(Use the buttons below to download the complete chart)

Highlights:

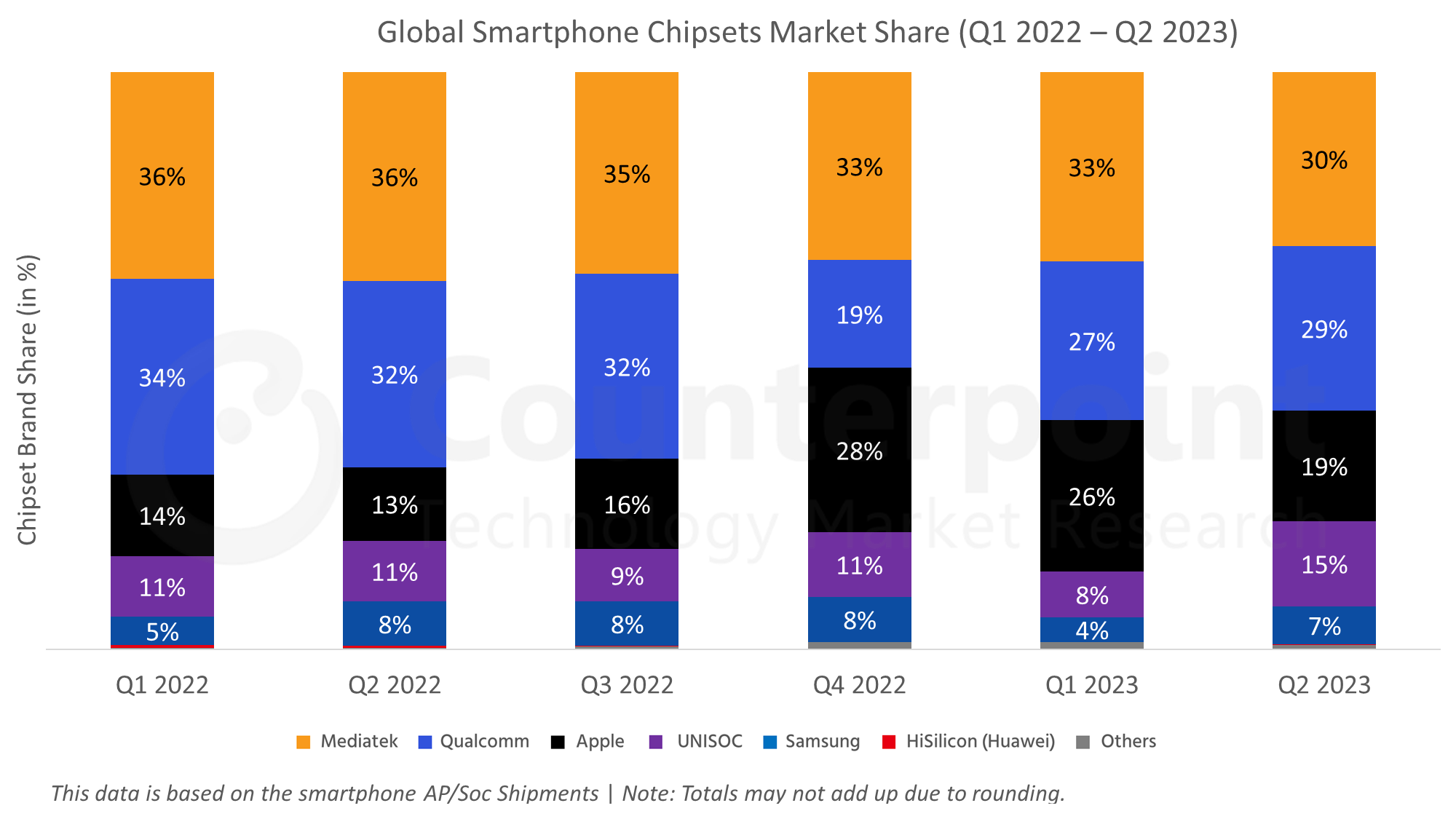

Apple’s sales declined in Q2 2023 due to seasonality. Its Pro series did better.

MediaTek’s shipments increased slightly in Q2 2023 with reduced inventory levels and growing competition in the entry-level 5G smartphone market. New smartphone launches in the low-to-mid-end segments increased the shipments of Dimensity 6000 and Dimensity 7000 series. The Dimensity 9200 Plus was added to the premium tier.

Qualcomm在2023年第二季度的出货量增加由于Snapdragon 8 Gen 2’s adoption in Samsung’s flagship smartphones and by Chinese OEMs. The launch of Samsung’s Flip and Fold series also contributed to this growth. Qualcomm refreshed the Snapdragon 7 Gen 1, Snapdragon 6 Gen 1 and Snapdragon 4 Gen 1 series to gain some share back. However, the premium segment’s growth remained in focus.

Samsung’s shipments increased in Q2 2023. The Exynos 1330 and 1380’s launch added volumes to the low and mid-high segments.

UNISOC在2023年第二季度的发货量增长疲软的Q1。它gained some share in the $100-$150 LTE segment. In H2 2023, as entry-level 5G smartphones pick up in regions like LATAM, SEA, MEA and Europe, UNISOC will gain some share.

For a more detailed smartphone AP-SoC shipments & forecast tracker, click below:

Global Smartphone AP-SOC Shipment & Forecast Tracker by Model – Q2 2023

This report tracks the smartphone AP/SoC Shipments by Model for all the vendors. The scope of this report is from the AP/SoC shipments from all the key vendors like Apple, Qualcomm, MediaTek, Huawei, Samsung, UNISOC and JLQ. We have covered all the main models starting fromQ1 2020 to Q2 2023.We have also included aone-quarter forecast for Q3E 2023.This report will help you to understand the AP/SoC Market from the shipment perspective. Furthermore, we have also covered key specs for these AP/SoC covering market view by:

Network(4G/5G AP/SoC)

Foundry Details(like TSMC, Samsung. etc.)

Process node(5nm, 6nm, 8nm, etc.)

Manufacturing Process(FinFET, N7, N5, etc.)

CPU Cores Architecture and CPU Cores Count

Modem(External/Internal)

Modem Name

Secure Element Presence

Security Chip

AI Accelerator

For detailed insights on the data, please reach out to us atsales(at)www.arena-ruc.com.If you are a member of the press, please contact us atpress(at)www.arena-ruc.comfor any media enquiries.

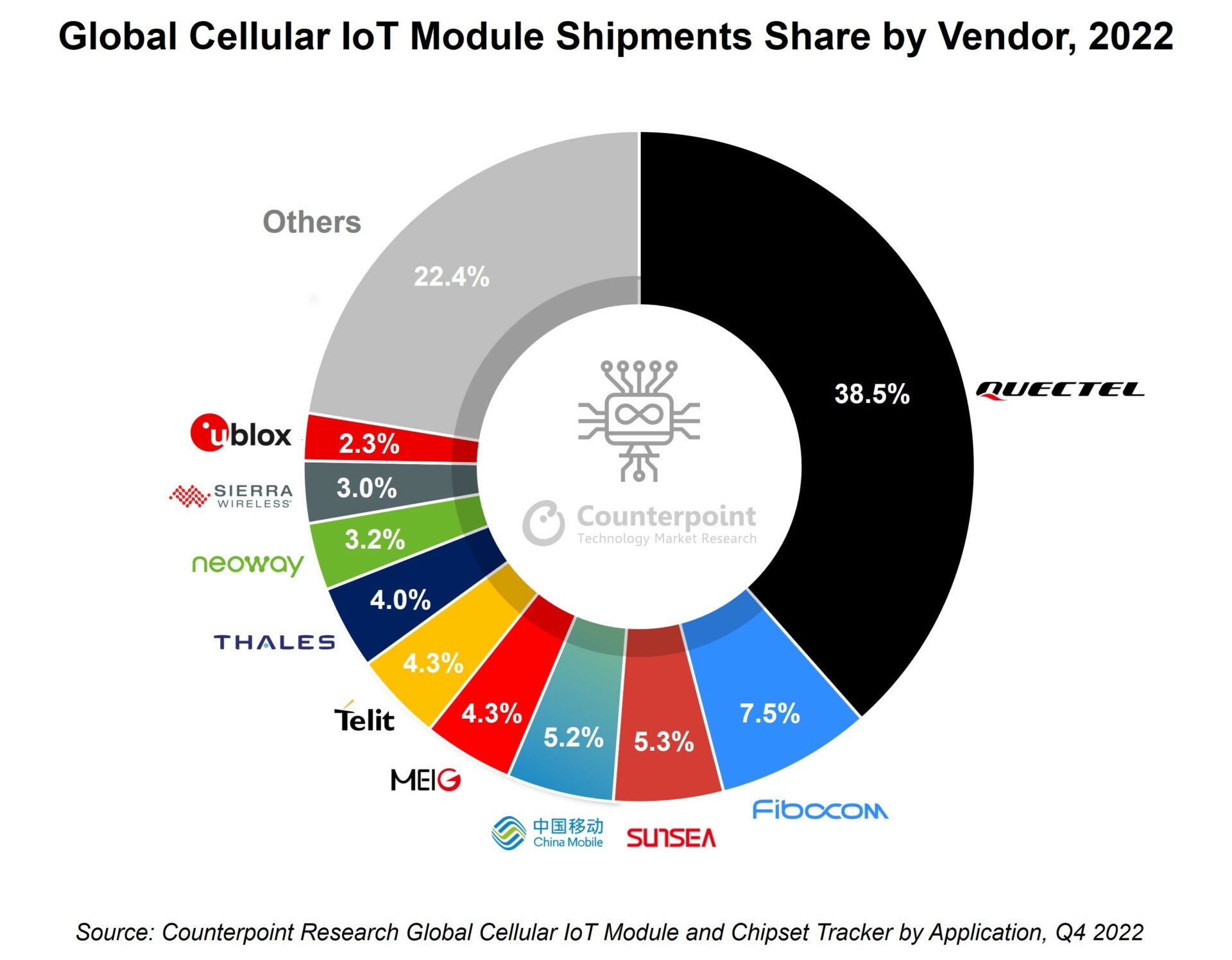

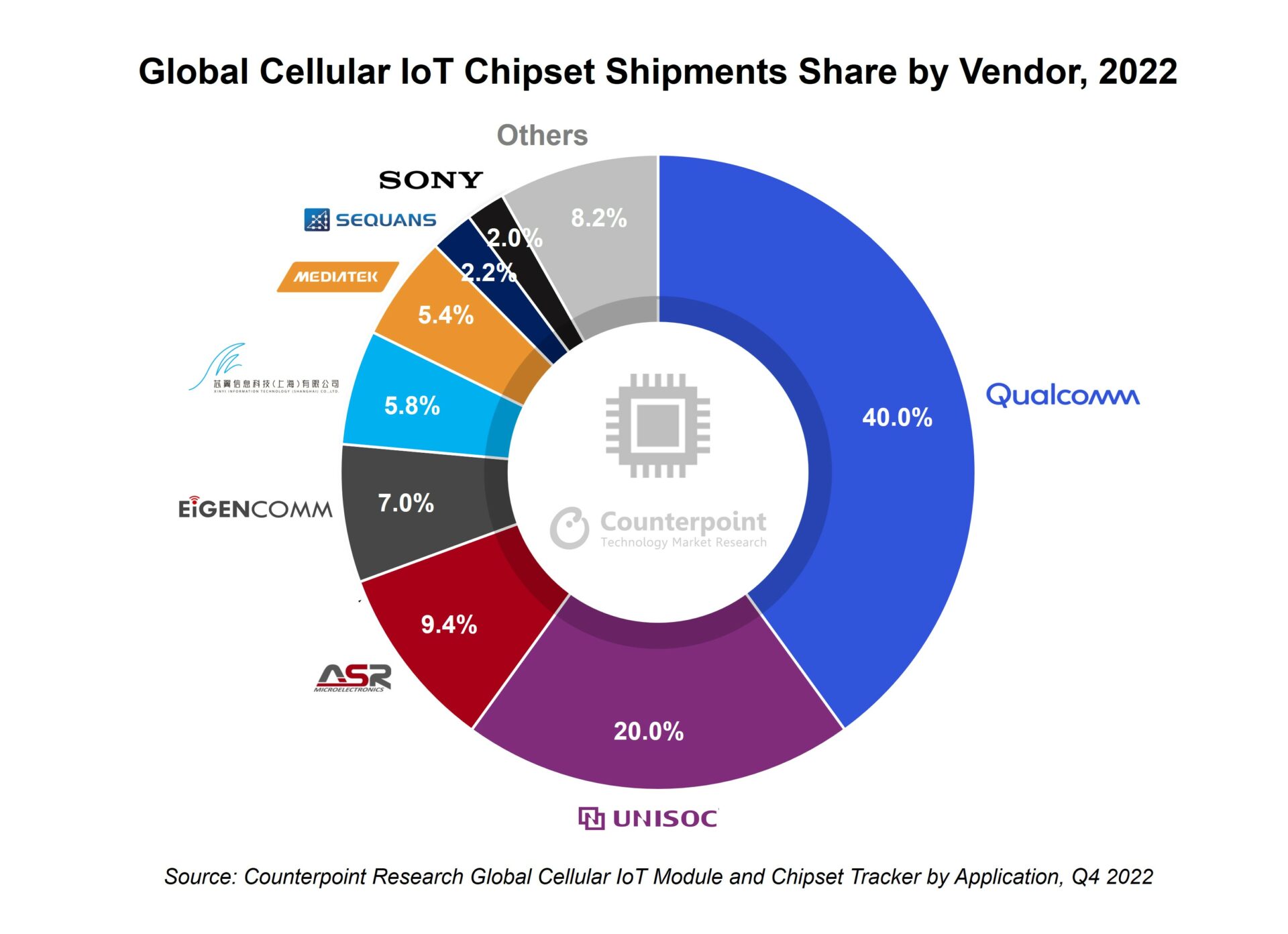

Quectel and Qualcomm dominated the cellular IoT module and chipset markets, respectively.

NB-IoT is still popular among technologies but is expected to lose some market share to 4G CAT1.bis in 2023.

5G adoption to get a boost in 2024 if ASP declines to sub-$100 and 5G RedCap-based solutions become available.

China continues to lead IoT module market, followed by North America and Western Europe.

San Diego, Buenos Aires, London, New Delhi, Hong Kong, Beijing, Seoul – March 29, 2023

Global cellular IoT module shipments grew 14% YoY in 2022 to register record high annual volume, despite macroeconomic headwinds, according to Counterpoint’s latestGlobal Cellular IoT Module and Chipset Tracker by Applicationreport. The resumption of smart meter implementation, ongoing retail POS upgrades, intelligentasset trackingand the continued growth in connected cars due to progress in electrification and autonomous capabilities were some of the key drivers for the double-digit percentage growth in demand for IoT modules.

Chinacontinued to lead the global cellular IoT module market in terms of demand, followed byNorth AmericaandWestern Europe.Meanwhile,Indiawas the fastest growing market, followed by Latin America and North America. Although India has a smaller base, it has immense potential.Eastern Europewas the only region that registered a decline due to the prolonged Ukraine-Russia war.

Commenting on the competitive dynamics among cellular IoT module OEMs,Senior Research AnalystSoumen Mandalsaid, “In 2022, Quectel was the top cellular IoT module player inChina, the world’s largest market for these components. Meanwhile, China Mobile and Fibocom captured second and third place, respectively, enjoying their tremendous scale in the domestic market. Outside of China, Quectel remained the leader followed by Telit and Thales which have merged and will commence operations as a new brand,Telit Cinterion,starting Q1 2023.

Quectelincreased its focus in the consolidating automotive (NAD module) segment in 2022 and secured multiple design wins with major automakers. The competition in the NAD module market is intensifying as the industry transitions to 5G connectivity. With every transition of cellular technology, we have seen the market consolidate as it becomes increasingly challenging to serve the automotive segment, which requires heavy customization but garners a lower margin.

China Mobile, the world’s largest CSP and IoT connectivity player, is becoming more vertically integrated by leveraging its massive scale to capture maximum value. It has the potential to break into the top three global cellular IoT module rankings this year. However, the company primarily operates in China and will need to expand into other verticals and markets via a robust partnership model to maintain its momentum.”

Commenting on the IoT cellular connectivity chipset player dynamics,Associate DirectorEthan Qisaid, “Qualcommcontinued to dominate the cellularIoT chipsetmarket in 2022 with nearly 40% shipments share. Qualcomm strengthened its position in the LTE CAT 4 and higher technologies while also maintaining a dominant position in the 5G market. Qualcomm recently launched its latest 4G CAT1.bis chipset, QCX216, to compete head-on with the LTE CAT1.bis leaders UNISOC and Eigencomm.

Qiadded, “In 2022, UNISOCandASRmaintained their second and third positions due to strong adoption of the fast-growing LTE CAT1.bis and CAT 1 based modules, respectively. During the year, two new players from China,EigencommandXinyi Semiconductor,broke into the top five cellular IoT chipset vendor rankings, filling the gap left by Hisilicon. Eigencomm focuses on NB-IoT and 4G CAT1.bis applications while Xinyi Semiconductor focuses on NB-IoT chipsets, both being low-cost but high-volume segments.”

Commenting on the technology landscape,Mandaladded, “During 2022,NB-IoTremained the most popular LPWA IoT connectivity technology followed by the fast-growing 4G CAT 1 and 4G CAT 4 modules. Together, these contributed to 60% of the total IoT module market. For most of 2022, China was under lockdown due to the resurgence of COVID-19 which drove greater demand for products such as smart door locks, digital thermometers and wearables, mostly powered by NB-IoT.

NB-IoT saw strong adoption in China but has been less popular outside the country. In contrast,4G CAT.1bishas been gaining traction globally and has the potential to be an alternative to several NB-IoT and existing 2G/3G applications such as smart meters. However,5Gsaw slower adoption in IoT than in smartphones last year due to the higher module costs. The key initial 5G applications are PCs, CPEs and some industrial/enterprise applications.

We believe 5G will enter the mainstream market once the module ASP breaks the sub-$100 barrier and receives a further boost from the5G RedCapcommercialization in coming years.”

Commenting on the IoT market outlook for 2023,Associate DirectorMohit Agrawalsaid, “Global cellular IoT module shipments (including NAD modules) are expected to register robust growth of19%YoY in 2023. The growth of IoT module shipments in the high-value industrial segment will be key for the IoT projects that have struggled to move beyond the pilot stage and for companies that are focusing more on ROI in a tough macroeconomic environment. Nevertheless, shipments of IoT modules for thesmart meter,point of sale(POS) and theautomotivemarkets are expected to continue seeing strong growth, which will offset a slowdown in other segments.”

The market has been undergoingconsolidationacross theIoTvalue chain from module players andconnectivitymanagement to IoTplatform的球员。这凸显了sc的重要性ale, choosing the right vertical and capturing value by striking the right partnerships or developing the right capabilities. We could see some more exits and mergers in 2023 because IoT, which is very vertical driven, has been seeing volatile growth due to internal or external factors.”

For detailed research, refer to the following reports available for subscribing clients and individuals:

Counterpoint tracks 1,500+ IoT module SKUs on a quarterly basis and provides forecasts on shipments, revenues and ASP performances for 80+ IoT module vendors, 12+ chipset players and 18+ IoT applications across 10 major geographies.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the technology, media and telecom (TMT) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Qualcomm dominates automotive connectivity chipset market with more than 80% share

Rolling Wireless leads the automotive connectivity module market, followed by LG and Quectel

One in two connected cars will have 5G connectivity by 2027

San Diego, Buenos Aires, London, New Delhi, Hong Kong, Beijing, Seoul – September 22, 2022

Global automotive connectivity module and chipset shipments grew by just 3% YoY in H1 2022, according to the latest research from Counterpoint’sGlobal Automotive NAD Module and Chipset Tracker.

Chinais the largest region as electric vehicle players, including new start-ups such asNIO, Xpeng Motor and Seres, are offering infotainment systems with large displays and smart cockpit solutions that have a wide array of features, andADASthat requires embedded connectivity. But during H1 2022, automotive connectivity module shipments in China declined by almost 7% YoY due to slow car production caused bysupply chain disruptionand COVID-19 restrictions.

Automakers across Europe are trying to generate significant revenues from in-car software services via subscriptions. For this, they are now offering embedded connectivity, even in lower vehicle trims. TheUkraine crisisderailed the European automotive market’s post-COVID recovery. Automotive connectivity module shipments in Europe declined by more than 10% YoY as car production in Germany, France, UK, and other European nations suffered due to the lack of components caused by the Ukraine crisis.

While the two biggest markets could not avoid the effects of the geopolitical crisis and fresh COVID restrictions, North America remained more resilient with automotive connectivity module shipments increasing by 27% YoY during H1 2022.

Commenting on the market dynamics,SeniorResearch AnalystSoumen Mandalsaid, “With the increasing adoption of digital features andADAS, the requirement for embedded connectivity in passenger vehicles will increase. The sales penetration ofconnected carssurpassed those of non-connected cars for the first time H1 2022. Previously, embedded connectivity was prevalent in luxury models, but now mainstream players like Volkswagen, Toyota and Stellantis are offering connectivity for their mass-market cars.

Qualcommhas a dominant position in the chipset market with more than 80% market share. The strong product portfolio and partnerships with major tier-1 suppliers and automakers are all helping Qualcomm. And now, Qualcomm is offering complete solutions for automotive digital transformation starting with hardware and extending to cloud services with the Snapdragon Digital Chassis. This one-stop solution is helping ecosystem players reduce time to market and be more competitive.

联发科和三星推出5克去年你们的解决方案ar. As the automotive sector is gradually adopting 5Gconnectivity,我们预计联发科和三星增加market share in 5G automotive connectivity. However, they will likely require a more concerted effort to substantially grow their share and benefit from greater economies of scale.”

Source: Counterpoint Global Automotive NAD Module and Chipset Tracker, Q2 2022

Automotive specialists lead, but IoT giants aiming for slice of module market

Commenting on the automotive connectivity module player dynamics,Research Vice PresidentNeil Shahsaid, “Automotive connectivity modules must pass various quality and compliance tests and certifications, hence special expertise is an advantage. Consequently specialist automotive connectivity module players such as Rolling Wireless and LG areleading the market.最大的物联网模块Quectel球员,broken into the top three rankings due to strong performance in its domestic China market. We have seen Quectel gain certification for automotive-grade modules with North American and European telecom operators. This will give strong competition to traditional specialist players like Rolling Wireless, LG, Continental and Harman.

The entry barriers are relatively high for IoT module players but the revenue opportunity afforded by the automotive transformation is attractive. Nevertheless, geopolitical trade tensions and data security concerns will likely be a barrier to Chinese IoT module players penetrating international markets.

Automakers will aim to multisource modules to offset supply-chain risks while supporting the growing demand for connectivity. In addition, we expect some emerging countries like India, Indonesia, Thailand and Brazil will try to build their own manufacturing ecosystem to have better control over the supply chain.”

Source: Counterpoint Global Automotive NAD Module and Chipset Tracker, Q2 2022

Discussing the market outlook,Research Vice PresidentPeter Richardsoncommented, “Automotive connectivity module shipments are expected to grow annually by around 11% on average to reach 97 million units by 2030. The demand for 5G modules is increasing and we expect around a half of connected cars sold in 2027 will have 5G connectivity. The evolution of centralised architecture with digital cockpit, autonomous capability (ADAS L3+) and electrification will drive growth for 5G technology.

In terms of revenue, the automotive connectivity module market is projected to reach $5 billion by 2030. The multi-billion segment opportunity will ensure the segment remains vibrant and highly competitive.”

For detailed research, refer to the following reports available for subscribing clients and individual subscription:

Counterpoint tracks and forecasts on a quarterly basis 25+ NAD module vendors’ shipments, revenues and ASP performance across 10+ chipset players, and major geographies.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

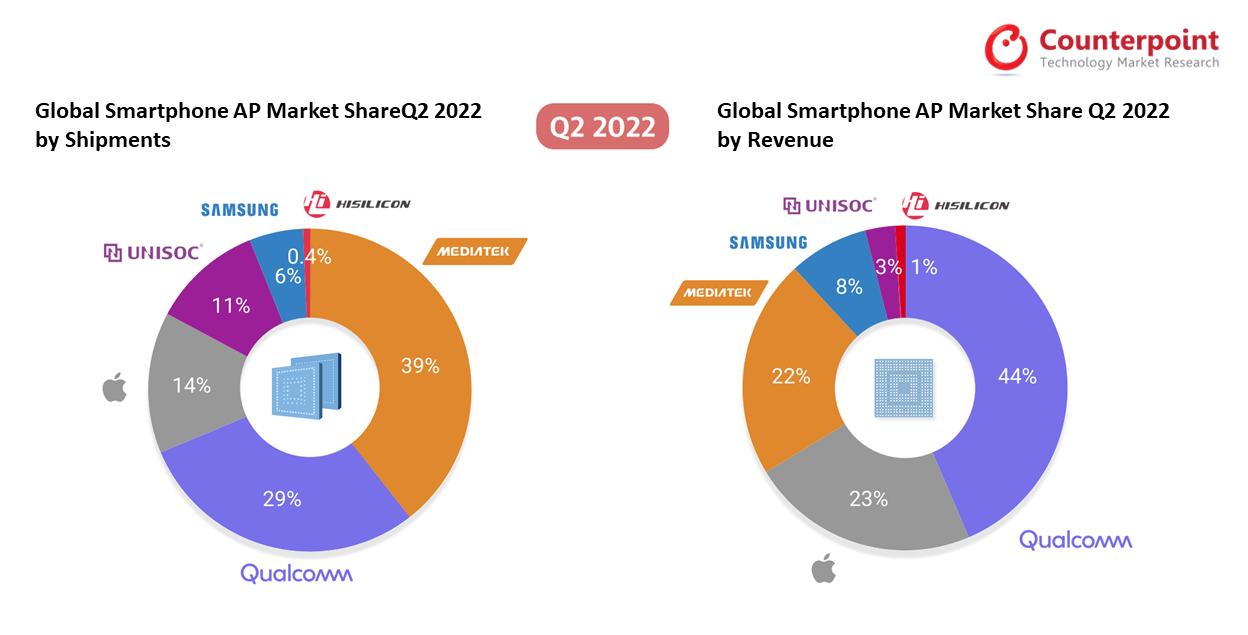

MediaTek dominated the smartphone SoC market with a share of 39%. MediaTek leads the low-mid tier wholesale price segment, driven by its Helio G series and Dimensity 700 series. There is a slight decline in MediaTek shipments in Q2 2022 compared to the previous quarter due to order cuts from major Chinese OEMs. Qualcomm captured a 29% share in the quarter. Qualcomm maintained its position in the premium segment despite tough macroeconomic situations and the declining smartphone market.

Global Smartphone AP Market Share by Revenue

Qualcomm has dominated the AP market by 44% in terms of revenue in Q2 2022. The share for Qualcomm has grown 56% YoY in Q2 2022 driven by the higher premium mix which has led to growth in the ASPs. Also, the recently announced partnership between Qualcomm and Samsung for the galaxy s22 family will support the revenues for the premium tier. MediaTek has captured a 22% share in the AP market. Qualcomm further gains revenues from baseband shipped to Apple. MediaTek’s revenue was driven by the higher 5G ASP and entry into the premium market with Dimensity 9000 series.

Use the button below to download the high-resolution PDF of the infographic:

After declining in Q1 2022, the global cellular IoT module market recovered in Q2 2022 despite macroeconomic headwinds and lockdowns in China, the largest IoT market.

The quarter also saw a series of consolidations in the highly competitive IoT module space.

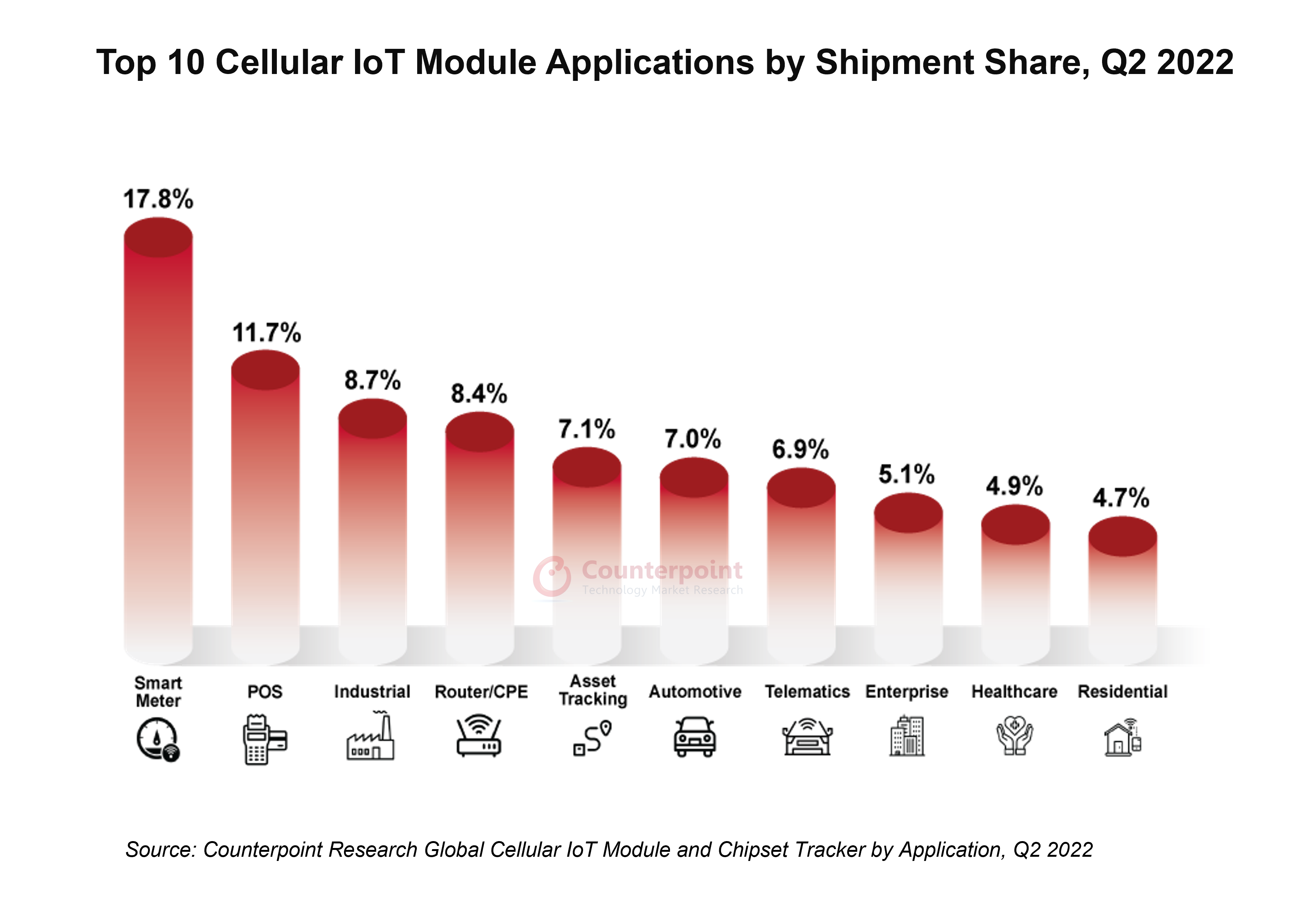

Asset-tracking reached the highest share ever at 7% to break into the top five applications.

Smart meter, POS and industrial were the top three applications in this quarter.

NB-IoT and 4G Cat 1 were the most preferred technologies for cellular IoT applications.

San Diego, Buenos Aires, London, New Delhi, Hong Kong, Beijing, Seoul – September 20, 2022

Global cellular IoT module shipments grew 20% YoY in Q2 2022, according to the latest research from Counterpoint’sGlobal Cellular IoT Module and Chipset Tracker by Application.The global cellular IoT module market continued to recover despite a tighter supply chain, COVID-19 lockdowns in China and macroeconomic headwinds. The growth was driven by the ongoing digital transformation involvingpotential applicationsaround critical infrastructure and logistics catered by some key fast-growing low-tier cellular technologies such as Cat-1 and NB-IoT. Further, module players modified their product offerings, striking partnerships across the value chain, from newer connectivity solution providers to acquiring some key competitors, as the IoT industry enters a very exciting growth phase.

Chinaretained its position as the world’s largest IoT market, contributing to more than half of the demand despite the lockdowns. The country’s cellular IoT module market recovered slightly from previous months this year, driven by lockdown-triggered applications like smart locks, surveillance systems and routers. The North American and western European markets grew steadily and held their second and third positions respectively in the global cellular IoT module market. Again,Indiawas the fastest growing IoT module market (+264% YoY), albeit growing on a lower base, driven by smart meter, telematics, POS and automotive applications.

Commenting on the market dynamics,SeniorResearch AnalystSoumen Mandalsaid, “The IoT module market is going through a critical phase where the Chinese brands have become bigger, making it very difficult for international brands to grow in silos. As a result, we have seen the first wave of market consolidation withTelitacquiring Thales’ cellular IoT module business as well as acquiring IoT solutions design house Mobilogix. Also, during the quarter,Semtech, one of the big component vendors and the key chipset provider for the proprietary LoRa-based IoT network, acquired leading cellular IoT and router vendor Sierra Wireless to build an end-to-end wireless IoT portfolio. This kickstarts an exciting phase where the Western vendors are trying to become more ‘integrated’ to capture more value across the value chain, even though the IoT market is a blue-ocean opportunity.”

Mandal added, “With six out of the top 10 IoT module vendors being fromChinaand with the rising geopolitical competition and data privacy concerns, international players see an opportunity to consolidate and carve out a dichotomy in this segment. Further, having a robust portfolio and post-sales support is the key. Telit, Thales, u-blox and Sierra Wireless improving their offerings over the last 12 months has been a step in the right direction. With consolidation, these vendors can garnerscaleand some competitive edge to at least compete well on pricing and value against the competition”

Note: Figures may not add up to 100% due to rounding

Market summary

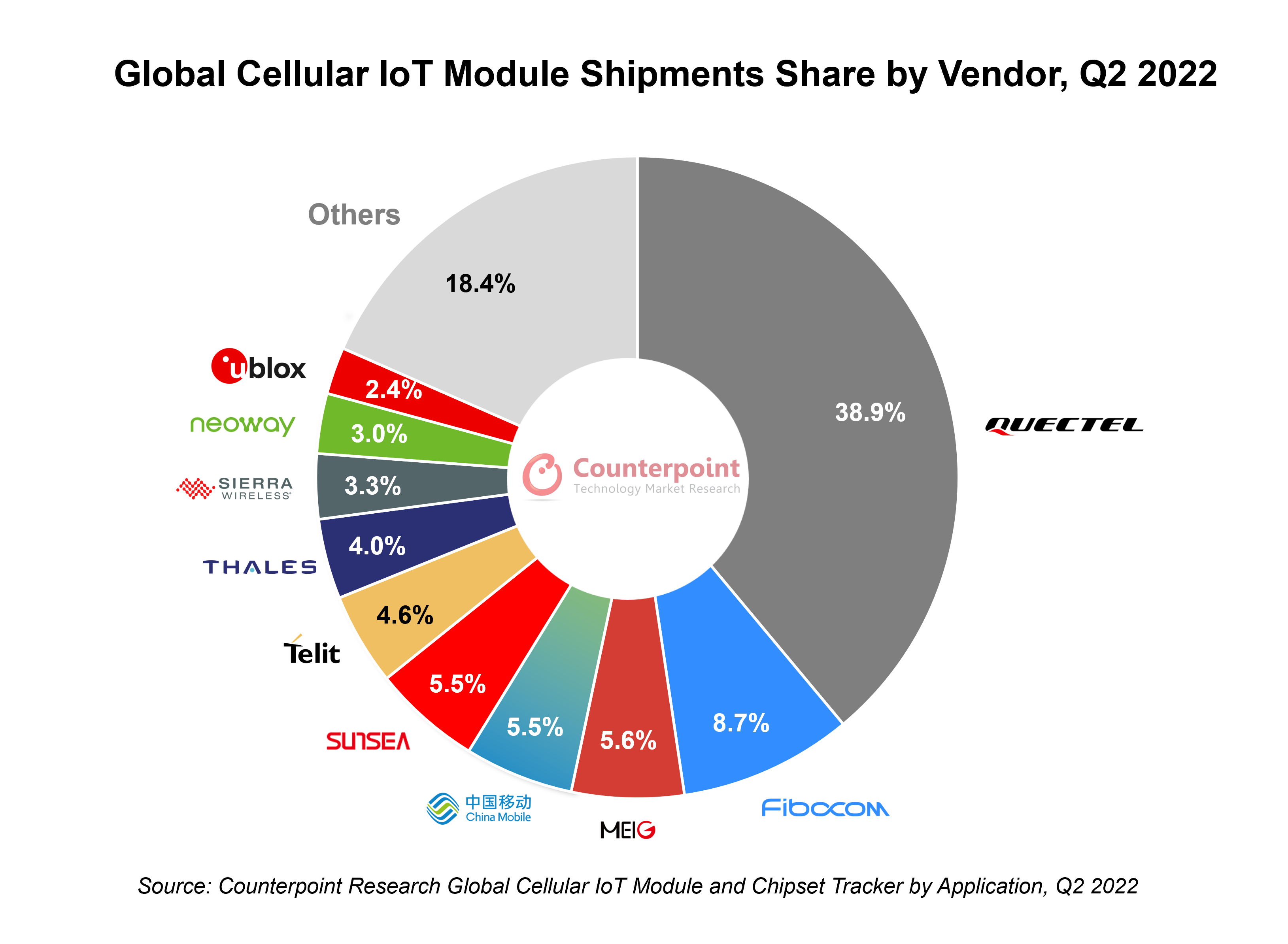

The top three players accounted for more than half of the market. Interestingly,Quectel’s shipment share was equal to that of the remaining players in the top 10 list.

Quectel:Quectel’s module shipments increased 47% YoY, further increasing its gap with the remaining players. During the quarter, Quectel launched 4G Cat 4smart modulesSC200E and SG150H, based on Qualcomm and UNISOC chipsets respectively. Furthermore, Quectel unveilediSIM-supported LPWA module BG773A-GL with the help of Kigen, through which it will be able to target M2M applications such as POS, smart metering, asset tracking and wearable devices.

Fibocom: The second largest module vendor, Fibocom, saw 12% YoY growth in its module shipments. Nearly 60% of its module shipments came from the China market. Fibocom has already entered partnerships with Qualcomm, MediaTek, UNISOC, Sequans and Autotalks to increase its share in international markets. This can help Fibocom bridge some of its wide gap with Quectel in the international IoT module market.

MeiG:After a slow Q1 2022 due to China lockdowns, MeiG registered growth which helped it to enter the top three IoT module ranks globally. While focusing onhigher-end IoTmodule applications, MeiG is expanding into the fast-growing 4G Cat 1 bis market, targeting applications such as POS, industrial, asset tracking, smart meter and enterprise. MeiG is also diversifying its supplier portfolio. It has partnered with fast-growing 4G chipset vendor ASR for the 4G Cat 4 module market, especially for the highly competitive China market and other low-cost international markets.

China Mobile:中国移动保持第四的位置global cellular IoT module market by catering to its huge existing and prospective customer base and extensive cellular network. The operator partnered with Xinyi Semiconductor for focusing on lower-end applications. This has helped both to target 2G-to-4G transitioning IoT applications. China Mobile’s growing 5G footprint and partnerships across the value chain will help the world’s largest operator to rapidly scale its end-to-end 5G IoT solutions in the coming quarters.

Sunsea:Sunsea (SIMCom + Longsung) has been consistently improving its performance over the last 10 quarters. Sunsea is following a strategy similar to that of other Chinese players to offerQualcomm-based solutions for the international market and MediaTek/UNISOC/ASR/Xinyi-based solutions for the homegrown China market. Sunsea added ASR as a partner besides Qualcomm to cater to the increasing demand and offer affordable pricing in China.

Telit:Telit is the first non-China player in the global IoT module vendors’ rankings. Telit is focussing on LPWA-Dual Mode, 4G Cat 1 and LTE-M technologies to target applications such as industrial, healthcare, asset tracking, router/CPE and energy. The vendor has launched 4G Cat 1 bis industrial grade module LE910R1 with 2G fallback to target the APAC and EMEA markets. With the sunset of 2G and 3G technology, this module can be used as a substitute for low-to-mid-end applications. After the acquisition of Thales, Telit has the potential to emerge as the largest module vendor outside of China and eventually match Quectel in scale.

Among other players,Neowayperformed well. It was the fastest growing in QoQ terms (+162%) among top vendors. Besides China, India is turning out to be an important market.

u-bloxrecorded a strong quarter by remodeling and redesigning its products and clearing backlogs. The demand was strong for u-blox in industrial,automotiveand healthcare applications.

Commenting on the key connectivity technology trends in the IoT space,Associate DirectorMohit Agrawalsaid, “The top five technologies, including NB-IoT, 4G Cat 1, 4G Cat 4, 4G Cat 1 bis and LPWA-Dual Mode captured more than 80% of the shipments in this quarter. We are witnessing increasing shipments of 4G Cat 1 and 4G Cat 1 bis modules driven by the sunset of 2G and 3G technologies and higher demand in low-to-mid-end applications. Some module players are still shipping 2G modules to cater to specific low-cost applications in some emerging markets, like Africa, Asia and eastern Europe. The 5G IoT module shipments remain steady withpricesstill high and many projects still in pilot stages. It will take at least a couple of years to reach an inflection point. We expect the second half of 2023 to see a ramp-up for the 5G IoT modules with good pan-country5Gcoverage and scale.”

The top five applications in Q2 2022 – smart meter,POS, industrial, router/CPE and asset tracking – captured more than half of the totalIoT modulemarket. Compared to the previous quarter, significant improvements were seen in the router/CPE and residential markets. Theautomotiveconnectivity market did not show much traction due to the poor performance of the automotive industry in China during this quarter.

For detailed research, refer to the following reports available for subscribing clients and individuals:

Counterpoint tracks and forecasts on a quarterly basis 1,500+ IoT module SKUs’ shipment, revenue and ASP performance across 80+ IoT module vendors, 12+ chipset players, 18+ IoT applications and 10 major geographies.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Qualcomm, UNISOC, ASR and MediaTek were the top four cellular IoT chipset vendors in Q1 2022.

4G (Cat 1 and Cat 1 bis) contributed to almost one-third of the cellular IoT module chipset shipments.

Smart meters, POS, industrial, automotive and telematics were the top five applications in the quarter.

New Delhi,San Diego, Buenos Aires, London, Hong Kong, Beijing, Seoul – July 7, 2022

Global cellular IoT module chipset shipments grew 35% YoY in Q1 2022, according to the latest research from Counterpoint’sGlobal Cellular IoT Module and Chipset Tracker by Application.China was the key region for cellular IoT module chipset consumption during the quarter, with China, North America and Western Europe accounting for over 75% of the volume. PC, router/CPE and industrial were the top three applications for 5G.

Commenting on the market dynamics,Research AnalystAnish Khajuriasaid, “Qualcomm, UNISOC and ASR held the top three positions in the global cellular IoT module chipset market in Q1 2022, accounting for nearly 75% of the total shipments.UNISOC,QualcommandASRwere top chipset players in China in terms of shipments. For the rest of the world,Qualcommled, followed byUNISOCandSequans.4G (Cat 1 and Cat 1 bis) grew 79% YoY in this quarter.”

Qualcommled with a 42% share and 30% YoY growth across nine out of the ten key regions globally. However, competition from local players in China, such as UNISOC and ASR, in key fast-growing segments like LTE Cat-1/Cat-1 bis and NB-IoT limited Qualcomm’s growth opportunities in the world’s largest IoT market, China. However, Qualcomm has been broadening its IoT chipset portfolio, targeting premium 4G and 5G solutions for verticals such as retail,automotive, industrial robotics and smart cities. It is also collaborating with several industry application and technology providers, including Microsoft, ZTE, BMW and Bosch, to focus on high-value artificial intelligence and 5G IoT capabilities, also termed as the5G AIoTsegment.

UNISOC,the second-largest cellular IoT chipset player globally with a 26% share in shipments, has been strong across 4G (Cat 1 and Cat 1 bis) and NB-IoT technologies. Its cellular IoT chipset shipments have continued to grow for nearly last five quarters, filling the gap which HiSilicon left in the market. Moreover, it is making steady improvements in advanced cellular technologies such as 4G Cat4+ and 5G. It has also succeeded in expanding its customer base, addingQuectel, Fibocom, China Mobile and other international module players. This helped it to capture more than one-fourth of shipments in Q1 2022. UNISOC is focused on low-end applications like smart metering,POSand industrial with stronger demand for its Cat1 bis 8910DM chipset.

ASRMicroelectronics保持在第三排在细胞物联网芯片set market in Q1 2022 due to strong performance in the high-volume 4G Cat 1 and 4G Cat 4 module segments. China continues to be the key market for ASR. The company is yet to launchNB-IoT和5 g的解决方案,因此将不得不工作long-term capabilities and strategy to maintain this high growth which could continue through 2025. ASR has increased its production capacity this year to meet demand. Local partnerships with several module players in 4G Cat 1 and Cat 4 technology, like Quectel, SIMCom, Neoway, Longsung and Rinlink, are helping drive the scale.

Commenting on the competitive dynamics,Vice President ResearchNeil Shahsaid, “The cellular modem chipset competition is heating up in the IoT module space with a growing number of players entering the higher-volume LPWA (LTE-M and NB-IoT) and lower-category 4G LTE (Cat 1 and Cat 1 bis) segments as incumbent players such as Qualcomm and MediaTek focus on the higher-value and more integrated 4G LTE and 5G segments. The move from a two-chip (discrete MCU + cellular modem) to an integrated SoC solution is happening as we enter the 5G era. Further, the addition of AI/ML capabilities in future advanced cellular IoT applications is also catalyzing this trend. However, the low-power and less advanced applications will continue to prevail into the next decade and we could see some adoption of SoC-based integrated solutions. But the discrete solutions will prevail, driving sizeable opportunities for the likes of UNISOC, ASR, Sequans, Sony Semi, Eigencomm, Xinyi and Nordic Semi.”

Other Players

MediaTektook the fourth position in this market. However, it is not much focused on the cellular IoT market compared to the smartphone chipset market. This is one of the key reasons for MediaTek having a 5% shipment share in this quarter. The company is also focusing on 5G enhancement and recently launched Kompanio 900T, a new 5G platform for tablets, notebooks and other IoT devices. The MediaTek T750 chipset launched earlier is growing strong inFWA and CPEdevices.

Global Cellular IoT Module Chipset Shipments Share by Vendor, Q1 2022

Source: Counterpoint Global Cellular IoT Module and Chipset Tracker by Region, Q1 2022

Eigencomm注册gro最高wth of 869% YoY during Q1 2022, thanks to a strong partnership with Quectel and Fibocom for NB-IoT modules. However, the brand needs to diversify in terms of supporting cellular technologies beyond NB-IoT in its portfolio as well as beyond China.

Xinyiwas the second fastest growing chipset player in the market during the quarter with 230% YoY growth. Similar to Eigencomm, the company is currently focusing on the NB-IoT chipset and China region. For the near-to-mid-term, Xinyi needs to leverage its strong partnership with major module vendors such as Quectel, China Mobile, Fibocom, SIMCom, Cheerzing, Longsung, MeiG and Ai-Link and expand into newer cellular technologies to maintain the growth and market share.

Sequanswas also in a growth mode in Q1 2022 with a robust 4G, LPWA and 5G chipset portfolio and rising demand in key markets such as smart meters, healthcare and asset tracking. Sequans is the world’s second chipset vendor after UNISOC to commercialize the 4G Cat-1 bis chipset to increase its share and design wins in the growing Cat 1 bis-based IoT applications.

Sony Semicon(Altair) also saw growth this quarter with solid cooperation with Sierra Wireless and Wistron NeWeb focusing on the markets for smart meters, asset trackers and smart cities. Sony is only focusing on LPWA technology with low-power and high-security features on chipsets.

For detailed research, refer to the following reports available for subscribing clients and also for individual subscriptions:

Counterpoint tracks and forecasts on a quarterly basis 1,450+ IoT module SKUs’ shipments, revenues and ASP performance across 80+ IoT module vendors, 12+ chipset players, 18+ IoT applications and 10 major geographies.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Quectel, Foxconn, China Mobile, WNC, Telit, MeiG, Sequans, Gosuncn were the fastest growing vendors in Q1 2022.

Smart Meters, POS, industrial, automotive and telematics were the top five applications in the quarter.

China, North America, and Western Europe accounted for over 75% of the volume.

San Diego, Buenos Aires, London, New Delhi, Hong Kong, Beijing, Seoul – June 23, 2022

Global cellular IoT module shipments grew 35% YoY in Q1 2022, according to the latest research from Counterpoint’sGlobal Cellular IoT Module and Chipset Tracker by Application.India was the fastest growing market (59% YoY) followed by Middle East Africa, Japan, North America, China, Western Europe and Korea, all registering healthy double-digit growth. However, the largest IoT module market, China, saw demand dip by 11% QoQ due to the new wave of COVID-19 and resulting lockdowns.

Commenting on the market dynamics,SeniorResearch AnalystSoumen Mandalsaid, “The cellular IoT module market remains competitive, but there is growing consolidation. For example, Quectel, Fibocom and Sunsea accounted for more than half of the globalIoTcellular module shipment volumes for the first time ever. This highlights the growing influence, expertise, and scale of these Chinese vendors in the fast-growing global market.

Quectel’scellular IoT module shipments grew 77% YoY in Q1 2022 to a healthy 38% of global volume. Quectel now ships more modules than the next ten vendors combined. Quectel continues to dominate geographically with leadership in seven out of ten key markets globally.Quectelcommands a strong position in 4G and NB-IoT modules. Quectel is expanding its 5G portfolio and aims to gain scale as the technology ramps.

Fibocom’s shipments grew by 24% YoY benefitting from the surging demand for 4G Cat 1 bis modules, which is one of the fastest growing segments and led by Fibocom globally. 4G Cat 1 bis is becoming a key technology targeting the 2G and 3G IoT installed base and similar applications such as POS andtelematics.Fibocom is also heavily focusing on 5GAIoTbased smart modules to maintain a lead in high value applications.

SunseaAIoT which includes the brands SIMcom and Longsung, has cemented its place in the top three brands. It focuses on 4G Cat-1 and NB-IoT modules. China continues to be the key market for Sunsea; it will need to diversify if it wants to scale and grow at the same pace as its peers.

Telitcaptured 4.6% share and is the only non-Chinese brand in the top five players. Demand for its modules remains healthy in North and Latin America. The module mix shifted slightly with increasing demand for legacy 2G and 3G modules offsetting some volume decline in 4G modules due to supply chain constraints. Telit leads the Latin America market and is among the top three vendors in North America.

China Mobile,Sierra Wirelessandu-bloximproved their market share in Q1. The world’s largest EMS,Foxconn, also entered our top ten module players list with growing demand in the CPE and connected PC segments. The relationship with top device makers, potentialEVbusiness growth and a focus on 5G technology, should help Foxconn to grow in this sector in the mid- to long-term.”

Commenting on cellular IoT technology evolution,Associate DirectorEthan Qi, said, “There is a significant shift happening in the adoption and proliferation of different cellular IoT access technologies, from LPWA (NB-IoT, LTE-M) to 4G (Cat 1, Cat 1 bis) to 4G Cat 3+, 5G and upcoming5G Redcap.This is driven not only by the wide range of different applications, but also regional and operator adoption dynamics. NB-IoT is considered a key and fast-growing technology for low power IoT applications and has been widely adopted in China and some other parts of the world. Whereas LTE-M is preferred in markets such as Japan, Australia, North America, and parts of Europe. However, we are also witnessing many regions and operators favouring 4G Cat 1 and Cat 1 bis for some mature and some new IoT applications. While most of these technologies are complimentary, operators still have to selectively invest in one over others, depending on the IoT verticals of most importance to them.

As we see 5G rolling out, many of the advanced IoT applications such asautomotive, router CPEs, PCs will move to 5G from advanced 4G technologies. Furthermore, the advent of 5G Redcap will also supplant some legacy technologies such as 3G/4G in some IoT applications. So, the entire IoT ecosystem has a wide array of cellular access technology solutions to choose from depending on the applications, data requirements, cost constraints and operator dynamics in a particular market.

The technology mix also shapes the overall cellular IoT module Average Selling Price (ASP), which declined by 3% annually in Q1 due to an increasing mix of lower cost 4G Cat 1 and 4G Cat 1 bis modules. Furthermore, the 4G Cat 4+ modules are still facing supply chain constraints and the % share of 5G modules remains small contributing to the overall ASP decline. We believe the 4G module supply chain issues will moderate later this year, but the fallingASPfor 5G modules will provide an option for device OEMs to either select 4G or 5G modules moving forward.”

Commenting on which IoT applications are hottest,Research Vice PresidentNeil Shahsaid, “Cellular IoT powers a diverse set of applications and the number of things that can be connected to the internet continues to rise.

Smart meters,POSand industrial were the top three applications in the global cellularIoTmodule market in Q1 2022. These segments are contributing to nearly 40% of total cellular IoT module shipments.

Smart meter projects have restarted in many markets post-COVID and the segment is seeing strong growth with shipments doubling compared to a year ago. Meanwhile, demand in the router/CPE segment is steadily growing as the supply constraints lessen and demand increases forFWA CPEsfor the work-from-home segment, and 4G/5G upgrade projects increase for enterprise-grade routers across retail, factories, offices, etc.”

For detailed research, refer to the following reports available for subscribing clients and also for individual subscription:

Counterpoint tracks and forecasts on a quarterly basis 1500+ IoT module SKUs’ shipments, revenues, and ASP performance across 80+ IoT module vendors, 12+ chipset players, 18+ IoT applications and 10 major geographies.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

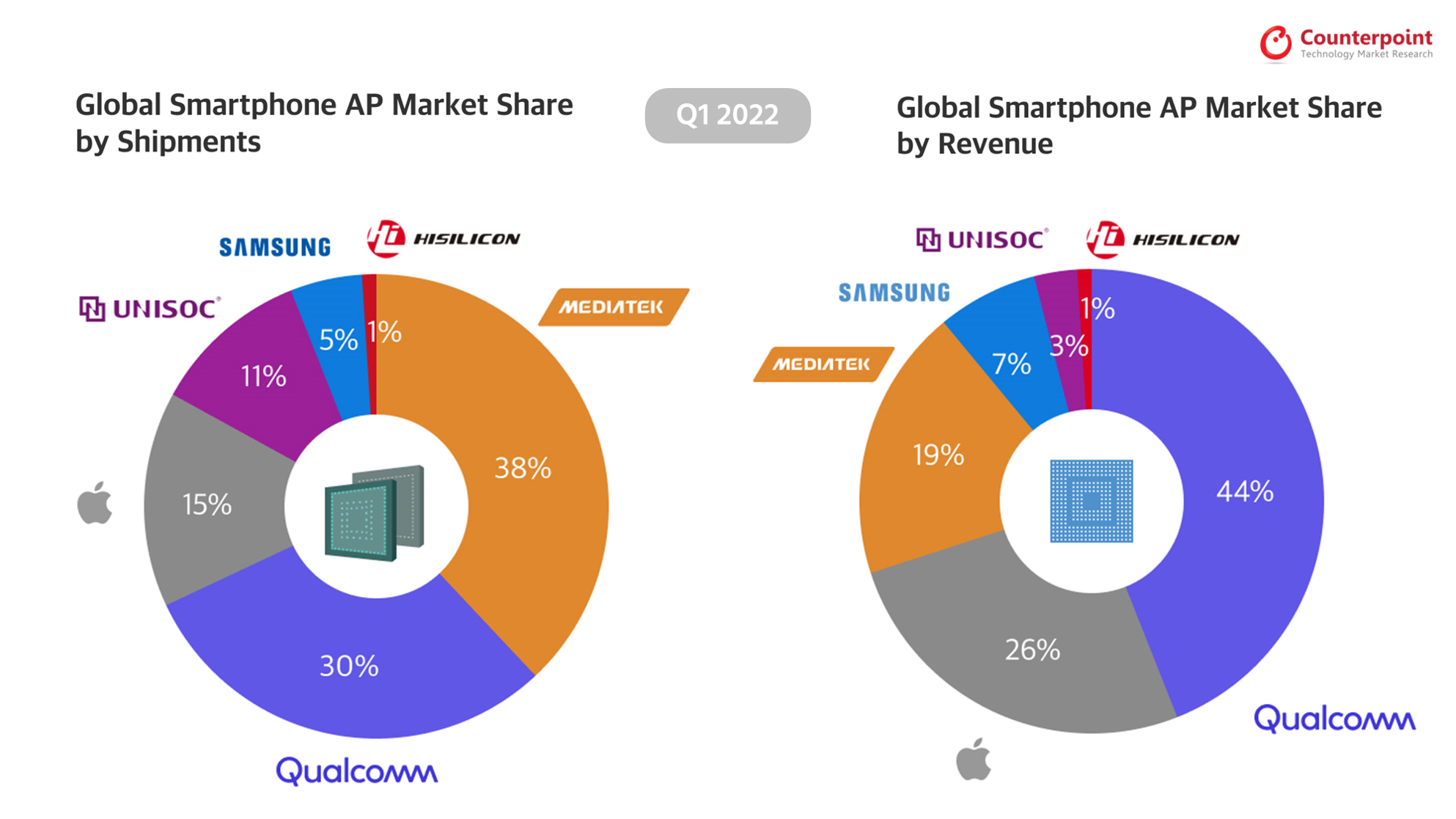

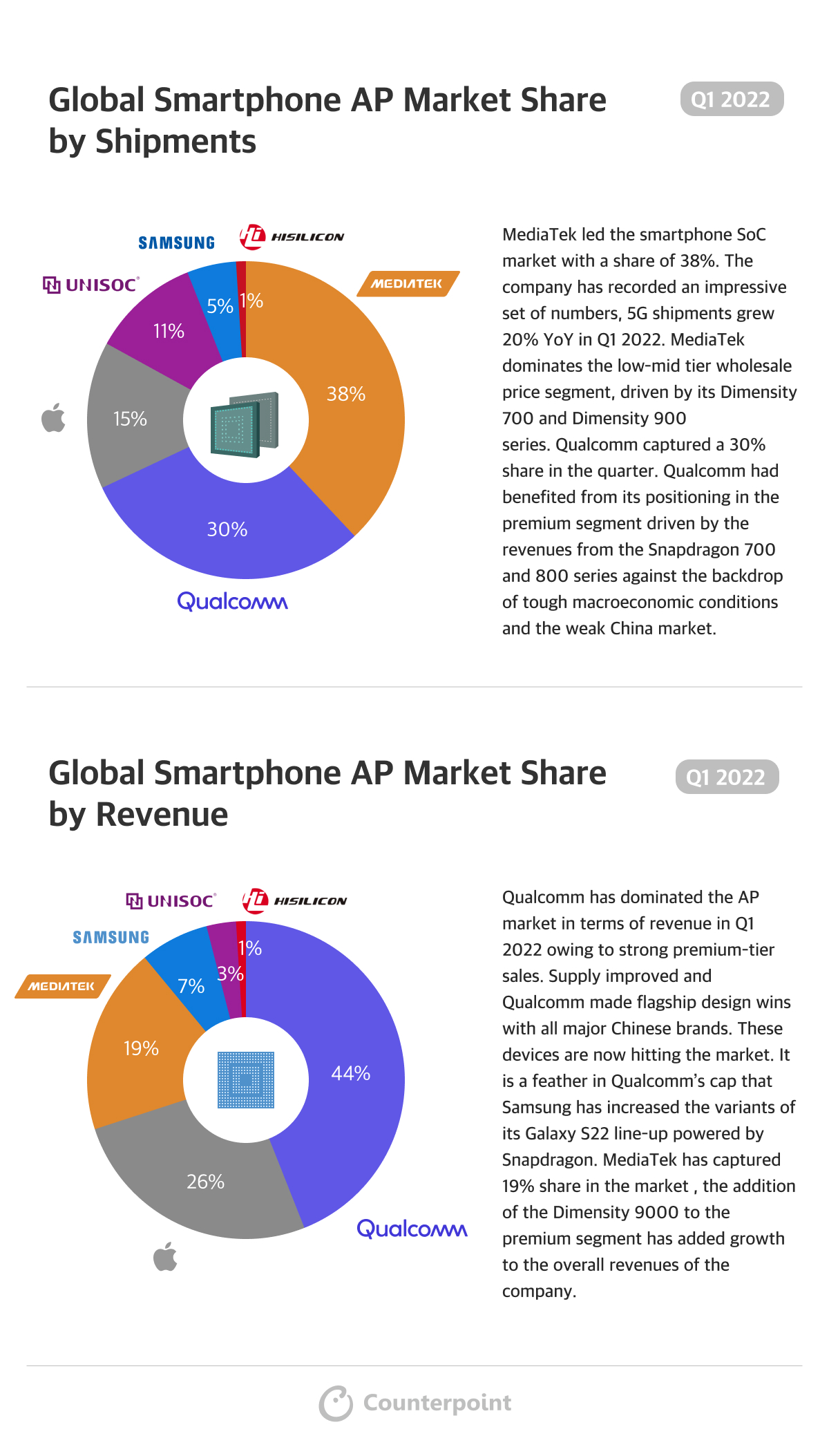

MediaTek led the smartphone SoC market with a share of 38%. The company has recorded an impressive set of numbers, 5G shipments grew 20% YoY in Q1 2022. MediaTek dominates the low-mid tier wholesale price segment, driven by its Dimensity 700 and Dimensity 900 series.

Global Smartphone AP Market Share by Revenue

Qualcomm has dominated the AP market in terms of revenue in Q1 2022 owing to strong premium-tier sales. Supply improved and Qualcomm made flagship design wins with all major Chinese brands. These devices are now hitting the market. It is a feather in Qualcomm’s cap that Samsung has increased the variants of its Galaxy S22 line-up powered by Snapdragon.

Use the button below to download the high resolution PDF of the infographic:

Both Qualcomm and MediaTek posted healthy growth in Q1 2022.MediaTekrecorded an impressive set of numbers for the quarter with revenues growing 32% YoY and 10.2% QoQ to reach $4.8 billion. Qualcomm saw its third consecutive quarterly record revenue in Q1 2022 at $11.6 billion. Its business units recorded annual growth of between 28% and 61%.

MediaTek led the Android smartphone SoC market in 2021 with a 44% share, followed by Qualcomm with 35%, according to the latest research from Counterpoint’sGlobal Handset Model Sales Tracker.

Qualcomm’s focus on the premium smartphone segment (>$500) has helped it to grow revenues. Its Snapdragon 800 series and Snapdragon 700 series, notably the flagshipSnapdragon 8 Gen 1and Snapdragon 778G, are both key volume drivers. Furthermore, Qualcomm has gained a 75% share of Samsung’s Galaxy S22 series shipments. In previous Samsung flagship models, there was a more equitable split between Qualcomm Snapdragon-powered SKUs and Samsung Exynos-powered SKUs. Qualcomm is also driving more revenues with its RFFE (RF Front End), allowing it to capture a higher share in theBoM.

MediaTekdominates the low-mid tier wholesale price segment ($100-$299), driven by its Dimensity 700 and Dimensity 900 series. Also, the 4G SoC in the <$199 price band is driven by the P35, G80 and G35 chipset models. MediaTek has entered the premium segment with the Dimensity 9000 series, but the sales will only start to pick up in Q2 2022.

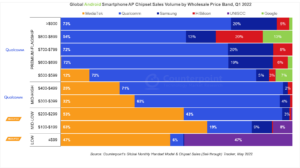

AP Chipset Share for Android Smartphones by Price Band, Q1 2022

Qualcomm

Qualcomm专注于高端(> 500美元)和矮秆($300-$499) segments for revenue growth. Qualcomm is an industry benchmark when it comes to premium smartphones.

Qualcomm’s focus is on the 7 and 8 seriesSnapdragonchipsets, which drive higher revenue and profitability. Qualcomm acknowledged it has seen a slowdown in the low- and mid-price tiers. But this was more than offset by strong premium-tier sales.

Further, the design wins with 75% of sales of theGalaxy S22family, up from 45% of the S21 family, helped Qualcomm strengthen its position in the premium Android segment in Q1 2022.

Qualcomm’s share in the >$500 band increased from 47% in Q1 2020 to 71% in Q1 2022, growing 23% YoY in Q1 2022, owing to the launch of its Snapdragon 888 andSnapdragon 8 Gen 1 chipsets.

Focus on the premium segment will help Qualcomm ride out the slowChinamarket, global macro-economic situation and high inventories.

MediaTek

MediaTekdominated the <$299 price tier and drove significant volumes both for 4G and5Gin this tier. Entry of theDimensity 9000enables MediaTek to capture share in the premium band (>$500). This is the first timeMediaTekhas entered this tier. MediaTek has already announced design wins with Chinese smartphone OEMs likeOPPO,vivo,Xiaomiand HONOR. This opens more competition and opportunities for growth in the premium segment.

The volume in the ≤$99 price band was driven byLTEsmartphones, where MediaTek captured a 47% share. LTE SoCs have been affected by the ongoing shortages and will be in short supply in 2022.

In the $100-$299 price band for Android, MediaTek captured a 60% share in Q1 2022 driven by its Dimensity 700 and 900 series.

MediaTek will continue to gain share in the $100-$299 price band as 5G penetrates markets like India, APAC others, LATAM and MEA. Smartphone OEMs likeXiaomi, Samsung,OPPOandvivowill likely launch affordable 5G smartphones under $200.

MediaTek has entered the premium segment with its Dimensity 9000 series. However, the sales are only expected to pick up in Q2 2022.

Overall, we forecast around an 8% share for MediaTek in the premium segment in 2022.MediaTekgrowth in Q2 2022 is expected to come from mid-high range phones due to the shifting of demand fromLTEto5GAP/SOCs. Further, with the launch of the Dimensity 8000 series, MediaTek wants to focus on and consolidate the $300-$499 price bands. This will also help MediaTek pivot volumes from the low-mid segment to mid-high to premium segments.

Samsung

SamsungExynos’ share declined in Q1 2022 due to the loss in share to Qualcomm in theGalaxy S22series and also due to the low yields of the 4nm premium Exynos chipsets.

Share in the premium segment declined from 34% in Q1 2021 to 23% in Q1 2022.

Samsung has launched the Galaxy A33 and A53 with its Exynos 1280 SoCs. These are the volume drivers that will help it to regain share from MediaTek and Qualcomm through the rest of 2022.

In the low-mid segment ($100-$299), Samsung’s share declined to 7% in Q1 2022 from 10% in Q1 2021 due to outsourcing of its models (A, F and M series) to ODMs, which integrated mostly Qualcomm, MediaTek or UNISOC solutions in different models depending on the target price bands.

In the low tier, Samsung is using UNISOC SOCs in the Galaxy A03 smartphone. The share of Samsung smartphones is almost negligible in this segment.

UNISOC

UNISOCcontinues to gain share in the low bands (<$99) driven by the LTE portfolio. Its share in the <$99 band grew to 47% in Q1 2022 from 20% in Q1 2021.

With realme, HONOR, Motorola and Samsung launching phones with its Tiger series SoC, UNISOC has expanded its customer base with design wins at ZTE and TECNO and entry into the Samsung Galaxy A series.

It has also captured an 8% share in the $100-$199 price band with HONOR, realme and Samsung.

For 2022, we expect UNISOC to maintain the momentum with its portfolio catering to LTE smartphones, as MediaTek struggles withsupply issuesfor 4G chipsets and Qualcomm focuses on5Gsolutions. Also, a few design wins with 5G chipsets will add to its overall volumes and help support its value growth.

HiSilicon

We expectHiSiliconvolumes to decline in 2022 as the inventory is depleted. Huawei has already started using Qualcomm SoCs in its new launches, but these are limited to 4G due to the prevailing US sanctions.

u-blox, a global leader in wireless and positioning technologies, has announced its 2021 financial results. The company made a strong rebound after the strong decline in 2020. Revenue reached a record $453.1 million in 2021, an increase of 27.6% from the previous year.

u-blox achieved strong growth across all segments in 2021. Theautomotivesegment grew 41% YoY due to higher demand for navigation and infotainment applications, especially forelectricvehicles. The industrial and consumer segments grew 24% and 51% from 2020, respectively.

In 2021, the revenue from Americas increased 37.6% YoY driven by strong demand for navigation, infotainment and industrial automation solutions after the decline in 2020. The strong recovery in the automotive sector and consumer telematics helped EMEA revenue to increase by 30.1%. APAC revenue increased by only 11.8% as China’s revenue remained flat due to COVID-19 andsupply chainshortages. However, strong demand for industrial automation, navigation and automated driving helped Japan and South Korea in the APAC region to register significant growth. Recently, u-blox’s LTE-M modules got certified by KDDI in Japan and LGU+ in South Korea, which also pushed growth.

This year, 81% and 18% of the total revenue came from modules and GNSS chips respectively. u-blox made many design wins for its IoT modules which helped its IoT module business to witness continuous growth.

GNSS module market

u-blox is one of the top players in the GNSS module market. The company shipped nearly 25.3 million units of its GNSS module in 2021. The GNSS module revenue is contributing more than half of the total module revenue. u-blox’s GNSS modules are used a lot inautomotiveapplications.

Some GNSS module design wins for u-blox in 2021:

Xpeng Motors selected u-blox’s F9 high-precision GNSS technology for smart electric vehicles.

Wi-Fi/BT module market

In 2021, u-blox shipped nearly . Most of the u-blox Wi-Fi/BT modules are used in industrial and healthcare applications.

Some Wi-Fi/BT module design wins for u-blox in 2021:

Bluetooth module NINA-B406 used for smart lighting with Douglas Lighting.

u-blox’s ANNA-B112 Bluetooth 5 sip used for a headset for chronic pain treatment with EXSURGO.

u-blox’s NINA-B306 standalone Bluetooth 5 low-energy module used by (greenTEG) CORE to communicate wirelessly.

Cellular IoT module market

According to Counterpoint Research, u-blox’scellular IoT modulesegment grew 12% YoY to reach $125 million in 2021. u-blox accounted for 2% of the global cellular IoT module market whileQuectel, Telit and Thales remained the top three vendors in 2021 in terms of revenue.

The cellular IoT module market remains highly competitive and u-blox has played to its strength while prioritizing GNSS and BT/Wi-Fi module business segments over cellular IoT modules.

u-blox launched 4G Cat 1 module LARA-R6 and 4G Cat 1 bis module LENA-R8 in 2022 to strengthen its cellular IoT module portfolio. With LARA-R6, u-blox wants to target North America, EMEA, APAC, Japan and LATAM markets with applications like telematics, smart meters, point of sales, asset tracking, healthcare and smoke detector. With LENA-R8, it will target EMEA, APAC and LATAM with telematics and asset tracking applications. u-blox is the third player among international (outside China) module players after Sequans and Thales to launch a Cat 1 bis module. We expect these modules to help u-blox regain its share in the cellular IoT module market.

Some cellular IoT module design wins for u-blox in 2021:

Modmo, an e-bike sharing company, used u-blox’s 4G cat 1 module LARA-R211 to provide connectivity in its e-bikes.

Digital Matter preferred u-blox’s 2G module SARA-G350 for its asset tracking device.

GNSS chip market

u-blox shipped nearly 47 million GNSS chips in 2021, which contributed $82 million to the total revenue. Besides using its GNSS chipset in its module, u-blox also provides it to other GNSS module vendors like Navisys and YIC.

Some GNSS chip design wins for u-blox in 2021:

iGPSPORT u-blox M10平台交付使用ltra-long performance for the latest cycling computer.

Market outlook

We expect u-blox revenue to continue to grow more than 20% YoY in 2022 supported by increasing demand from the automotive and navigation segments across all regions. u-blox is on a mission to build its ecosystem with its ‘silicon to cloud’ journey. It wants to use its chipset in its module and connect its module to its cloud platform. u-blox acquired Thingstream, an IoT service platform, in 2020 to provide data and security services to its customers. Further, it took full ownership of Sapcorda, a GNSS augmentation service provider for centimeter-level positioning accuracy, in 2021. These strategic investments are also expected to help u-blox in increasing both product and service revenues, especially in the GNSS segment.

In order to access Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not. Personal Information When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time. In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company. – Passwords are for user’s individual use – Passwords may not be shared with others – Users may not store documents in shared folders. – Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified. Accuracy of Information: While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links: This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience. This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.

This data is based on the smartphone AP/SoC shipments

This data is based on the smartphone AP/SoC shipments

GNSS module market

GNSS module market