a time when the market declined by 1%. And it isn’t as if Huawei was slowing down. In Q4 2018, its volume growth reached 130%, YoY. Astonishingly, this growth came despite Huawei not being present in around 37% of the LATAM smartphone market as it does not operate in Brazil and exited Argentina in Q3 2018.

By the end of 2018, Huawei was the leader of the market in Peru and a very solid number two in Chile and Colombia. In Colombia, Huawei became the second largest brand in 2018 and also the leading Chinese brand with 24% market share after including sales of its co-brand HONOR. HONOR entered Colombia in H2 2018, and quickly picked-up share. In Mexico, its biggest LATAM market, Huawei has been increasing volumes through a two for one mix between high and low-price band devices and recently challenged Samsung to be the number one brand in the country. Even in Peru, Huawei keeps challenging for the top spot.

Part of Huawei success in LATAM is due to its improving reputation for offering excellent quality products. Heavy spending on marketing; up to several millions of dollars yearly, in sponsorship, and both online and offline campaigns has successfully built the Huawei brand in the region.

Further, its sales team was big enough to help the brand get into all channels and carriers. Huawei even opened flagship repair stores in most of the capital cities of the biggest countries in LATAM. All these efforts were quite synchronized.

However, just as it seemed Huawei was about to reach a peak for its consumer business unit, the US government decided to impose the export ban. Under a business-as-usual scenario, Huawei’s diligent efforts to enter Brazi would likely have been successful and further boosted its presence in LATAM. But in the current geopolitical environment, entering Brazil looks increasingly unlikely. For the short-term, it will be difficult for Huawei to maintain momentum in LATAM. Counterpoint Research’s analyst team has measured the multiple impacts of the ban in LATAM and other regions, as well as other Huawei business units. This analysis is available to all subscribing clients.

Huawei was the fastest growing brand (76% YoY growth including HONOR co-brand), surpassing Motorola to become the second largest brand in Colombia

New Delhi, Hong Kong, Seoul, London, Beijing, San Diego, Buenos Aires – May 22nd, 2019

Smartphone shipments in Colombia grew 2% year-on-year but declined 26% quarter-on-quarter (QoQ) during Q1 2019, according to the latest research from Counterpoint’s Market Monitor service. The sequential fall was primarily due to extraordinary volumes in the previous quarter driven by the Christmas holiday season.

Commenting on the findings,Senior Analyst,Tina Lusaid, “Four out of top five brands in Colombia have increased shipment volumes YoY during Q1 2019. This is driving consolidation in the market. Top five smartphones brand in Colombia, represented more than 77% of the market, a nearly eight-percentage point increase YoY. This leaves more than 40 brands to fight for the remaining 23% of the market. The device market is already looking very crowded. For any new brand seeking to enter Colombia, it might not be an easy task.”

Commenting further,Tinanoted, “The Colombian market was one of the few markets in LATAM that has been growing YoY every single quarter during 2018. Most of the top five brands have increased shipment volumes compared to the previous year, driven by new users and replacements. Smartphone penetration in Colombia was below 65% at the end of 2018. Therefore, there will be new users that would offset replacement slow down. As a result, it still had room to resist the global smartphone market decline. Smartphone growth is also pushing the feature phone segment to a sharp decline.”

Commenting on the pricing strategies,Research Analyst,Parv Sharma, added, “Low-end smartphones dominated the Colombian market. During Q1 2019, eight out of 10 smartphones were below US$200. However, smartphone shipments in the

Exhibit 1: Colombia Smartphone Market Share by Brand, 2018 Q1 vs 2019 Q1

Source: Counterpoint Market Monitor Q1 2019

Samsung is the absolute leader in the Colombian market with a 30% share, an increase of more than one percentage point share compared to the previous year.

Samsung’s ASP increased by 16%, driven by growing volumes in the flagship and mid-to-high price band.

Huawei’s sales volumes (excluding HONOR co-brand) have grown 60% YoY in Q1 2019, and it has become the second largest smartphone brand in Colombia.

Huawei’s co-brand, HONOR, launched in Colombia during H2 2018. It has already managed to capture more than 1% of the Colombian market.

Huawei migrated its portfolio to lower price bands. Its success was a combination of the excellent product lineup, very aggressive pricing, and heavy investment in channel management.

Motorola has managed to increase shipments slightly despite Huawei’s aggressive push.

With Motorola entering Comcel during 2018, it gave the brand extra boost to maintain its share.

Alcatel’s share deteriorated in 2018, especially in the smartphone category. It was one of the many brands that were deeply affected by Huawei.

Lanix是当地最畅销的品牌。然而,我ts volume decreased by half YoY.

Local Kings got demoted to mainly supplying feature phones and 3G smartphones. They lost market share to the increasing number of Chinese brands.

LTE capable smartphones grew 22% YoY driven by more affordable LTE enabled devices and replacements.

Smartphone ASP has grown almost 13% YoY, boosted by Samsung and Huawei.

The comprehensive and in-depth Q1 2019 Market Monitor is available for subscribing clients. Please feel free to contact us atpress(at)www.arena-ruc.comfor further questions regarding our in-depth latest research, insights or press inquiries.

The Market Monitor research is based on sell-in (shipments) estimates based on vendor’s IR results, vendor polling triangulated with sell-through (sales), supply chain checks and secondary research.

Chinese OEMs continues to gain traction in the region

New Delhi, Hong Kong, Seoul, London, Beijing, San Diego, Buenos Aires –

November 23st, 2018

根据latest research from Counterpoint’s Market Monitor service, the Latin American (LATAM) Smartphone market has declined by more than 7% YoY due to economic uncertainty in four out of the six major countries in LATAM. Colombia, Brazil and Mexico’s markets were affected by presidential elections. These elections brought uncertainty to the economy and hence altered consumer purchasing behavior.

评论拉丁美洲市场开发t, Counterpoint’s Senior Analyst, Tina Lu, highlighted, “The replacement rate of local consumers is noticeably slowing. The cost of purchasing a new smartphone is a major investment for many consumers and, in most cases, they pay for their devices in 18 or 24 monthly installments. There is, therefore, a strong desire to make the smartphone last longer than the installment payment period. This change in user behavior has also brought a new level of importance to after-sales services. This has knock-on benefits in driving more business to companies providing after-sales service and refurbished smartphones”.

Commenting on vendor performances, Parv Sharma, Research Associate, noted: “Following the overall market decline, the sale of all top-selling brands in volume terms apart from Huawei, have also decreased. Huawei has once again recorded strong growth of 37% YoY, and 10% sequentially. Huawei has been driving volume, in its biggest market, Mexico, with a two for one mix between high and low-price band devices. Huawei is gaining brand preference as its reputation for offering excellent quality products widens.”

Source: Counterpoint Research Market Monitor Q3 2018

Samsung remains the absolute leader in the LATAM market. However, it lost around 1% share.

Samsung’s unit volume decline came mostly from Argentina, Chile and Brazil. Argentina’s market contracted by more than 40% YoY.

Motorola managed to retain its share, despite its decision to gradually decrease the volume of its bestselling C-series models and in the face of stiff competition from other Chinese brands.

Motorola grew in markets which were traditionally a challenge for it, such as Colombia, where it managed to achieve more than 50% YoY growth by increasing its share with local operators.

在大多数的regi华为两位数的增长on’s markets in which it operates. The one exception was Argentina where its volume reduced by more than a quarter YoY due to the company’s decision to outsource sales and distribution – a process that is not yet finalized.

LG’s business has been the most impacted. LG remains in the top three brands in Brazil, the largest market in LATAM, but it was not enough to offset a sharp drop in most other markets in the region.

Mexico was the only country, in LATAM, to be included in the first round of the latest iPhone launches. In all the other countries, Apple launched its latest iPhone models between October and November.

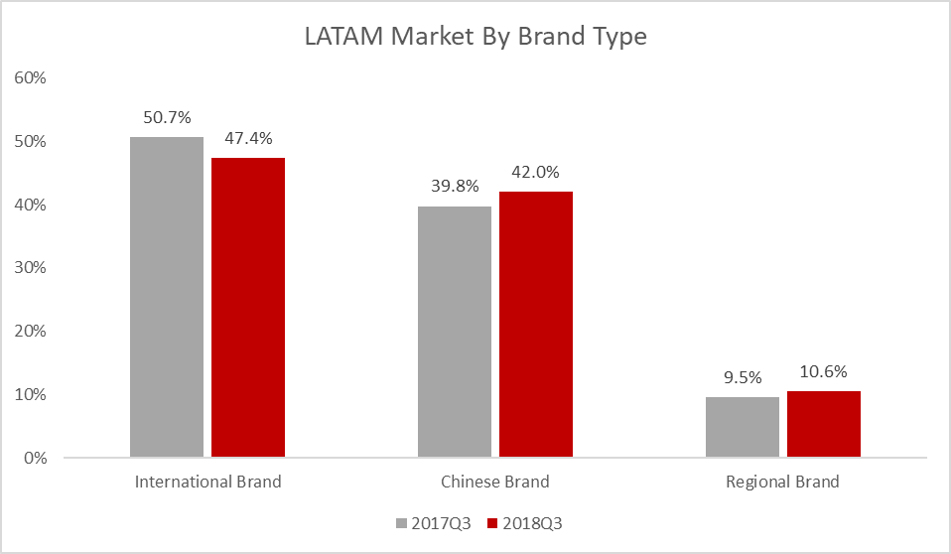

Exhibit 2: Latin America Brands Origin Variation 2017 Q3 vs 2018 Q3

Source: Counterpoint Research Market Monitor Q3 2018

International brands still dominate the LATAM smartphone ecosystem, Samsung is the best-selling brand in this group.

Although some Chinese brands such Huawei and Xiaomi enjoyed strong performances, the Chinese brands’ group had only around 2% growth, offset by the decline of other Chinese brands such as Alcatel, Lenovo and ZTE.

Regional brands grew by 1% driven by the increasing numbers of local brands that managed to enter the distribution channel of most LATAM’s carriers.

Brazilian local brands such as Multilaser or Positivo also drove the growth of these regional brands.

Chinese brands are expected to grow in the LATAM region, but not massively until 2020 as two of the biggest LATAM markets, Brazil and Argentina will continue to effectively be closed to direct imports in 2019.

LATAM’s overall market will likely return to growth in 2019. Partly due to an easy comparison with a depressed 2018 and because many of the events that have caused the slowdown in 2018 will have passed.

The comprehensive and in-depth Q3 2018 Market Monitor is available for subscribing clients. Please feel free to contact us atpress(at)www.arena-ruc.comfor further questions regarding our in-depth latest research, insights or press enquiries.

In order to access Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not. Personal Information When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time. In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company. – Passwords are for user’s individual use – Passwords may not be shared with others – Users may not store documents in shared folders. – Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

公司有权改变、更新or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified. Accuracy of Information: While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links: This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience. This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.

Source: Counterpoint Research Market Monitor

Source: Counterpoint Research Market Monitor

Source: Counterpoint Market Monitor Q1 2019

Source: Counterpoint Market Monitor Q1 2019