Counterpoint is attending IDMC on September 13th – September 14th, 2023

Our analysts will be attending the India Display Manufacturing Conference (IDMC), 2023. You can schedule a meeting with them to discuss the latest trends in the technology, media and telecommunications sector and understand how our leadingresearchandservicescan help your business.

Here is the list of team members attending the event:

At IDMC, thought leaders from across the world will converge to share their insights and perspectives on the sector’s outlook and opportunities. This event will bring together prominent investors, business leaders in the global display industry, and leading Indian corporations.

Additionally, the event will feature an exhibition, unveiling the latest display products and trends, making it a gathering for anyone seeking to stay at the forefront of the industry.

Click here(or send us an email at contact@www.arena-ruc.com) to schedule a meeting with them

Weaker-than-expected macroeconomicsituationcontinuedto weigh on TSMC’sQ2 2023 business performance.Muted smartphone and PC/NB demand negatively impactedtheoverall utilization rateduring the quarter.Though largely expected by the market, the company further cut its full–year revenue guidance ontheweaker end demandexpected forH2 2023.However,TSMCprojects astrong AI demand inQ32023and,going forward,sees itself asthe key enablerfor AI GPUsandASICs that requirealarge diesize.We give ourtakeson the key points discussed during theearnings call:

Is AI semiconductor demand real?

Chairman(Mark Liu):Neither can we predict the near future, meaning next year, how the sudden demand will continue or will flatten out. However, our model is based on the data center structure. We assume a certain percentage of the data center processors areAIprocessors and based on that, we calculate the AI processor demand. And this model is yet to be fitted to the practical data later on. But in general, I think the trend of a big portion of data center processors will be AI processors is a sure thing. And will it cannibalize the data center processors? In the short term, when thecapexof the cloud service providers is fixed, yes, it will. It is. But as for the long term, when their data service – when the cloud services have the generative AI service revenue, I think they will increase the capex. That should be consistent with the long-term AI processor demand. And I mean the capex will increase because of the generative AI services.

Adam Chang’sanalyst take:Supply chain checks reveal that cloud service providers such as Microsoft, Google, and Amazon aggressively invest in AI servers.NVIDIAis continuing to add orders for the A100 and H100 to the supply chain, echoing the strong momentum for AI demand. TSMC holds a significant market share in AI semiconductorwaferproduction, mitigating the risk of misjudging CoWoS capacity expansion concerning AI demand.

Akshara Bassi’s analyst take:Over the medium term, as hyperscalers continue to develop their own proprietary AI models and look to monetize through AI-as-a-Service and simiilar models, the infrastructure demand should remain robust.

Can AI semiconductor demand offset short-term macro weakness?

CEO (Che-Chia Wei):Three months ago, we were probably more optimistic, but now it’s not. Also, for example, China economy’s recovery is actually also weaker than we thought. And so, the end market demand actually did not grow as we expected. So put all together, even if we have a very good AIprocessordemand, it’s still not enough to offset all those kinds of macro impacts. So, now we expect the whole year will be -10% YoY.

Adam Chang’s analyst take:Although there is a lot of promise around AI, it would only account for around 6% of total revenues in 2023. Therefore,AIis not a panacea for broader short-term demand weakness.

Is TSMC CoWoScapacity enough to fulfill current AI demand?

CEO (Che-Chia Wei):For AI, right now, we see very strong demand, yes. For the front-end part, we don’t have any problem to support, but for the back end, the advanced packaging side, especially for the CoWoS, we do have some very tight capacity to — very hard to fulfill 100% of what customers needed. So, we are working with customers for the short term to help them to fulfill the demand, but we are increasing our capacity as quickly as possible. And we expect these tightening will be released next year, probably toward the end of next year. Roughly probably 2x of the capacity will be added.

Adam Chang’s analyst take:Due to TSMC’s CoWoS capacity constraints, the company is finding it challenging to fulfill the strong AI demand from customers,, including NVIDIA,Broadcom, and Xilinx, at the moment. NVIDIA is actively seeking second- source suppliers asTSMClooks to outsource some of its production.

N3E/N3/N2 status

CEO (Che-Chia Wei):N3 is already involved in production with good yield. We are seeing robust demand for N3 and we expect a strong ramp in the second half of this year, supported by both HPC and smartphone applications. N3 is expected to continue to contribute mid-single-digit percentage of our total wafer revenue in 2023. Our N2 technology development is progressing well and is on track for volume production in 2025. Our N2 will adopt a narrow sheet transistor structure to provide our customers with the best performance, cost, and technology maturity.

Adam Chang’s analyst take:Apple is the sole customer expected to adopt TSMC’s 3nm technology in its A17 Bionic and M3 chips during 2023. TheQualcommSnapdragon 8 Gen 4 processor is also anticipated to join the TSMC 3nm family (N3E) in 2024. Moreover, Intel is likely to adopt TSMC’s 3nm technology for its Arrow LakeCPU, scheduled to launch in H2 2024.

Results summary

Q2 2023resultsbeatslightly:TSMC reported $15.67 billion in sales, slightly above the midpoint of guidance. EPS beat consensus due to higher non-operating income. Both GPM and OPM slightly beat guidance thanks to favorable FX and cost control efforts.

Q3 2023guidance in line:管理指导16.7美元- 50亿美元(+ 9%不可小觑midpoint), gross margin in the range of 51.5%-53.5%, and operating margin in the range of 38%-40%. The gross margin dilution resulting from the N3 ramp-up would be 2-3 percentage points in Q3 2023 and 3-4 percentage points in Q4 2023. This impact would persist throughout the entire year of 2024, affecting the overall gross margin by 3-4 percentage points. Notably, this dilution is higher than the 2-3 percentage points gross margin dilution experienced during the N5’s second year of mass production in 2021.

2023revenue guidance revised down but expected:TSMC revised down the full-year revenue guidance to -10% YoY. The management sees weaker-than-expected macroeconomics in H2 2023 affecting the demand for all applications except for AI.

Strong AIdemand, 50% revenue CAGR forecast:AI revenue currently makes up 6% of TSMC’s total revenue. The company anticipates a remarkable compound annual growth rate (CAGR) of nearly 50% from 2022 to 2027 in the AI sector. As a result of this significant growth, the AI revenue percentage share in TSMC’s total revenue is projected to reach the low teens by 2027.

CoWoScapacity expected to double by 2024 end:TSMC is experiencing strong demand in the AI sector, with sufficient capacity for the front-end part but facing challenges in advanced packaging, particularly CoWoS.It is working with customers to meet demand in the short term while rapidly increasing capacity which it expects to double by the end of 2024, easing the current tightness.

Financial journalistGovindraj Ethirajtalks toNeil Shah, Our Research Vice President and talked aboutIndia’s Latest Big Bang Electronics projects and where will they land.

Podcast Chapter Markers

[00:56]Tata Steel sacks 38 employees, Sets A New Benchmark For Disclosures

[04:07]India’s Latest Big Bang Electronics Projects, Where Will They Land?with Neil Shah

[15:03]Hmm…IVF clinics are under the tax man’s scanner

[18:39]Mark Zuckerberg and Meta launch Threads, A Twitter Alternative, 10 million downloads and counting

[19:32]The CEOs Diet: The How & Why Of Breakfasts In Our Busy Lives

Joining the US-led effort to restrict chipmaking equipment exports to China, Japan has put in place restrictions that are more draconian than that of the US and where the Japanese state has effectively taken control of the country’ssemiconductorcapital equipment market.

Japan is imposing export restrictions on 23 types of equipment used to makesemiconductors.But instead of limiting the restrictions just to China, it has flipped the entire industry on its head.

Instead of being able to ship to anyone unless told not to, now the Japanese companies can’t ship to anyone unless they are allowed to.

This effectively gives the Japanese trade ministry life and death power oversemiconductorequipment, which may prove to be detrimental to the local industry’s health in the long run.

Unlike theUSDepartment of Commerce, where the presumption is denial of a license, it seems the Japanese Ministry of Trade will operate under the presumption of granting licenses.

Any other mode of operation would be highly detrimental to its own industry.

This represents a bigger step than what many analysts were expecting from Japan. It will really hinderChina’sability to manufacture chips at non-leading edge nodes below 20nm.

This was the weakness of the new measures announced by the US last October, as at 20nm-10nm, it is possible to build a fab using non-US equipment.

However, when you add Japan into the mix, this then becomes virtually impossible and there will be no point in buying machines from ASML, meaning that the combination of the US and Japan represents an effective embargo.

This means thatChinawill now have to rely on domestically produced capital equipment which is going to be a real problem.

尽管华为声称能够制造一个t 14nm, it did not say whether it could do so at volume with good yields which is what is required for Huawei to be able to use these chips economically in its products.

The net result is that Japan’s actions make the US actions far more effective and deal a blow to any workarounds that the Chinese may have found to build fabs without US equipment.

This reinforces the view that China is in real trouble when it comes tosemiconductors, which will hamper and slow its rise as a technological superpower.

That being said, there will be a likely bounce in the Chinese economy in H2 2023, although the lack of action on stimulating the economy remains a cause for concern.

If it comes, the rising tide will lift all boats and especially the beleaguered technology sector.

Micron: A display of weakness

China’s review of Micron on “national security” grounds is a tit-for-tat retaliation that shows just how weak its hand is in the game ofsemiconductorbrinksmanship.

The Cyberspace Administration of China (CAC) has said it would review Micron’s imports into China to ensure that using its products would not compromise the security of its information infrastructure.

It seems that this move has nothing to do with national security but is instead an attempt to damage US interests in China without compromising its own technological ambitions.

If China was really concerned about “national security”, it would be reviewing many other companies. But a blockade on the import of products from many of these companies would hurt China just as much as the US, if not more.

In the case of Micron, China can still buy the same products from South Korea or Japan with no ill effects on its development of technology.

This is precisely why Micron has been targeted. It is unlikely that other companies that export chips to China will be targeted as it would do more harm than good.

The move is also unlikely to give China much in the way of negotiating leverage and so this will prove to be an isolated incident that is pretty irrelevant to the overall technological and ideological struggle.

(This is a version of a blog that first appeared on Radio Free Mobile. All views expressed are Richard’s own.)

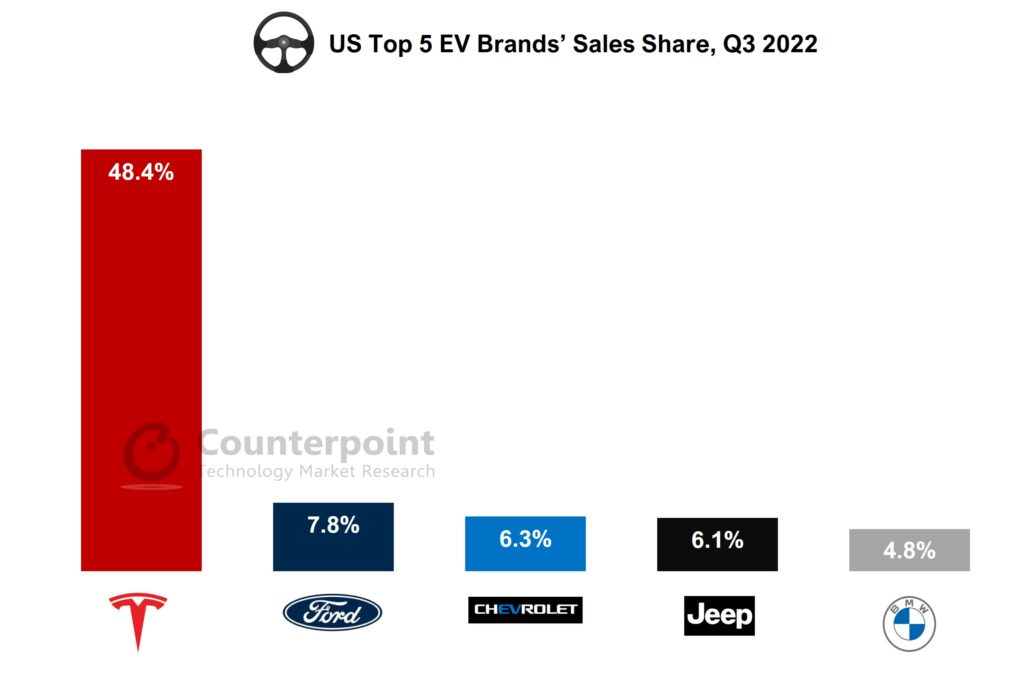

EV sales in the US grew by 52% YoY during Q3 2022.

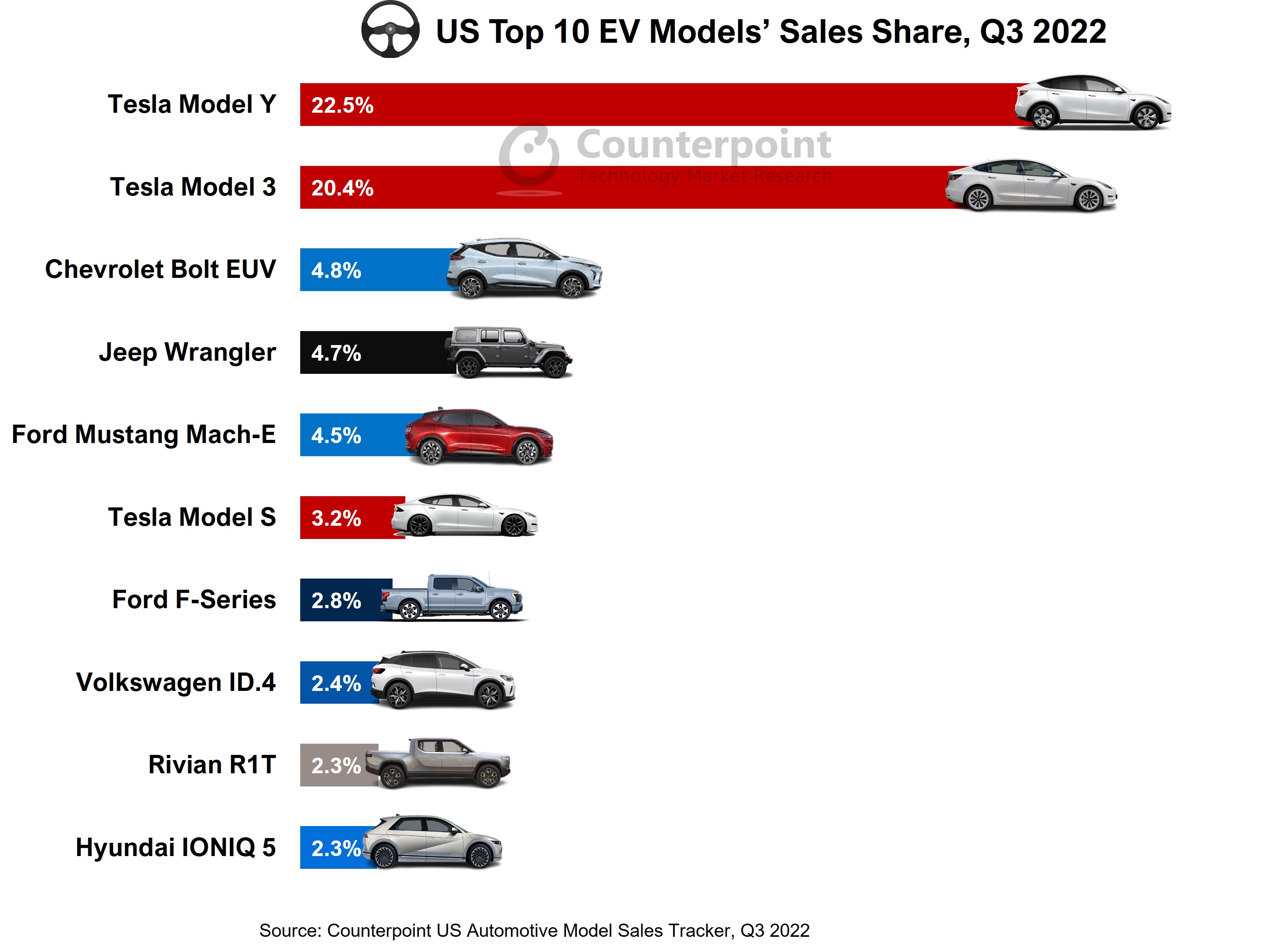

Top 10 EV models constituted almost 70% of EV sales.

US EV sales are expected to exceed 10 million units annuallyby 2030.

New Delhi,London,San Diego, Buenos Aires, Hong Kong, Beijing, Seoul –January 4, 2023

美国电动汽车(EV) * * *增长了almo销售st 52% YoY during Q3 2022 despite macroeconomic headwinds, according toCounterpoint Global Passenger Vehicle Model Sales Tracker.Battery EVs (BEVs) constituted over 80% of the total US EV sales. BEV sales grew by more than 78% YoY during Q3. Tesla’s Q3 sales eclipsed the next 15 brands combined.

Commenting on market dynamics,Associate DirectorHanish Bhatiasaid, “Overall US passenger vehicle sales will likely suffer due to macroeconomic pressures until at least mid-2023. Higher interest rates are hitting both loan and leasing routes to ownership. However, the affordability of EVs will be revitalized once EV policies and credit subsidies take effect.”

Source: Counterpoint Global Passenger Vehicle Model Sales Tracker, Q3 2022

Market summary

Teslasales in the US grew by more than 56% YoY during the quarter. Although Tesla has had some headwinds in meeting orders and delivering vehicles, it has remained the undisputed market leader for at least the previous 19 quarters. The Model Y and Model 3 are its most sold models.

Fordsold over 18,000 EV units during Q3, registering almost 132% YoY growth. With the introduction of the electric version of the best-selling F-150, the company has been able to mark its position in the US EV market.

Chevroletcatapulted its EV sales growth rate by 225% YoY to over 14,000 units. The Bolt and Bolt EUV are the only two Chevrolet EV models being offered currently. The Bolt EUV sales volume almost quadrupled from the previous year. The brand is on track to introduce three new EV models – Silverado EV, Equinox EV and Blazer EV.

Thetop 10 best-selling EV modelsconstituted almost 70% of the country’s EV sales in Q3. Tesla’s Model Y has been the best-selling EV model since the third quarter of 2020.

Commenting on the market outlook,Research DirectorJeff Fieldhacksaid, “Tax credits are expected to boost EV demand. Moreover, a price reduction is expected as more battery manufacturing firms are being set up across the North American continent. Batteries constitute 40% to 45% of the cost of EVs. The availability of multiple battery suppliers and a decrease in logistics costs for batteries will positively impact the US EV market. EV sales in the US are expected to exceed 10 million units annually by 2030 at a CAGR of 37%, according to Counterpoint’sGlobal Passenger Vehicle Forecast.”

*For EVs, we consider only BEVs and PHEVs. This study does not include hybrid EVs and fuel-cell vehicles.

**Sales refer to wholesale figures, i.e. deliveries from factories by the respective brands/companies.

Feel free to reach us at press@www.arena-ruc.com for questions regarding our latest research and insights.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

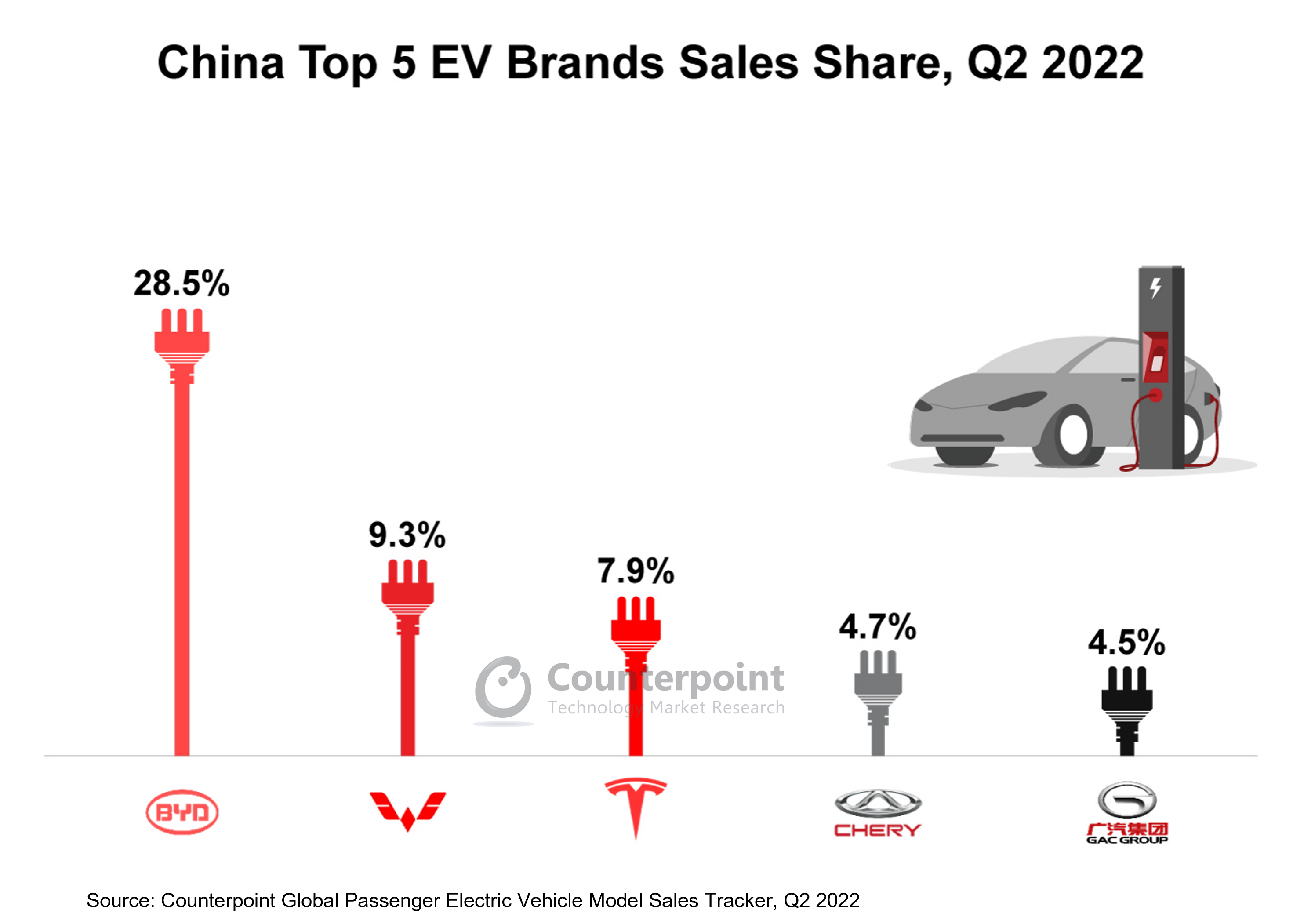

BYD led China’s EV market, followed by Wuling, Tesla, Chery and GAC Group.

Top 10 EV models in China accounted for more than 44% of the country’s total Q2 2022 EV sales.

One in four cars sold in China will have an electric powertrain by the end of 2022.

New Delhi,Beijing, London,S迭戈,布宜诺斯艾利斯,香港、首尔——September 15, 2022

中国2022年第二季度客运电动汽车(EV) sales* almost doubled from that a year ago, despite the quarter being a weak one, according to Counterpoint’sGlobal Electric Passenger Vehicle Model Sales Tracker.Pure battery electric vehicles (BEVs) accounted for almost 78% of total EV sales, while the remaining were plug-in hybrid electric vehicles (PHEVs). BYD remained the market leader, followed by Wuling and Tesla. Emerging brands, such as Xpeng Motor, Neta (Hozon Auto), Leapmotor, Li Auto,NIOand AITO (Seres), proved to be strong competition for the top players.

Commenting on the market dynamics,Senior AnalystSoumen Mandalsaid, “China is a mature EV market but it still has immense potential to expand further. Fresh COVID-19 cases from March 2022 onwards and the supply chain crisis due to theRussia-Ukrainewar have adversely affected the Chineseautomotiveindustry. Had it not been for these factors, the China EV market would have achieved sharper growth. Theprice hikeby most Chinese automakers during March, followed by strict COVID-19 lockdowns during April and May around Shanghai, restricted growth in the domestic automotive industry. Although better results are expected in H2 2022, the economic downturn, energy crisis, supply chain bottlenecks and rising geopolitical tensions may hinder market growth, especially for EVs.”

Market summary:

BYD Auto:BYD, which has been the market leader in China since mid-2021, sold more than 353,000 EV units in Q2 2022. The automaker’s BEV segment grew 229% YoY while its PHEV division expanded 312% YoY. The company’s decision to discontinue the production and sales of pure ICE vehicles since March 2022 allowed it to focus on electrified vehicles and become the global EV leader.

Wuling: The SAIC-GM-Wuling joint venture has been very successful in China. Wuling’s Hongguang MiniEVhas been the flag bearer for the brand since the end of 2020 and has been China’s best-selling EV model for more than the past 18 months. Wuling’s EV sales grew almost 16% YoY during Q2 2022.

Tesla: The pandemic-related lockdowns in Q2 2022 severely hurtTesla’s business. Production ramp-ups were almost completely halted in April and May during which its sales in China fell 49% YoY to reach the lowest number for the automaker since 2020. The situation improved only after production resumed to full capacity in June 2022. The company ended Q2 2022 on a positive note with 10% YoY growth in sales.

Commenting on the EV infrastructure development,Associate DirectorBrady Wangsaid, “Direct subsidies toconsumershave played a big role in increasing EV adoption across China. Now, as the government plans to phase out direct subsidies to consumers, the country’s dual credit policy for EV production is likely to play an important role. Moreover, many laws that were implemented to save China’s automotive industry from the onslaught of foreign OEMs are being lifted as domestic brands have matured and are now even penetrating other markets, such as Europe andSoutheast Asia.Moreover, China’s component industry, especially the battery supply chain, has been strong and is expected to maintain its global dominance. Apart from the increased EV sales and a strong battery supply chain, China also has a goodcharging networkand domestic players are currently focusing on developing proper battery recycling facilities. China is at the forefront in every aspect of the EV ecosystem and has become the leading global figure in the EV space.”

The top 10 EV models in China accounted for more than 44% of the country’s total EV sales in Q2. Wuling’s Hongguang Mini EV remained the undisputed best-selling model for the quarter followed by BYD’s Song and Tesla’s Model Y. However, in June 2022, the Model Y overtook the Hongguang Mini EV to become the top-selling model. China’s EV market is dominated by domestic brands, along with Tesla. Six of the top 10 models were from BYD, among which the BYD Yuan Plus and BYD Dolphin were released after Q2 2021.

Source: Counterpoint Global Passenger Electric Vehicle Model Sales Tracker, Q2 2022

Commenting on the market outlook,Research Vice PresidentNeil Shahsaid, “EV sales in China constituted 15% of the total passenger vehicle sales in 2021. According to Counterpoint’s Global Passenger Car Forecast, EV sales are expected to cross the 6-million-unit mark by the end of this year. The market will likely remain subdued due to the ongoing chip crisis,COVID-19 outbreaks, energy crisis, geopolitical tensions and rising consumer inflation. However, we believe one in four cars sold will have anelectric powertrainby the end of 2022.”

*Sales here refer to wholesale figures, i.e. deliveries out of factories by respective brands/companies.

*在电动车(电动车),我们正在考虑only battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs). Hybrid electric vehicles and fuel cell vehicles (FCVs) are not included in this study.

Feel free to reach us at press@www.arena-ruc.com for questions regarding our latest research and insights.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

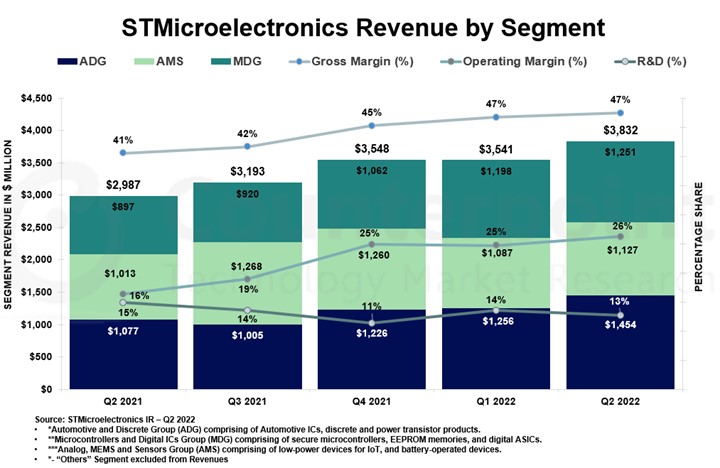

Net revenue grew 28.3% YoY as the company recorded decent growth in all product groups and subgroups. Gross margin of 47.4% came in above the norm due to favorable pricing and improved product mix.

STMicro recorded net revenues of $3.84 billion for Q2 2022, primarily driven by the strong demand from factory automation, robotics and industrial infrastructure and automotive sectors.

STMicro is teaming up with 20+ car makers in power train electrification using its silicon carbide (SiC) MOSFET. Automotive market continued to see strong demand in Q2, with the ongoing electrification and digitalization transformation across the supply chain and automotive industry.

Automotive:Strong demand was seen in Q2 across theautomotivesupply chain due to the ongoing electrification and digitalization of the industry. Between the automotive and industrial markets, STMicro has around 102 projects spread over 77 customers. Multiple wins have been recorded in silicon carbide (SiC), power module and other electrical vehicle-related applications for Tier 1 automotive manufacturers. The Volkswagen Trinity project is a collaborative effort between Volkswagen Group and STMicro that aims to address multiple applications with new zonal architectures by adding an MCU and system-on-chip.

Industrial:This sector has seen a tremendous increase in semiconductor content due to the increase in digitalization, power management and efficiency in devices and systems. Design wins have been seen in intelligent power switches, MOSFETs and wireless charging solutions.

Consumer electronics and PC:This segment has shown some signs of softening. STMicro is focusing on selected high-volume smartphone applications and multiple design wins for wireless charging solutions in smartphones and smartwatches. Some of the consumer application design wins include a pressure sensor for hard disks, time-of-flight senses forlaptops, and MasterGaN family for high-power-density charging adapters.

Segment revenues

Automotive and Discrete Group (ADG)revenues increased 35.1% on growth in both automotive and power discrete. ADG has seen increased capability in manufacturing.

Analog, MEMS and Sensors group (AMS)revenues grew 11.3% on higher analog, MEMS and imaging product sales.

Microcontrollers and Digital ICs Group(MDG)revenues increased 39.5% on growth in both microcontrollers and RF communications.

Company forecast

Revenues:Q3 2022 net revenues will be around $4.24 billion at mid-point, growing 32.6% YoY and 10.5% QoQ. Also, for the full year of 2022, revenues are expected to be in the range of $15.9 billion-$16.2 billion, driven by the strong demand in ADG. ADG and MDG will register growth, but AMS will be affected by tight capacity.

Demand and supply:Strong customer demand and planned investments will increase capacity in 2022. Manufacturing capacity for some products is fully saturated by the strong demand from factory automation,roboticsand industrial infrastructure andautomotivesectors. Backlog visibility is now above 18 months and well above the company’s current and planned manufacturing capacity through 2023.

Capex and investment:Capex in Q2 2022 was $809 million compared to $438 million in Q2 2021. For 2022, capex investment is expected to be in the range of $3.4 billion-$3.6 billion. Financial support from France for the 300-mm wafer fab in Crolles will result in a high-volume manufacturing plant ranging from 90nm to 28nm and covering embedded non-volatile memory, RF mixed signal and other technologies.

Key takeaways

In the long term, the 300-mm semiconductor manufacturing facility will be a major enabler for ST’s $20-billion-plus revenue ambition. The new fab in Italy will ramp up the production of SiC and GaN products in H1 2023.

High-volume applications such assmartphones, communication equipment, computers and5G infrastructureproducts have resulted in an increase in semiconductor content per device. In the long term, power-related semiconductor and analog content will further increase as more and more people are embracingEVsand 5G-related equipment.

STMicro continues to drive design wins for car electrification, and with the increase in the use of silicon carbide, the revenue target is expected to reach $1 billion by 2023.

STMicro’s major growth driver in 2023 will be the automotive segment through the company’s alliance with Volkswagen Group.

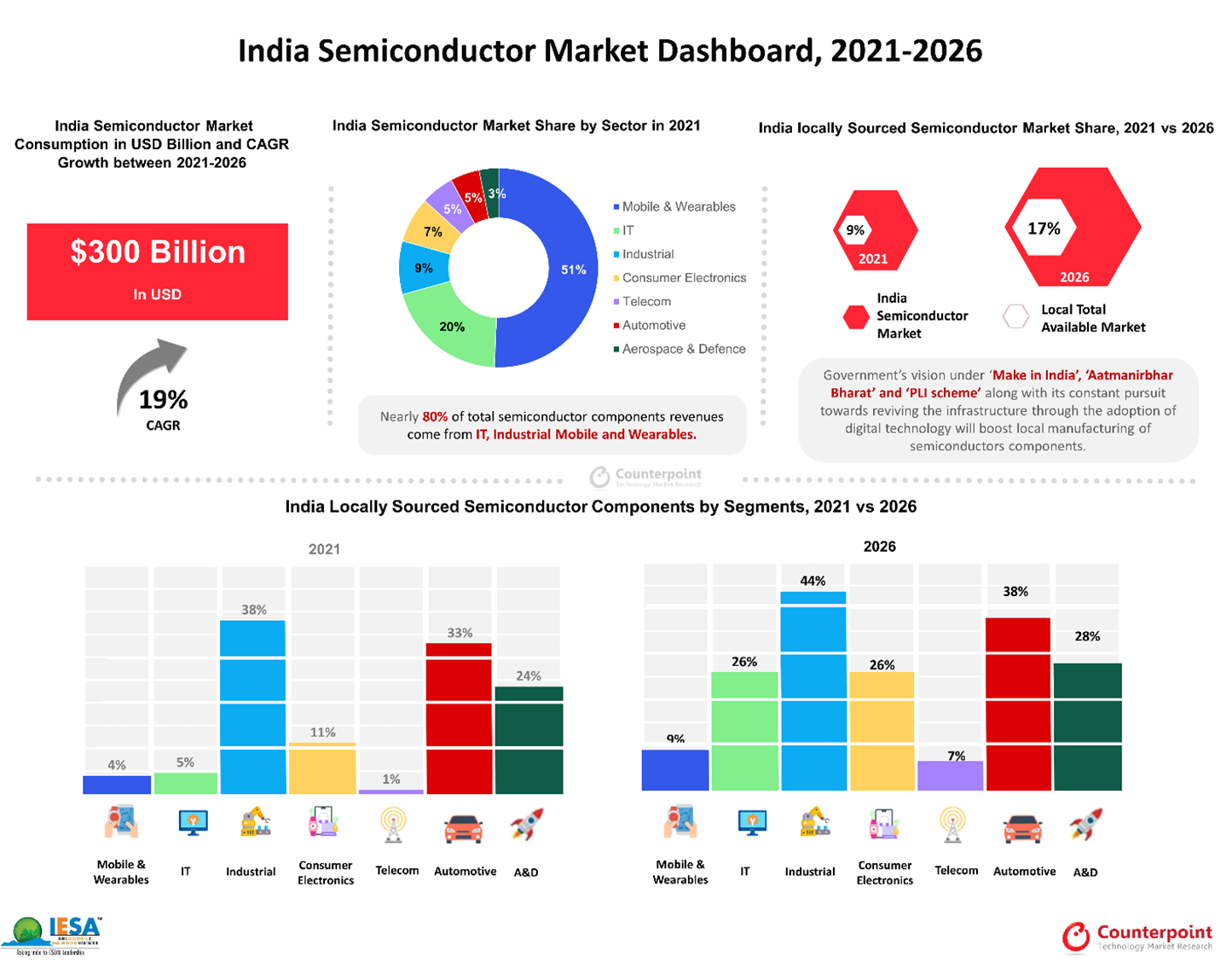

Mobile and wearables, IT and industrial segments currently contribute around 80% of the semiconductor revenues in India.

‘Make in India’ and Production Linked Incentive schemes will boost local sourcing of semi-components in the coming years.

Further policy reforms and building of a semiconductor ecosystem will reduce reliance on imports going forward.

New Delhi, Seoul, San Diego, Buenos Aires, London, Hong Kong, Beijing – August 16, 2022

India’ssemiconductor componentmarket will see its cumulative revenues climb to$300 billion during 2021-2026, according to the‘India Semiconductor Market Report, 2019-2026’, a joint research by the India Electronics & Semiconductor Association(IESA)andCounterpoint Research.方面是行业组织代表the ESDM and intelligent electronics industry in India. It acts as a trusted knowledge partner to the central and state governments, helping devise policies and incentives for the industry to attract investments into India. The comprehensive research on India’ssemiconductor marketfocuses on the bottom-up modelling unit as well as revenue demand for semiconductor components covering the entireBill of Materials (BoM)of multiple end-device and equipment categories across seven major sectors in India –MobileandWearables,Information Technology,Automotive,Industrial,Telecom, Aerospace and Defence, andConsumer Electronics– from domestic consumption as well as export perspective. The report provides detailed recommendations, potential policies and a framework for building a robust domestic semiconductor ecosystem to boost local production and sourcing.

Source: India Semiconductor Market Report

IESA CEO and PresidentKrishna Moorthysaid, “Before the end of this decade, there will be nothing that will not be touched by electronics and the ubiquitous ‘chip’. Be it fighting carbon emissions, renewable energy, food safety, or healthcare, thesemiconductorchipwill be all-pervasive. Imagine this – all children all over India get educated in virtual classrooms by the country’s best teachers.The chip makes it possible.Again, imagine everyone in the country gets quality healthcare and diagnostics done remotely. Medicines are delivered by drones at your doorstep, even in the farthest villages of India. Thechipwill make it possible, and we will see this in front of our eyes very soon. Let us make India the semiconductor nation.”

India is poised to be the second largest market in the world from the perspective of scale and growing demand for semiconductor components across several industries and applications.This demand is being pushed by the increasing pace of digital transformation among the country’s consumers, enterprises and public sector through the adoption of new technologies, from advanced connectivity to content consumption to the cloud. These coversmartphones, PCs, wearables, cloud data centers, Industry 4.0 applications, IoT, smart mobility, and advancedtelecomand public utility infrastructure.

Mobile and wearables,它和工业部门造成了lmost 80% of the semiconductor revenues in India in 2021.Commenting on the mobile and wearables industry,Research Director at Counterpoint ResearchTarun Pathaksaid, “The mobile and wearables sector was the biggest contributor to India’s semiconductor industry in 2021.Mobile deviceshave become a primary tool for internet connectivity given that broadband andlaptop/PCpenetration remains low. In the last five years, the ‘consumer digital transformation’ has accelerated with the availability of cheap mobile internet, andmobile deviceshave connected a big part of the Indian population. Also, the gradual shift from feature phones tosmartphoneshas been generating increased proportions of advanced logic processors, memory, integrated controllers, sensors and other components. This will continue to drive the value of the semiconductor content insmartphones, which is still an under-penetrated segment in India, aided by the rise of wearables such assmartwatchandTWS.”

Commenting on the potential opportunity in the mid-to-long term,CounterpointResearch Vice PresidentNeil Shahsaid, “The next big boom for semiconductor components will come from across sectors. However, thetelecomsector with the advent of5Gand fiber network rollout will be a key catalyst in boosting the semiconductor components consumption. This consumption will not only come from the advanced semiconductor-heavy 5G andFTTH networkinfrastructure equipment, which will contribute to more than 14% of the total semiconductor consumption in 2026, but also from the highly capable AI-driven5Gendpoints, fromsmartphones,tablets,PCs, connected cars, industrial robotics to private networks. Also, ongoing efforts to embrace cleaner and greener vehicles (electric vehicles) will provide an impetus for theautomobile industryto adopt advanced technologies, which in turn will boost the demand for semiconductor components in India.Consumer electronics, industrial, andmobile and wearableswill be the other key industries for the growth of the semiconductor market in India. Further, this semiconductor demand will not only be driven by domestic consumption but also by the growing share of exports.”

In 2021, India’s end equipment market stood at $119 billion in terms of revenue. It is expected to grow at a CAGR of 19% from 2021 to 2026.The Electronic System Design and Manufacturing (ESDM) sector in India will play a major role in the country’s overall growth, from sourcing components to design manufacturing. Thesemiconductor industryin India is on a path to immense growth over the next few years to help India’s economy reach the next stage for both domestic consumption and exports.While the country is becoming one of the largestconsumers of electronic and semiconductor components, most components are imported, offering limited economic opportunities for the country. Currently, only 9% of this semiconductor requirement is met locally.

The demand for semiconductors is growing astronomically worldwide. However, multiple factors, including the pandemic and global geopolitical events, have heavily impacted the manufacturing of the components. This research is aimed at analyzing the market situation, manufacturing supply chain, and prospects for India as a premier manufacturing destination not only for finished goods but also forsemiconductor components.目前当地生产低,印第安纳州ia has immense potential to become a leading semiconductor component supplier in the coming years, provided the talent pool and resources are utilized correctly. The government’s initiatives, from‘Make in India’ to Production Linked Incentive (PLI), will help accelerate this journey but will need some additional reforms to increase local manufacturing and sourcing of semiconductor components.If this is done, the semiconductor market can be a major contributor to economic growth, and India’s push to become a $5-trillion economy.

IESAVice PresidentSunil G Acharyasaid, “半导体swill be inside everything intelligent. India is becoming a tech-centered growth story with advancing technologies and innovation being integral to democratizing access. The semiconductor study will play a major role inIndia’sgrowth. A large young population combined with an increased focus on digitalization, advancing skill levels, growing manufacturing and foreign investment traction will take India’s semiconductor industry to the next level in the coming years.”

Commenting on the current stage of local manufacturing,Research Analyst at Counterpoint ResearchShivani Parasharsaid, “To achieveIndia’ssemiconductor vision, a robust and indigenous technology ecosystem will be required to build on the existing policy foundation throughPLI-like schemes.Renewed focus is needed for incentivizing the country’s design ecosystem in a manner that helps create a stronger foundation for design-led manufacturing and allied sectors, be it for local consumption or exports. This strategy will transform the landscape in the coming years to drive local sourcing trends.The share of local sourcing is expected to grow to over 17% by 2026. This translates into a six-fold rise in potential locally-sourcedsemiconductorrevenues.”

IESA Vice President (Public Policy, Government and Corporate Relations)Anurag Awasthisaid, “From safety razors to space shuttles, everything will be powered by thechip.Let us ensure ourchipsare not down in the world of tomorrow! Keeping this as an aim, MeitY is working further towards makingIndiaone of the next technology powerhouses, especially in apandemic-struckworld where there has been a realization of the need for more flexible and diverse supply chain ecosystems. The government is keen to leverage India’sexisting strengths inmobile manufacturing, software and start-up hubs for other critical industries in the ESDM sector.”

Research Analyst at Counterpoint ResearchPriya Josephadded, “Government policies includingPLI, New Electronics Policy, 2019, Electronics Manufacturing Clusters, and Scheme for Promotion of manufacturing of Electronic Components and半导体s(SPECS) are all being equipped to boost domestic design, manufacturing and assembly. To help drive more initiatives under the themes of Make inIndiaand Digital India, thegovernment, in its last budget, pushed the total allocation to $936.2 million. This step not only aims to incentivize India-based manufacturing but also catalyze investments in the sector to support job creation, ease of doing business, import reduction and export promotion.”

To access the full report, please contact IESA at the coordinates below.

Feel free to contact us atpress(at)www.arena-ruc.comfor questions regarding semiconductor research and insights.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

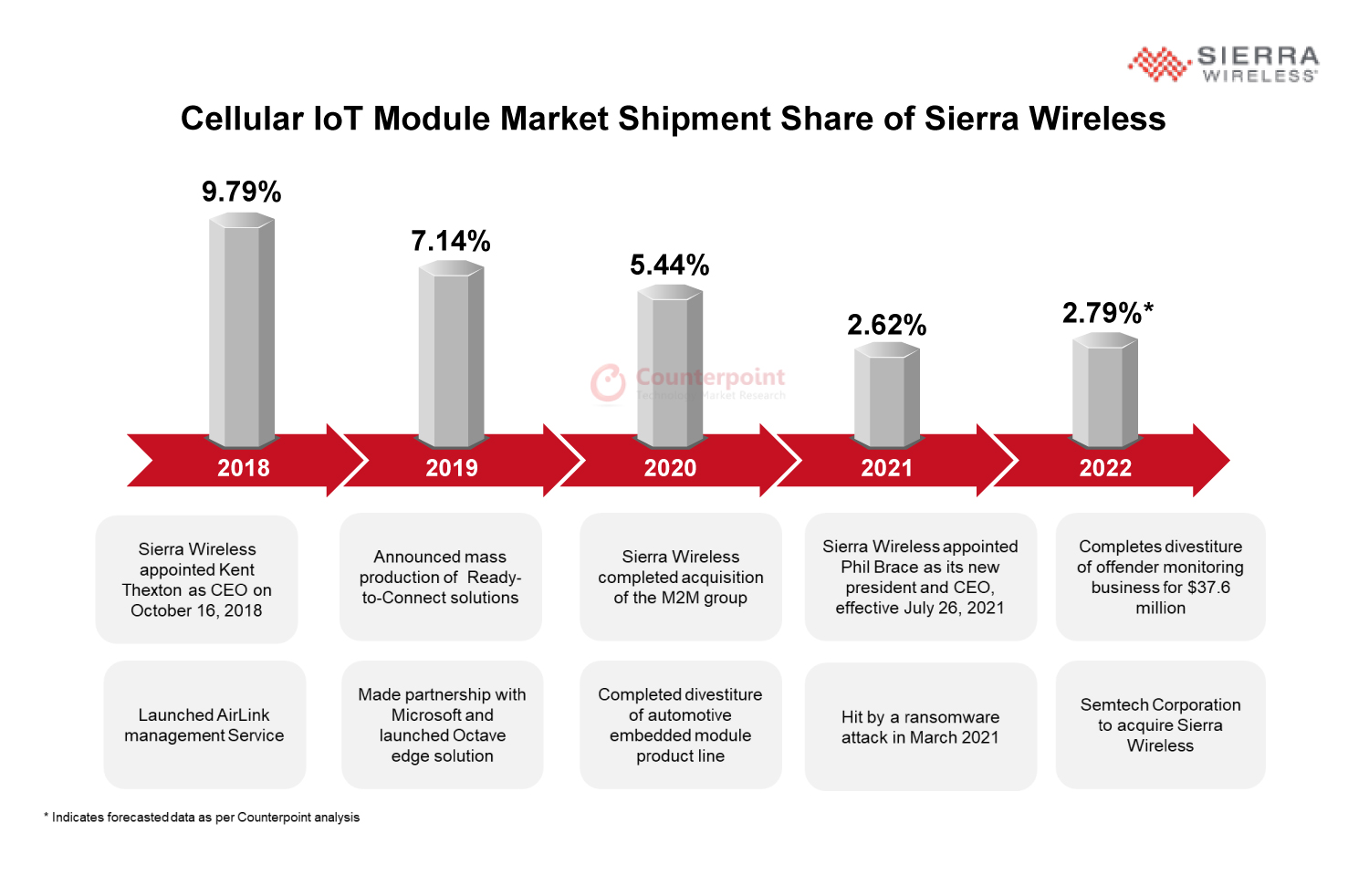

US-based semiconductor manufacturer and LoRa pioneer Semtech announced a $1.2-billion deal on Wednesday to acquire Canada-based cellular IoT module and device supplier Sierra Wireless. The deal comes after last week’s merger deal between Telit and Thales’ cellular IoT business. The IoT module market has entered a consolidation phase and we can expect a few more announcements in the near future.

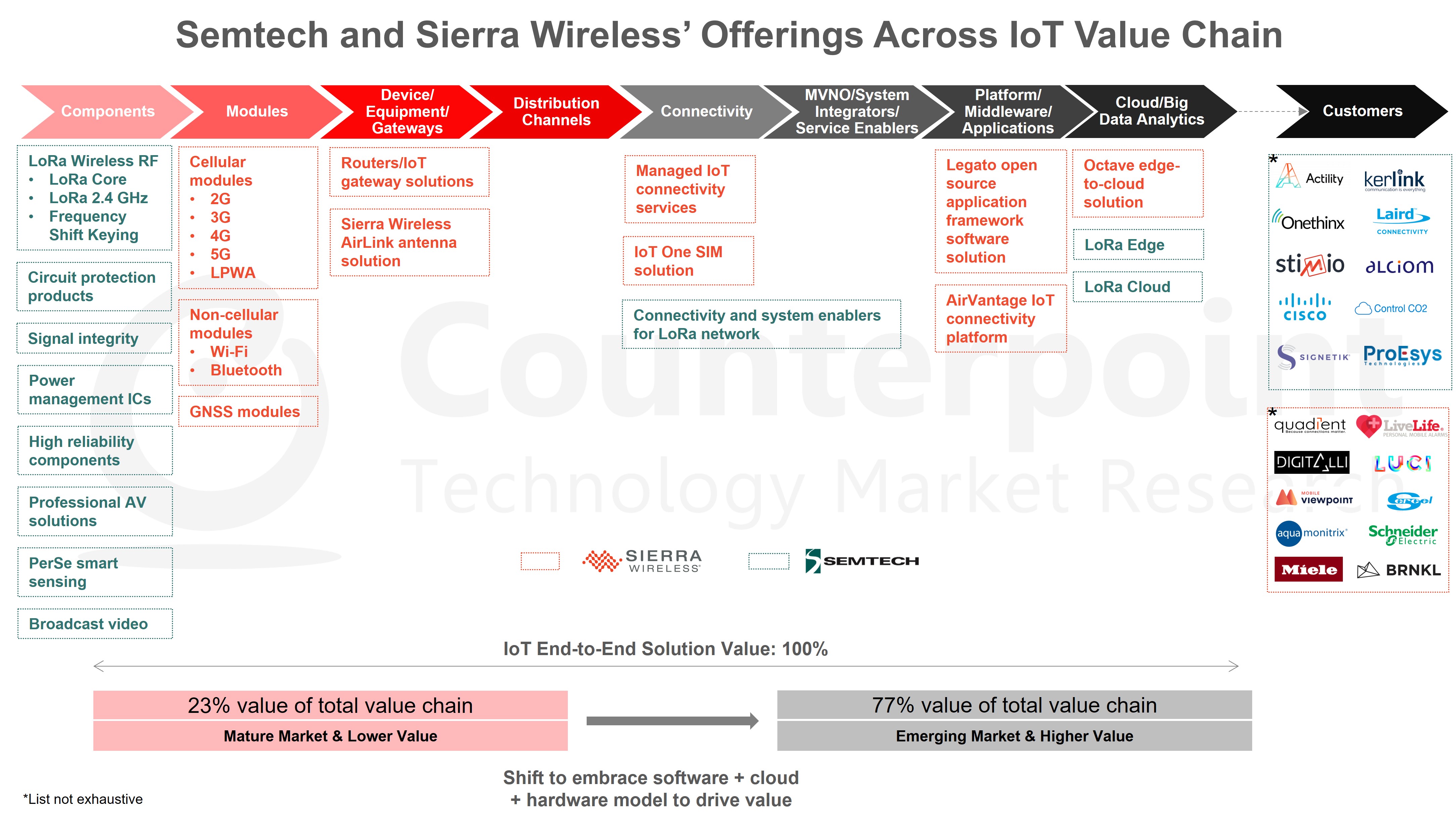

TheIoT modulemarket is fragmented. Many brands are struggling to improve performance, scale up products and face competitors. Some players are moving towardsservices, which comprise 77% value of the total IoT value chain, for better revenue opportunities instead of sticking to hardware only. For example,u-bloxacquired Thingstream in 2020 to generate more revenue and offer complete IoT solutions, from chipset to cloud. In some cases, companies are trying to build up their ownsupply chainecosystem through integration. For example, Quectel entered theIoTantenna space last year. In the future, we may witness some large players offload their cellular IoT module business which is not a core business for them.

The Semtech-Sierra Wireless deal is an important announcement for theIoTspace. It can change offerings in the IoT industry. Here are somekey takeawaysfrom this deal from Counterpoint analysts:

塞拉无线主要集中在细胞business, whereas Semtech is focused on the non-cellular business. The ultra-low power benefits of LoRa and higher-bandwidth capabilities of cellular networks will bring innovation to IoT use cases. They can also solve problems faced inmassive IoTadoption across all segments.

International brands such as Sierra Wireless, Telit, Thales and u-blox were struggling to compete with Chinese module vendors such asQuectel, Fibocom and MeiG in terms of scale and bringing innovation to the field.

Sierra Wireless divested its auto business in 2020 to focus on the router/CPE segment but the COVID-19 pandemic, supply chain disruptions and ransomware attack hit Sierra Wireless’ efforts to regain its market share last year. Interestingly, the automotive spin-off business was acquired by a consortium led by Chinese module vendor Fibocom.

We also witnessed a corner-room change at Sierra Wireless to revive brand glory when Phil Brace replaced Kent Thexton as the CEO in July 2021.

This year, Sierra Wireless divested its Omnilink offender monitoring business to Sentinel for $37.6 million. This was not a core business for the company and it offloaded Omnilink to focus more on the services industry. Product segments can generate revenue for one time, whereas services can generate revenue on a recurring basis. That is why we have been seeing many IoT module players shifting towardsIoT platforms, cloud and services.

According to itschip-to-cloudstrategy for IoT adoption, Semtech aims to offer solutions across the IoT value chain. However, it has no good presence in the module, device and platform categories. Moreover, LoRa isn’t suitable for each IoT application. LoRa and cellular technologies may complement each other in serving segments across the IoT value chain.

Sierra Wireless will bring a rich experience of cellular IoT modules, cellular gateways and cloud service platform to Semtech, while Semtech will offer LoRachips, LoRa gateways and cloud services. In the future, we may see more hybridcellular+LoRasolutions instead of dual cellular module-based solutions. In this type of application, the cellular module can be used for data communication and LoRa can be used for device management and other applications where a low payload is required. This can change offerings in the IoT module space and help Semtech increase its market share in the cellular space too.

Semtech already has a good hold on smart meter, smart city, industrial, smart grid and asset-trackingapplicationsthrough LoRa solutions. The addition of Sierra Wireless products will help Semtech targethigh-endmarkets such as security cameras, gateways,fleetand PC.

Outlook

The combined entity is looking for a 10x growth opportunity to reach a $10-billion serviceable addressable market (SAM) by 2027. To achieve this figure,IoT platformandcloud serviceswill play a pivotal role as these can contribute revenue on a recurring basis. At the same time, Semtech needs to be careful not to disrupt the standalone LoRa ecosystem partners and customers. We believe cellular+LoRa-based industrial applications such as security, smart campus, factory and private networks will be a big opportunity for Semtech.

COVID-19, along with the rise of advanced capabilities such as5G, AI andimagingtechnologies, has catalyzed the semiconductor demand for the last over two years. Monitoring the contribution of upstream players in the semiconductor value chain, which are actually building technologies and capacities, has become extremely important.

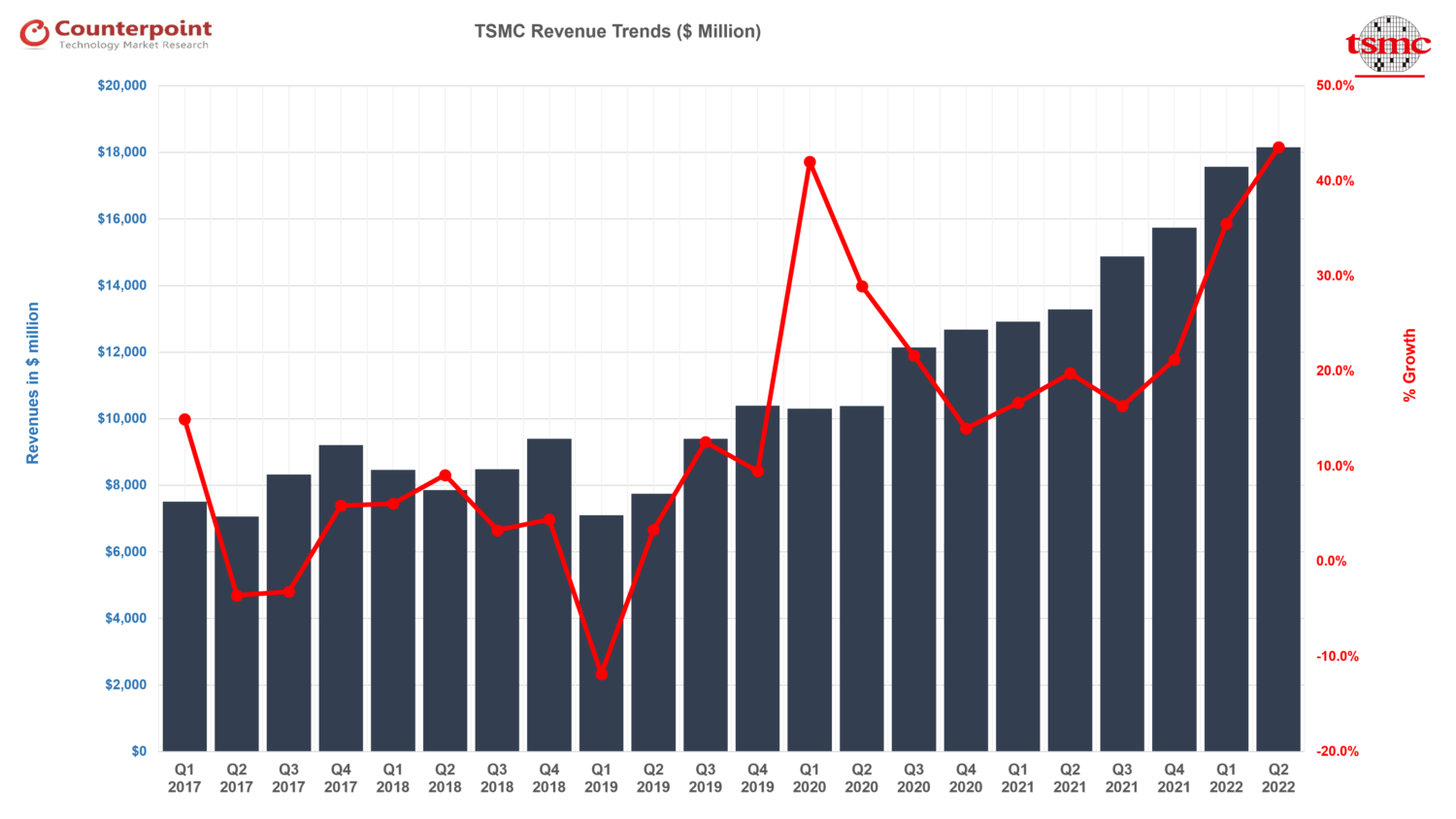

TSMC is a great benchmark for the health of the semiconductor industry considering it manufactures 70% of all keysmartphonechipsets. The company posted record earnings in Q2 2022 with growing advanced semiconductor content in processing (AI,GPU,SoC) and connectivity (5G) being the key factors.

Key financial highlights:

Net revenue increased 37% YoY to $18.2 billion driven by high-performance computing (HPC),IoTand automotive-related demand.

Gross margin and operating margin were at 59.1% and 49.1% respectively, up 3.5 percentage points on a favorable foreign exchange rate, cost improvement and value selling.

From the geographical perspective, North America accounted for the highest share (64%) of total net revenue.

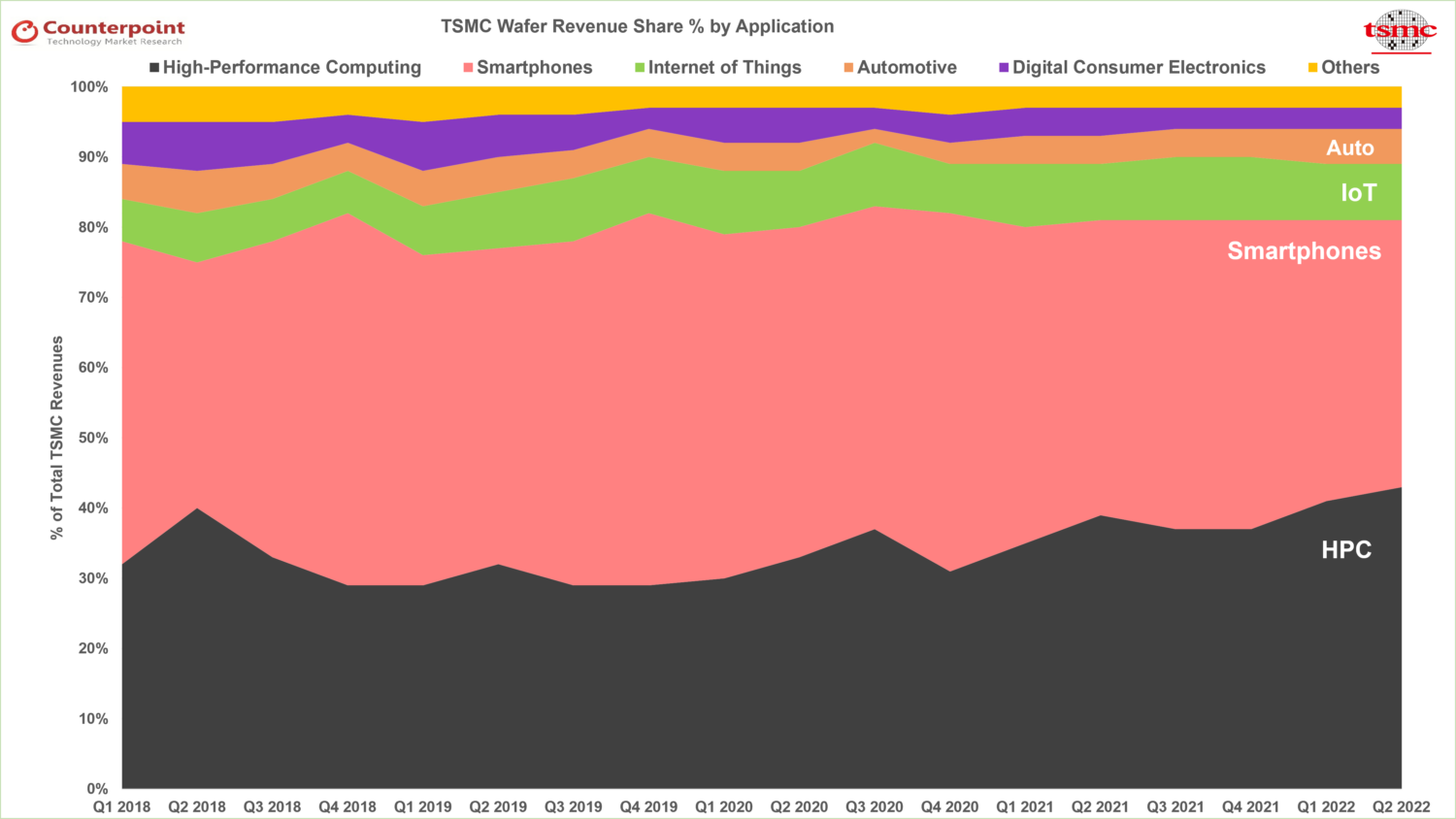

TSMC wafer revenues share

By application

Smartphones and HPC represented 38% and 43% of net revenues respectively, while IoT, Automotive, Digital Consumer Electronics (DCE) and Others represented 8%, 5%, 3% and 3% respectively.

HPC surpassed Smartphones in revenues thanks to Nvidia, Intel, AMD and others.

TSMC’s reliance onApple,QualcommandMediatekwas lesser as HPC surpassed Smartphones in revenue contribution.

Automotive semiconductor content was the dark horse.

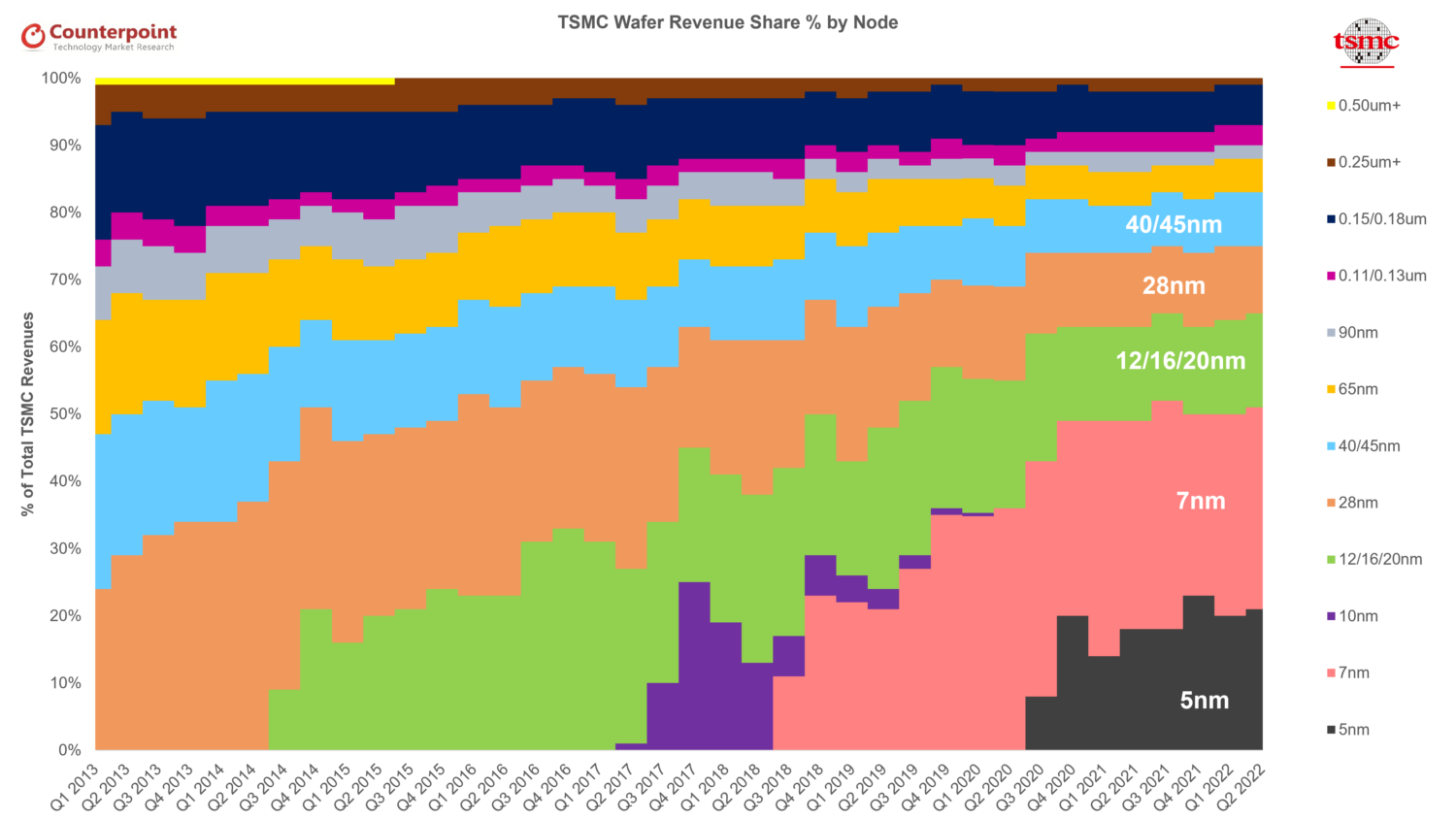

By node

5nm process technology contributed 21% of total wafer revenues in Q2 2022 while 7nm accounted for 30%.

Combined revenue from advanced process nodes with 5nm and 7nm accounted for 51% of total wafer revenues, thanks to growingcapex, making it very difficult for current and potential competition to catch up at least in next 10 years.

Double-digit growth was seen in matured nodes thanks to the rising need for chipsets in the IoT andautomotive.

N2 and N3 updates

N2 node will implement the platform scaling concept wherein benefits of power delivery schemes, advanced packaging and chiplet will be utilized to control cost and have an overall advantage.

N3 node will be the longest node to be used before migrating to N2 due to the introduction of TSMC FINFLEX architectural innovation, which offers flexibility to customers to create designs precisely tuned for their needs with functional blocks implementing the best-optimized fin configuration and integrated into the same chip.

The introduction of 3nm nodes will begin in H2 2022 and adoption by customers and revenue contribution will start in Q1 2023. The introduction of 3nm nodes will lower the gross margin by 2%-3% in 2023.

While the capex is growing, some of it will be spread out over quarters with theWFEvendors struggling with backlogs as building fab equipment also requires semiconductors! This will help TSMC realize healthy margins for the coming quarters and offset any gross margin decline due to N3 introductions.

Key takeaways

TSMC’s net revenue will cross $75 billion in 2022, which means it will surpass Intel’s revenues.

HPC will drive TSMC’s revenue growth in the long term and achieve a 15%-20% CAGR.

3D IC design solution System on Integrated Chips (SoIC) will account for a significant share of revenue in the long term due to its extensive application in HPC.

Efforts to resolve tool delivery schedule challenges in advanced and mature nodes through discussions with entire supply chain partners remains a top priority.

Growing silicon content, shipments and ASP will drive revenue growth in the long term.

Inventory adjustment will continue till Q1 2023 and ease off by H2 2023. However, long-term semiconductor demand will be firm.

In order to access Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not. Personal Information When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time. In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company. – Passwords are for user’s individual use – Passwords may not be shared with others – Users may not store documents in shared folders. – Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified. Accuracy of Information: While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links: This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience. This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.