Generative AI has been a hot topic, especially after the launch of ChatGPT by OpenAI. It has even exceeded Metaverse in popularity. From top tech firms like Google, Microsoft and Adobe to chipmakers like Qualcomm, Intel, and NVIDIA, all are integrating generative AI models in their products and services. So, why is generative AI attracting interest from all these companies?

While generative AI and ChatGPT are both used for generating content, what are the key differences between them? The content generated can include solutions to problems, essays, email or resume templates, or a short summary of a big report to name a few. But it also poses certain challenges like training complexity, bias, deep fakes, intellectual property rights, and so on.

In the latest episode of ‘The Counterpoint Podcast’, hostMaurice Klaehneis joined by Counterpoint Associate DirectorMohit Agrawaland Senior AnalystAkshara Bassito talk about generative AI. The discussion covers topics including the ecosystem, companies that are active in the generative AI space, challenges, infrastructure, and hardware. It also focuses on emerging opportunities and how the ecosystem could evolve going forward.

OpenAI, Midjourney and Microsoft have set the bar for chargeable generative AI services withChatGPT(GPT-4) and Midjourney costing $20 per month and Microsoft charging $30 per month for Copilot. The $20-per-month benchmark set by these early movers is also being used bygenerativeAI start-ups to raise money at ludicrous valuations from investors hit by the current AI FOMO craze. But I suspect the reality is that it will end up being more like $20 a year.

To be fair, if one can charge $20 per month, have 6 million or more users, and run inference onNVIDIA’slatest hardware, then a lot of money can be made. If one then moves inference from thecloud终端设备,更多的公司是可能的st of compute for inference will be transferred to the user. Furthermore, this is a better solution for data security and privacy as the user’s data in the form of requests and prompt priming will remain on the device and not transferred to the public cloud. This is why it can be concluded that for services that run at scale and for the enterprise, almost all generative AI inference will be run on the user’s hardware, be it a智能手机, PC or a private cloud.

Consequently, assuming that there is no price erosion and endless demand, the business cases being touted to raise money certainly hold water. While the demand is likely to be very strong, I am more concerned with price erosion. This is because outside of money to rent compute, there are not many barriers to entry andMetaPlatforms has already removed the only real obstacle to everyone piling in.

The starting point for a generative AI service is a foundation model which is then tweaked and trained byhumansto create the service desired. However, foundation models are difficult and expensive to design and cost a lot of money to train in terms of compute power. Up until March this year, there were no trained foundation models widely available, but that changed when Meta Platforms’ family of LlaMa models “leaked” online. Now it has become the gold standard for any hobbyist, tinkerer or start-up looking for a cheap way to get going.

Foundation models are difficult to switch out, which means that Meta Platforms now controls anAI标准的,类似于开放的方式AI controls ChatGPT. However, the fact that it is freely available online has meant that any number of AI services for generating text or images are now freely available without any of the constraints or costs being applied to the larger models.

Furthermore, some of the other better-known start-ups such as Anthropic are making their bestservicesavailable online for free. Claude 2 is arguably better than OpenAI’s paid ChatGPT service and so it is not impossible that many people notice and start to switch.

Another problem with generativeAIservices is that outside of foundation models, there are almost no switching costs to move from one service to another. The net result of this is that freely available models from the open-source community combined with start-ups, which need to get volume for their newly launched services, are going to start eroding the price of the services. This is likely to be followed by a race to the bottom, meaning that the real price ends up being more like $20 per year rather than $20 per month. It is at this point that the FOMO is likely to come unstuck as start-ups and generative AI companies will start missing their targets, leading to down rounds, falling valuations, and so on.

There are plenty of real-world use cases for generativeAI, meaning that it is not the fundamentals that are likely to crack but merely the hype and excitement that surrounds them. This is precisely what has happened to theMetaverse的发展这一点并没有改变在哪里ents or progress over the last 12 months, but now no one seems to care about it.

(This is a version of a blog that first appeared on Radio Free Mobile. All views expressed are Richard’s own.)

MediaTek’srevenues were slightly up sequentially but down 43% annually in Q2 2023. Inventory has gradually come down to a relatively normal level, but the demand for智能手机swill remain slow due to the global macroeconomic situation and therefurbished智能手机market. Against this backdrop, MediaTek is diversifying its portfolio by focusing on theauto, smart edge and customASIC segments. The company is estimated to take over two years to get material revenues from these segments.

AI and ASIC Opportunity

CEO:“As for ASIC, we recently see growing enterprise ASIC business opportunities in AI and datacenter markets. With our strong IP and SoC integration capabilities, we aim to continue to grow this business in the future.”

Parv Sharma’s analyst take: “With the growth in generative AI, the demand for edge AI processing has accelerated. Being one of the top players in edge devices, MediaTek is well-positioned to benefit from this shift. The company will focus on winning enterprise ASIC projects but catching up with major players like Broadcom and Marvell will take time, as customers typically work with existing suppliers for repeat projects.”

Growing focus on auto and partnership with NVIDIA

CEO:“We’re very excited about the recently announced partnership between MediaTek and NVIDIA to develop a full-scale product roadmap for the automotive industry. We believe our industry-leading low-power processors and 5G, WiFi connectivity solutions, combined with NVIDIA’s strong capability in software and AI cloud, will help us become highly competitive in the future connected software-defined vehicles market and shorten our time to market to accelerate our growth.”

Shivani Parashar’s analyst take: “MediaTek launched Dimensity Auto to focus on cockpit and connectivity solutions. With its partnership with NVIDIA, the company aims to develop a full-scale product roadmap for the automotive industry. Auto design cycles are long so it will take some time (2026-2027) for the company to increase revenues from this segment. Overall, we can say the auto segment will become a long-term revenue growth driver for MediaTek.”

Customer and channel inventories come down

CEO:“We observed that customer and channel inventories across major applications have gradually reduced to a relatively normal level. Recent demand from our customers has shown certain level of stabilization. However, our customers are still managing their inventory cautiously as global consumer electronics end market demand remains soft. For the near-term, we expect our business to gradually improve in the second half of the year”

Shivani Parashar’s analyst take: “According to our supply chain checks, inventory levels are coming down and will get back to normal in the second half of 2023. OEMs will start restocking but will be cautious due to weak consumer demand and global macroeconomic conditions.”Result summary

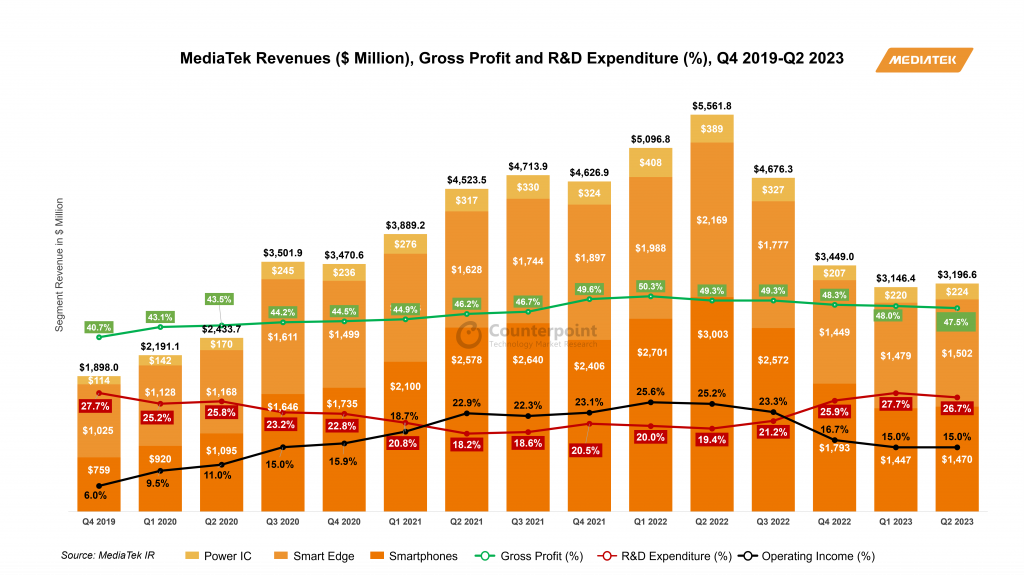

Slight improvement in revenues: MediaTek recorded$3.2 billionin revenues in Q2 2023, a slight increase of 2% QoQ but a decrease of43% YoYdue to the weakglobal demandfor end products and the second-hand smartphone market. Customer and channel inventories across major applications have come down to a relatively normal level.

Maintained mobile segment revenue due to 5G SoCs:The mobile phonesegment contributed 46% to the company’s revenue in Q2 2023, which declined by51%YoY and increased by 2% QoQ. The demand for 5G SoCs improved during the quarter. The new flagship Dimensity SoC will be launched in the coming month.

New opportunities for smart edge:The smart edge segment contributed 47% to the company’s revenue in Q2, growing 2% sequentially. The demand for connectivity remained stable in the quarter. Business opportunities are growing for the ASIC segment.

Price discipline: MediaTek will focus on maintaining gross margin, following price discipline at a time of uncertainty in the global semiconductor industry.

Favorable guidance: MediaTek guided Q3 revenues in the range of$3.3 to $3.5 billion, growing 4%-11% sequentially. Gross margins are expected to be around47%while the operating expense ratio is expected to be around 32% in Q2 2023. The smartphone, connectivity and PMIC segments will see revenue growth. The smart TV segment will witness declining revenues in the third quarter due to excess inventory.

Autosegment is picking up:Automotivewill contribute$200 to $300million to MediaTek’s revenue in 2023. More significant revenue can be seen from 2026. The current auto design pipeline revenue for MediaTek is over $1 billion.

Weaker-than-expected macroeconomicsituationcontinuedto weigh on TSMC’sQ2 2023 business performance.温和smartphone and PC/NB demand negatively impactedtheoverall utilization rateduring the quarter.Though largely expected by the market, the company further cut its full–year revenue guidance ontheweaker end demandexpected forH2 2023.However,TSMCprojects astrong AI demand inQ32023and,going forward,sees itself asthe key enablerfor AI GPUsandASICs that requirealarge diesize.We give ourtakeson the key points discussed during theearnings call:

Is AI semiconductor demand real?

Chairman(Mark Liu):Neither can we predict the near future, meaning next year, how the sudden demand will continue or will flatten out. However, our model is based on the data center structure. We assume a certain percentage of the data center processors areAIprocessors and based on that, we calculate the AI processor demand. And this model is yet to be fitted to the practical data later on. But in general, I think the trend of a big portion of data center processors will be AI processors is a sure thing. And will it cannibalize the data center processors? In the short term, when thecapexof the cloud service providers is fixed, yes, it will. It is. But as for the long term, when their data service – when the cloud services have the generative AI service revenue, I think they will increase the capex. That should be consistent with the long-term AI processor demand. And I mean the capex will increase because of the generative AI services.

Adam Chang’sanalyst take:Supply chain checks reveal that cloud service providers such as Microsoft, Google, and Amazon aggressively invest in AI servers.NVIDIAis continuing to add orders for the A100 and H100 to the supply chain, echoing the strong momentum for AI demand. TSMC holds a significant market share in AI semiconductorwaferproduction, mitigating the risk of misjudging CoWoS capacity expansion concerning AI demand.

Akshara Bassi’s analyst take:Over the medium term, as hyperscalers continue to develop their own proprietary AI models and look to monetize through AI-as-a-Service and simiilar models, the infrastructure demand should remain robust.

Can AI semiconductor demand offset short-term macro weakness?

CEO (Che-Chia Wei):Three months ago, we were probably more optimistic, but now it’s not. Also, for example, China economy’s recovery is actually also weaker than we thought. And so, the end market demand actually did not grow as we expected. So put all together, even if we have a very good AIprocessordemand, it’s still not enough to offset all those kinds of macro impacts. So, now we expect the whole year will be -10% YoY.

Adam Chang’s analyst take:Although there is a lot of promise around AI, it would only account for around 6% of total revenues in 2023. Therefore,AIis not a panacea for broader short-term demand weakness.

Is TSMC CoWoScapacity enough to fulfill current AI demand?

CEO (Che-Chia Wei):For AI, right now, we see very strong demand, yes. For the front-end part, we don’t have any problem to support, but for the back end, the advanced packaging side, especially for the CoWoS, we do have some very tight capacity to — very hard to fulfill 100% of what customers needed. So, we are working with customers for the short term to help them to fulfill the demand, but we are increasing our capacity as quickly as possible. And we expect these tightening will be released next year, probably toward the end of next year. Roughly probably 2x of the capacity will be added.

Adam Chang’s analyst take:Due to TSMC’s CoWoS capacity constraints, the company is finding it challenging to fulfill the strong AI demand from customers,, including NVIDIA,Broadcom, and Xilinx, at the moment. NVIDIA is actively seeking second- source suppliers asTSMClooks to outsource some of its production.

N3E/N3/N2 status

CEO (Che-Chia Wei):N3 is already involved in production with good yield. We are seeing robust demand for N3 and we expect a strong ramp in the second half of this year, supported by both HPC and smartphone applications. N3 is expected to continue to contribute mid-single-digit percentage of our total wafer revenue in 2023. Our N2 technology development is progressing well and is on track for volume production in 2025. Our N2 will adopt a narrow sheet transistor structure to provide our customers with the best performance, cost, and technology maturity.

Adam Chang’s analyst take:Apple is the sole customer expected to adopt TSMC’s 3nm technology in its A17 Bionic and M3 chips during 2023. TheQualcommSnapdragon 8 Gen 4 processor is also anticipated to join the TSMC 3nm family (N3E) in 2024. Moreover, Intel is likely to adopt TSMC’s 3nm technology for its Arrow LakeCPU, scheduled to launch in H2 2024.

Results summary

Q2 2023resultsbeatslightly:TSMC reported $15.67 billion in sales, slightly above the midpoint of guidance. EPS beat consensus due to higher non-operating income. Both GPM and OPM slightly beat guidance thanks to favorable FX and cost control efforts.

Q3 2023guidance in line:The management guided $16.7-$5 billion (+9% QoQ at midpoint), gross margin in the range of 51.5%-53.5%, and operating margin in the range of 38%-40%. The gross margin dilution resulting from the N3 ramp-up would be 2-3 percentage points in Q3 2023 and 3-4 percentage points in Q4 2023. This impact would persist throughout the entire year of 2024, affecting the overall gross margin by 3-4 percentage points. Notably, this dilution is higher than the 2-3 percentage points gross margin dilution experienced during the N5’s second year of mass production in 2021.

2023revenue guidance revised down but expected:TSMC revised down the full-year revenue guidance to -10% YoY. The management sees weaker-than-expected macroeconomics in H2 2023 affecting the demand for all applications except for AI.

Strong AIdemand, 50% revenue CAGR forecast:AI revenue currently makes up 6% of TSMC’s total revenue. The company anticipates a remarkable compound annual growth rate (CAGR) of nearly 50% from 2022 to 2027 in the AI sector. As a result of this significant growth, the AI revenue percentage share in TSMC’s total revenue is projected to reach the low teens by 2027.

CoWoScapacity expected to double by 2024 end:台积电在AI secto正在经历强劲需求r, with sufficient capacity for the front-end part but facing challenges in advanced packaging, particularly CoWoS.It is working with customers to meet demand in the short term while rapidly increasing capacity which it expects to double by the end of 2024, easing the current tightness.

As surely as autumn and winter follow summer, the current exuberance aroundAIis not going to last simply because the machines remain incapable of living up to the expectations that have been set for them.

These cycles typically take the form of a discovery of some description followed by a ramping of expectations which in turn leads to large amounts of money being invested for fear of missing out (FOMO).

The problem is that the expectations that are set are always unrealistic, meaning that when the time comes to deliver on those expectations, disappointment sets in. This is followed by collapsing valuations, bankruptcies and forced consolidation as investors are no longer willing to suspend disbelief.

This is the fourth AI Hype cycle with the others occurring in the 1960s, 1980s and 2017-2019, and this hype cycle looks exactly the same as the others except that it is much larger. Looking at investment activity and news flow, it is also very clear exactly where we are in the cycle.

First, expectations

The ability of Large Language Models (LLMs) to mimic human behavior has convinced some of the big names (like Professor Geoffrey Hinton) that artificial superintelligence is now materially closer than it was before.

While LLMs do have some very useful and lucrative use cases, they still have no causal understanding of the tasks they are performing.

This is why they hallucinate, make the most basic factual errors and are generally completely unreliable.

Therefore, the machines remain as stupid as ever. There is no evidence whatsoever that these machines are able to think.

But the problem is that they are so good at pretending to think that they are able to fool the great minds that created them.

Instead, all they do is calculate statistical relationships, meaning that the big promises that have been made will not be kept.

Second, investment

There are already many examples of money being thrown at start-ups with valuations and fundamentals being an afterthought:

OpenAI’s $30-billion valuation with a corporate culture that doesn’t want to make any profit.

Inflexion AI raising $1.3 billion fromMicrosoftandNVIDIAat an estimated valuation of around $5 billion despite having only been around for a year and having no commercial product.

Mistral AI raising $113 million at a $260-million pre-money valuation despite being only a few weeks old with no revenues, no product and probably only the vaguest idea of what it is going to do.

This can be described as the very definition of a bubble where rationality gets lost in the mad rush toward the next big thing. A lot of shirts are going to be lost.

The latest innovations around LLMs have produced some remarkable abilities which, no doubt, will be put to both good and lucrative use. However, the technology upon which they are based has not changed, meaning that the limitations that preventeddigitalassistants and autonomous driving from being useful for anything more than the most basic tasks are also going to trip LLMs up.

Furthermore, this is no longer the exclusive realm of the big, well-financed companies that can pay tens of millions of dollars for massive compute capacity, as the hobbyists and enthusiasts are now creating generative AI.MetaPlatforms’ series of LLMs called LlaMa are now freely available to anyone who wants to tinker and advances in training techniques have meant that it is possible to fine-tune a 7bn parameter model on a powerful laptop.

This is why there are models popping up all over the place that are completely free to use. Some of them actually work quite well. Hence, the pricing of $20 per month for services likeGPT-4, Perplexity AI and Midjourney may soon come under relentless pressure. This is really bad news for investors relying on spreadsheets for their return because no one seems to have modeled this scenario out.

The first sign of trouble will come when companies come back to the market after spending the money on fancy offices and expensive staff but nothing to show for the investments so far. This is when the down rounds begin, disillusionment sets in, reality makes its presence felt and winter begins.

One suspects this will begin sometime in the first half of 2024 and the fallout will not be pretty.

(This is a version of a blog that first appeared on Radio Free Mobile. All views expressed are Richard’s own.)

NVIDIA and Softbank recently announced that they had developed a dual-purpose AI-driven 5G MEC and vRAN distributed platform based on NVIDIA’s new GH200 Grace Hopper superchip. The two partners intend to deploy a network of regional data centres across Japan later this year to capitalize on the demand for accelerated computing and generative AI services. The shared multi-tenant platform will also offer a range of 5G vRAN applications and Softbank is creating 5G applications for autonomous driving, AI factories, augmented and virtual reality, computer vision and digital twins.

Key Takeaway No. 1: Platform Limitations

Softbank is offering a dual-purpose platform where the main application is AI compute via a high-performance edge analytics platform to capitalise on the expected surge in demand for AI processing capacity. Although the company is also developing a range of 5G applications, the AI and 5G workloads will be offered simultaneously. Counterpoint Research believes that the platform is unlikely to be feasible for vRAN workloads alone and understands that the two partners are not targeting this market.

Key Takeaway No. 2: Leveraging GPU Usage in the RAN

NVIDIA GPU计划利用其处理capacity in the RAN in a number of ways, for example, to improve spectral efficiency. One way of doing this is to apply AI to optimise channel estimation feedback data between a user device and a base station. A compute intensive problem with mMIMO radios, using AI to compress receiver feedback data would reduce signalling overhead, thereby resulting in an useful increase in uplink channel capacity. This could be particularly effective at the edges of a cell. Using its GPUs in this way, NVIDIA claims that it can boost gain for cell edge users by 14-17 dB. Other applications include using AI to optimise beamforming management in millimetre wave mMIMO radios as well as to accelerate Layer 2 scheduling.

The full version of this insight report, including a complete set of Key Takeaways is published in the following report, available to clients of Counterpoint Research’s5G Network Infrastructure Service (5GNI).

Snapshot Key Highlights – 5G MEC Telco Network – Grace Hopper Superchip – Leveraging Software Resources – Performance Details – Use Case and Deployment Options – Key Partners – Competitors Analyst Viewpoint – Platform Limitations – Benefits of RAN-in-the-Cloud – Eliminating RAN hardware dependency – The Intel vs ARM battle – Leveraging GPUs in the RAN – A Crowded Market

Tech giants showcased their most advanced solutions in AI and computing at the COMPUTEX 2023 show in Taipei in the first week of June. If NVIDIA CEO Jensen Huang’s keynote address focused on the company’s game-changing innovations around AI, Arm CEO Rene Haas’ keynote had compelling demonstrations showcasing Arm’s capabilities in AI. Qualcomm focused on on-device intelligence enhancement and Hybrid AI as the mainstream format ofAIin the future. With meaningful upgrades in computing capability, we expect to see the beginning of a new chapter in the coming years. In the following sections, we summarize the key takeaways from COMPUTEX 2023.

NVIDIA: Grace Hopper Superchip to boost AI revolution

The world’s first-of-its-kind Grace Hopper Superchip, which is manufactured by the TSMC 4nm process node, is likely to level up NVIDIA’s determination on AI. In addition, more GPUs will be used for generative AI training and inference models, which willacceleratethe transformative technology in the near term, highlighted Mr. Huang.

Our Associate Director,Brady Wang,shared his ideas and insights at the influential event.

NVIDIA also introduced the Spectrum-X platform, a fusion of the Spectrum-4 switch and Bluefield-3 DPUs, which boasts a record 51Tb/sec Ethernet speed and is tailor-made forAI networks. Combined with BlueField-3 DPUs and NVIDIA LinkX optics, it forms an end-to-end 400GbE network optimized for AI clouds. This innovation not only fits NVIDIA’s target but also consumes a great amount of foundry capacity, especially TSMC.

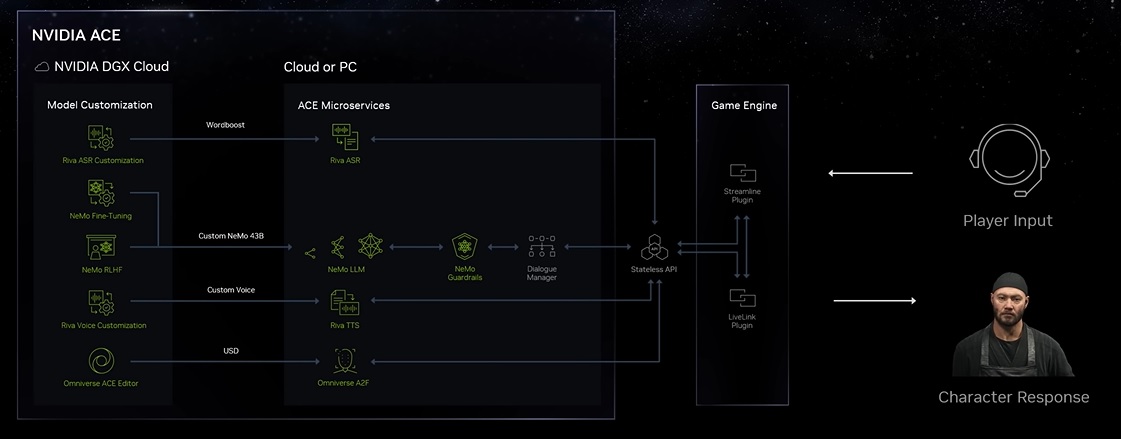

NVIDIA ACE Framework

Source: Nvidia

NVIDIA: Avatar Cloud Engine (ACE) for Games

NVIDIA did not forget its loyal gamers. This time, it introduced the Avatar Cloud Engine (ACE) for Games, a groundbreaking custom AI model service. ACE empowers non-playable characters (NPCs) in games with AI-driven natural language interactions, revolutionizing the gaming experience. With ACE, gamers can enjoy more immersive and intelligent gameplay.

Notes from analyst Q&A with NVIDIA founder and CEO Jensen Huang

If most of the workload involves training AI models, the data center operates as an AI factory. An optimal computer is capable of handling both training and inference tasks, although the selection of processors is contingent upon the specific inference type.

In the foreseeable future, AI is poised to become the predominant force within the realm of NPCs in video games. These NPCs will possess a distinctive narrative and contextual background, effortlessly engaging with one another in a harmonious manner. Their movements will be fluid and their comprehension of instructions will be exceptional.

AI revolutionizes the user experience onPCs, propelling the advancement of personalized recommender systems. Furthermore, even on compact smartphones, it taps into extensive personalized internet data. As a result, future interactions generate real-time, customized content, transitioning towards generative processing to accommodate the escalating demand for personalized information. This groundbreaking development signifies the dawning of a new era characterized by the proliferation of generated and augmented information, thereby departing from the previously dominant retrieval-centric paradigm.

InfiniBand excels in high-performance computing, offering superior throughput for single computers and AI factories. It dominates in supercomputers and AI systems, while Ethernet is prevalent in cloud environments.

China leads the way in cloud services, consumer internet and digital payments. It has swiftly advanced in electric and autonomous vehicles, showcasing local innovation through numerous GPU start-ups. This underscores China’s technological dominance and promising future growth.

Omniverse streamlines computer setup with cloud integration and partnerships, enabling effortless information streaming through browser-based access. It optimizes factory design and simulation, minimizing work, errors and expenses.

Arm: Everything now is a computer; AI runs on Arm

Citing the remarkable 260% increase in data center workloads from 2015 to 2021,ArmCEO Rene Haas emphasized the pivotal role of data centers, automotive technology and AI in driving the compute demand powered by ARM designs.

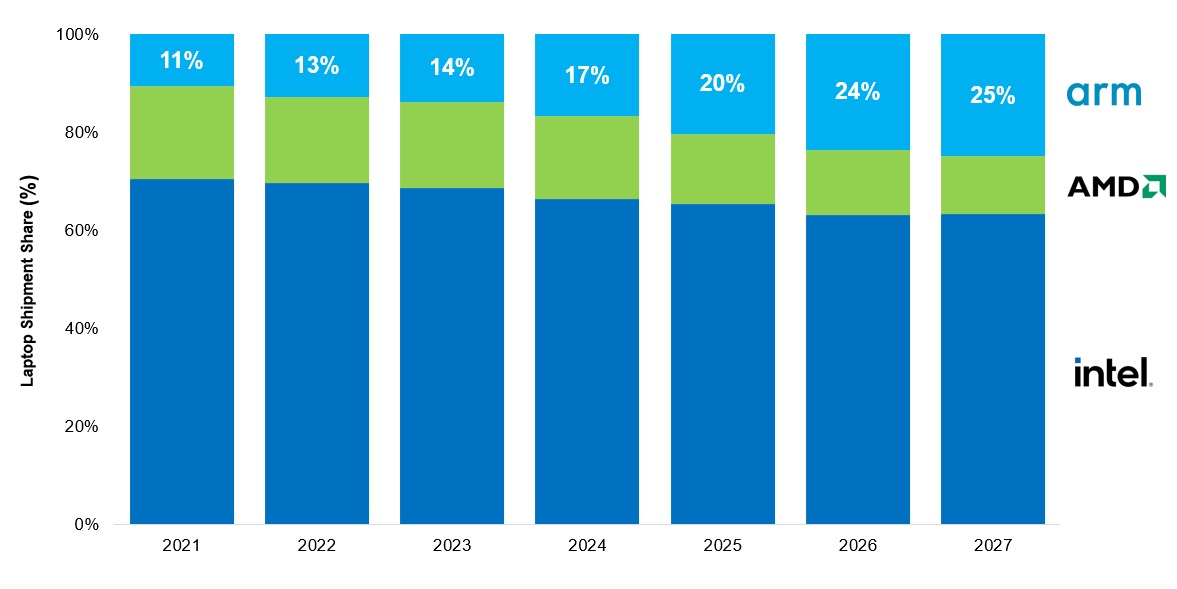

According to Counterpoint Research,Arm-based notebookswill gain over Intel and AMD, almost doubling their shipment share to 25% by 2027 from 14% today.

Laptop Shipment Share by CPU/SoC Type %

source: Counterpoint Research

AI emerged as a focal point during Haas’ keynote, where he captivated the audience with compelling demonstrations showcasing Arm’s capabilities. That said, Arm is poised to support an even broader range of applications in the future.

We also echo Arm’s view and believe that generative AI, digital twins and edge computing will emerge as top technology trends in 2023 and affect the whole tech industry.

Qualcomm: Focus on on-device intelligence enhancement, Hybrid AI

Qualcomm’s “AI” Hexagon processor offers 3-5 times better computing performance compared to existing CPU/GPU solutions. The company aims to expand the application of its Snapdragon 8cx Gen 3 processor to the laptop industry with thorough support from Microsoft.

For AI, Qualcomm believes there are limitations to the efficiency improvements of Edge AI or Cloud AI. However, leveraging Qualcomm’s connectivity solutions and combining edge AI with cloud AI can provide incremental benefits in terms of cost/energy savings, privacy and security enhancements, reliability, and latency. Therefore, the company guides that Hybrid AI (Edge AI + Cloud AI) will be the mainstream format of AI in the future.

Conclusion

With the COVID-19 pandemic loosening its grip,COMPUTEXwas back in its on-site mode this year in Taipei with solid and eye-catching AI solutions. We are stepping into a newcomputingera, with generative AI set to transform our lives. Not only server vendors and data center hyper-scalers, but mobile and PC vendors are also working together to facilitate technology improvements with AI support.

Counterpoint’s analysts continue to work closely with the tech product market to monitor all changes and trends.

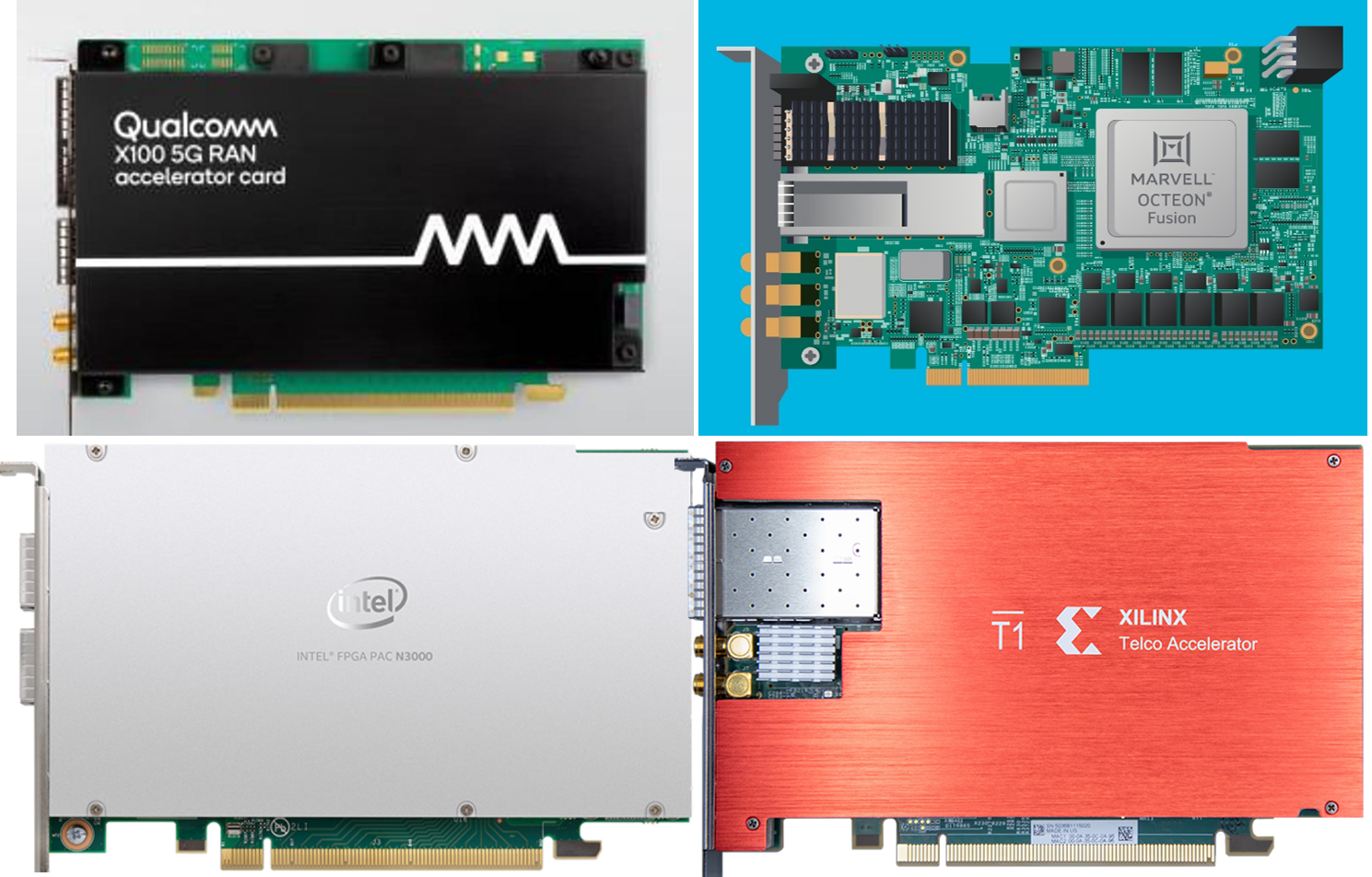

The transition of the Radio Access Network (RAN) from a standalone, integrated network into a disaggregated, virtualized solution is well underway. However, all open RAN deployments to date rely on Intel’s x86-based COTS servers, with most deployments also using Intel’s proprietary FlexRAN软warearchitecture. Recently, various silicon vendors have announced that they are developing alternatives to Intel’s x86 platform based on ASICs, GPUs as well RISC-V architectures. Several of these vendors are currently testing their new PCIe-based Layer-1 accelerator cards with CSPs and commercial versions of these products are expected to become widely available during the next three years.

Thisreportprovides an overview of the emerging open RAN PCIe-based Layer-1 accelerator cardmarketbased on new merchant silicon and highlights the opportunities and technical challenges facing the open RAN chip community as they strive to develop alternativechipsolutions capable of efficiently processing real-time, latency-sensitive Layer-1 workloads.

Key Takeaway No. 1: Too much diversity?

The launch of new L1 accelerator cards from various vendors, large and small, should be welcomed by CSPs calling fordiversityand will go some way to quell criticism that the openRANmarket is too Intel-based. However, CSPs may now be faced with another dilemma – too much choice! They must now face the difficult challenge of testing and comparing multiple accelerator cards, inevitably involving complicated technical and commercial trade-offs.

Key Takeaway No. 2: Look-Aside or In-Line Accelerators?

At present, the choice ofacceleratorarchitecture is binary: either look-aside or inline. Both types have their advantages and drawbacks. Depending on use cases and applications, Counterpoint Research believes thatoperatorsmay need to use both types of accelerators. However, only one vendor currently offers a software/silicon platform with the capability to do this.

Key Takeaway No. 3: Interoperability and Vendor Lock-In

Developing commercial-grade Layer 1 software suitable for massive MIMO networks is an expensive process requiring very specific skills and a lot of experience – but with no guarantee of commercial success. Although openRANis designed to promote interoperability and vendor diversity, all L1 stacks are currently tied to the underlying silicon architectures and hence are not portable between hardware platforms. This introduces a new form of vendor lock-in for CSPs. Clearly, there is an urgent need for an universal software abstraction layer between the L1 stack and the various hardware platforms to enable stack portability.

The complete versions of these Key Takeaways, including the full set of Takeaways is published in the following report, available to clients of Counterpoint Research’s5G Network Infrastructure (5GNI) Service.

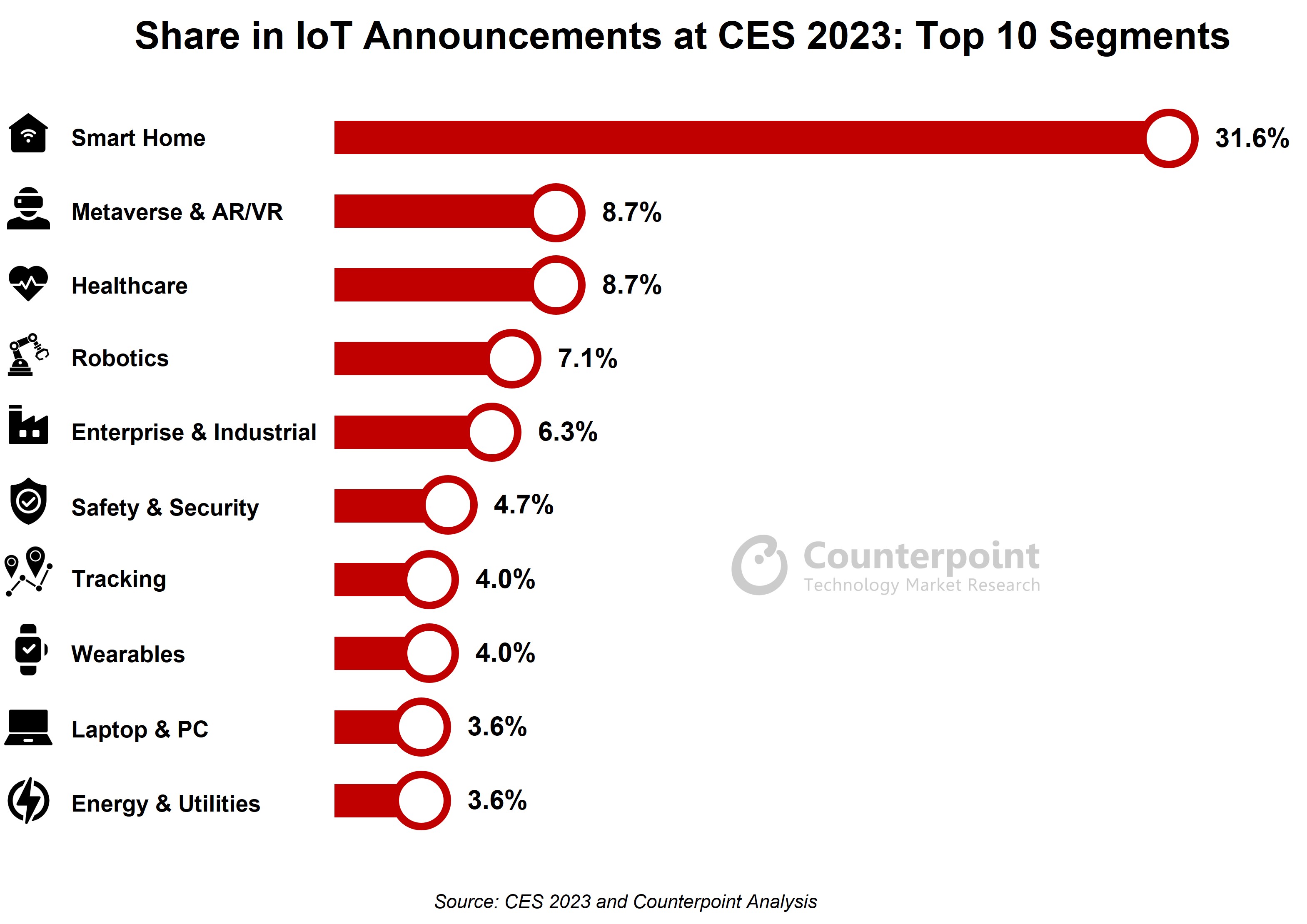

At the first full-fledgedCESevent after the pandemic, the excitement was palpable. Theevent没有让人失望的各种伊斯兰教纪元呢uncements across the internet of things (IoT) spectrum. Our teams, both on-ground and online, tracked over 260 announcements made by over 240 companies covering a range of segments across consumer, enterprise and industrial.

Devices formed the most popular category, with three out of every five announcements relating to this segment. As expected, the consumer and smart home sectors took center stage, but it was intriguing to see new launches in industry segments such as agriculture. Additionally, smart home, metaverse, augmented reality, healthcare and robotics were among the most talked about segments, attracting large crowds.

Here are the top 10 IoT announcements from this year’s CES, according to Counterpoint analysts:

MediaTek introduced the Genio 700 IoT chipset targeting industrial, smart home and smart retail applications. This chipset will be available by Q2 2023. MediaTek also showcased Wi-Fi 7-supported products like gateways, mesh routers,televisions, streaming devices, smartphones, tablets and laptops partnering withTP-Link,Lenovo, Hisense, ASUS, BUFFALO INC, Skyworks, AMD, Qorvo, LitePoint and MAC MLO among others.

MediaTekis slowly diversifying its offerings beyond smartphones. The availability of products with superior capabilities and increased partnerships will help MediaTek increase its footprint in the IoT market.

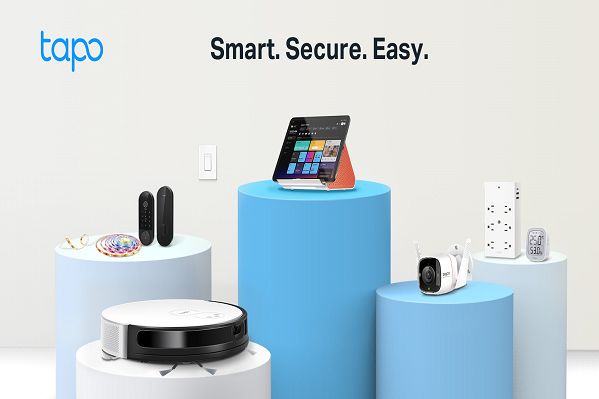

2.Smart Home:TP-Link expands Tapo smart home products

TP-Link unveiled new products under its Tapo line of smart home devices. These new additions include cameras, a doorbell camera, a smart video door lock, robot vacuums and a smart hub home connection center. Besides, the company also launched its first Matter-certified smart plugs, smart switches, smart outlet extenders and smart bulbs. The launch of these products at CES 2023 highlights TP-Link’s focus on expanding and diversifying its offerings in the smart home market.

The company’s adoption of the Matter protocol for its Tapo and Kasa lines of smart home products shows its commitment to making smart home technology more accessible and user-friendly.

In addition to the smart home products, TP-Link also showcased Wi-Fi 7-supported router and gateway solutions for use in homes, enterprises and ISPs. The integration of Wi-Fi 7 will improve the gaming experience, as well as increase productivity in enterprise applications.

3.Asset Tracking:Pod introduces paper-thin tracker with SODAQ, Lufthansa

Pod Group, in partnership with SODAQ and Lufthansa Industry, has developed a paper-thin smart labeltrackingdevice that utilizes low-power cellular connectivity (LTE-M) for a battery life of up to six months. This sustainable, eco-friendly device uses alkaline batteries instead of lithium and has the potential to revolutionize the tracking and logistics industry by improving supply chain efficiency and reducing operational costs.

Similar efforts by SODAQ with Vodafone and Bayer utilizing NB-IoT technology have been observed, but the use of Low Power Wide Area Network (LPWAN) may be more beneficial as it targets a wider range of telecommunications operators.

Bosch Group subsidiary Bosch Sensortec presented a variety of new sensors at CES 2023. These offerings include an AI-enabled smart sensor system, magnetometer, barometric pressure sensor, and an air quality sensor. These sensors demonstrate advancements in power efficiency, accuracy and compact size, and aim to enhance the user experience by tracking personal health and fitness, providing accurate data and prolonging battery life.

Bosch has been a leading manufacturer of micro-electromechanical system (MEMS) sensors since 1995 and has produced over 18 billion units to date. It is also investing in quantum sensors, which can provide measurements that are significantly more precise than current MEMS sensors and enable more accurate diagnosis of neurological diseases. Additionally, the company is developing angular rate sensors that use the nuclear magnetic resonance of noble gas atoms and are optically pumped. These could prove to be highly precise and stable for navigation applications. Bosch believes that sensors will play a key role in IoT and continues to make investments in this area.

Quectel is partnering with Skylo to integrate satellite connectivity into its 5G-ready BG95x/BG77x series of LPWA modules. This hybrid connectivity solution improves network coverage and makes it ideal for a variety of applications, such as trackers, wearables, smart cities and smart meters. Low-earth orbit (LEO) satellites are going to be a key for the non-terrestrial networks (NTN) coming up in 3GPP Rel17/18 in addition to the high-altitude platform system (HAPS).

Quectel also launched the AG59X series of automotive-grade5G modulesbased on Qualcomm’s SA525M platform to supportautonomous driving. The company has strong partnerships with Chinese automakers such as Li Auto, Nio and BYD, and this module will further strengthen its efforts to increase share in the automotive connectivity market.

6.AR/VR:Thundercomm unveils XR2 VR HMD, 5100 AR glasses and smart vending machine

Thundercomm Thundersoft之间的合资企业nd Qualcomm, unveiled a VR HMD solution based on the Snapdragon XR2 platform and AR glasses based on the Snapdragon W5 platform. These products will not only provide flagship experience but also offer low power consumption, higher resolution and more wear comfort. The AR/VR space is heating up with the increased participation from leading technology and smartphone players such as Meta, Apple, HTC and Google. However, an early entry can be beneficial for Thundercomm.

The newly launched smart vending machine will help increase operational efficiencies for retailers. Moreover, this solution will improve the shopping experience and further extend retailers’ reach. Thundercomm is expanding its product lines to capture maximum value from both the consumer and enterprise IoT markets.

Autel Robotics has unveiled a new drone, the EVO Max 4T, which is capable of a variety of applications such as autonomous navigation, semi-autonomous flight missions, firefighting, and inspections. It is equipped with three high-quality cameras, capable of capturing footage from a distance of 1.2 km. Autel has also released the Dragonfish NEST infrastructure, which supports automated eVTOL systems, and the EVO NEST infrastructure, which can operate in all weather conditions.

Drones and eVTOLs will see higher adoption in the future with better efficiency in power consumption, security improvements and better regulatory compliances. These innovations will help Autel increase its presence in the enterprise market and remain competitive with companies like DJI.

8.Industrial IoT:ZVISION partners NVIDIA to improve industrial sensing

ZVISION, a provider of solid-state MEMS LiDAR solutions, is working with NVIDIA to use its robotics simulation platform Isaac Sim to develop advanced robot sensing capabilities and provide high-performance LiDAR solutions.

In Industry 4.0, robotics and simulation will play a key role. Its partnership withNVIDIAwill allow ZVISION to expand its applications beyond vehicles, while also reducing costs and speeding up time-to-market for companies undergoing digital transformation. ZVISION offers both short- and long-range LiDAR options that can be tailored to various applications.

9.Platform:Tuya pushes PaaS 2.0, Cube for digital transformation

Tuya officially launched PaaS 2.0 to develop personalized solutions to fulfill global customers’ demands for “product differentiation and independent control”. For private cloud customers, it also unveiled Cube, an enterprise-levelIoT platformdeployment solution.

PaaS 2.0 is a unique innovation that can assist customers in reducing R&D costs and increasing product competitiveness. Tuya is focusing on public and enterprise cloud applications which are dominated by big cloud players like Alibaba cloud and Tencent cloud.

10.Healthcare:OMRON launches blood pressure monitor with ECG

OMRON introduced a new upper-arm blood pressure monitor with built-in ECG capabilities. This device aims to facilitate the early detection of heart disease by combining blood pressure monitoring and ECG technology. Utilizing home-monitored data, healthcare professionals will be able to provide early treatment and detect Atrial Fibrillation (AFib) at an early stage.

The company also announced the expansion of its digital healthcare apps with new features, such as the Personal Heart Health Coach and the Care Team within the OMRON Connect app. These new features will utilize AI technology to analyze vital data and provide patients with personalized guidance and exercise advice. OMRON’s innovative solution, leveraging technologies like AI, ML andIoT, will help healthcare professionals to better understand patient data through analysis.

Conclusion

CES 2023为我提供了丰富的精神食粮ndustry executives. Each of the announcements made at the event has significant implications for the direction of the industry. For example, the satellite-related announcements made by chipset and module players could help IoT companies focus on new use cases. Additionally, with Wi-Fi 7 becoming mainstream and Matter-certified home products being rolled out, we can expect to see a significant uptick in demand for smart home products. These developments and more continue to shape the future of IoT and solidify the role technology plays in our daily lives. With more innovation, the possibilities are endless and we are excited to see how the industry will continue to evolve.

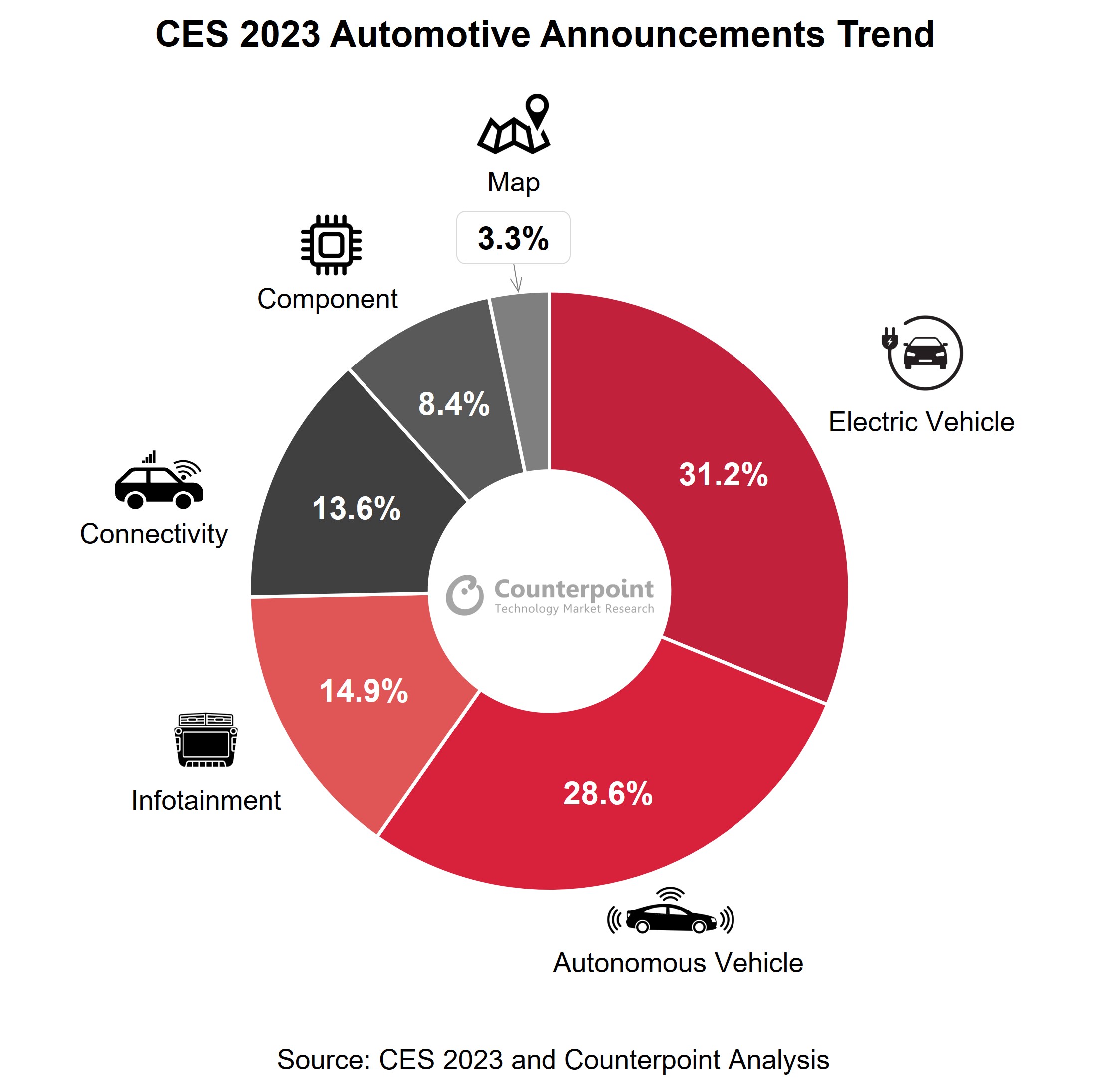

The annual Consumer Electronics Show (CES), held in Las Vegas from January 5 to 8 this year, focused primarily on theautomotive,IoT, smart home, healthcare, metaverse andXR, AI and computing segments. Counterpoint’s automotive team analyzed over 150 automotive-related announcements during CES to identify key trends. The main focus of the automotive industry at this year’sCESwas on electric vehicles (EV), followed byautonomous vehicles, infotainment,connectivity, components and maps. There was a lot of excitement surrounding autonomous vehicles at the event, but EVs accounted for the biggest share of news flow.

Here are the top 10 automotive announcements from this year’s CES, according to Counterpoint analysts:

1. Qualcomm unveils Snapdragon Ride Flex SoC to bring软ware-defined vehicles to reality

Qualcomm announced the Snapdragon Ride Flex SoC, a disruptive solution for expanding its low-power, advanced computing capabilities into the automotive space as part of its Snapdragon Digital Chassis initiative. This solution is built on a heterogenous compute architecture that addresses multiple workloads and is pre-integrated with the Snapdragon Ride Vision Stack. This gives automakers the flexibility to use the Ride Vision Stack across all vehicle tiers without sacrificing performance. In addition, its cloud-native architecture enables a smooth workflow for software development and deployment. The Snapdragon Ride Flex SoC is expected to go into production by 2024.Qualcommis striving to maintain its leadership position in the software-defined vehicle era and make the transition easier for automakers and tier-1 suppliers.

For a more detailed report on CES 2023’s automotive announcements, click here:

2. Sony Honda Mobility introduces Afeela EV brand

Sony Honda Mobility finally announced its JV brand Afeela, which will bring its first EV model to North America in 2026 followed by Japan and Europe. Afeela’s first production model was teased at CES 2023. Sony and Honda announced their JV back in March 2022. Afeela will introduce a series ofEVmodels that will carry Sony’s expertise in IVI systems, ADAS components and in-cabin electronics, while Honda will contribute to the brand’s performance with its e-powertrain system as well as battery sourcing and charging capabilities. According to the announcement, Afeela aims to offer better vehicles at a relatively lower cost. These EVs are expected to be positioned above Honda’s own EVs, but whether Afeela will share the same slot with Honda’s premium Acura brand is yet to be determined.

3. BMW previews next-gen color-changing concept with ‘digital emotional experience’

BWM previewed its next-gen 3 series concept model based on the Neue Klasse platform. The new i Vision Dee concept (Dee stands for ‘digital emotional experience’) showcased a monolithic exterior styling that can be divided into 240 different segments. The whole exterior can support different design styles like stripes, patterns and animation, and can curate up to 32 different colors. Though detailed specifications have not been shared, i Vision Dee features a new OS and a new fully controllable HUD with windscreen projection. Traditional infotainment has been removed. The dashboard conceals various touch sensors which can be used to display content on the HUD. The model will be powered by BMW’s sixth-generation EV powertrain and is expected to enter production in 2025 as a BMW i3 successor.

4.大众展示新ID.7裹着电工实习oluminescent camouflage

Volkswagen showcased its sixth all-electric ID model, the VW ID.7, wrapped in special QR code-inspired camouflage to hide the final styling. The camouflage was inspired by electroluminescent technology which lights up 22 different sectors of the car. Volkswagen disclosed some technical details before the model’s final reveal during the second quarter of 2023. Initially, the ID.7 will have a 77kWh battery pack and a claimed 700-km range. The interior will feature a 15-inch touchscreen infotainment system, an AR-based HUD and a smart HVAC system that can automatically modify the cabin temperature when the key fob is close. Volkswagen expects its new model will compete with Hyundai’s Ioniq 6 and Tesla’s Model 3.

5. LG, Magna form second JV for ‘executable’ autonomous driving, infotainment solutions

Two of the biggest tech companies LG and Magna have again joined hands to develop solutions for automated driving by leveraging their areas of expertise. LG and Magna already have a JV that manufactures e-powertrain and other hardware like inverters, motors and onboard chargers for EVs. The new JV will explore theADASand AV market to develop “executable” automated driving and infotainment solutions to enhance customer experience by addressing the toughest challenges. LG’s vehicle component arm has been eyeing new openings in the automotive market and believes the increased connectivity of cars of the future presents new opportunities.

6. Harman aims to make driving assistance more intuitive, safer

Harman is all set to deliver enhanced in-cabin safety and awareness through its AR-based HUD hardware and AR-based software products. Harman has been a trusted name for vehicle audio for decades but now as the automotive industry makes a transition towards software-based experiences, the company has developed its own technology that enhances the drivers’ experience by bridging the gap between physical and digital worlds in a non-intrusive manner through its AR-based HUDs. Harman’s Ready Vision uses ML-based 3D object detection and computer vision to deliver collision warnings, lane departure, low-speed zone notification, blind spot warnings and lane change assist with high precision without breaking the driver’s concentration. Harman claims Ready Vision works with precision even in the most unfamiliar driving scenarios, making driving safer.

7. BlackBerry has a busy CES with launches, partnerships

BlackBerry’s IVY software platform, developed in collaboration with Amazon, won its first design contract with PATEO for the all-electric VOYAH H97 model’s digital cockpit. BlackBerry also launched QNX Accelerate, which supports the QNX RTOS and QNX OS for safety in the AWS marketplace. Leading tier-1 suppliers like Continental and Marelli are already testing it to create automotive metaverse environments for software-defined vehicles. BlackBerry is partnering with Elektrobit to develop automotive safety solutions using the Rust programming language. It has also formed partnerships with Texas Instruments for embedded software development and with Garmin for improving the in-car experience. These partnerships show that BlackBerry is attempting to regain market presence through its infotainment, security and OS products.

8.Innoviz推出新的激光雷达,形成多个部分nerships

Innoviz, a leading player in solid-stateLiDARsensors and perception software, unveiled the Innoviz360, a cost-effective and high-performance LiDAR that will support a range of non-automotive applications such as smart cities, logistics, maritime, heavy machinery, and construction, in addition to Level 4-5 (L4 and L5) autonomy applications. Loxo, a zero-emission autonomous vehicle provider for last-mile delivery, has partnered with Innoviz to use the InnovisOne LiDAR. Deep-tech company EXways, which works in 3D LiDAR processing, has also partnered with Innoviz to leverage the technology for multiple applications.

Innoviz has previously formed partnerships with major automakers such as BMW and Volkswagen, as well as tier-1 supplier Magna. At CES, Innoviz also showcased the InnovizTwo LiDAR, which it claims offers a 30x performance improvement over the InnovizOne and a 70% cost reduction. With the growing adoption of autonomous vehicles, LiDAR technology is expected to be high in demand as major auto OEMs including Mercedes-Benz, Nissan, BMW, Stellantis, Volkswagen and Volvo plan to use it.

NVIDIA is partnering with Hyundai Motor, BYD and Polestar to offer a cloud gaming experience through itsNVIDIAGeForce NOW service for cars. GeForce users will be able to access over 1,000 paid and free games through this service. While video games are not new in cars, the addition of GeForce will provide a more PC-like gaming experience. This will also drive the trend of cellular connectivity in the passenger vehicle market, as cloud gaming will require embedded 4G or 5Gconnectivity.

10. Google launches HD maps, partners with Volvo, Polestar

Google announced that it would make HD maps available for Level 2+ autonomous vehicles. The Volvo EX90 and Polestar 3 will use Google’s HD maps service in addition to Google’s Android Auto solution. While Google is gaining some traction in the automotive sector through its Android Auto offerings, it will face strong competition from existing players like HERE and TomTom whose offerings in HD maps and other related services are helping them maintain leadership in thelocation platformmarket. To compete with these leading players and local players like Amap, Navinfo, Naver, MapmyIndia and Zenrin, Google is seeking to enhance the user experience in this segment.

In order to access Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not. Personal Information When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time. In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company. – Passwords are for user’s individual use – Passwords may not be shared with others – Users may not store documents in shared folders. – Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified. Accuracy of Information: While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links: This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience. This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.

Result summary

Result summary