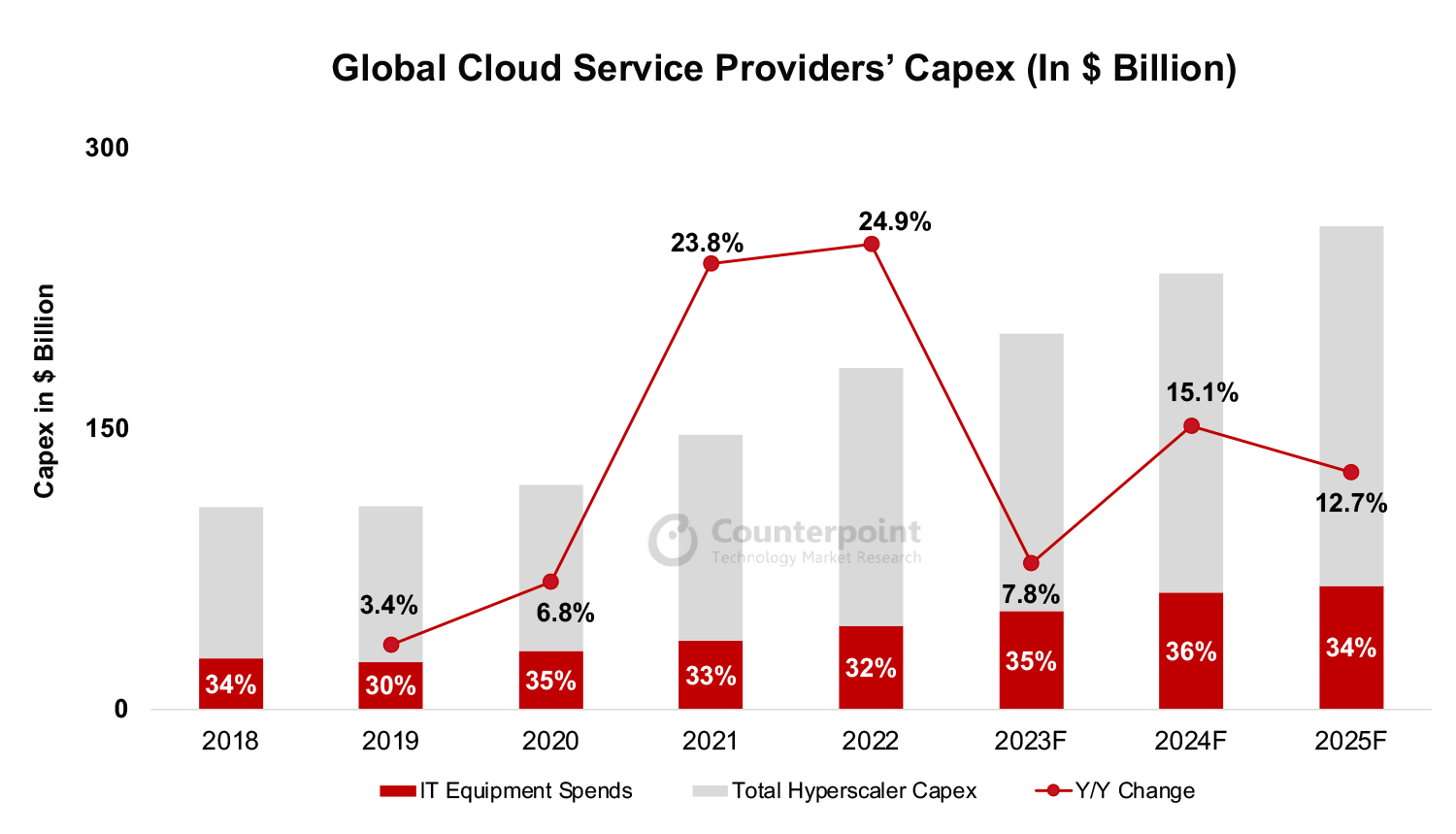

Cloud service providers’ capex is expected to grow by around 8% YoYin 2023 due to investments in AI and networking equipment.

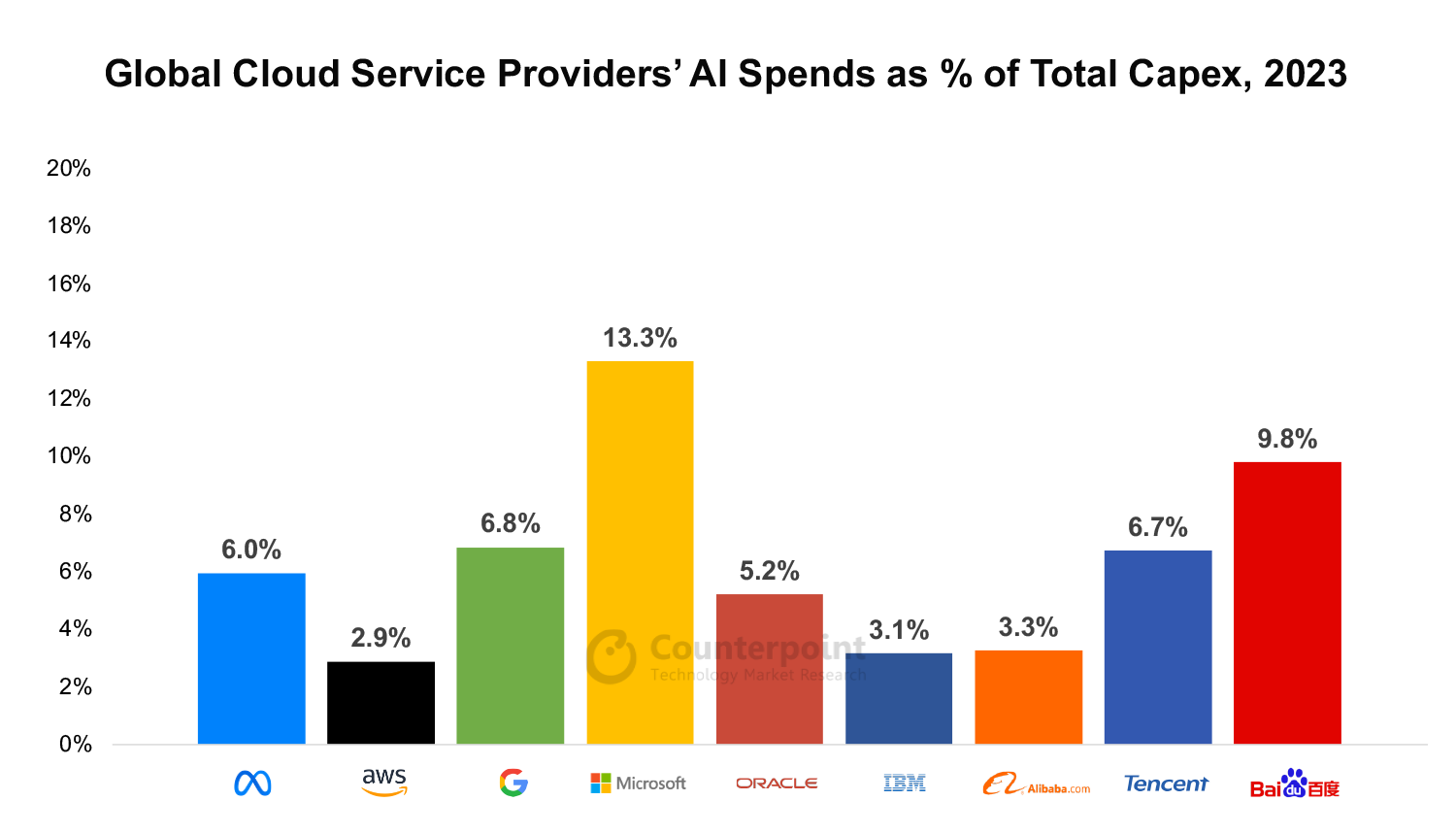

Microsoft and Amazon are among the highest spenders as they invest in data center development. Microsoft will spend over 13% of its capex on AI infrastructure.

AI infrastructure can be 10x-30x more expensive than traditional general-purpose data center IT infrastructure.

Chinese hyperscalers’ capex is decreasing due to their inability to access NVIDIA’s GPU chips, and decreasing cloud revenues.

New Delhi, Beijing, Seoul, Hong Kong, London, Buenos Aires, San Diego –July 25, 2023

Globalcloudservice providers will grow capex by an estimated 7.8% YoY in 2023, according to the latest research from Counterpoint’sCloud Service. Higher debt costs, enterprise spending cuts and muted cloud revenue growth are impacting infrastructure spend in data centers compared to 2022.

Commenting on the large cloud service providers’ 2023 plans,Senior Research Analyst Akshara Bassisaid, “Hyperscalers are increasingly focusing on ramping up theirAIinfrastructure in data centers to cater to the demand for training proprietary AI models, launching native B2C generative AI user applications, and expanding AIaaS (Artificial Intelligence-as-a-Service) product offerings”.

According to Counterpoint’s estimates, around 35% of the total cloud capex for 2023 is earmarked for IT infrastructure including servers and networking equipment compared to 32% in 2022.

Source: Counterpoint Research

Source: Counterpoint Research

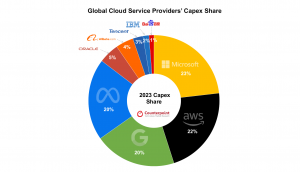

In 2023,MicrosoftandAmazon(AWS) will account for 45% of the total capex. US-based hyperscalers will contribute to 91.9% of the overall global capex in 2023.

Chinese hyperscalers are spending less due to slower growth in cloud revenues amid a weak economy and difficulties in acquiring the latestNVIDIAGPU chips for AI due to US bans. The scaled-down version – A800 of the flagship A100/H100 chips – that NVIDIA has been supplying to Chinese players may also come under the purview of the ban, further reducing access to AI silicon for Chinese hyperscalers.

Source: Counterpoint Research

Based on Counterpoint estimates, Microsoft will spend proportionally the most on AI-related infrastructure with 13.3% of its capex directed towards AI, followed byGoogle在6.8%左右capex. Microsoft has already announced its intention to integrate AI within its existing suite of products.

AI infrastructure can be 10x-30x more expensive than traditional general-purpose data center IT infrastructure.

Though Chinese players are investing a larger portion of their spends towards AI, the amount is significantly less than that of the US counterparts due to a lower overall capex.

The comprehensive and in-depth ‘Global Cloud Service Providers Capex’ report is available. Please contact Counterpoint Research to access the report.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the technology, media and telecom (TMT) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

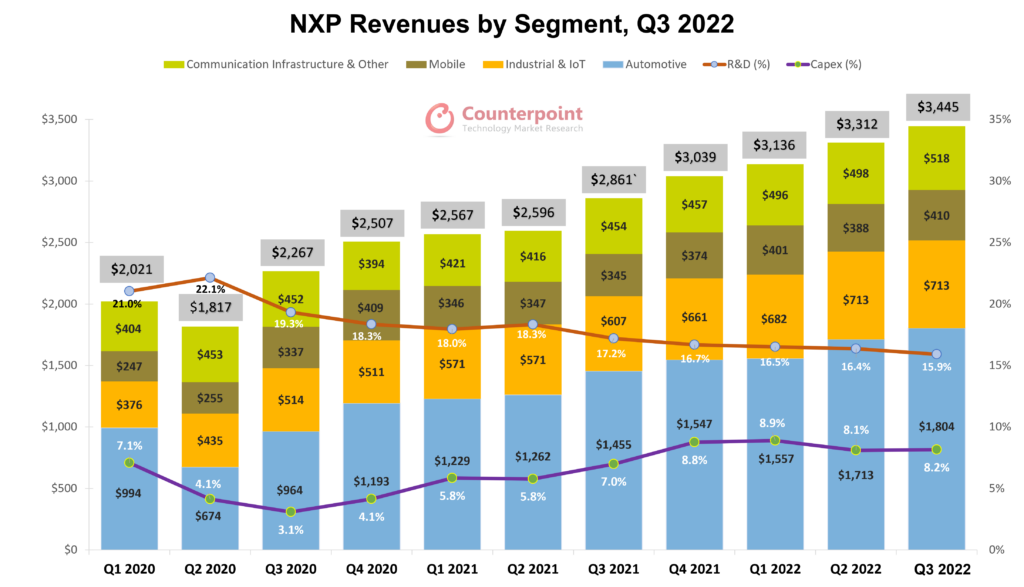

NXP’s Q3 2022 revenues were $20 million more than the midpoint of the company’s previous guidance. The automotive, mobile and communication infrastructure segments performed better than expected. But the consumer-exposed IoT and Android mobile segments experienced weakness.

NCNR order book continued to surpass NXP’s 2023 supply capabilities.

For Q4, the company expects revenue of about $3.3 billion (± $100 million). This would mean an increment of 9% YoY with 4% downside sequentially. Non-GAAP gross margins are expected to be 57.8% (± 50 bp) and operating expenses are expected to be near $720 million (± $10 million).

NXPreported revenues of $3.45 billion in Q3 2022, an increase of 20.4% YoY and 4% QoQ, and $20 million more than the midpoint of the company’s previous guidance. NXP’s automotive, mobile and communication infrastructure segments performed well compared to Q2, while the industrial and IoT segment struggled. Specifically, the consumer-exposed IoT business, accounting for almost 40% of revenue, experienced weaker sell-through in the channel. However, demand from automotive and core industrial customers remained resilient supported by accelerated growth drivers. Due to higher factory utilization and sales volume, the non-GAAP gross profit was almost $2 billion and the margin was 58%, up 150 basis points YoY.

Sources: Company, Counterpoint

Automotive

NXP’s strong suit, the automotive segment accounted for 52.4% of the total revenue in Q3 and stood at $1.8 billion. This was a 24% YoY and 5% QoQ growth. Auto demand for silicon content continues to be robust with risingEVpenetration and increasedautonomyefforts. Strong growth for advanced analog, automotive processing and radar solutions was visible in Q3. However, due to supply constraints, there was a shortage of microcontrollers and analog products in automotive. The NCNR order book in this segment continued to outstrip the company’s supply capacity, which will remain “sold out” next year too.

The company also announced collaborations and a product launch in the third quarter. NXP’sS32family of domain and zonal automotive processors is gaining traction among automakers as a preferred scalable platform for software-definedvehicles. A leading global automaker has selected the S32 MCUs/processors for its upcoming fleet of vehicles, starting 2025. NXP released the second-generation RFCMOS radar transceiver,TEF82xx,which supersedes the market-proven TEF810xx. This high-performance, single-chip solution supports short-, medium- and long-range radar applications including cascaded high-resolution imaging radar. Besides, NXP has collaborated withChargePointof the US for charging solutions and has also included its proprietary payment solutions to allow a seamless process for the customers.

For Q4 revenues, NXP is estimating this segment to be in the high teens and flattish on a YoY and QoQ basis respectively.

Industrial & IoT

The industrial andIoTsegment’s revenue was $713 million, an increase of 17.5% YoY with no QoQ change and $32 million below the company’s guidance. The YoY increase was driven by the demand for crossover processors, 32-bit AMR MCUs,point-of-salesecurity solutions and more. As mentioned earlier, the consumer-exposed IoT business was much impacted. Since August, there was a global softening visible in the consumer IoT market withChinagetting affected strongly. Since NXP has a sizeable channel exposure in China and serves thousands of customers via distribution partners, the revenues in that domain took a hit.

Going forward, NXP could ship more into the channel but instead decided to limit channel inventory to 1.6 months (as opposed to the long-term target of 2.5 months) to prevent losses due to uncertain macro conditions. The company will closely gauge and adhere to market requirements depending on the developing demand and, if required, redirect it to other customers. With respect to on-hand inventory, the DIO increased five days sequentially to 99 days with more increments expected in the future.

For Q4, theindustrialand IoT segment is expected to be in the negative territory in both YoY (low double-digit) and QoQ (high teens) terms.

Mobile

The mobile segment had revenues of $410 million, up 19% YoY and $30 million more than what was expected. Despite seeing weakness in the Android mobile market, NXP attained better than estimated revenues due to being exposed to the higher-end (which seems to be doing better) rather than the lower-endmobilephone market, increased attach rate for its secure mobile wallet, advanced analog high-speed interfaces,eSIMconnectivity and more.

As Ultra-Wideband (UWB) penetration starts picking up in different verticals like mobile, IoT and cars, the company will be able to accrue more revenues in the future, from its UWB technology along with mobile wallet solutions.UWBuse cases are already visible in China as UWB functionality in phones (flagship models) such as those from Apple,Samsungand Xiaomi. These smartphone players have collaborated with automakers to implement UWB-based solutions in cars to offer consumers secure car access. NXP expects four Chinese OEMs to offer this technology by the end of this year with a minimum of three more to follow in 2023.Kostalis using NXP’s UWB technology for its digital key system, which is being adopted by local companyNio.

For Q4, the company is expecting this segment to be up in the low single-digit range YoY and down in the upper single-digit range QoQ.

Communication Infrastructure & Other

The communication infrastructure and “other” segment’s revenue was $518 million, slightly above the guidance. Annual and quarterly growth rates were 14% and 4% respectively. The growth can be attributed to the demand for networkedgeequipment, RFID tagging solutions,cellular base stationsand more.

NXP launched its new higher-powerBTS7202 RX front-end modules (FEM)andBTS6403/6305pre-drivers for 5G massive multiple-input multiple-output (MIMO) going up to 20 W per channel. These solutions complement its 32T32R active antenna systems and are developed using the company’s silicon germanium (SiGe) process. As 5G network coverage expands, there is a need for higher-power solutions to ensure consistent network quality along with reduced operational costs for MNOs. The newly announced devices can cater to these requirements with higher power per channel and modest consumption.

For Q4, the guidance seems positive and stands in the low-teens range YoY and flattish QoQ.

Capex Overview and Inventory

Cash flow generation continues to be excellent according to the company. In Q3, cash flow from operations stood at $1.14 billion compared to $819 in Q2. Net capex accounted for 8.2% of the revenue or $281 million. Due tosupplyconstraints and strong demand (especially in the auto sector), internal utilization remained in the high 90s. More than 65% of the capacity was focused on IP proprietary mixed-signal, auto-centric capacity internally.

Capexfor this year has decreased from 10% to 8% due to delays in equipment deliveries. For 2023, it will range between 6% and 8%.

From the demand perspective, there is weakness in the consumer IoT and Android mobile market, whereas the automotive and core industrial markets are witnessing resilient demand. On the supply side, the situation is reversed with the latter markets facing supply crunches and not being able to cater to the true demand. On the other hand, in the former markets, excessive shipping in channels is being prevented because of uncertain macro conditions.

Conclusion

NXP’s supply capabilities have improved over time but major end markets like auto and core industrial continue to faceshortages. Prevalent weak macro conditions and extended China lockdowns will cause further hindrances to the revenue recovery of consumer-oriented markets. However, the company is being cautious and trying to mitigate costs by reducing its discretionary spending, lowering incentive compensations, and focusing on a strict approach to managing distribution channel inventory.

Second quarter revenues for NXP were $37 million more than the midpoint of the company’s previous guidance with the automotive and industrial segments performing well while the mobile and communication infrastructure segments were in line with its expectations.

Amid the ongoing macroeconomic and supply chain turmoil, the company is banking on its NCNR orders to provide its customers with supply assurances. For 2023, NCNR orders are already more than what the company can supply. Therefore, NXP is focused on de-risking its existing backlog for potential double/stale orders and improving supply capabilities.

For the third quarter, the target is to achieve 20% YoY growth at $3.425 billion. The automotive and industrial segments will take the center stage again to provide a safe landing going forward with respect to demand.

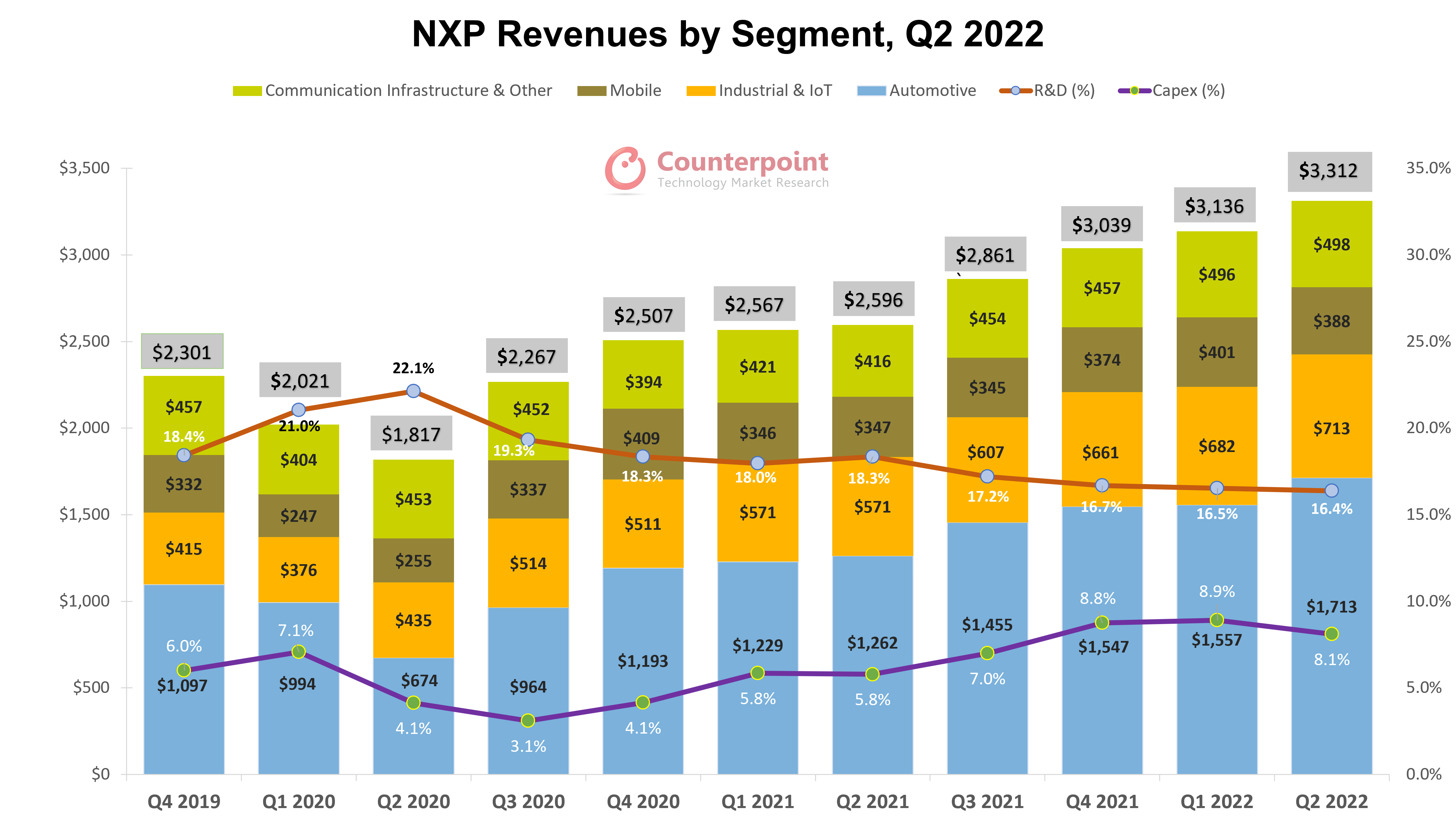

Despitemacroeconomicheadwinds and supply chain constraints, NXP reported healthy Q2 2022 revenues at $3.31 billion, an increase of 27.6% YoY and 5.6% QoQ. Major revenue drivers for this quarter were the automotive and industrial segments, accounting for almost three-fourths of the total revenue. Strong customer demand within these segments is outstripping the company’s improving supply capabilities.

Sources: Company, Counterpoint

Automotive

NXP’s automotive segment captured almost 52% of the total revenue and stood at $1.7 billion, rising 35.7% YoY and 10% QoQ respectively. From the supply point of view, the automobile industry is still feeling the effects of factors like COVID-19 lockdowns in China,Ukraine-Russiawar andsemiconductorshortages, resulting in fewer cars being produced. On the demand side, consumer sentiment is muted due to macroeconomic factors affecting purchasing power. However, despite the production being down, the content within cars is increasing due to increaseddigitizationand the growing penetration ofxEVsin the market, which is where NXP benefits a lot.

Products in demand include battery management systems, inverter control, MCU/MPU, Goldbox (service-oriented gateway) and more. Theautomotiveindustry is pivoting towards software-defined vehicles, which will be complemented by two parallelarchitecturalevolutions, namely zonal and domain. To support these vehicular functions and accelerate integration, NXP introduced two new processor families, S32Z & S32E, to extend the benefits of its innovative S32 automotive platform. Additionally, the company also announced that it would be working with Hon Hai Technology Group (or Foxconn) to jointly develop platforms for a new generation of connected cars. This collaboration will enable solutions focused on architectural innovation and platforms for electrification,connectivity, and safe automated driving.

Industrial & IoT

The industrial andIoTsegment grew by 25% YoY and 4.5% QoQ to reach $713 million. The segment contributed 21.5% to the total revenue. Use cases for smart and connected applications, like within homes or factories, are evolving and leveraging the potential of IoT. NXP is serving the needs of its customers through secure connected edge solutions in the form of advanced analog solutions, general purpose MCUs and application processors. Its broad portfolio includes scalable compute platforms along with collaborations with multiple cloud players likeAWS, Azure, and Baidu, which allows for differentiatedsoftwareenablement and services. In June, NXP announced the newArmCortex-M core-based MCX portfolio (MCX N/A/W/L series) of microcontrollers which are scalable, flexible enough to simplify migration and allow developers to maximize software reuse across the portfolio to minimize total system cost. These MCUs are suitable for smart homes, smart factories, smart cities and across many emerging industrial and IoT edge applications.

The supply chain constraints are evident based on NXP’s channel inventory. Its industrial business, especially in China, is dominated by the distribution channel and is sitting on a channel inventory of 1.6 months, which is still a month below its target of 2.5. However, the Chinese government’s stimulus programs are providing respite for the company’s industrial and automotive market operations. According to NXP, since June, the effects of the stimulus have been significant and would prove to be beneficial for the second half of the year as well.

Communication Infrastructure & Others

The segment saw a flat sequential growth but an almost 20% YoY increase to reach revenues of $498 million. This capex-drivenwireless infrastructuresegment accounted for 15% of the revenues. NXP’s increased value proposition stems from its technological leadership (in wireless solutions and RF components & processors catering to applications like enterprise networking, wired/wireless networkinfrastructureand data center), system expertise and manufacturing scale. Its leadership in accelerated growth driver RF power systems for cellular base stations is witnessing robust demand. Furthermore, as 5G deployments continue to expand globally and carriers optimize power consumption for sustainable 5Gnetworks, NXP is in place to serve all 5G configurations and systems ranging from 5G Macro and 5G mMIMO to 5GmmWave.

NXP has expanded its massive multiple input, multiple output (mMIMO) product portfolio by launching a new series of RF power discrete solutions for 32T32R active antenna systems, employing its proprietary Gallium Nitride technology (GaN). This new series complements its existing portfolio of discrete GaN power amplifiers for 64T64R radios. These5GmMIMO systems were produced in NXP’s own advanced GaN manufacturing facility and it now has the largest offerings for the RF GaN portfolio for massive MIMO 5G radios. For 5G rollouts in densely populated areas, 64T64R solutions are appropriate and for less dense urban/suburban areas, 32T32R solutions are suited best.

Mobile

This is the only segment that saw its revenues going down QoQ (-3.2%). But they grew 11.8% on a yearly basis. Revenues reached $388 million, a decline of $13 million from the previous quarter. The segment witnessed a QoQ decline due to macroeconomicweakness in Chinawhere the company is exposed to low-endAndroidplayers. NXP has faced supply issues in this segment in the past quarters as well, hence it has been very careful to not grow any inventory down the chain. Furthermore, it is shifting its supply from mobile to other segments like auto and IoT as the demand in these segments is more robust and consistent. However, its strong hold in the securemobilewallet (which includes technologies likeNFC, eUICC and MIFARE 2GO), embedded power solutions, and UWB ecosystem solutions (accelerated growth driver) has experienced continued strong adoption. UWB technology is gaining traction and seeing an increased installed base across different verticals likeIoT, cars and mobile, and NXP is well-positioned to drive this ecosystem.

NXP has collaborated with ING andSamsungfor innovations in payment services by bringing forth the industry’s first UWB-enabled peer-to-peer payment application. Project NEAR will leverageUWBING银行的三星Galaxy智能手机application to allow consumers to send money directly to peers when twoGalaxyphones are in proximity. Instead of inputting bank details, the sender can simply be in close range of the recipient and a swift transaction can happen, made possible via NXP’s Trimension SR100T UWB chips. Further, the company’s SN110 convergenceeSIMsolution (which integrates eSIM, NFC and secure element) is used in Xiaomi’s Redmi Note 10T and HONOR’s Magic4 Pro models forremote SIM provisioningwith multiple MNO subscriptions, along with advanced features like smart access, payment, and secure mobile transit.

Future Guidance and Capex Overview

为即将到来的季度,该公司预计到ttain $3.425 billion in revenue, plus or minus about $75 million at the midpoint. This is up 20% YoY and about 3% QoQ. The non-GAAP gross margin is expected to be about 57.8%, plus or minus 50 basis points. NXP has attempted to de-risk its Q3 outlook keeping in mind the macroeconomic conditions that are already affecting its mobile and consumer end markets. But the auto andIoTsegments will continue to perform well due to strong customer demand. Both auto and IoT segments are expected to be in the low 20% range YoY and in the mid-single digit range QoQ.

Q2的资本支出为2.68亿美元,下跌1美元1 million from the previous quarter. The company is focused on improving its supply capabilities by employing a hybrid manufacturing model and making sure no excess inventory is being built down the chain in any of its major end markets. NXP is remodeling its factories (all are 200 millimeter) to focus on manufacturing proprietary specialty processes unique to the company. Furthermore, it is transferring more of the CMOs to its foundry partners to create more internal space for its facilities, allowing it to work on advanced products catering to the ever-growing needs of different industries. Currently, 60% of thewafersupply is coming from the foundry process, most of which is turned into CMOs logic processes (especially for the ones below 90 nanometers and pertaining to 300 millimeter).

Conclusion

The automotive and industrial segments continue to be NXP’s strong suit where most of the recurring revenue is generated. The company remains bullish on these segments for the second half as well. This is evident as the company is already sold out for the rest of the year with respect to these segments and there are ever-growing content increases in these underlying sectors. The automotive sector will see morexEVsproduced in the second half and by the end of the year, the share of green vehicles will be 26% of the global car production. Higher EV penetration means more semiconductor content (higher ASP for silicon content as well) and ultimately more revenue growth for the company.

Going forward, NXP is aiming to improve inventories and supplies for its major end markets because for the foreseeable period, it estimates its supply capabilities to cover 80% of the underlying demand. Based on its aforementioned new product launches, design win commitments and healthy NCNR order book, NXP is confident that its future growth and investments are well-aligned with the long-term market requirements.

COVID-19, along with the rise of advanced capabilities such as5G, AI andimagingtechnologies, has catalyzed the semiconductor demand for the last over two years. Monitoring the contribution of upstream players in the semiconductor value chain, which are actually building technologies and capacities, has become extremely important.

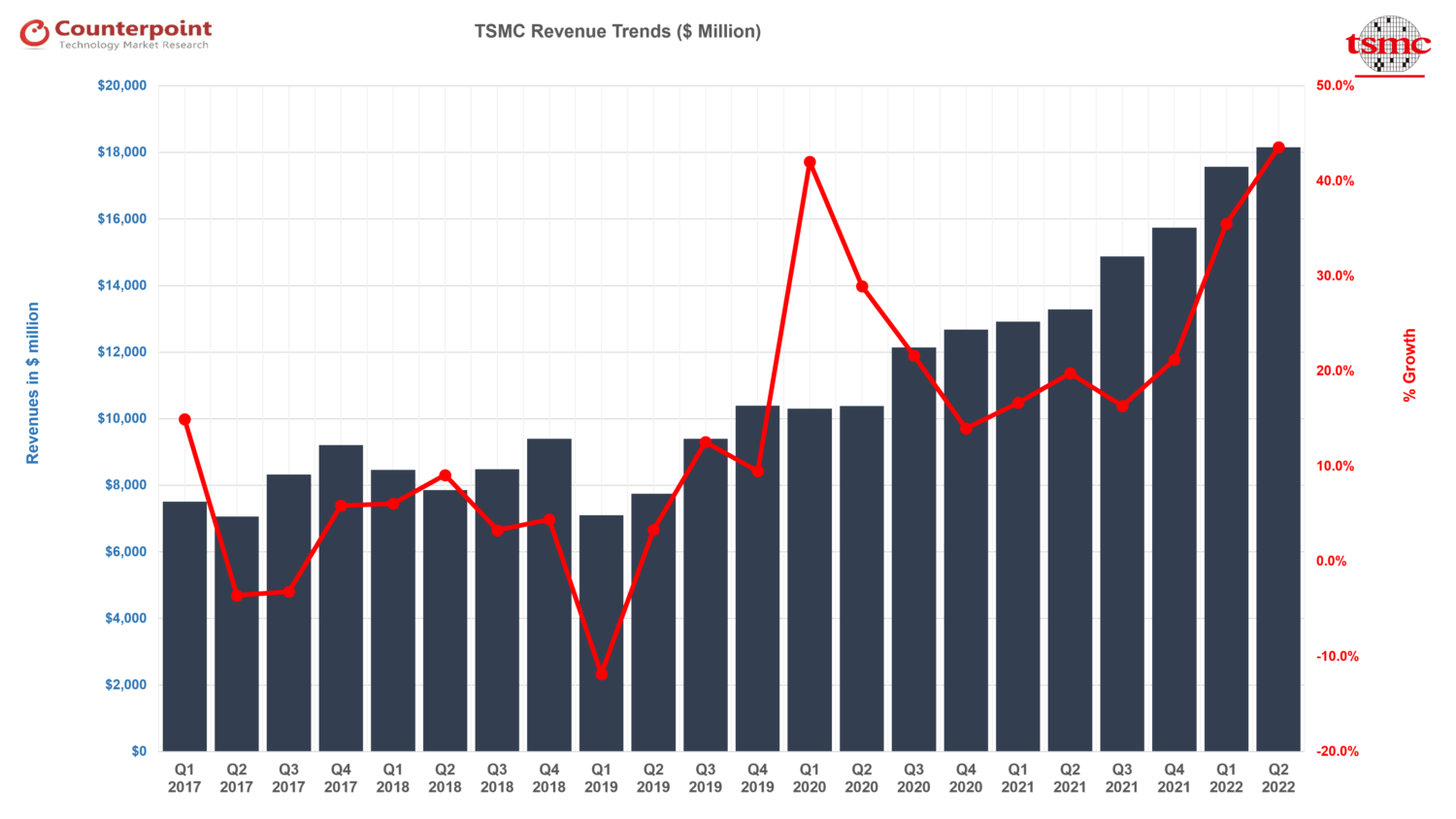

TSMC is a great benchmark for the health of the semiconductor industry considering it manufactures 70% of all keysmartphonechipsets. The company posted record earnings in Q2 2022 with growing advanced semiconductor content in processing (AI,GPU,SoC) and connectivity (5G) being the key factors.

Key financial highlights:

净集团营收同比增长37%至182亿美元ven by high-performance computing (HPC),IoTand automotive-related demand.

Gross margin and operating margin were at 59.1% and 49.1% respectively, up 3.5 percentage points on a favorable foreign exchange rate, cost improvement and value selling.

From the geographical perspective, North America accounted for the highest share (64%) of total net revenue.

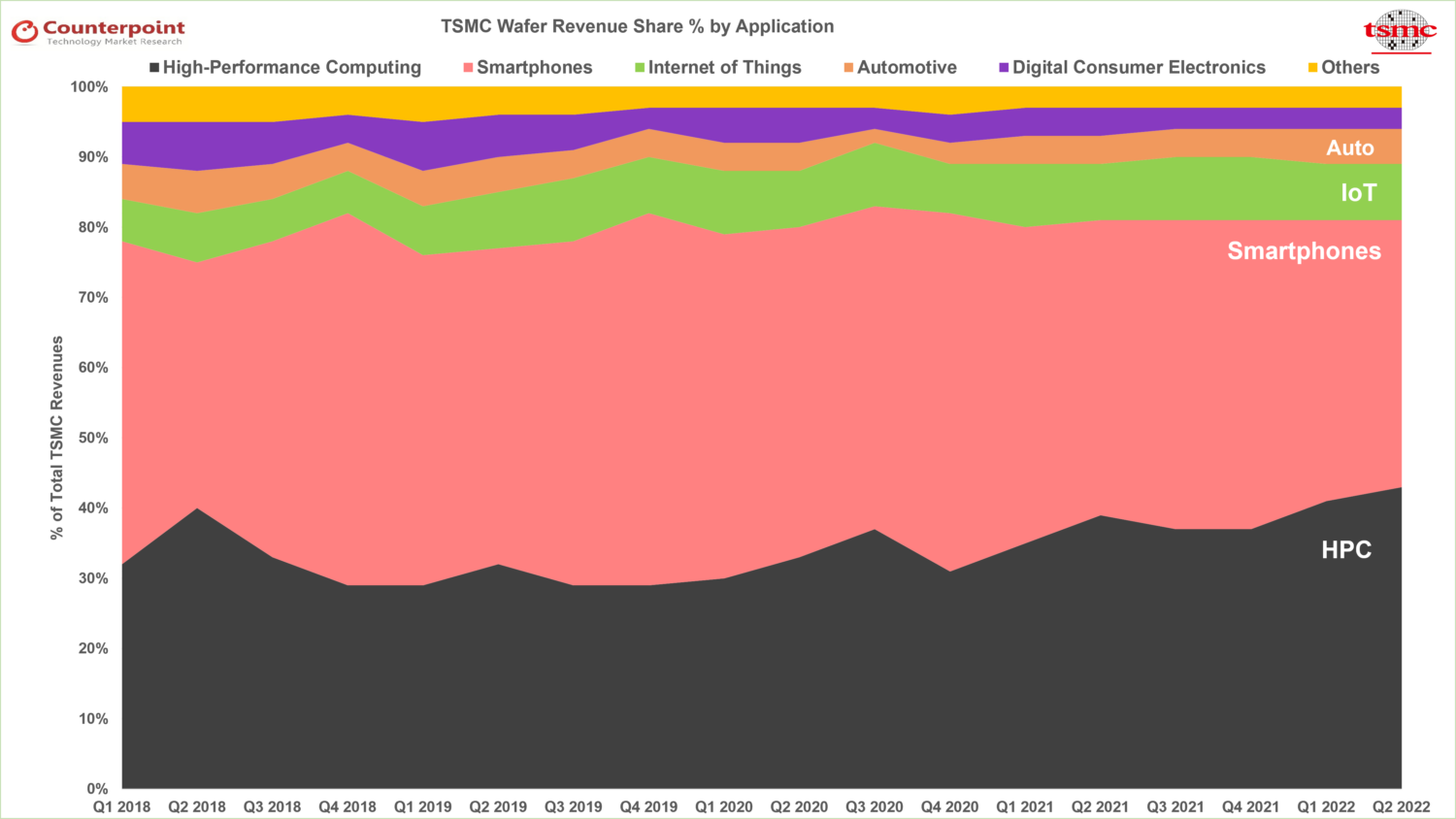

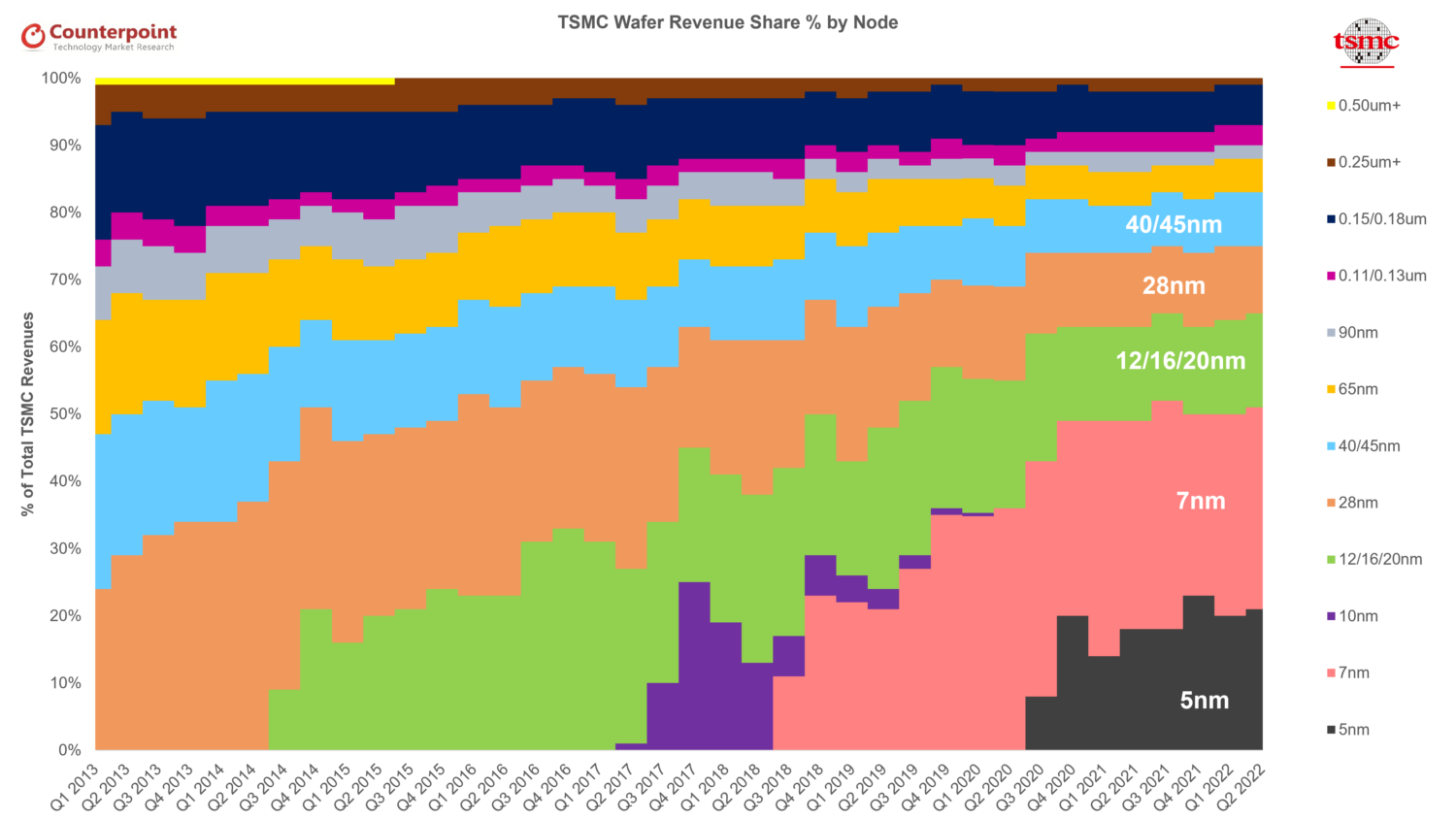

TSMC wafer revenues share

By application

Smartphones and HPC represented 38% and 43% of net revenues respectively, while IoT, Automotive, Digital Consumer Electronics (DCE) and Others represented 8%, 5%, 3% and 3% respectively.

HPC surpassed Smartphones in revenues thanks to Nvidia, Intel, AMD and others.

TSMC’s reliance onApple,QualcommandMediatekwas lesser as HPC surpassed Smartphones in revenue contribution.

Automotive semiconductor content was the dark horse.

By node

5nm process technology contributed 21% of total wafer revenues in Q2 2022 while 7nm accounted for 30%.

Combined revenue from advanced process nodes with 5nm and 7nm accounted for 51% of total wafer revenues, thanks to growingcapex, making it very difficult for current and potential competition to catch up at least in next 10 years.

Double-digit growth was seen in matured nodes thanks to the rising need for chipsets in the IoT andautomotive.

N2 and N3 updates

N2 node will implement the platform scaling concept wherein benefits of power delivery schemes, advanced packaging and chiplet will be utilized to control cost and have an overall advantage.

N3 node will be the longest node to be used before migrating to N2 due to the introduction of TSMC FINFLEX architectural innovation, which offers flexibility to customers to create designs precisely tuned for their needs with functional blocks implementing the best-optimized fin configuration and integrated into the same chip.

The introduction of 3nm nodes will begin in H2 2022 and adoption by customers and revenue contribution will start in Q1 2023. The introduction of 3nm nodes will lower the gross margin by 2%-3% in 2023.

While the capex is growing, some of it will be spread out over quarters with theWFEvendors struggling with backlogs as building fab equipment also requires semiconductors! This will help TSMC realize healthy margins for the coming quarters and offset any gross margin decline due to N3 introductions.

Key takeaways

TSMC’s net revenue will cross $75 billion in 2022, which means it will surpass Intel’s revenues.

HPC will drive TSMC’s revenue growth in the long term and achieve a 15%-20% CAGR.

3D IC design solution System on Integrated Chips (SoIC) will account for a significant share of revenue in the long term due to its extensive application in HPC.

Efforts to resolve tool delivery schedule challenges in advanced and mature nodes through discussions with entire supply chain partners remains a top priority.

Growing silicon content, shipments and ASP will drive revenue growth in the long term.

Inventory adjustment will continue till Q1 2023 and ease off by H2 2023. However, long-term semiconductor demand will be firm.

The semiconductor supply chain has been suffering capacity constraints since H2 2020, with both TSMC and Intel guiding more than 18 months of supply tightness ahead.

We believe the shortage will be prominent at relatively mature nodes across 200mm and 300mm foundries due to strong demand from multiple sectors.

Further, we expect the lingering demand-supply imbalance to continue, with prices seeing another round of hikes of at least 10-20% in 2022.

To tackle the shortage, TSMC has revised up its 2021 capex guidance to $30 billion while Intel will work more closely with clients to seek solutions.

The global semiconductor supply chain has been suffering severe capacity constraints since H2 2020 due to pent-up demand in different sectors. Foundry capacity remains largely booked with fully-loaded utilization rates across different process nodes. Our checks suggest some IC design companies have already experienced 30-40% price hikes in certain product categories in 200mm foundries when compared with H2 2020. Therefore, we are looking at a new normal here.

TSMC’s $100-bn plan for capacity expansion

TSMC, the largest foundry vendor in the world with ~55% market share, has revised up its 2021 capex guidance to $30 billion (from the previous guidance of $25-28 billion in January 2021), with 80% of this being meant for advanced node investments (3/5/7 nm), 10% for advanced packaging services and 10% for specialty technologies.

During the Q1 2021 earnings call, TSMC also reaffirmed its $100-billion capex plan for 2021-2023, mainly supported by customers’ promising outlook and commitments, which could translate into 10-15% CAGR of the USD revenue during 2020-2025.

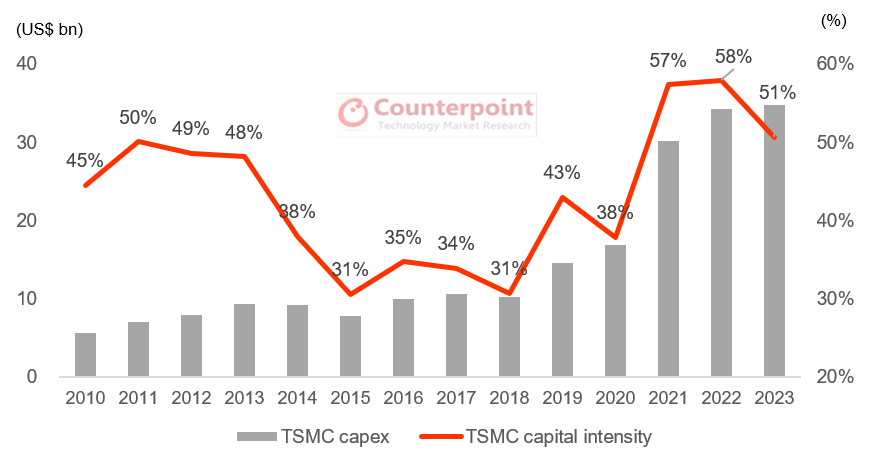

Exhibit 1: TSMC’s Capex and Capital Intensity

However, TSMC and Intel have both highlighted that the overall semiconductor demand-supply mismatch will continue until the end of 2022, withcapacity expansionfailing to keep up with the skyrocketing demand, especially at certain mature process nodes. In general, the semiconductor industry is going through a significant structural demand shift. Therefore, both foundries and customers are on the same page in maintaining a higher inventory level to deal with uncertainties.

Decelerating capacity expansion and demand rally push up foundry costs

Recently, some foundry companies announced capacity expansion plans. These include TSMC’s 28 nm plant in Nanjing, UMC’s 28 nm in Southern Taiwan and Vanguard’s acquisition of another 200mm fab in Hsinchu. Supported by a few vendors’ de-bottlenecking expansion, we expect major additional capacity to be created at comparatively mature nodes soon.

迁移从200毫米到300毫米在过去数年s has been too slow to eliminate supply constraint risks on mature nodes. Now, foundries are getting less support from the 200mm equipment vendors. Therefore, with the capacity failing to fulfill incremental orders and demand popping up in the short term, price hikes will emerge. We have even witnessed 30-40% price hikes on specific process nodes, apart from a generally 10%+ extra cost to design houses.

Unfortunately, this rise in prices will not stop in 2021. In order to secure 2022 capacity, design houses are negotiating with foundries. We foresee at least 10-20% higher costs here.

Intel foresees best days on solid demand

Intel has also shared a robust outlook, seeing its best days around the corner. Betting big on the tremendous demand for computing, the strength of itsIDM 2.0 strategy, and ongoing technology investments, Intel expects to restore its leading position in the semiconductor industry. The company has also announced a capex plan of ~$20 billion for 2021, up 35-40% YoY and covering expenditure on two fabs in Arizona ($20 billion in total).

5G phone, HPC and automotive drive foundry capacity expansion

In terms of sales growth drivers, we believe smartphones will continue to play an important role for at least three years due to the5G smartphonereplacement cycle. Nevertheless, smartphone shipments growth has decelerated in recent years and is no longer sufficient to justify an aggressive capex plan and a robust sales growth outlook from foundry vendors.

We believe high-performance computing (HPC) will step forward and consume a lot of new capacity for several years, mostly driven by emerging AI applications, connected devices, virtual reality/augmented reality and intelligent manufacturing. These segments require unprecedented computing power in both communication infrastructures and cloud data centers. Intel says nearly every application is now infused with artificial intelligence and machine learning. Global hyperscale data center vendors and cloud solution providers have put a lot of resources into capacity expansion. We believe this trend will continue to enhance computing power to support the sharp growth in HPC demand.

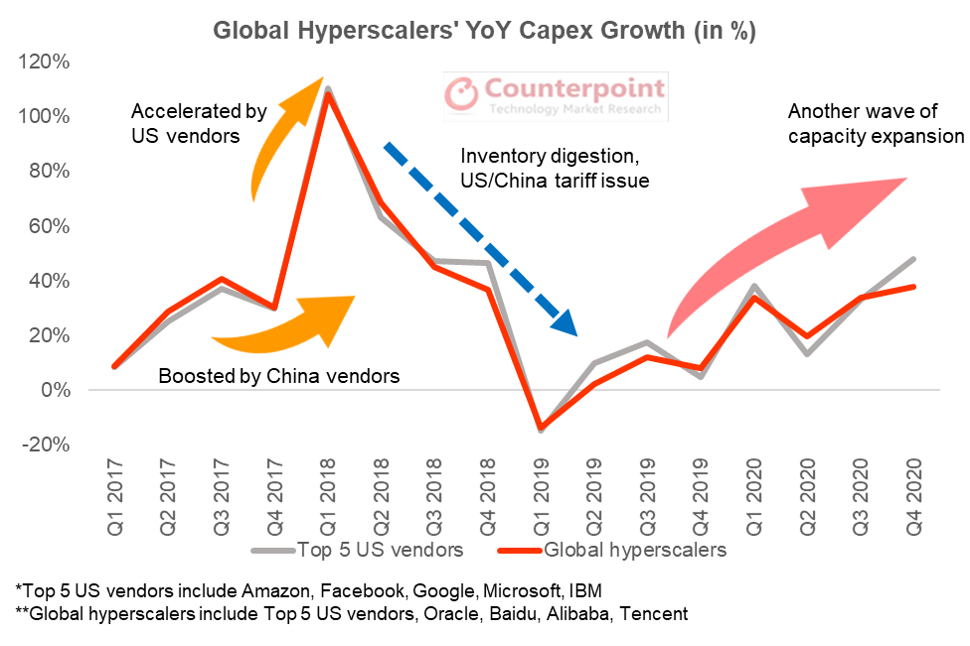

Exhibit 2:Hyperscale Vendors’ Capex Supports Worldwide Computing Power

在其他领域,汽车目前ries (electric vehicles, autonomous driving, charging devices) are expected to gradually become semiconductor-consuming giants on increasing semi content per car and the V2X (vehicles to everything) ecosystem. TSMC has already marked the automotive market to be its top priority in the upcoming years though it only accounted for 4% of its total revenue in Q1 2021 (against 45% from smartphones and 35% from HPC).

Conclusion:

Foundry cost hike in 2021 has largely settled down while another price increase for 2022 is already around the corner. Design houses are in the process of negotiating foundry costs and capacity quota with chipmakers. We expect the demand-supply imbalance to last for another year, along with another round of price hikes of at least 10-20% in 2022.

In order to access Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not. Personal Information When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time. In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company. – Passwords are for user’s individual use – Passwords may not be shared with others – Users may not store documents in shared folders. – Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified. Accuracy of Information: While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

第三方链接:这个网站可能包含链接to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience. This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.