Qualcomm’s Premium Portfolio Leads Record Revenues in Handsets

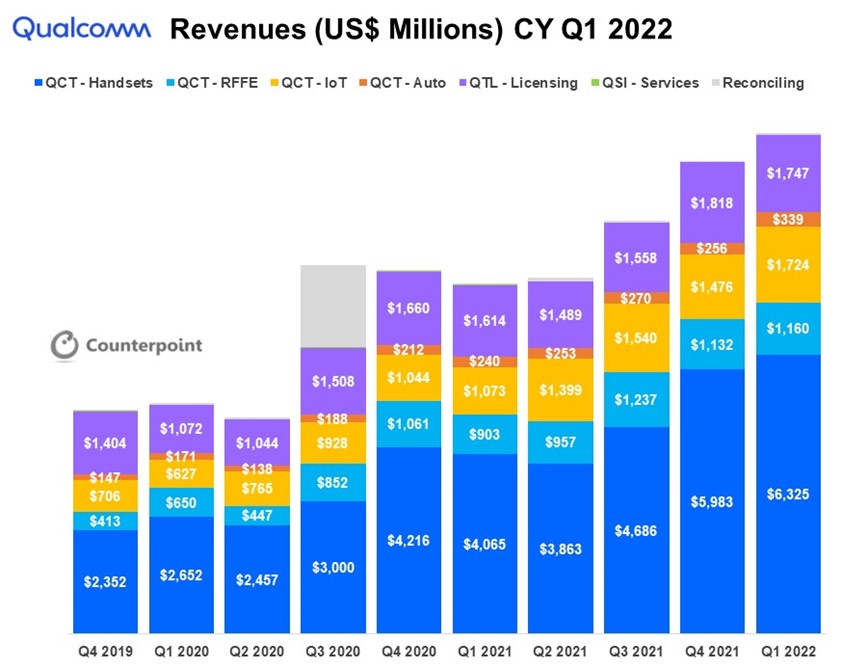

After some big gains in 2021, the semiconductor space has seen volatility recently thanks to war, inflation, growing inventory in some segments and shortages in others. However, Qualcomm had a very strong Q1 2022, its third consecutive quarter to see record revenues, including in its handset segment. All business units grew between 28% and 61%.

Qualcomm’s strategy to diversify from being a handset communications company to a connected processor company servicing the connected edge continues to move forward. The company reiterates that its “one technology” road map can expand its total addressable market by seven times. Despite a blowout quarter of its handset business, Qualcomm’s other business units contributed 34% of its Q1 2022 revenues.

Source: Qualcomm Investor Relations

Some key highlights from the quarter:

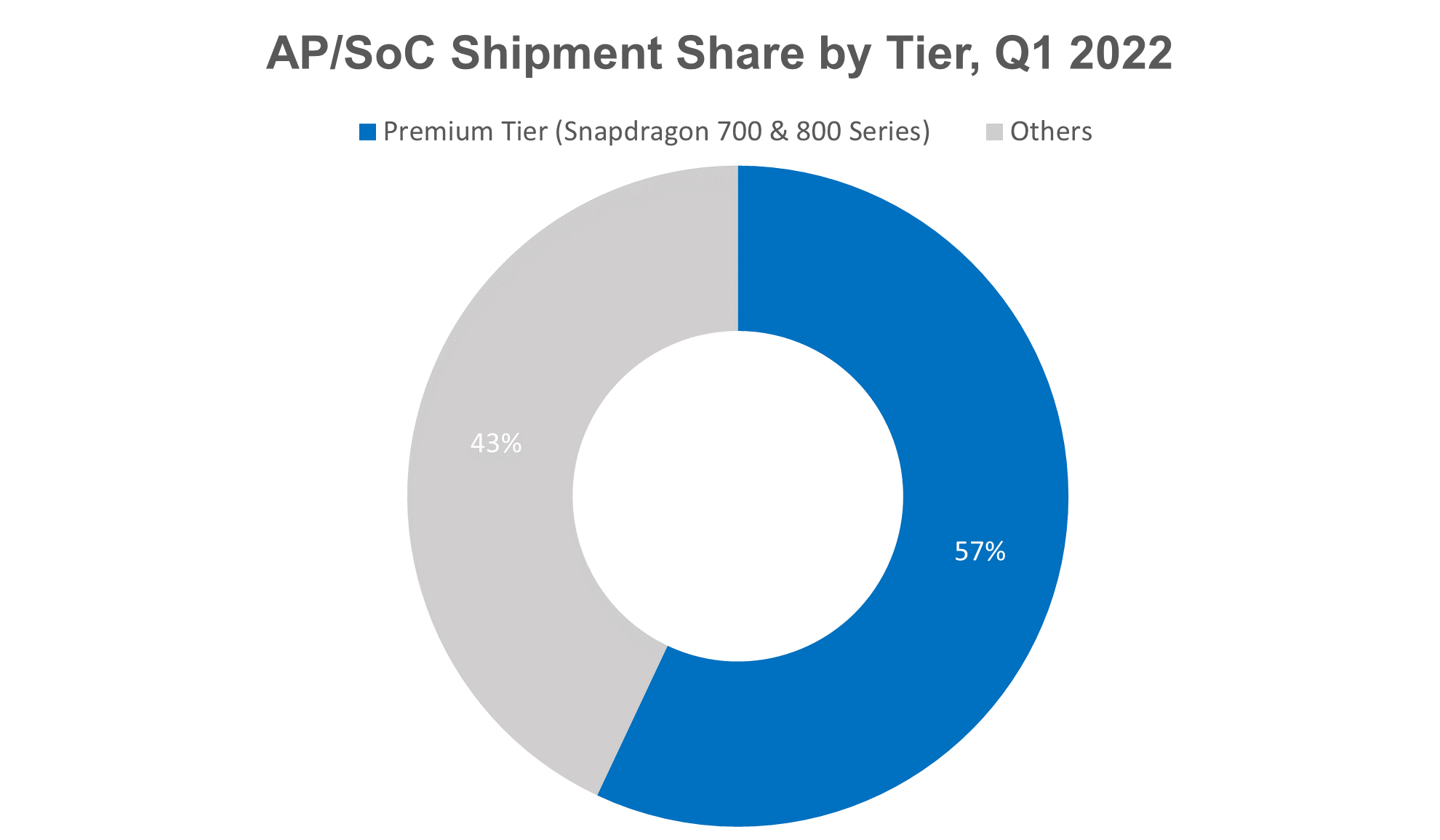

- Thehandsetbusiness grew 56% YoY to $6.3 billion — tremendous growth despite the headwinds of a sales slowdown and further COVID-19 shutdowns in China. The company acknowledged it saw a slowdown in the low- and mid-price segments. But this was more than offset by very strong premium-tier sales. Supply improved and Qualcomm made flagship design wins with all major Chinese brands. These devices are now hitting the market. It is a feather in Qualcomm’s cap that Samsung has increased the variants of its Galaxy S22 line-up powered by Snapdragon. Qualcomm claims it now drives 75% of the S22 family sales – up from 45% of the S21 family. According to Counterpoint Research’sGlobal Smartphone AP-SoC Shipments & Forecast Tracker, premium-segmentSnapdragon 700 and 800series contributed to around 57% of the AP/SoC shipments in Q1 2022.

Source: Counterpoint Research’sGlobal Smartphone AP-SoC Shipments & Forecast Tracker

- TheIoTbusiness grew 61% YoY and reached $1.7 billion with growth coming from all three segments — consumer, edge networking and industrial.

- In theconsumer段,采用物联网高端安卓tablets and demand from entry-level to premium tiers, like the adoption of the Qualcomm 8 Gen 1 by the Samsung Galaxy S8 series and OEMs like Lenovo, HP and Opel, pushed the shipments. Also, some momentum came from Windows on ARM adoption in the Qualcomm 8CX Gen3-powered Lenovo ThinkPad X13S. The adoption of the NUVIA team’s new CPU designs is expected to be implemented in late 2023. This will enable more powerful, always-connected PC designs.

- Theedge networkingandindustrialsegments are being driven by the migration to Wi-Fi 6 and 6E mesh technologies. 5G Fixed Wireless Access (FWA) is another segment that is gaining momentum. According to Counterpoint Research’s latestGlobal FWA+CPE Forecast, 2019-2030, H1 2021, FWA will have a 36% share of the global fixed broadband subscriptions by 2030. Qualcomm’s 5G FWA solution has 125 designs announced or in development by more than 40 OEMs. The industrial segment growth is being driven by connectivity and advanced processing at the edge in applications like ruggedized handhelds,roboticsand hospital handhelds. Qualcomm has also announced itsWi-Fi 7solutions to drive the next growth opportunity for connectivity.

- Theautomotivebusiness grew 41% YoY and reached $339 million driven by the adoption of the Snapdragon digital chassis. Digital chassis includes solutions like telematics, connectivity, digital cockpit, ADAS, and autonomy and cloud services. It will be the key revenue segment going forward, with the design win pipeline now exceeding $16 billion. Further, the incorporation of Arriver’s computer vision, drive policy and driver assistance assets into the Snapdragon Ride Platform will enable Qualcomm to win more semi content in vehicles. OEMs like BMW andStellantis are adopting Snapdragon Ride and Snapdragon automotive cockpitplatforms in their vehicles.

Source: Qualcomm

- TheRFFEbusiness grew 28% YoY and reached $1.2 billion driven by the adoption of the 5G modem RFFE advanced features like AI integration, mmWave and Sub6GHz dual connectivity, and 5G Sub6GHz CA for FDD and TDD spectrum.Handsets contribute a significant share in the RFFEbusiness, while expansion in the IoT and automotive segments will drive further growth in the RFFE revenues. Qualcomm is also the dominant player for 5G mmWave RFFE in smartphones, 5G FWA CPE, and more.

- Guidancefor Q2 2022 sees revenues at $10.5 billion to $11.3 billion, non-GAAP EPS at $2.75 to $2.95, QTL revenues at $1.4 billion to $1.6 billion, EBT margins at 69% to 73%, QCT revenues at $9.1 billion to $9.6 billion and EBT margins at 31% to 33%. On a sequential basis, seasonal decline in the handset and RFFE businesses and mid-single-digit growth in the IoT and automotive businesses are seen. Overall, a weak global macroeconomic situation, slowdown in China, COVID-19 and supply chain issues will impact the handset and PC markets. Also, the shift towards the premium segment will continue to drive revenues for the handset business. Qualcomm is focusing on the high-tier segment for bigger margins and the addition of RF and other categories to gain more content in Android devices.

We expect Qualcomm to benefit from its positioning in the premium segment driven by the revenues from the Snapdragon 700 and 800 series against the backdrop of tough macroeconomic conditions and weak China market. Q3 2022 will see an inflection point driven by premium launches, Apple and RFFE, which are tied to handset revenues. For 2023-2024, automotive, IoT and RFFE will sustain growth. Automotive design wins will take 2-3 years to materialize due to long cycles. Adoption of 5G, digital chassis and autonomy will drive semi content across the automotive segment. Also, RFFE will see growth across IoT and automotive with the adoption of 5G connectivity. Revenues from consumer IoT, like 5G FWA, Windows on ARM and Wi-Fi migration, and enterprise will sustain growth in the coming years.